What are Qualifying Earnings for Auto Enrolment?

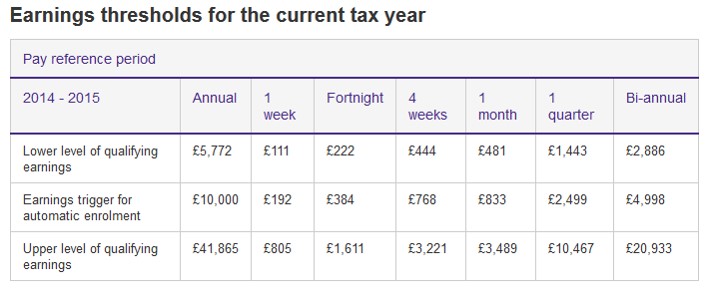

These are defined as sums which you pay to an employee in connection with his or her employment. They can be salary, wages, commission, bonuses, overtime. Statutory sick pay and maternity/paternity/adoption pay are included too. Benefits in kind (known as P11D benefits), for example, car and fuel, and tips and gratuities do not have to be included. In 2014/2015 Qualifying Earnings are earnings between £5772 and £41,865.

Employers are only required enrol employees earning over the Earnings Trigger of £10,000 (subject to age criteria) but employees can opt in once they earn above the lower level. According to Payroll and Benefits Magazine...

The AE process can be very administration-heavy and, unlike Real Time Information, employees and workers will have to be continually assessed. For example, employers will need to continuously monitor their workforce to identify when a jobholder must be automatically enrolled. In particular, the employer will need to monitor a worker’s age because this may trigger AE and opt-in activity.Although small employers will need at least six months before their staging date to prepare for AE, larger ones may need between 12 and 18 months.AE does not only apply to employees, but also to workers, including contractors who provide services on a personal basis but not as a company.

Can you cope with Auto Enrolment?

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was.

58% had not set up an auto-enrolment pension scheme.

90.5% of employers without an auto-enrolment pension scheme hadn’t even started researching one.

If you think you can ignore Auto Enrolment, think again, The Pensions Regulator will make you comply……..

Non-statutory action

We can issue guidance and instruction by telephone, email, letter and in person. Or we can send a warning letter confirming a set time frame for compliance with the duties.

Statutory notices

Statutory notices can direct you to comply with your duties and / or pay any contributions you have missed or are late in paying. We have further discretionary powers which allow us to estimate and charge interest on unpaid contributions and direct you to calculate and / or pay unpaid contributions.

Penalty notices

We can issue penalty notices to punish persistent and deliberate non-compliance.

A fixed penalty notice will be issued if you don’t comply with statutory notices, or if there’s sufficient evidence of a breach of the law. This is fixed at £400 and payable within a specific period.

We can also issue an escalating penalty notice for failure to comply with a statutory notice. This penalty has a prescribed daily rate of £50 to £10,000 depending on the number of staff you have.

We can issue a civil penalty for cases where you fail to pay contributions due. This is a financial penalty of up to £5,000 for individuals and up to £50,000 for organisations.

Where employers fail to comply with a compliance notice or there is evidence of a breach, we can issue a prohibited recruitment conduct penalty notice. This is currently set at a maximum fixed daily rate of £5,000 for organisations with over 250 staff. We aim to fully recover all the penalties that we issue.

Court action

We can take civil action through the court to recover penalties.

Employers who deliberately and wilfully fail to comply with their duties may be prosecuted.

We can also confiscate goods where there is a criminal conviction and restrain assets during criminal investigations.

The first case was Dunelm http://www.thepensionsregulator.gov.uk/docs/section-89-dunelm.pdf

Research shows that Accountants are most likely to be asked to help SME’s and Business Accountant (a service provided by CIMA Members in Practice) have created a booking service to assist SME’s in getting help https://business-accountant.com/auto-enrolment/

So don’t be scared by Auto Enrolment, don’t delay drawing up a project plan, take action now to avoid problems with the Pension Regulator later!

steve@bicknells.net

Working on it or in it?

I often hear people say ‘I am working really hard but my business seems to be stagnating’, this is probably due to working in rather than on the business. For a business to be successful, you need to focus on your strategic goals, and take steps to achieve them.

As business owners of small and medium sized enterprises, we often get pulled into the nitty gritty of running our businesses on a day to day basis. It could be dealing with a customer issue, or a staff management issue or purely a product or service review. It is really hard to take yourself out of your day to day management role and review the strategy and direction of your business. However it is critical to do this on a regular basis, ideally weekly or monthly, but here at KMA Accountancy would certainly recommend half yearly or quarterly at the very least.

Once a week we meet with fellow business owners and discuss areas of our business that we want to improve, we block out a couple of hours in our diaries, sit down in a quiet meeting room, and discuss the business issues that are keeping us awake or causing us pain and bounce ideas off each other. This enables us to come up with a clear strategy to implement to remove this obstacle from our path.

It’s all too easy to get lost in the day to day work, to put off these meetings, but it’s really important in moving the business on to where we want it to be. It’s all about taking time out to focus on the bigger picture. It’s easy to do, but it’s also easy not to do. It’s the constant small step changes that makes a massive impact over time.

Here at KMA Accountancy we like to practice what we preach, we do this process with our clients. We meet with our clients and discuss what is their really pressing burning issues that are worrying them and keeping them awake at night. We discuss the issues and help them to come up with a strategy for overcoming them and making those step changes in their business, be it improving systems to free up more time, increasing your marketing reach and getting more sales, increasing sales , increasing overall profitability in the business down to delegating more, outsourcing or advising on staffing issues and incentives.

I would definitely recommend setting aside a couple of hours with your accountant to bounce ideas off and help you to get clear in your mind how to move your business on and achieve what you want from it, before even more time just flies by.

Good luck in working on your business. If I can help then please feel free to contact me.

Kim Marlor http://www.kimmarlor.co.uk

photo credit: <a href=”http://www.flickr.com/photos/42931449@N07/6812497415/”>photosteve101</a> via <a href=”http://photopin.com”>photopin</a> <a href=”http://creativecommons.org/licenses/by/2.0/”>cc</a>

Would your Suppliers like to be paid faster?

Yes of course they would, silly question, everyone wants to be paid faster but how can it be done?

Santander may have the answer, they are offering a facility to SME’s called Supplier Payments and its part of the Funding for Lending Scheme.

Supply Chain Finance has been around for a while, this an extract from an article in the Telegraph in October 2012

Supply-chain finance, which is sometimes known as “reverse factoring”, allows big businesses to notify a bank as soon as a supplier’s invoice has been approved. The bank, armed with the assurance the bill will be paid, will then extend a full, immediate advance of the bill to the supplier at a low interest rate.

The Prime Minister hailed the technique as “win-win” because large companies get greater protection from small suppliers going bust, while the small business avoids having to wait for payment and, since the invoice is approved, avoids any risk of non-payment.

Most of the main banks have solutions for large businesses but it isn’t normally available to SME’s.

Is this an option for your suppliers?

steve@bicknells.net

When will my business Stage for Auto Enrolment?

Your staging date is the date the new duties come into force for your business. It’s the date from when automatic enrolment activities must become ‘business as usual’, just like real-time PAYE.

You can find out your staging date using the Pension Regulators Calculator or this link provides a quick summary by number of employees.

Auto Enrolment isn’t easy, there is a lot to do before you Stage, here is a checklist (Pension Regulator) of activities you should do 6 months before Staging

Modified staging dates for some small employers

- You can change your staging date to a later date if you:

- had fewer than 50 staff on 1 April 2012, and

- had, or were part of, a PAYE scheme that has more than 50 people in it.

Bringing your staging date forward

All employers are able to bring their staging date forward. You may choose to do this to align it with other business practices, like the start of your financial year.

Or you might have several employers in a corporate group and want to align the smaller employers’ staging dates with the largest. If you plan to do this, you must notify The Pensions Regulator, which you can do online.

You can postpone assessing your workforce for up to 3 months, but this does not change your staging date and staff can choose to opt in during the postponement period.

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope with the preparation for Auto Enrolment and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was!

Do you have a Second Income? own up now!

On the 9th April 2014 HMRC launched the Second Income Campaign….

A second income could come from:

- consultancy fees, eg for providing training

- organising parties and events

- providing services like taxi driving, hairdressing or fitness training

- making and selling craft items

- buying and selling goods, eg at market stalls or car boot sales

You need to tell HM Revenue and Customs (HMRC) if your additional income hasn’t been taxed through either:

- your main job

- another Pay As You Earn (PAYE) scheme

- Self Assessment

This is called a ‘voluntary disclosure’. To get the best possible terms you need to tell HMRC that you want to take part in the campaign.

You’ll have 4 months to calculate and pay what you owe.

You can find out about the campaign and how to make a disclosure here

The criteria used to assess if an activity is a hobby or a business are:

- The size and commerciality of the activity.

- The frequency of the activity and transactions

- The application of business principles.

- Whether there is a genuine profit motive.

- The amount of time devoted to the activities.

- The existence of arm’s-length customers (as opposed to just selling your wares to family and friends).

If you have a Second Income its better to disclose it now rather than wait till HMRC find you.

Get HMRC to pay you

HMRC will pay you interest

It is not that well-known that HMRC will pay you interest on tax paid early. The interest rate is only 0.5% though, so it isn’t going to change your life.

In the case of Corporation Tax, any payment is due 9 months and a day after your year-end. If you have a business bank account that pays no interest and the cash to pay your tax early you can pay your tax as soon as you have filed your return. After the 9 months is up HMRC will send you the interest calculated.

What spare cash?

See my earlier post on paying your debts first. In the situation where you have cash in the bank that you aren’t putting to good use and no outstanding debts paying your tax liability early will yield a small benefit.

Get your tax return done early

It is difficult to plan your cash flow if you don’t know how much tax you are due to pay. Even if you don’t want to pay your tax early, it is helpful to know how much cash you will need to set aside. The later you leave it to file your tax return the more pressure you can end up putting on your cash flow. More importantly the later you leave it, the more pressure you put on your accountant. Most accountants increase their fees as tax deadlines approach – or to put it another way you are likely to get a discount for starting early!

Don’t be late!

It won’t surprise anyone that HMRC will charge interest on late payments. The interest rate isn’t the measly 0.5% mentioned above but is currently 3%. As Bank of England rate increases – expect this to increase too!

For support and advice on preparing your annual accounts and filing your tax returns contact Alterledger or visit the website alterledger.com.

Read all about it!

It is now 6 months since I started writing and distributing my newsletter Bright Business Bulletin and I have certainly learned a lot along the way.

I came up with the idea of producing a monthly printed newsletter at the Entrepreneur’s Convention back in September. Two clear messages of the Convention were that doing what every on else was doing was not a sensible way to stand out in business, and that if you have an idea you should act on it quickly. A perfect idea which is not put into action is worthless. However, an imperfect but relevant idea that comes to fruition will move you forward.

I have always liked the idea of producing a newsletter with genuinely useful information. I felt that sending out an e-newsletter would not be the best use of my time as most people receive many emailed newsletters but few actually get read.

So I decided that my newsletter had to be printed and sent out the old fashioned way by Royal Mail – in red envelopes of course! I would send it out to 80 people I thought would be interested and who I wanted to keep in touch with – clients, strategic introducers, business partners etc. (I have since made the newsletter available to download from my website).

For the October newsletter I had only 3 days to design my newsletter format, write the content, source envelopes, get it printed, stuffed in envelopes and posted (as well as doing the day job!), because I was due to go on holiday. It was tight but I did it!

Having just sent out my 6th newsletter I certainly feel a sense of achievement.

The feedback I have had has been really gratifying. People are clearly reading the newsletters and engaged enough to comment back to me about what they like, to thank me if I have featured their business, and take part in the competition I ran.

So what have I learned so far?

Firstly, and most importantly, have a format that is easy to follow each month, so you are not confronted by a blank sheet of paper. I have clear smallish sections that are easy to think about in isolation. For example, I have my Pooh quote of the month, Ask Jenny (my financial agony aunt column), featured business and partner, Michael’s minutes and dates for your diary, as standard columns.

Secondly, it may seem like a big commitment to do a newsletter monthly but, like blog writing, once you get into the habit it is relatively easy. It is difficult to get into a habit if you only do an activity irregularly or quarterly.

Finally, having sections about other people and their businesses is a great idea, because it is easier to write about others than ourselves, and readers love the fact that someone else is interested enough in them to write about them.

Now I am not worried about what I will write about each month but actually enjoy the challenge of creating something interesting.

So, if you are thinking about creating a newsletter don’t spend a lot of time worrying about it – just do it!

Fiona 🙂

Do you need a part time FD?

Many SME’s wait too long before employing their first FD.

SME’s that would most benefit from an FD are those looking to invest or spend large sums of capital on assets, expand into new markets, perform mergers and acquisitions, exit from the business or prepare for a stock market flotation.

There are two part time options open to SME’s – recruiting a part time FD or Outsourcing.

When choosing a part time FD its important to look carefully at their experience and track record as the objective is to build a long term relationship.

Having the right FD will release management time to focus on other business issues.

Smarta have a checklist to help you when deciding whether or not to recruit an FD

- Determine the point at which your company is, and assess the state of your finances

- Decide on what the next step for your company is: where do you want it to be? Are you going forward for further investment? How do you want your business to grow? You need to be able to communicate this to your FD

- Determine the ways an FD’s professional input could improve how your business is run, and factor this into the job description

- Ensure the person you take on is experienced, knowledgeable and a good cultural fit

- If you cannot afford to take on a full-time FD, consider taking on a flexible or part-time FD – and make sure they are committed

You could speak to one of our team members if you need help https://business-accountant.com/the-team/

steve@bicknells.net

Frost Group and Business Accountant Offer MVL Service

Frost Group are extremely pleased to be working with CIMA members in practice through their Business Accountant service and sharing with CIMA MiPs our knowledge and experience of Members Voluntary Liquidations.

Jeremy Frost, Insolvency Practitioner and Managing Director of the Frost Group commented:

“Recent developments in the tax regime have caused an increase in the requirement to use Members Liquidations when considering legitimate tax mitigation measures. We believe that CIMA members in practice are better placed than most accountants to recognise and deliver the benefits that will accrue to their clients from this procedure. It makes perfect sense to train them in the process and we are delighted to be able to assist”.

Frost Group are corporate recovery experts, licensed insolvency practitioners and business advisors, and are now in our tenth year of trading. Our continued aim remains to develop partnerships with CIMA members in practice who can benefit from ongoing support and a modern, pragmatic and commercial approach. To learn more about Frost Group, visit our website at http://www.frostbr.co.uk.

Contact Jeremy Frost at the Frost Group on 0845 260 0101. We look forward to working with you.