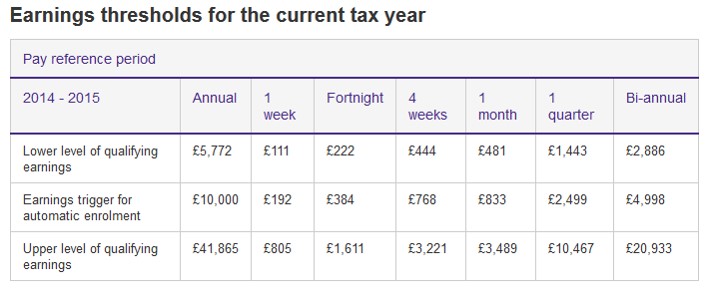

These are defined as sums which you pay to an employee in connection with his or her employment. They can be salary, wages, commission, bonuses, overtime. Statutory sick pay and maternity/paternity/adoption pay are included too. Benefits in kind (known as P11D benefits), for example, car and fuel, and tips and gratuities do not have to be included. In 2014/2015 Qualifying Earnings are earnings between £5772 and £41,865.

Employers are only required enrol employees earning over the Earnings Trigger of £10,000 (subject to age criteria) but employees can opt in once they earn above the lower level. According to Payroll and Benefits Magazine...

The AE process can be very administration-heavy and, unlike Real Time Information, employees and workers will have to be continually assessed. For example, employers will need to continuously monitor their workforce to identify when a jobholder must be automatically enrolled. In particular, the employer will need to monitor a worker’s age because this may trigger AE and opt-in activity.Although small employers will need at least six months before their staging date to prepare for AE, larger ones may need between 12 and 18 months.AE does not only apply to employees, but also to workers, including contractors who provide services on a personal basis but not as a company.

Zero Hours Contracts and fluctuating payments will add to the complication of assessing those employees who need to be enrolled.

steve@bicknells.net