Home » Financial Reporting

Category Archives: Financial Reporting

Now we have Deferred Tax on Investment Properties!

FRS102 has led to many changes in the way we account for things and investment property is a prime example.

The fair value of investment properties changes over time, generally, it goes up in value.

The reporting of gains and losses under old and new UK GAAP differs fundamentally.

Under FRS 102, annual changes in the fair value of Investment Properties are taken to profit or loss, whereas under SSAP 19, equivalent gains and losses were taken in most cases to the Statement of Recognised Gains and Losses. This may have a significant impact on reported performance. The resultant earnings volatility may need to be explained to lenders and other users of the accounts.

FRS 102 removes some of FRS 19’s exemptions from recognising deferred tax. As a result, in contrast to current UK GAAP (that is, FRS 19), companies will often need to recognise significant deferred tax liabilities on revaluation gains.

The tax won’t be payable until the gain is realised.

Many property investors are likely to switch to Micro-entity accounting because its much simpler and doesn’t require property revaluations and deferred tax.

Breaking up is hard to do? (Demergers)

A demerger is a form of corporate restructuring in which the entity’s business operations are segregated into one or more components. (Wikipedia)

Demergers are not defined in Tax Law but can be successfully used by Trading Companies and do get special tax treatment.

CTA10/S1075 & TCGA92/S192

A demerger is a series of transactions which have the effect and purpose of dividing the trading activities carried on by a single company or group of companies between two or more companies or groups of companies. CTA10/S1075 and TCGA92/S192 provide special tax treatment if certain conditions are met. Companies may seek advance clearance under CTA10/S1091 that proposed transactions will be an exempt demerger. CTM17200 onwards gives further guidance on the action to be taken by local offices in dealing with demergers.

Basically there are 3 ways to do Demergers

- Distribution in specie – CTM17250

- Liquidation

- Reduction in Capital

Property Investment Companies are not trading companies so demergers are extremely complicated as explained in this article in Taxation

steve@bicknells.net

Does your team understand the business strategy? (Balanced Scorecard)

Created in 1992 by Drs. Robert S. Kaplan and David P. Norton, the Balanced Scorecard (BSC) is a revolutionary way to handle strategy management. Notably, it centers your vision and strategy around four distinct measures: Customer, Internal Processes, Financial, and Learning/Growth. Essentially, the Balanced Scorecard allows you to get your whole team on the same page with organizational goals in a clear and understandable way. Although it started out being used primarily in the private sector, you’ll now see the Balanced Scorecard in healthcare, non-profit, government organizations, and a number of other types of associations. [Clear Point Strategy]

Here are 10 examples for different types of businesses – click here

This the Balanced Scorecard for Barclays Bank

About half of major companies in the US, Europe and Asia are using Balanced Scorecard Approaches. The exact figures vary slightly but the Gartner Group suggests that over 50% of large US firms had adopted the BSC by the end of 2000. A study by Bain & Co finds that about 44% of organisations in North America use the Balanced Scorecard and a study in Germany, Switzerland, and Austria finds that 26% of firms use Balanced Scorecards. The widest use of the Balanced Scorecard approach can be found in the US, the UK, Northern Europe and Japan.

Even the most brilliant strategy is worth nothing if it isn’t executed well, especially by your front line — the employees who interact daily with your customers. Unfortunately, these employees are regularly asked to execute strategies that others developed and that they may not understand, never mind feel committed or connected to. In fact, according to Robert Kaplan and David Norton, the founders of the Balanced Scorecard, only 5% of employees understand their company’s strategy. This makes successful execution nearly impossible.

Watch this video, how well would your employees do if you asked them about strategy?

steve@bicknells.net

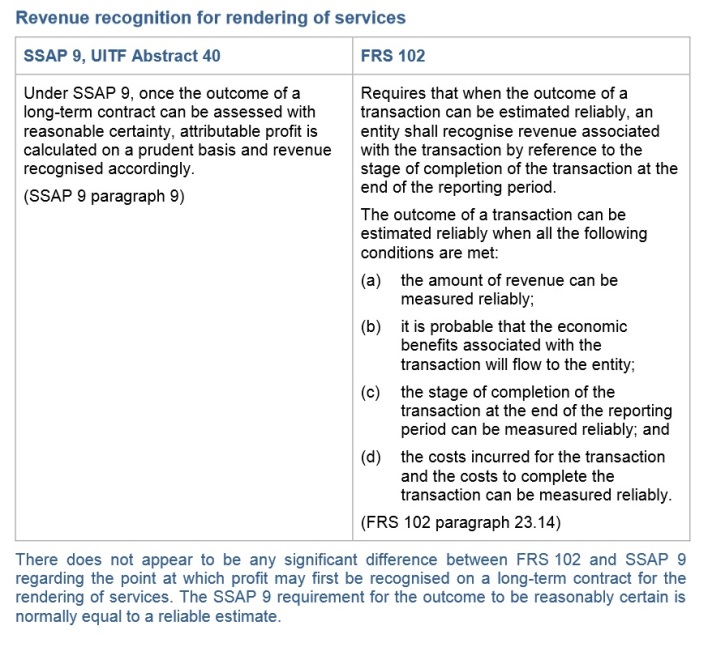

When should you recognise revenue on services provided?

The International Accounting Standard IAS 18 states

‘where the outcome of a transaction involving the rendering of services can be estimated reliably, associated revenue should be recognised by reference to the stage of completion of the transaction at the end of the reporting period’ . In other words, the revenue is recognised gradually, rather than all at one ‘critical point’, as is the case for revenue from the sale of goods. IAS 18 further states that the outcome of a transaction can be estimated reliably when all the following conditions are satisfied:

(a) The amount of revenue can be measured reliably.

(b) It is probable that the economic benefits associated with the transaction will flow to the seller.

(c) The stage of completion of the transaction at the end of the reporting period can be measured reliably.

(d) The costs incurred to date for the transaction and the costs to complete the transaction can be measured reliably.IAS 18 does not prescribe one single method that should be used for determining the stage of completion of a service transaction. However the standard does provide some examples of suitable methods:

(a) Surveys of work performed.

(b) Services performed to date as a percentage of total services to be performed.

(c) The proportion that costs incurred to date bear to the estimated total costs of the transaction.If it is not possible to reliably measure the outcome of a transaction involving the provision of services (perhaps because the transaction is in its very early stages) then revenue should be recognised only to the extent of costs incurred by the seller, assuming these costs are recoverable from the buyer.

In the UK UITF40 and SSAP9 defined the way we report revenue and profit in relation to Services, although accountants and lawyers were among the most high profile casualties of the new regime back in 2005, which forced them to re-catagorise WIP and Revenue, many other service providers also had to consider how they accounted for income. Professionals such as surveyors, architects, doctors and dentists all had to consider the impact of the new rules on their tax liabilities.

FRS102 has not changed the rules.

steve@bicknells.net

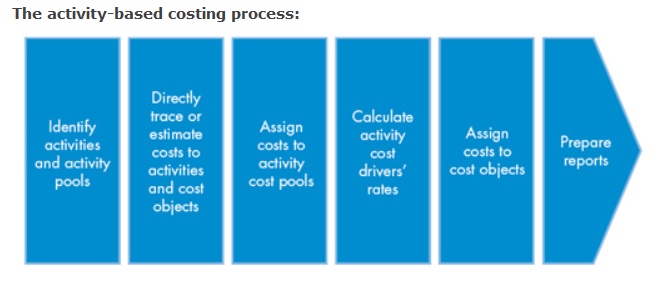

Overhead allocation using ABC

CIMA Official Terminology describes activity-based costing as an approach to the costing and monitoring of activities, which involves tracing resource consumption and costing final outputs. Resources are assigned to activities and activities to cost objects. The latter use cost drivers to attach activity costs to outputs.

What are Activity Pools and Cost Drivers?

Activity Pools

- Purchase Orders

- Machine Set Ups

- Packaging

Cost Drivers

- Number of Purchase Orders

- Number of Machine Set Ups

- Number of items to package

What would the traditional methods of allocation have been?

- Direct Labour Hours

- Machine Hours

- Floor Area

Using Activity Based Costing can produce very different results to Traditional Methods, click here for an example

steve@bicknells.net

FRS105 – The new Financial Reporting Standard for Small Entities (in draft) – (aka – FRED58 at present)

The Financial Reporting Council (FRC) has recently published FRED 58, being the Exposure Draft for FRS105, which in turn will become the new FRSSE (or replace the existing FRSSE, we believe).

Comments on the Exposure Draft was due by 30 April 2015, so if you missed it, we are afraid the the train has already left the station.

In a nutshell, we have some serious conceptual and philosophical concerns the FRED 58 does not address (and staff at the FRC at a recent event in London, prior to the General Election, could not provide assurances on).

Effectively FRS 105 (as it will be know), once it is ratified and adopted in parliament, will not be IFRS ‘Lite-lite‘, although it will have some of the overall principles of Fair Value Accounting contained within it.

At a fundamental level micro-entities (* as defined below) can choose to adopt either FRS 105 or FRS 102. However, be very careful in which one you choose, as the two standards have some fundamental differences contained within them, which, later down the line (as the proverbial can is kicked up the road), might cost you additional compliance fees and time and effort, if you need to convert from FRS 105 reporting to FRS 102 (New UK GAAP).

Our concern is this:

“The overall objective of all the initiatives (driven from Brussels) is HARMONISATION. The differences in approach between FRS 105 and FRS 102 do not underscore this fundamental principle!”

Hence, our health warning:

Think and consult carefully, before adopting either standard (FRS 102 or FRS 105) if you are a micro-entity caught in the compliance reporting net.

If you have any questions or concerns, please contact any Business Accountant in our network for more details.

3resource ©2015

*Definition of a micro-entity:

Micro-entities – HMRC guidance – May 2015 (as per the HMRC web site at the post’s publishing date)

Micro-entities are very small companies. Your company will be a micro-entity if it has any 2 of the following:

a turnover of £632,000 or less

£316,000 or less on its balance sheet

10 employees or less

If your company is a micro-entity, you can:

prepare simpler accounts that meet statutory minimum requirements

send only your balance sheet with less information to Companies House

benefit from the same exemptions available to small companies

Why working with accounting is about to get so much better

Anyone who works with businesses is fully aware of how important accounting is for the success of a company. Yet many business owners have a negative attitude towards accounting. A high percentage of entrepreneurs see accounting as a necessary evil and often a hindrance to starting a new company.

How is that possible? Wasn’t accounting invented to help companies manage their business?

The IT industry has brought us computers and the ability to create software to automate bookkeeping. While there is no doubt that accounting software has been a great help, when we look at the usage of it, something is wrong. More than half of the businesses in the UK keep track of their finances by using a combination of spreadsheets and word processors rather than using accounting software. In an age where computing power is ubiquitous and virtually never too far from our pocket, we should be able to do better than this.

In 2013, international accounting software provider e-conomic was considering what its next generation accounting software should look like. And decided to take a different approach. What would happen if we created a piece of accounting software for people who had no knowledge of accounting? And what if we made the basic functions free for people to use? We hoped that it would make accounting approachable by virtually anybody.

That’s how the Debitoor invoicing and accounting software was born.

Introducing simple accounting to the world

Today, more than 33,000 people in the UK and almost 300,000 people worldwide have signed up for Debitoor and have given us the privilege of approaching accounting in a different way. Debitoor is used in more than 30 countries, from the UK to South Africa, from Colombia to Australia and New Zealand.

Debitoor is an accounting package for very small businesses. It allows them to manage their customers, create quotes and invoices. It allows them to register their purchases, deal with bank and payments and helps them report their VAT directly to HMRC at the click of a button. Debitoor helps those small companies manage their assets and keep track of what’s on their balance sheet in a very simple manner. Finally, Debitoor helps business owners collaborate with their accountants by allowing them to share their data with them.

Debitoor’s mission is to make accounting cool to work with. Two years after we started, the typical reaction we get from accountants is: “Wow, convincing my clients to use this is going to be super easy!”. We have captured the essence of Debitoor in this video.

Letting users shape accounting software

But what have we done to make this possible? The most important ingredient has been a clear focus. Our mission has always been to make accounting easy for small business owners who know very little about accounting.

Here are some of the key principles we followed to build the Debitoor invoicing and accounting software:

– Approachable: We have removed any obstacles to getting started. There is no setup needed, we do not ask questions, users can start on the free package, the program is ready to go.

– Natural: We have eliminated all technical lingo. You will not find the words “debit” and “credit” in Debitoor. The workflows in the program follow the natural flows of a user with no accounting knowledge and the program uses the typical words he’d use.

– Forgiving: People make mistakes; and accounting systems typically make it quite complicated to correct mistakes. In Debitoor, actions can be undone and mistakes can easily be corrected.

– Instructive: We assume people do not know much about accounting, so we have structured the entire program to let users learn along the way. This is not just functionality but it encompasses the entire packaging of the product.

– User-driven: In an open forum, users can give their feedback and suggest new features, vote for their own or others’ suggestions and influence the further development of the software. This transparency is super important for us to develop a truly user-driven program.

– Collaborative: Most of our users share their data with their accountants in order to get help with taxes, reporting and ensuring quality.

We also had the privilege of building the product with the technology which was available in 2013. This has huge benefits for our users because it allows us to provide them with a service which is reliable, improving at a fast pace and very secure. Having a modern architecture also ensures that Debitoor is very easy to connect to other popular cloud services.

Debitoor’s user base is very diverse as its appeal is quite broad. Many of our users are freelancers, artists, consultants, designers or other creative people, but we have also small artisans and shop keepers or owners of clinics and small distributors. They all have missions and purposes in their lives and we try to help them with their accounting.

Check out the stories of Felicia Matheson from Prohibition Drinks in Newscastle, Northern Ireland and the story of Esther from The Roasting Shed in London.

Changing how an industry works

As with any change in technology, this brings great opportunities to the industry it affects. The introduction of new technology, however, takes a bit of time to mature. When television started to gain mass adoption in the 1950s, broadcasters used it as it was radio. The first shows had older men with glasses reading papers in front of a microphone. This was how it used to be with radio programs.

The availability of cloud software has created a set of providers who simply made traditional accounting software available on the internet. This, we believe, will change and we will see more and more software which is transformational in nature. That is what we are trying to do with Debitoor.

We are only at the beginning of this journey. The roadmap for Debitoor will focus on three main aspects:

1. Continue to add simple flows to support what today are very difficult accounting scenarios

2. Introduce more and more automation and intelligence to enable our users to do more with less knowledge

3. Strengthen the collaboration between users and their accountants by facilitating the sharing of data between them.

What will this mean for accountants and the accounting industry? This is what our users are telling us: They love doing their invoices and keeping track of their costs in Debitoor. It gives the nice feeling of being in control, it keeps them organized and allows them to focus on their business going forward.

At the same time, they also tell us that they need help from their accountants. They need help with taxes, they need help with reporting to authorities and a lot of them need a quality check from the experts. In addition, most of them need legal and financial advice on ad hoc issues they encounter in their life as entrepreneurs.

The biggest change for accountants is to be prepared to embrace the possibilities that technology gives us. Things like cloud storage and online applications will substitute manual processes, paper and data disks. Everything is now available via a web browser on your computer or on your phone.

In order to be successful, accountants will have focus on services that draw on their knowledge and experience and they will need to be prepared to serve their customers as they move towards those new technologies.

Increased access will not be limited to technology but also to services. This will also mean increased competition. The best thing an accountant can do is embrace change and be ahead of the curve, start small but start early. The customers are already going there.

Companies House reports will be Free in 2015

Its time to review your subscription to company information databases!

Companies House is to make all of its digital data available free of charge. This will make the UK the first country to establish a truly open register of business information.

As a result, it will be easier for businesses and members of the public to research and scrutinise the activities and ownership of companies and connected individuals. Last year (2013/14), customers searching the Companies House website spent £8.7 million accessing company information on the register.

Until it becomes free in 2015, you will still have to pay

| Companies House WebCHeck | Charges |

|---|---|

| Company accounts | £1 |

| Annual return | £1 |

| Company record report | £1 |

| Current appointments report | FREE |

| Monitor Service (per company, per year) | FREE |

This change will come into effect from the second quarter of 2015 (April – June).

steve@bicknells.net

When will your company stop being small?

Back in June 2013 the EU passed a directive 2013/34/EU which changed the thresholds for small companies.

| Present | Proposed | |

| Turnover | £6,500,000 | £10,200,000 |

| Total assets | £3,260,000 | £5,100,000 |

| Average no. of employees | 50 | 50 |

As before its a 2 out of 3 test. The Audit thresholds are unchanged.

The UK was required to transpose this into UK Law no later than 20th July 2015.

The Dept for Business Innovation and Skills (BIS) concluded their consultation (24th October 2014) and the plan is currently to implement the change for financial years starting on or after 1st January 2016.

As pointed out by SWAT

This could mean that a company with a turnover between £6.5m and £10.2m will be required to prepare its accounts for year ended 31 December as follows:

2014 as a medium sized company under present UK GAAP;

2015 as a medium sized company under FRS 102;

2016 as a small company under the applicable accounting regime for small companies.

This might depend on whether the company could early adopt the new regulations for its 2015 accounts. The possibility of early adoption is one of the questions asked by BIS.

Surely BIS can see that not allowing early adoption will place an unnecessary reporting burden on Small Companies?

steve@bicknells.net

What flavour is your Accountant?

Thanks to http://www.freedigitalphotos.net

One of the great joys of working as a ‘CIMA MiP’ (“Chartered Institute of Management Accountants, Member in Pratice”) is that we are generally dealing with ‘small’ and ‘micro’ client firms (micro defined by EU regulations as firms with less than 10 employees/ £2m turnover; small defined as firms with less than 50 employees/ £10m turnover) and that we become involved in an enormous breadth and depth of subjects.

One of the less welcome challenges however is that as far as most small and micro business owners and managers are concerned, one accountant is the same as any other and this includes the myriad unqualified accountants who practice their particular brand of accounting services at rock-bottom rates. Indeed it is rare that I have been asked whether I am a ‘qualified’ accountant, and is rarer still that I am asked what that qualification is (in fact I cannot ever recall being asked that question by a client). The client generally assumes that because one calls oneself an ‘accountant’ then one can ‘do accounts’ and that accountants are all the same.

We’re not.

My particular practice specialises in manufacturing clients and most new clients have come from existing client referrals. Fortunately I do not need to be a great sales person to convert a prospect into a new client when (a). there is a recommendation from an existing client and (b). we appear to ‘speak the same language’. Clients generally put this down to my having owned and run manufacturing firms and to some degree that is true, but is is also because of my CIMA training.

If you’re looking for year end accounts, audit, or tax computation then you will likely be talking to a ‘Certified Accountant’ or ‘Chartered Accountant’, but where they will be reporting back to you on how well (or otherwise) you did overall last year and what your tax liability is, the CIMA ‘Chartered Management Accountant’ will be working with you to establish what activities made money and why, and whether you can do more of it, and of course which did not and how to avoid this in future; indeed the focus is very much ‘future’ as much as ‘past’.

In terms of the client business, it’s not difficult to see that helping the client to understand their business is a valuable element in managing, changing, and improving the business, and this is something which CIMA qualified people have to offer any business, so it’s a great shame that Chartered Management Accountants tend to be employed by big businesses who understand the difference between the different accounting disciplines.

None of this is to say that a Certified Accountant or Chartered Accountant could never do what the Chartered Management Accountant does, but it is not what they have been trained to do and equally as a Chartered Management Accountant in practice for twenty-two years I provide a ‘full service’ including year end accounts and tax returns for my clients, albeit the main focus remains helping them to improve their business.

I would urge Chartered Management Accountants to seriously consider a career in the small and micro business sector which accounts for 99.3% of the 4.7 million businesses in the UK (source: BIS 2013) and 47% of private sector employment (source: FSB 2013) and which is a vital part of the UK economy: whether in practice servicing a number of clients, or a full-time employee of a particular firm, I am sure that you will find the experience very rewarding

I would equally urge owners and managers in that sector to become aware of the differences between the main accounting bodies and the relative strengths of each, and to be sure that whoever they engage with will meet the needs of their particular business.

Paul Driscoll is a Chairman of CIMA MiPs in South West England and South Wales, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and a number of manufacturing companies, and is a board level adviser to a variety of other businesses.