Home » Tax Avoidance

Category Archives: Tax Avoidance

How does s455 tax apply to Directors Loans? what if you ‘bed and breakfast’ the loan?

Directors (participators in a closed company) often borrow money from their companies with the intention of paying a dividend to repay the loan.

If the loan is outstanding more than 9 months after the company year end, then an extra 25% corporation tax charge is due, this is the s455 tax which is refunded when the loan is repaid as explained in this blog

http://stevejbicknell.com/2015/02/04/new-tax-procedure-for-directors-loans-s-455/

HMRC were concerned that some participators were avoiding this tax by raising funds short term to repay an outstanding loan. They would then draw a new loan very shortly afterwards – HMRC refer to this as “bed and breakfasting”. New anti-avoidance rules were therefore introduced in 2013.

These new rules incorporate two provisions – the “30-day rule” and the “intentions and arrangements” rule.

30-day rule

This applies where within a 30-day period:

- a shareholder makes repayments of their s455 loan; and

- in a subsequent accounting period, new loans or advances are made to the same shareholder or their associate.

So basically prevents the use of ‘Bed & Breakfasting’

‘intentions and arrangements’ Rule

Relief is denied regardless of the 30 day rule, if prior to repayment there is an outstanding amount of at least £15,000 and at the time the amount is repaid to the company, any person intended to redraw any of that amount or had made arrangements to make a new withdrawal; and a new withdrawal is made.

The relief denied is the lower of the amount repaid and the amount redrawn.

steve@bicknells.net

HMRC Solicitors Campaign – do you have anything to declare?

You can tell HM Revenue and Customs (HMRC) about any income you haven’t declared (this is known as ‘voluntary disclosure’).

The Solicitors Tax Campaign gives you the chance to do this if you work within the legal profession as a solicitor in a partnership or company, or as an individual.

How to tell HMRC about undeclared income

- Fill in a notification form by 9 March 2015.

- Fill in a disclosure form and pay what you owe by 9 June 2015.

Use the calculator to help work out what you owe. Only use the calculator if both of the following apply:

- your tax affairs are straightforward

- you’re entitled to only basic personal allowances

There’s a different calculator if you need to tell HMRC about more than 5 years of unpaid tax.

Call the helpline before 9 June 2015 if you need more time to pay.

Help and advice

You can read more about how to make your voluntary disclosure.

Call the Solicitors Tax Campaign helpline if you need more help.

Solicitors Tax Campaign helpline

Telephone: 0300 013 4749

From outside the UK: +44 300 013 4749

Monday to Friday, 8am to 8pm

https://www.gov.uk/solicitors-tax-campaign

steve@bicknells.net

Have you got undeclared Credit Card sales?

The Credit Card Sales Campaign is an opportunity to bring your tax affairs up to date if you’re an individual or business that accepts credit or debit card payments.

Who can do this

This opportunity is for you if:

- you accept card payments for goods or service

- you haven’t declared all your UK tax liabilities

Get the best terms

You need to tell HM Revenue and Customs (HMRC) if you either:

- haven’t registered with them

- have failed to declare all your income

This is called a ‘voluntary disclosure’.

What happens if you should disclose but don’t

HMRC has details of all credit and debit card payments to UK businesses. This information is used to identify individuals and businesses that might not have paid what they owe.

Credit Card Sales Campaign Helpline

Telephone: 0300 123 9272

From outside the UK: +44 300 123 9272

Monday to Friday, 9am to 5pm

steve@bicknells.net

Doctor, Doctor, I think you should be an Employee

A report in the Telegraph on the 14th July 2014…

Dozens of NHS executives face possible investigation by HM Revenue and Customs after they refused to answer questions about their tax arrangements, it can be revealed.

An investigation has identified 86 senior health service officials paid off-payroll who have refused to give assurances to their employers that they are paying the correct level of income tax and national insurance.

They are paid through service companies – arrangements that allow public sector employees to be paid as contractors through private companies, potentially cutting their tax bills.

Monitor found 30 foundation trusts had issues to resolve in their report of the 10th July 2014:

- 20 foundation trusts have 1 or more senior employees paid through an off-payroll arrangement, and they are waiting for responses after asking those employees for assurance about their tax arrangements

- 23 foundation trusts (including some of the 20 above) still have at least 1 board member or senior member of staff with significant financial responsibility employed through an off-payroll arrangement

- of these 23 trusts, 9 are facing wider issues relating to their performance which they have explained is affecting their ability to recruit and retain permanent skilled staff; this resulted in the need to use interim off-payroll contracts to attract high-performing staff to help improve the foundation trust’s situation

- as a result of their performance issues, these 9 trusts are facing current enforcement action by Monitor, which is unrelated to their use of off-payroll employment

- out of those 23 trusts, the other 14 which are not facing enforcement action have plans to end off-payroll arrangements by the end of the year

Will this end the use of PSC’s in the NHS?

steve@bicknells.net

Is there any point in DOTAS if the tax will be paid upfront?

The Finance (No2) Bill 2014, which is due to receive Royal Assent in July, contains legislation which will enable HMRC to demand payment upfront of disputed tax in certain cases, principally involving tax avoidance or deferral. It is estimated that up to 43,000 taxpayers could receive such a demand. Those demands will be issued over an extended period but the first are likely to be issued as early as September 2014.

Taxpayers who have sought tax advantages through tax avoidance schemes that fall within the Disclosure of Tax Avoidance Schemes (DOTAS) are likely to be most affected.

Here is a link to the SRNs (Scheme Reference Numbers) affected – click here

Over the next 2 years HMRC estimates that it will rake in £7 billion through the use of these notices. Of this £7 billion, individuals will weigh in with £5.1 billion. This would equate to each person having a gross income of £262,000.

Last week the Financial Times reported that Ingenious Media, an investment company, warned 1,300 of its investors, including business leaders, entertainers and sporting celebrities, such as David Beckham, to expect substantial tax bills with interest, as reward for using its tax avoidance scheme. (Contractor Weekly)

This is a radical change and many might say its been a long time coming.

It has always struck me as slightly bizarre the DOTAS were registered and allowed to exist.

steve@bicknells.net

HMRC aims to raise further £5bn in tax revenue

Thanks to http://www.freedigitalphotos.net

Her Majesty’s Revenue & Customs (“HMRC”) are seeking new powers as follows:

1. Advance Payment – basically in any dispute between HMRC and a tax payer HMRC would be able to assess what tax they believe is due and require the tax payer to pay this as a sort of ‘refundable deposit’ until such time as the dispute is resolved through arbitration or court. Perhaps more importantly, if granted, these powers will be applied retrospectively.

Given that at the current time there are unresolved cases going back ten years or more and that once HMRC has the tax payers’ money there will be even less incentive for them to come to a resolution then this is essentially HMRC to act as judge, jury, and executioner. Isn’t this simply a ‘guilty until proven innocent’ treatment of tax payers?

2. Direct Debit – where HMRC believe that the tax payer owes them money then they will be able to simply take money directly from the tax payer’s bank account. As I understand it there will be further powers to obtain previous bank statements and this will no doubt lead to further tax investigations.

The legislation which will encapsulate these powers is currently going through Parliament, and despite opposition from lobby groups and committee members alike, HMRC seem intent upon pushing this legislation through with a view to achieving Royal ascent in mid July 2014.

Of course, should HMRC gain these powers they will hit the easy targets first i.e. those who have ‘played by the rules’ and properly disclosed everything through DOTAS, and those who operate proper business bank accounts, so it will do nothing to address those who have hidden their activities from HMRC and those who operate in the black ‘cash-in-hand’ economy.

Whilst the general public may have little sympathy for people who ‘don’t pay their fair share of tax’ (if there is such as thing – see Did Jimmy Carr just use the wrong vehicle?) we have to remember that tax avoidance is entirely legal as it simply takes the rules and regulations enacted in law and uses these to reduce a tax payer’s liability.

The new powers will do nothing to tackle tax evasion, which is illegal, and so it is no surprise that spokesmen for HMRC, and representatives for HM Government, have sought to blur the lines between legal avoidance and illegal evasion in recent times. We can be equally sure that HMRC will not be tackling the multi-nationals like Google and Starbucks who have made recent headlines with their tax affairs, and so it will (as ever) be small firms that will bear the brunt of any HMRC action.

What we shall no doubt see is an increase in non-DOTAS schemes being made available to tax payers by providers of such schemes, and I fear beyond that we shall see a rise in business insolvencies and loss of jobs, all of which will run contrary to HMRC’s aim to raise further tax revenues.

Paul Driscoll is a Chartered Management Accountant, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and AJ Tensile Fabrications Limited, and is a board level adviser to a variety of other businesses.

A Trillion Euro’s lost to tax evasion in the EU

A Trillion is a huge amount, its almost too large to imagine.

Here is the latest campaign video

http://ec.europa.eu/avservices/video/player.cfm?ref=I080915

As part of the intensified battle against tax fraud, the Commission launched on 6th February 2014 the process to start negotiations with Russia and Norway on administrative cooperation agreements in the area of Value Added Tax (VAT). The broad goal of these agreements would be to establish a framework of mutual assistance in combatting cross-border VAT fraud and in helping each country recover the VAT it is due. VAT fraud involving third-country operators is particularly a risk in the telecoms and e-services sectors. Given the growth of these sectors, more effective tools to fight such fraud are essential to protect public budgets. Cooperation agreements with the EU’s neighbours and trading partners would improve Member States’ chances of identifying and clamping down on VAT fraud, and would stem the financial losses this causes. The Commission is therefore asking Member States for a mandate to start such negotiations with Russia and Norway, while continuing exploratory talks with a number of other important international partners.

http://ec.europa.eu/taxation_customs/taxation/tax_fraud_evasion/missing-part_en.htm

steve@bicknells.net

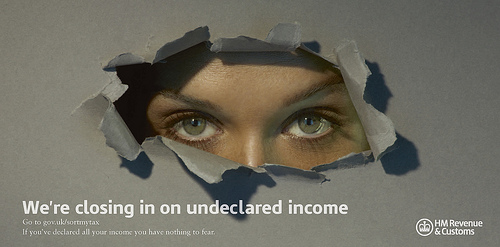

How HMRC use IT systems to seek out tax evaders

There is no doubting the resolve of HMRC to track down and prosecute tax evaders.

The Government has committed to spend £917m to tackle tax evasion and raise an additional £7bn each year by 2014/15.

HMRC are using 2,500 staff to tackle avoidance, evasion and fraud, there is also a website to help those who want to declare income https://www.gov.uk/sortmytax

In the search for tax evaders, HMRC have a £45m computer system called Connect which in 2011 delivered £1.4bn in tax revenue and the system is getting bigger and better all the time. According to Accounting Web:

It uses a mathematical technique to search previously unrelated information and detect otherwise invisible ‘relationship’ networks. Using Connect, HMRC sifts through information on property transactions at the Land Registry, company ownerships, loans, bank accounts, employment history, voting and local authority rates registers and compares with self-assessment records to spot taxpayers who might be under-declaring or not declaring income.

Last year Connect made links between tax records and third party data from hospitals, pharmaceutical companies, insurers and even gas SAFE registrations. DVLA records and the shipping and Civil Aviation Authority registers help identify owners of cars and planes who declare income that the computer suggests cannot support such purchases.

In addition HMRC have also identified 200 accountants, lawyers and professionals who advise on tax avoidance structures and its currently unclear how HMRC will be dealing with them and their clients.

It is important to remember that most people pay the correct tax, in fact HMRC calculate that 93% of tax due is paid correctly, its only a small minority who try to evade tax.

steve@bicknells.net

HMRC demand payment from Landlords

HMRC launched the ‘Let Property Campaign‘ on the 10th December 2013.

If you’re a landlord who has undisclosed income you must tell HMRC about any unpaid tax now. You will then have 3 months to calculate and pay what you owe.

The Let Property Campaign is an opportunity open to all residential property landlords with undisclosed taxes. This includes:

- those that have multiple properties

- landlords with single rentals

- specialist landlords with student or workforce rentals

- holiday lettings

- anyone renting out a room in their main home for more than £4,250 per year, or £2,125 if the property was let jointly, but has not told HMRC about this income

- those who live abroad or intend to live abroad for more than 6 months and rent out a property in the UK as you may still be liable to UK taxes

According to the Telegraph….

Fewer than 500,000 taxpayers are registered with HMRC as owning properties other than their home. And yet other sources put the number of Britain’s growing army of landlords at between 1.2million and 1.4million.

Why the discrepancy? No one can say for sure, but the taxman has his answer: not enough people are declaring – and paying tax on – their property incomes and gains.

HMRC will identify those who they believe should have made a disclosure by:

- comparing the information already in their possession with customers’ UK tax histories

- continuing to use their powers to obtain further detailed information about payments made to and from landlords

Where additional taxes are due HMRC will usually charge higher penalties than those available under the Let Property Campaign. The penalties could be up to 100% of the unpaid liabilities, or up to 200% for offshore related income.

If you owe tax, you must tell HMRC of your intention to make a disclosure. You need to do this as soon as you become aware that you owe tax on your letting income.

At this stage, you only need to tell HMRC that you will be making a disclosure.

You do not need to provide any details of the undisclosed income or the tax you believe you owe.

steve@bicknells.net

Key Points from the Autumn Statement 2013

The Chancellor George Osborne presented the Autumn Statement to the House of Commons on 5th December 2013 and things are getting better, economic growth forecasts for this year have more than doubled from 0.6% to 1.4% but the austerity plan is set to continue.

Here is a summary of the key announcements:

Business Rates

Business rate increases in England will be capped at 2% in 2014/15 (they were set to increase by 3.2%) and businesses will be able to pay over 12 months rather than 10.

The Retail Sector will also get a £1,000 discount in 2014/15 and 2015/16, this applies to pubs, cafes, restaurants and charity shops with a rateable value below £50,000.

A reoccupation relief of 50% is being introduced for up to 18 months on premises that have been empty for a year or more and it will apply from 1st April 2014 to 31st March 2016.

Small Business Rate Relief has been extended to April 2015 under the scheme small businesses with a rateable value of £6,000 or less can get 100% relief, the relief is scaled down to zero on rateable values of £12,000 and there is a lower multiplier on rates between £12,001 and £17,999.

Income Tax

As previously announced the personal allowance will be £10,000 for the tax year 2014/15.

From April 2015, a spouse or civil partner who is not liable to income tax will be able to transfer £1,000 of their allowance to a basic rate tax paying spouse and as a result save £200 in tax.

State Pension Age

By 2020 it will be 66, by 2028 it will be 67 and by mid 2030′s 68, then in 2040′s 69.

Capital Gains Tax

The annual exempt amount will be £11,000 for individuals for 2014/15.

But there was an exemption for principle private residence letting for 36 months and from 6th April 2014 it will be reduced to 18 months.

Consultation will start in April on non-residents paying capital gains on property disposals.

Individual Savings Account (ISA)

The limit will rise to £11,880 for 2014/15 and of this £5,940 can be invested in cash ISA’s

Mortgage Guarantee Scheme

The scheme started in October will run for 3 years and end in January 2017.

Buyers will only need a 5% deposit and the government and the funder will guarantee 15% of the loan in return for a fee.

IR35

Legislation will be tightened from April 2014.

Anti-avoidance

A range of measures were discussed in addition to IR35 and these included:

- Partnership Tax

- Controlled foreign companies

- Charities

- High risk tax avoidance schemes

- Dual contracts

Other headline measures

- Employers NI for under 21′s to be scrapped in 2015

- Rolling back green levies to allow an average saving of £50 on energy bills

- Free school meals for infants

- Scrapping of 1% above inflation rail fare increases

- Electronic tax discs

- Abolition of next years 2p per litre fuel duty rise

steve@bicknells.net