Home » IR35

Category Archives: IR35

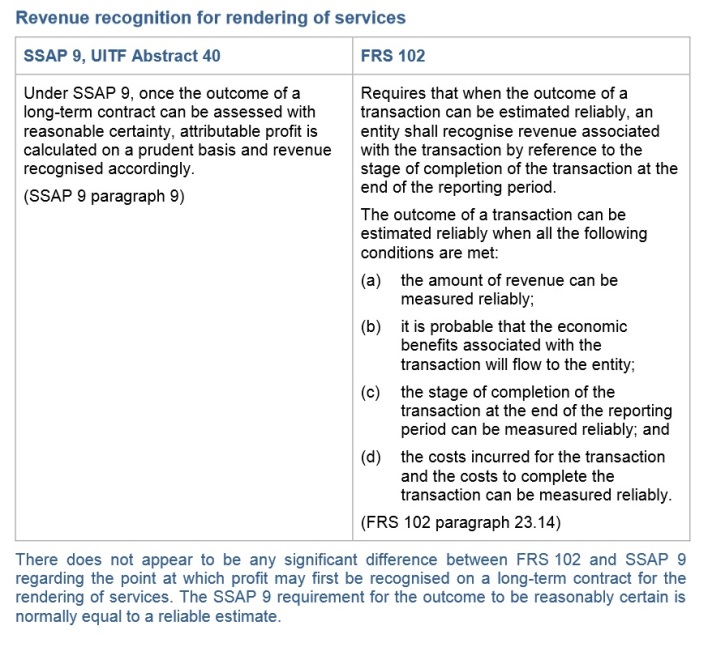

When should you recognise revenue on services provided?

The International Accounting Standard IAS 18 states

‘where the outcome of a transaction involving the rendering of services can be estimated reliably, associated revenue should be recognised by reference to the stage of completion of the transaction at the end of the reporting period’ . In other words, the revenue is recognised gradually, rather than all at one ‘critical point’, as is the case for revenue from the sale of goods. IAS 18 further states that the outcome of a transaction can be estimated reliably when all the following conditions are satisfied:

(a) The amount of revenue can be measured reliably.

(b) It is probable that the economic benefits associated with the transaction will flow to the seller.

(c) The stage of completion of the transaction at the end of the reporting period can be measured reliably.

(d) The costs incurred to date for the transaction and the costs to complete the transaction can be measured reliably.IAS 18 does not prescribe one single method that should be used for determining the stage of completion of a service transaction. However the standard does provide some examples of suitable methods:

(a) Surveys of work performed.

(b) Services performed to date as a percentage of total services to be performed.

(c) The proportion that costs incurred to date bear to the estimated total costs of the transaction.If it is not possible to reliably measure the outcome of a transaction involving the provision of services (perhaps because the transaction is in its very early stages) then revenue should be recognised only to the extent of costs incurred by the seller, assuming these costs are recoverable from the buyer.

In the UK UITF40 and SSAP9 defined the way we report revenue and profit in relation to Services, although accountants and lawyers were among the most high profile casualties of the new regime back in 2005, which forced them to re-catagorise WIP and Revenue, many other service providers also had to consider how they accounted for income. Professionals such as surveyors, architects, doctors and dentists all had to consider the impact of the new rules on their tax liabilities.

FRS102 has not changed the rules.

steve@bicknells.net

New reporting requirements for intermediaries

An intermediary is any person who makes arrangements for an individual to work for a third party or be paid for work done for a third party. An employment intermediary is also commonly referred to as an agency.

From 6 April 2015, intermediaries must return details of all workers they place with clients where they don’t operate Pay As You Earn (PAYE) on the workers’ payments. The return will be a report (or reports) that must be sent to HM Revenue and Customs (HMRC) once every 3 months.

Agencies will be required to let HMRC know the following details:

- Contractor’s name, address, date of birth, etc.

- PAYE reference.

- National Insurance number.

- How the contractor was engaged during the period (i.e. was he working via a limited company).

- The duration of each assignment.

- Details of the contractor’s limited company (e.g. company registered number).

- How much was paid to the contractor.

The regulations will give HMRC information that will enable it to decrease false self-employment and abuse of offshore working. This will help HMRC to:

- support intermediaries that comply

- penalise intermediaries that don’t comply

- make sure the right tax and National Insurance is paid by people working through intermediaries

- reduce unfair commercial advantage

Here is link to the full reporting requirements – Legislation Link

This is the link to consultation – Consultation

steve@bicknells.net

Would an online IR35 test help?

The Term “IR35” became established following a Budget press release issued by the Inland Revenue on 23rd September 1999. That press release was called “IR35”. At its simplest, IR35 is the way in which the taxman closed a loophole that was allowing many contractors and freelance professionals to avoid paying large amounts of Tax and National Insurance.

In 2012 HMRC put forward the Business Tests but they haven’t been as successful as first thought.

Here are the 12 tests, scores shown in()

- Business premises (10)

- PII (2)

- Efficiency (10)

- Assistance (35)

- Advertising (2)

- Previous PAYE (minus 15)

- Business plan (1)

- Repair at own expense (4)

- Client risk (10)

- Billing (2)

- Right of substitution (2)

- Actual substitution (20)

A score less than 10 is high risk and a score more than 20 is low risk. Fail the test and it could cost you a great deal in tax.

In general the key test tend to be:

- Substitution

- Control

- Financial Risk

HMRC launched the ESI (Employment Status Indicator) a while ago.

The recently published Minutes of the IR35 Forum’s last meeting held on 24th July reveal that HMRC are keen for contractors to be able to assess their employment status by way of the Employment Status Indicator (ESI) tool.

Will this resolve the IR35 Status problems?

steve@bicknells.net

We love Self Employment in UK…..

The UK has seen the fastest growth in self-employment in Western Europe over the past year, according to the Institute for Public Policy Research (IPPR).

The number of self-employed workers rose by 8%, faster than any other Western European economy, and outpaced by only a handful of countries in Southern and Eastern Europe.

The IPPR’s analysis shows that the UK – which had low levels of self-employment for many years – has caught up with the EU average. If current growth continues, it says, the UK will look more like Southern and Eastern European countries which tend to have much larger shares of self-employed workers.

According to Tax Research UK…

Something like 80% of all the new jobs created since 2010 are, in fact, self-employments, and there are a number of things that very significantly differentiate self-employments from jobs.

The first is security: there is none.

The second is durability: vast numbers of new small businesses fail, which is one reason why I doubt the official statistics. I am sure they record the supposed start-ups correctly but seriously doubt if they have properly counted the failures.

Then there is the issue of pay. The evidence is overwhelming that in recent years earnings from self-employment have, on average, declined significantly.

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

In summary, why is it attractive to use Self Employed Freelancers?

- Skill is more important than location in many business sectors – we live in world where internet can allow you to work with anyone at anytime, you can now track down the best person to work with even if they live thousands of miles away

- Lower fixed costs – Using Freelancers will lower your fixed costs (in similar way to Zero Hours Contracts), you employ them for a specific project and only pay for what you need so there isn’t any surplus capacity

- Tax advantages – Freelancers run their own business and that means they pay less tax than employees. Employers save tax too, such as Employers NI.

- Competitive Advantage – You can put together a team for a contract rather than finding contracts that fit your workforce, this means you can hire the best.

- 110% Commitment – A Freelancers success and future work depends on them performing to the highest level on every contract, failure is not an option for a successful contractor.

So do you think self employment is good for the UK?

Are you ready for the OTS to check your employment status?

Contractor Weekly reported on th 29th July 2014…

As part of the ongoing mission to create a simpler and fairer tax system the Office of Tax Simplification (OTS) has been tasked with carrying out reviews of employment status and also tax penalties, with a view to producing a report in time for next year’s Budget.

According to the OTS, the boundary between employment and self-employment no longer reflects modern working patterns, particularly in recent years. Many people have multiple jobs and can be classed as employed in one whilst self-employed in another. The rise of the freelancing business model has also caused some to suggest this is a ‘third way’ between employment and self-employment.

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

It will be interesting to see the report that the Office of Tax Simplification (OTS) produce, especially if they find a ‘third way’

steve@bicknells.net

What is your status – Self Employed or Employed?

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

If a worker should be an employee HMRC will seek to recover the employment taxes from the employer not the worker, so there are considerable risks for the employer if the status of its workers is wrongly assessed.

Some employers might decide to insist that sub-contractors must be limited companies, as companies can’t not be reclassified as employees.

The sub-contractor would then need to assess whether IR35 applies to their contract. If IR35 does apply then please read this blog on Deemed Payments

steve@bicknells.net

Service Company – Yes or No

It’s time to run your first RTI PAYE year end and you have your own limited company, how do you answer this question?

| Service Company | ‘Yes’ if you are a service company – ‘service company’ includes a limited company, a limited liability partnership or a partnership (but not a sole trader) – and have operated the Intermediaries legislation (Chapter 8, Part 2, Income Tax (Earnings and Pensions) Act 2003 (ITEPA), sometimes known as IR35). Otherwise indicate ‘No’. |

The question is now a bit more specific, which is great, because you will only answer ‘Yes’ if you have operated IR35.

steve@bicknells.net

What are the implications of being a Service Company? Q1 Page TR4 SA100

Here is the question:

If you provided your services through a service company (a company which provides your personal services to third

parties), enter the total of the dividends (including the tax credit) and salary (before tax was taken off) you withdrew

from the company in the tax year – read page TRG 21 of the guide

£ • 0 0

This is what the guide says:

Service companies

Box 1 If you provided your services through a service company

Complete this box if you provided your services through a service company.

You provided your services through a service company if:

• you performed services (intellectual, manual or a mixture of both) for a client (or clients), and

• the services were provided under a contract between the client(s) and a company of which you were, at any time during the tax year, a shareholder, and

• the company’s income was, at any time during the tax year, derived wholly or mainly (that is, more than half of it) from services performed by the shareholders personally.

Do not complete this box if all the income you derived from the company

was employment income.

http://www.hmrc.gov.uk/worksheets/sa150.pdf

The majority of limited company contractors are, by definition, ‘personal service companies’ and therefore this box is of relevance.

The question however has no statutory backing and you cannot be penalised for failing or refusing to answer it but if contractors ignore the question when HMRC know full well that their company is a ‘service company’ then they may be drawing unnecessary attention to themselves.

The information to be entered is the total of the gross salary and dividends taken from the contractor’s company in the year ended 5th April 2012.

http://shop.qdosconsulting.com/freelancer/news/2013/01/18/psc-question-on-sa-return

The point is not the whether you answer the question or not, its whether your company falls under IR35 that matters most.

IR35 came into existance in 1999, it was created to prevent workers previously employed from creating a limited company and then benefiting from lower taxes and national insurance through the use of dividends and expenses.

So you think you are self employed, does HMRC agree?

http://stevejbicknell.com/2012/01/28/so-you-think-you-are-self-employed-does-hmrc-agree/

Can your business pass the HMRC IR35 Business Entity Tests

http://stevejbicknell.com/2012/05/14/can-your-business-pass-the-hmrc-ir35-business-entity-tests/

Consultants beware of IR35

http://stevejbicknell.com/2011/09/10/consultants-beware-of-ir35-use-the-qdos-model-contract-free/

steve@bicknells.net

Key Points from the Autumn Statement 2013

The Chancellor George Osborne presented the Autumn Statement to the House of Commons on 5th December 2013 and things are getting better, economic growth forecasts for this year have more than doubled from 0.6% to 1.4% but the austerity plan is set to continue.

Here is a summary of the key announcements:

Business Rates

Business rate increases in England will be capped at 2% in 2014/15 (they were set to increase by 3.2%) and businesses will be able to pay over 12 months rather than 10.

The Retail Sector will also get a £1,000 discount in 2014/15 and 2015/16, this applies to pubs, cafes, restaurants and charity shops with a rateable value below £50,000.

A reoccupation relief of 50% is being introduced for up to 18 months on premises that have been empty for a year or more and it will apply from 1st April 2014 to 31st March 2016.

Small Business Rate Relief has been extended to April 2015 under the scheme small businesses with a rateable value of £6,000 or less can get 100% relief, the relief is scaled down to zero on rateable values of £12,000 and there is a lower multiplier on rates between £12,001 and £17,999.

Income Tax

As previously announced the personal allowance will be £10,000 for the tax year 2014/15.

From April 2015, a spouse or civil partner who is not liable to income tax will be able to transfer £1,000 of their allowance to a basic rate tax paying spouse and as a result save £200 in tax.

State Pension Age

By 2020 it will be 66, by 2028 it will be 67 and by mid 2030′s 68, then in 2040′s 69.

Capital Gains Tax

The annual exempt amount will be £11,000 for individuals for 2014/15.

But there was an exemption for principle private residence letting for 36 months and from 6th April 2014 it will be reduced to 18 months.

Consultation will start in April on non-residents paying capital gains on property disposals.

Individual Savings Account (ISA)

The limit will rise to £11,880 for 2014/15 and of this £5,940 can be invested in cash ISA’s

Mortgage Guarantee Scheme

The scheme started in October will run for 3 years and end in January 2017.

Buyers will only need a 5% deposit and the government and the funder will guarantee 15% of the loan in return for a fee.

IR35

Legislation will be tightened from April 2014.

Anti-avoidance

A range of measures were discussed in addition to IR35 and these included:

- Partnership Tax

- Controlled foreign companies

- Charities

- High risk tax avoidance schemes

- Dual contracts

Other headline measures

- Employers NI for under 21′s to be scrapped in 2015

- Rolling back green levies to allow an average saving of £50 on energy bills

- Free school meals for infants

- Scrapping of 1% above inflation rail fare increases

- Electronic tax discs

- Abolition of next years 2p per litre fuel duty rise

steve@bicknells.net

IR35 – How are deemed payments taxed?

The Intermediaries legislation known as IR35 was introduced on 6th April 2000.

The aim of the legislation is to eliminate the avoidance of tax and National Insurance Contributions (NICs) through the use of intermediaries, such as Personal Service Companies or partnerships, in circumstances where an individual worker would otherwise –

- For tax purposes, be regarded as an employee of the client; and

- For NICs purposes, be regarded as employed in employed earner’s employment by the client.

Many Freelance Contractors have some assignments within IR35 and some outside, you can ask HMRC for their opinion.

If you would like HMRC’s opinion on a particular engagement you should send your contract(s) to:

IR35 Customer Service Unit

HMRC

Ground Floor North

Princess House

Cliftonville Road

Northampton

NN1 5AE

e-mail: IR35 Unit

Tel No: 0845 303 3535 (Opening hours 8.30am to 4.30pm, Monday to Friday. Closed weekends and bank holidays) Fax No: 0845 302 3535

If your contract is within IR35 its not the end of the world, the chances are that you will still pay less tax than a direct employee, to calculate the tax you have to work through 8 stages of calculation, here is a summary:

- How much were you paid? deduct 5% for business costs

- Add any other payments/non cash benefits

- Deduct business expenses – travel, meals, accommodation

- Deduct capital allowances relevant to the work done

- Deduct pension contributions made by your company

- Deduct any NIC paid by your company on your salary and benefits

- Deduct any salary or benefits already paid and taxed

- If the answer is zero or negative then there is no deemed payment, if the answer is positive you do have a deemed payment which will be taxable

HMRC have a spreadsheet you can download which has further details.

steve@bicknells.net