Home » Accounting Records

Category Archives: Accounting Records

Are you ready for the changes to employee expenses?

From April 2016 all employee expense Dispensations agreed with HMRC will cease to apply!

You will need new systems for checking expenses, HMRC will be supply examples.

Expenses which are not covered by benchmark scale rates are likely to paid and taxed via the payroll with the employee claiming relief through P87 and Self Assessment SA100.

Are you ready for the new regime?

Will TAAR cause you problems on company distributions? (New Share Rules)

HMRC are currently consulting on new rules to start in April 2016.

The consultation is focusing on Capital Gains Tax (CGT) ways to extract money from companies to create Target Anti Avoidance Rules (TAAR) covering:

- A disposal of shares to a third party

- A distribution made in a winding up

- A repayment of Share Capital including Share Premium

- A valid purchase of own shares in an unquoted company

Here are the examples of ‘problems’ HMRC want to resolve, Example 1 is ‘moneyboxing’ and/or ‘phoenixism’ and sometimes involves ‘special purpose vehicles’

Example 2 involves creating a holding company…

The consultation ends on the 3rd February 2016, the results are likely to be controversial!

steve@bicknells.net

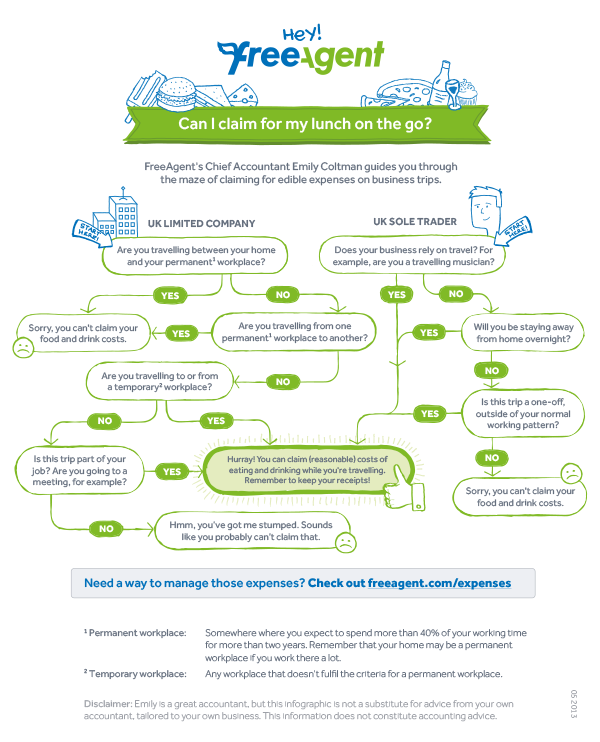

2016/17 rules on the tax free allowance for Sandwiches

What are business journeys (HMRC definition)

You can only get tax relief on the cost of business journeys. These are when, as part of your job:

- you have to travel from one workplace to another – this includes travelling between your main ‘permanent workplace’ and a temporary workplace

- you’ve got to travel to or from a certain workplace because your job requires you to

But business journeys don’t include:

- ordinary commuting – when you travel between your home (or anywhere that is not a workplace) and a place which counts as a permanent workplace

- private journeys – which have nothing to do with your job

steve@bicknells.net

10 ways to pay less VAT

Here are my top 10 ways to pay less VAT

1 Choose the best VAT Scheme for your business

Standard VAT Scheme – on this scheme the VAT is based on tax points from invoices

Flat Rate Scheme – try our calculator

VAT Cash Accounting Scheme – if your turnover is below £1.35m you can account for VAT on a Cash basis, this is particularly helpful if your customers pay you on slower terms than you pay your suppliers

Annual Accounting Scheme for VAT – if your turnover is below £1.35m you could join the Annual Scheme and complete one return for the year but you make either 9 interim payments or 3 quarterly interim payments

Retail VAT Schemes – These are specific schemes aimed at mainly at shops and help to overcome the issues of mixed vat rate goods

VAT Margin Scheme – The margin scheme relates to second hand goods and accounts for VAT on the margin, for example on the sale of cars

2 Claim Pre-registration VAT

When you register for VAT, there’s a time limit for backdating claims for VAT paid before registration. From your date of registration the time limit is:

- 4 years for goods you still have, or that were used to make other goods you still have

- 6 months for services

Be careful not to over claim – see this blog for details http://stevejbicknell.com/2015/06/24/preregistration-vat-confusion/

3 Property Investors might benefit from a Development Company

Property Development is a trade, where as Property Investment isn’t – renting out a residential property is a VAT exempt supply.

If you are planning significant building work, setting up a Development Company or using a building contractor might save VAT.

Assuming you employ a builder…

The VAT Rules are in VAT Notice 708 Buildings & Construction

Your builder may be able to charge you VAT at the reduced rate of 5 per cent if you are converting premises into:

- a ‘single household dwelling’

- a different number of ‘single household dwellings’

- a ‘multiple occupancy dwelling’, such as bed-sits, or

- premises intended for use solely for a ‘relevant residential purpose’

As your builder will be VAT registered, they reclaim the VAT they are charged and then charge you VAT at 5%.

If your business is property rental and you do the work yourself, you can’t take advantage of the 5% rate.

If your Development Company is VAT registered you can reclaim all the VAT.

4 Do you need to charge VAT on Intercompany Charges

There are situations where one company is VAT registered and other related companies are either partially exempt or not registered for VAT, so in these circumstances not charging VAT is an advantage.

The following are not Taxable supplies for VAT:

Common Directors – Notice 700/34 (May 2012)

Joint Employment – Notice 700/34 (May 2012)

Paying a Bill on behalf of an associated business

Insurance

5 Use VAT Groups for Business Acquisition Costs

Basically HMRC disallow Input VAT relating to Investments.

The most well known example of this was when BAA purchased Airport Development Investments Limited in June 2006, the decision was upheld by the Court of Appeal in February 2013.

The BAA VAT group sought to recover the VAT (£6.7m) incurred on the acquisition costs but recovery was refused by HMRC on the basis that they considered ADIL had not made onward taxable supplies, had not demonstrated any intention to make taxable supplies and was not a member of the VAT group at the time costs were incurred.

BAA used an SPV (Ferrovial) to purchase ADIL but did not bring the SPV into the BAA VAT Group until September 2006, 3 months after the acquisition.

The lessons to learn from this are:

- Once you have successfully made the acquisition join a VAT Group immediately and make it clear in correspondence that the SPV intends to join the VAT Group at the earliest opportunity

- Consider not using an SPV

- Buy the Assets instead of the Shares

- Show that the SPV will make taxable management charges

- Consider the scope of the advisors work, HMRC may disallow advice focussed on passively holding shares

6 How Hotels save VAT

Here are some VAT examples for Hotels – HMRC Reference:Notice 709/3 (October 2011) :

The Long Stay Rule

If a guest stays in your establishment for a continuous period of more than 28 days, then from the 29th day of the stay you should charge VAT only on that part of the payment that is not for accommodation.

VAT Exempt Meeting Rooms and Refreshments

Hiring a room for a meeting, or letting of shops and display cases are generally exempt, but you may choose to standard-rate them by opting to tax, see Notice 742A Opting to tax land and buildings.

VAT on Deposits

Most deposits serve as advanced payments, and you must account for VAT in the return period in which you receive the payment. If you have to refund a deposit, you can reclaim any VAT you have accounted for in your next return.

Normally, if you make a cancellation charge to a guest who cancels a booking, VAT is not due, because it is compensation.

7 VAT on Pool Cars

When you buy a car you generally can’t reclaim the VAT. There are some exceptions – for example, when the car is used mainly as one of the following:

- a taxi

- for driving instruction

- for self-drive hire

If you lease a car for business purposes you’ll normally be able to reclaim 50 per cent of the VAT you pay. But you can reclaim 100 per cent of the VAT if the car is used exclusively for a business purpose.

8 Use a Tronc for Tips

Tips are outside the scope of VAT when genuinely freely given. This is so regardless of whether:

• the customer requires the amount to be included on the bill

• payment is made by cheque or credit/debit card

• or not the amount is passed to employees.

Restaurant service charges are part of the consideration for the underlying supply of the meals if customers are required to pay them and are therefore

standard rated.

If customers have a genuine option as to whether to pay the service charges, it is accepted that they are not consideration (even if the amounts appear on the invoice) and therefore fall outside the scope of VAT.

Further information is available from: Notices 700 The VAT guide and 709/1 Catering and takeaway food

9 Get your TOGC right – Transfer of a Going Concern

Normally the sale of the assets of a VAT registered or VAT registerable business will be subject to VAT at the appropriate rate. A transfer of a business as a going concern for VAT purposes (TOGC) however is the sale of a business including assets which must be treated as a matter of law, as ‘neither a supply of goods nor a supply of services’ by virtue of meeting certain conditions. Where the sale meets the conditions then the supply is outside the scope of VAT and therefore VAT is not chargeable.

It is important to be aware that the TOGC rules are mandatory and not optional. So it is important to establish from the outset whether the sale is or is not a TOGC.

The main conditions are:

- the assets must be sold as part of the transfer of a ‘business’ as a ‘going concern’

- the assets are to be used by the purchaser with the intention of carrying on the same kind of ‘business’ as the seller (but not necessarily identical)

- where the seller is a taxable person, the purchaser must be a taxable person already or become one as the result of the transfer

- in respect of land which would be standard rated if it were supplied, the purchaser must notify HMRC that he has opted to tax the land by the relevant date, and must notify the seller that their option has not been disapplied by the same date

- where only part of the ‘business’ is sold it must be capable of operating separately

- there must not be a series of immediately consecutive transfers of ‘business’

The TOGC rules are compulsory. You cannot choose to ‘opt out’. So, it is very important that you establish from the outset whether the business is being sold as a TOGC. Incorrect treatment could result in corrective action by HMRC which may attract a penalty and or interest.

10 Choose the best time to register for VAT

You may decide to voluntarily register to reclaim VAT you have paid out to set up you business or you might decide to wait till you have to register to gain a competitive advantage.

You must register for VAT if:

- your VAT taxable turnover is more than £82,000 (the ‘threshold’) in a 12 month period

- you receive goods in the UK from the EU worth more than £82,000

- you expect to go over the threshold in a single 30 day period

steve@bicknells.net

Beware of letting your accounts become a shambles

It’s not uncommon for Directors and Senior Employees to get behind with their expense claims and paperwork, they are busy people trying to build their businesses and sometimes the paperwork gets put to one side.

But lets consider the recent HMRC case against the Directors of RSL (NorthEast) Ltd. Mr White was Director of RSL and he had a company credit card which he used for business and personal expenses, he travelled extensively on company business. Unfortunately RSL became insolvent, so HMRC assessed Mr White on credit card expenses as a benefit in kind.

Mr White appealed on the basis that he had lent the company large amounts of his own money and any credit card expenses were just a reimbursement.

HMRC argued…

- “Section 203(2) ITEPA does not grant any right to retrospectively make good a benefit. Income tax is an annual tax, and the value of the benefit depends upon what is made good in that tax year.”

- “Any “rewriting” [to reflect the money reimbursed to RSL] would have a retrospective effect on the Company accounts.” HMRC implied that this would not be allowed.

HMRC won the case, but mainly because the accounts were in a terrible shambles!

What can we learn from this?

- Keep good records, don’t put off doing your accounts!

- If you do get behind you do a have a ‘reasonable time to make good’ as noted in HMRC’s manuals http://www.hmrc.gov.uk/manuals/eimanual/EIM21121.htm

How do you switch over to Sage One?

So you’ve made the decision, its time to move to Cloud Accounting and you’ve choosen Sage One, what do you need to do to move your accounts to Sage One?

You need to start by deciding the best time to move, it could be your Year End or the end of VAT Quarter, but its likely to be on the 1st of a month.

Get some help, why not find a Sage One accountant and ask them to help you set up your Sage One, they might even offer you a deal and include your other accounting and tax needs.

Then you need to create your Contacts – Customers & Suppliers.

Then you enter opening balances – for example unpaid supplier invoices.

You also need to set up your Bank Feeds

http://uk.sageone.com/bank-feeds/

http://help.sageone.com/en_uk/accounts/extra-bank-feeds.html

To set up bank feeds

1. Banking > click the required bank account.

2. Manage Bank Account > Connect to Bank.

You enter your closing Trial Balance from your old accounting system on the last day of the month before your Sage One start date.

Keep the records and prints from your old accounting system for reference.

Then you are ready to get started, its all very easy and straightforward, nothing to worry about.

steve@bicknells.net

How do you calculate holiday pay for occasional workers?

Almost all workers are legally entitled to 5.6 weeks’ paid holiday per year (known as statutory leave entitlement or annual leave). An employer can include bank holidays as part of statutory annual leave.

Self-employed workers aren’t entitled to annual leave.

But what if your workers work irregular hours, or are part time, or are casual occasional workers, how can you work out how much paid holiday they are entitled to, well actually its not as hard as you think, its based on an accrual of 12.7% per hour worked, here is a spreadsheet to help you calculate it.

Calculating average hourly rate

To calculate average hourly rate, only the hours worked and how much was paid for them should be counted. Take the average rate over the last 12 weeks. If no pay was paid in any week, count back a further week, so that the rate is based on 12 weeks in which pay was paid.

steve@bicknells.net

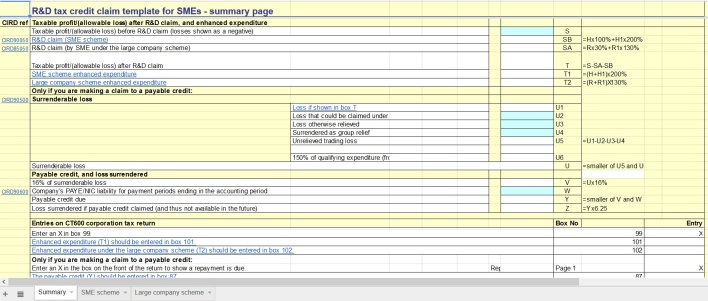

Why aren’t you claiming R&D Tax Credits?

R&D Relief is a Corporation Tax relief that may reduce your company or organisation’s tax bill.

Alternatively, if your company or organisation is small or medium-sized, you may be able to choose to receive a tax credit instead, by way of a cash sum paid by HM Revenue and Customs (HMRC)

But your company or organisation can only claim R&D Relief if it’s liable for Corporation Tax.

The Small and Medium-sized Enterprise Scheme

This scheme has higher rates of relief. Since 1 April 2015, the tax relief on allowable R&D costs is 230% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £130 on top of the £100 spent. It also includes a payable credit in some circumstances.

The Large Company Scheme

If your company isn’t small or medium-sized, then you can only claim under the Large Company Scheme.

Since 1 April 2008, the tax relief on allowable R&D costs is 130% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £30 on top of the £100 spent. If instead there’s an allowable trading loss for the period, this can be increased by 30% of the qualifying R&D costs – £30 for each £100 spent. This loss can be carried forwards or back in the normal way.

Government Statistics show a steady growth in claims

Construction Examples of R&D

- The investigation into the removal of contamination from sites, including land remediation

- Advancements in structural techniques that aid construction relating to unusual ground conditions

- The innovative use of green or sustainable methods and technology

- Development or adaptation of tools to improve efficiency

- The use of new or unique materials, e.g. recycled products

- Improvement on existing construction methods or development of new ideas to solve ongoing issues related to the site environment or project specifications

- Innovative architectural design

IT Systems Examples of R&D

- The design, construction and testing of systems, devices or processes e.g. new hardware or software components, digital interface and control systems

- Integration of legacy and new systems e.g. following a corporate merger or acquisition, the adoption of an Enterprise Architecture or externally with partners in joint ventures

- Advances in network management and operational tools, development of wired or wireless technologies, designing mobile and interactive services, evolution of new generation network switching and control systems

- Data intensive activities e.g. the collection, storage and analysis, distribution and retrieval. Defining or working with new or emerging data models and metadata standards, integration with third party content

These examples and more are shown on the Cost Care Website

There are also examples by Industry on the Alma CG website

http://www.taxdonut.co.uk/blog/2014/12/beginners-guide-claiming-rd-tax-credits-infographic

These are the key questions that you will be asked when requesting an R&D Tax Credit from HMRC:

- How was it decided that R&D had taken place

- A description of the scientific & technological advance sought

- The uncertainties involved

- How and when the uncertainties were resolved

- Why the knowledge being sought was not readily deducible by a competent professional

- Were any grants, subsidies or contributions received for the project within the claim

- Who owns the Intellectual Property of the products resulting from the R&D

- Was the R&D carried out for others ie clients, this could mean your claim is rejected

This HMRC Spreadsheet will help you calculate your Claim

steve@bicknells.net

How do you become self employed?

The UK saw the fastest growth in self-employment in Western Europe in 2014, according to the Institute for Public Policy Research (IPPR).

The number of self-employed workers rose by 8%, faster than any other Western European economy, and outpaced by only a handful of countries in Southern and Eastern Europe.

The IPPR’s analysis shows that the UK – which had low levels of self-employment for many years – has caught up with the EU average. If this growth continues, it says, the UK will look more like Southern and Eastern European countries which tend to have much larger shares of self-employed workers.

Your responsibilities

You’re responsible for:

- keeping records of your business’s sales and expenses

- sending a Self Assessment tax return every year

- paying Income Tax on your profits and Class 2 and Class 4 National Insurance – use HMRC’s calculator to help you budget for this

- your business debts

- bills for anything you buy for your business

- registering for VAT if your turnover reaches the VAT threshold

- registering with the Construction Industry Scheme (CIS) if you’re a contractor or sub-contractor in the construction industry

Naming your business

You can use your own name or trade under a business name – read the rules for naming your business.

You must include your own name and business name (if you have one) on any official paperwork, like invoices and letters.

When should you get help from an Accountant?

Often business owners wait too long before they realise that they need help from an accountant.

Key reasons are:

– not understanding the difference between a book keeper and an accountant

– thinking that an accountant will just be an extra cost – the reality is that most accountants will save the business many times their cost

– thinking that accountants are just bean counters.

But if you choose a qualified and experienced accountant they can bring huge benefits: management tools to improve profitability, cost controls, tax savings, growth strategies, business planning, business structures and much more. So don’t wait too long – getting an accountant should be a priority for all businesses!

Common Mistakes

First off – not having a separate bank accounts. Many start ups try mixing business and personal transactions in their personal bank accounts, its a total nightmare, don’t do it, get a business bank account. Mixing things up will almost certainly have tax implications.

Not registering for tax or filing returns is another one. Getting things right at the beginning is extremely important and a CIMA Accountant can make sure that you choose the right business structure and will help you register for VAT, PAYE, CIS and other taxes. Choosing the right VAT scheme will save you tax. Not registering and filing returns will have severe consequences and lead to fines and penalties.

Also – contract mistakes. Ask your Accountant to review your contracts, they will be able to give you lots of useful tips.

Running out of cash: draw up a Budget and Cashflow and forecast how much cash you will need to run the business, looking at your cash cycle and managing it will be vital. If you need funding ask your Accountant for help, they will be able to look at all the options and help you choose the option that’s best for your business.

Accounting – many start ups fail to keep control of their accounting, by working with an accountant and using Debitoor or Sage One you can avoid this problem.

steve@bicknells.net

What are the tax implications if a company pays a Directors personal expenses?

It’s not uncommon for Directors personal expenses to get mixed up with business expenses, for example the director is out buying things for the company and picks up some items for themselves at the same time and it goes on the same bill.

In a perfect world the Director would just repay the cost of personal purchases to the company, but we don’t live in perfect world, so what are the options?

Directors Loan Account

You could post the cost to the Directors Loan Account. These accounts are normally repaid when the Director is paid either salary or dividends.

If the loan is not cleared by year end then the company will have to pay a temporary corporation tax charge of 25% and reclaim the tax when the loan is repaid using form L2P

There may also be a notional amount of interest (4%) charged as a benefit in kind on the loan.

Benefit In Kind

You could have the expenses as a benefit in kind, some benefits may even be tax free, here is a list of my favourite tax free benefits

- Pensions – Up to £40k can be paid in to you pension scheme by your employer (2015/16) and you can use carry forward to pay in even more

- Childcare – Up to £55 per week but check the rules to makesure your childcare complies (HMRC Leaflet IR115) – new rules coming soon

- Mobile Phone – One per employee

- Lunch – Tax Free Lunch Blog

- Cycle Schemes – Cycle to Work Blog

- Fitness – Fitness Blog

- Parties and Gifts – Christmas Blog

- Parking – Parking Blog

- Business Mileage Allowance – 45p for the first 10,000 miles then 25p

- Long Service Award – A bit restrictive as you need 20 years service, the tax free amount is £50 x the number of years

- Eye Tests and Spectacles – The Eye Test must be needed under the Health & Safety at Work Act

- Suggestion Schemes – Suggestion Scheme Blog

- Insurance such and Death in Service and Income Protection – Medical Insurance Blog

- Travel Expenses – Travel Blog

- Working From Home – Working from Home Blog

Private Use of Company Assets

It may also be worth considering private use of company assets.

- The cost of the asset is allowed against Corporation Tax and you can claim Capital Allowances and the Annual Investment Allowance.

- The Assets could be purchased from the Director but they must be transferred at Market Value.

- The Benefit In Kind is generally 20% of the market value

steve@bicknells.net