Home » Articles posted by Fiona Jones

Author Archives: Fiona Jones

Business Premises Renovation Allowance

The Business Premises Renovation Allowance (BPRA) finishes in 2017 and is a great relief! Changes have been made to the relief to target it more effectively. Additionally the period for balancing adjustments has been reduced from seven to five years.

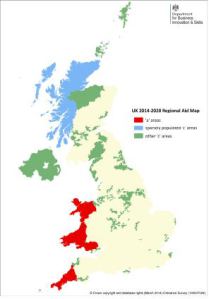

BPRA is aimed at the renovation of empty business premises, which have been empty for at least 12 months and which are located in an assisted area. See Assisted Areas Map below from the Gov.uk website:

Capital Expensiture must meet conditions A and B, and must be incurred before the expiry date. Also certain exclusions aply.

Condition A

The expenditure must be incurred on:

The conversion of a qualifying building into qualifying business premises.

The renovation of a qualifying building, provided it is or will become qualifying business premises.

Repairs to a qualifying building, or part of a qualifying building, provided those repiars are incidental in nature to that incurred…

View original post 153 more words

SMEs reluctant to borrow…

High growth small and medium-sized enterprises (SMEs) are reluctant to seek finance from banks to fund growth, a study by the Institute of Chartered Accountants of Scotland (ICAS) has found.

The study found that high growth SMEs are “highly reluctant borrowers” because of their lack of trust in banks. Many firms also said they were unwilling to sacrifice their autonomy in order to access bank finance.

The study also found that high growth SMEs:

- are 9% more likely to seek bank finance than other SMEs but are no more or less likely to receive it

- prefer bank finance to equity finance

- are likely to use a ‘mixed cocktail’ of finance, including internal resources and debt.

The report, Funding issues confronting high growth SMEs in the UK, was launched to study the demand for finance among high growth SMEs and investigate the problems they encountered.

It focuses specifically on high growth SMEs because of their capacity for growth and employment.

To read more about the recommendations to increase the liquidity to SMEs http://www.grant-jonesaccountancy.com/news-item/smes-reluctant-borrow

Fiona@grant-jonesaccountancy.com

New ISA’s (NISAs) just around the corner…

Nearly two thirds (63%) of UK adults are unaware of the tax free savings allowance one week before the launch of New ISAs (NISAs), according to research from MoneySuperMarket.

The survey by the comparison site reveals that 32 million people do not know about the introduction of NISAs.

Of those that have heard of them, 24% do not understand the new rules.

Key findings:

- 68% of 18 to 34 year-olds have not heard of NISAs, rising to 70% of people aged 35-54

- 35% of respondents said they are likely to use a NISA, while 30% said they are unlikely to

- 45% of 18 to 34 year-olds said they might use the new savings products

- 33% of over-55s are likely to use a NISA

- 28% believe NISAs will help them save more

- 45% of 18 to 34 year-olds think they will save more, dropping to 26% of 35 to 54 year-olds and 18% of over-55s.

Read more http://www.grant-jonesaccountancy.com/news-item/two-thirds-unaware-nisas

fiona@grant-jonesaccountancy.com

Limited Liability Partnerships

Limited Liability Partnerships came under closer scrutiny in the Budget 2013. The aim is to target LLPs which use the structure to hide the employment relationship of the partners and those with Corporate partners who divert business profits to the corporate partners in order to avoid tax.

Although the following measures come in to play from 6th April this year, the anti-avoidance measures make it effective from 5th December 2013. This is to prevent partnerships changing their arrangements in order to avoid the new rules.

The two main areas of focus are salaried or fixed profit share partners which is referred to as disguised employment, and profit and loss sharing arrangements within mixed partnerships.

LLP partners with fixed profit share

HMRC believe that many members of an LLP should be taxed as employees, because they don’t see them is true partners.

A new test has been brought in which has three conditions. Where the member tested meets all three conditions then he or she must be treated as an employed salaried member and be brought within the PAYE system with tax and class I NIC applied to any earnings, which had previously been Taxed as profit share.

This also means that if a vehicle is provided for the members use by the partnership this will be taxed as a benefit in kind. As such the member will have to pay tax and NIC and the LLP will have to pay Class 1a NIC on the benefit.

HMRC does actually accept that employment tax rules are imposed on the individual but that in fact the individual has no employment rights. This is because he is not actually an employee for employment law purposes.

The test is as follows. The provision is triggered when all conditions A to C are met:

Condition A: The Member is performing services for the LLP in his capacity as a member of the partnership and it’s reasonable to expect as a result of these arrangements that any amounts paid to him in respect of his services will be wholly or substantially wholly a disguised salary. In other words if his reward package is comparable to that received by an employee, either a fixed salary or a variable bonus based on performance rather than profit share.

Condition B: The Member doesn’t have significant influence over the affairs of the partnership.

Condition C: The Member’s capital contribution to the LLP is less than 25% of the total amount of his disguised salary which would be expected to be paid in the relevant tax year by the LLP in respect of the members performance of services as a member. Normally the relevant time would be the beginning of the new tax year.

These tests must be reviewed each tax year.

Corporate LLP Members

This applies to partnerships who have members which are not subject to UK income tax for example this might be a limited company. The problem here is that HMRC believes these structures are used to avoid tax on a very large scale. Where for example an individual member introduces his Ltd company as a corporate member, and which then receives a profit share that would otherwise have been paid to the individual member. If the Member then has the power to enjoy the fund which had been paid to his company then:

- The individual member will be treated as a salaried member.

- The amount paid to the company will be treated as employment income paid to the individual member.

There are anti-avoidance rules are in place to catch anyone trying to put measures in place to counteract these new rules.

fiona@grant-jonesaccountancy.com

EMPLOYER’S £2,000 NIC ALLOWANCE

Why the Ostrich? Well I think she’s pretty!

This valuable allowance is due to start for all businesses on 6 April 2014, and simply exempts the employer from the normal employer NICs of 13.8% of the earnings paid.

The mechanics are that the allowance will be obtained via standard payroll software and HMRC’s RTI system. A facility will be added to the RTI Employer Payment Summary referring to the allowance in the form of a “yes/no” indicator, with payroll software providers doing the same. The employer then offsets the allowance against each monthly Class 1 secondary NICs payment until fully claimed or the tax year ends. For the following tax year the allowance is available against NICs as the liability arises during the year.

For a small company rewarding working shareholders by way of dividends, the current thinking is that from 6 April 2014 it will usually be best to receive remuneration of £10,000 per annum instead of limiting it to the NIC secondary threshold of (currently) £7,696 as is normally done. This is because earnings of £10,000 will fully utilise the new level of personal allowance, whereas dividends effectively waste the allowance.

fiona@grant-jonesaccountancy.com

Contractor Loan Schemes

HMRC is challenging certain types of tax avoidance arrangements used by contractors and other professionals. These schemes aim to avoid tax by entering into a contract of employment with an offshore employer, meanwhile the contractor continues to provide their services in the UK. The contractor then receives a large proportion of the fees for their services in payments which are reported as loans. However HMRC argues that these arrangements do not succeed in avoiding tax.

Individuals using these schemes may shortly or already have received letters opening enquiries into their recent returns. HMRC will be sending tax assessments to those who have used these schemes between 2008 and 2011. If your client receives an assessment he can according to HMRC either accept the assessment and pay the tax due, try to reach an agreement with HMRC or appeal against the assessments and begin the tribunal process.

HMRC is urging individuals affected or their advisers to contact HMRC by phone or by email at the following link at http://www.hmrc.gov.uk/news/contractor-loan-schemes.htm.

Fiona@grant-jonesaccountancy.com