Home » Small Business

Category Archives: Small Business

How do you switch over to Sage One?

So you’ve made the decision, its time to move to Cloud Accounting and you’ve choosen Sage One, what do you need to do to move your accounts to Sage One?

You need to start by deciding the best time to move, it could be your Year End or the end of VAT Quarter, but its likely to be on the 1st of a month.

Get some help, why not find a Sage One accountant and ask them to help you set up your Sage One, they might even offer you a deal and include your other accounting and tax needs.

Then you need to create your Contacts – Customers & Suppliers.

Then you enter opening balances – for example unpaid supplier invoices.

You also need to set up your Bank Feeds

http://uk.sageone.com/bank-feeds/

http://help.sageone.com/en_uk/accounts/extra-bank-feeds.html

To set up bank feeds

1. Banking > click the required bank account.

2. Manage Bank Account > Connect to Bank.

You enter your closing Trial Balance from your old accounting system on the last day of the month before your Sage One start date.

Keep the records and prints from your old accounting system for reference.

Then you are ready to get started, its all very easy and straightforward, nothing to worry about.

steve@bicknells.net

Job opportunity at Alterledger

Trainee Accountant Vacancy

We are pleased to announce that another job opportunity at Alterledger has opened up for a Trainee Accountant.

Training for Chartered Management Accountant

If you have graduated in the last year and are looking for your first job after university there are some fantastic opportunities in Glasgow including a position at Alterledger as Trainee Accountant.

Related articles

Alterledger moved to Legal House

New office for Alterledger

Alterledger has been growing consistently over the last few years and the time has come to move into new office premises. Alterledger is now based at Legal House, 101 Gorbals Street, Glasgow G9 5DW

Growing the business and the team

We are pleased to announce that Graham has joined the team as Trainee Accountant and will be working through his ACCA qualifiation. For more information, please visit the Alterledger website.

Related articles

Small Business Saturday 2015 – Register Now!

The UK’s most successful small business campaign, Small Business Saturday, has been launched and this year it will be on Saturday 5th December.

In 2014, approximately 16.5 million adults supported at least one small business on Small Business Saturday, with almost two-thirds (64 per cent) of the British people aware of the campaign.

The organisers say…

We want all kinds of small businesses to get involved, so know that whether you are a family business, local shop, online business, wholesaler, business service or small manufacturer, Small Business Saturday is supporting you!

Small Business Saturday UK is a grassroots, non-commercial campaign, which highlights small business success and encourages consumers to ‘shop local’ and support small businesses in their communities. The day itself takes place on the first shopping Saturday in December each year, but the campaign aims to have a lasting impact on small businesses. In 2015 Small Business Saturday will take place on Saturday, December 5th.

Sign up and get involved https://smallbusinesssaturdayuk.com/

steve@bicknells.net

Goodwill is not so good for tax

Until the Summer Budget 2015 when you purchased a business (not its shares) into a limited company from an unrelated party you could write off the goodwill (Intangibles) against your corporation tax but that has now changed and you can’t, another tax relief bites the dust!

The Policy Statement reads as follows…

In accounting terms, purchased goodwill is the balancing figure between the purchase price of a business and the net value of the assets acquired. Goodwill can therefore be thought of as representing the value of a business’s reputation and customer relationships.This measure removes the tax relief that is available when structuring a business acquisition as a business and asset purchase so that goodwill can be recognised. This advantage is not generally available to companies who purchase the shares of the target company. The current rules allow corporation tax profits to be reduced following a merger or acquisition of business assets and can distort commercial practices and lead to manipulation and avoidance. Removing the relief brings the UK regime in line with other major economies,reduces distortion and levels the playing field for merger and acquisition transactions.

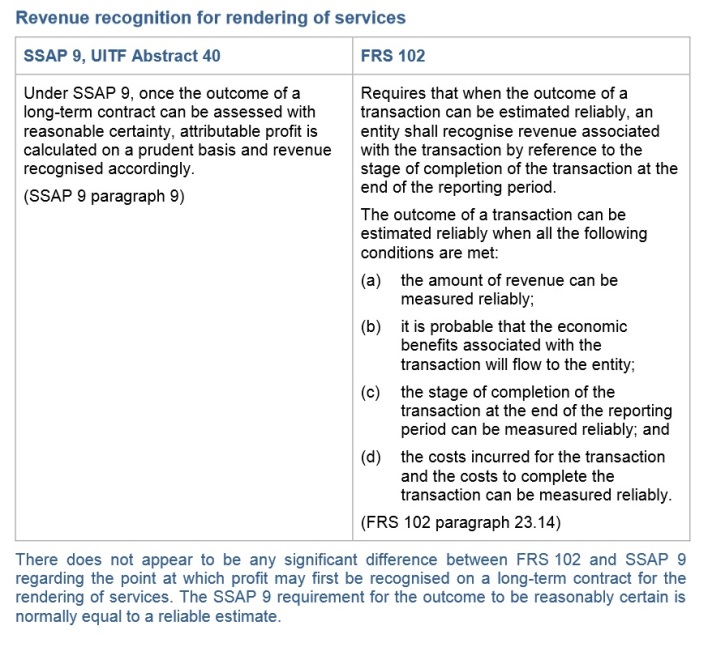

When should you recognise revenue on services provided?

The International Accounting Standard IAS 18 states

‘where the outcome of a transaction involving the rendering of services can be estimated reliably, associated revenue should be recognised by reference to the stage of completion of the transaction at the end of the reporting period’ . In other words, the revenue is recognised gradually, rather than all at one ‘critical point’, as is the case for revenue from the sale of goods. IAS 18 further states that the outcome of a transaction can be estimated reliably when all the following conditions are satisfied:

(a) The amount of revenue can be measured reliably.

(b) It is probable that the economic benefits associated with the transaction will flow to the seller.

(c) The stage of completion of the transaction at the end of the reporting period can be measured reliably.

(d) The costs incurred to date for the transaction and the costs to complete the transaction can be measured reliably.IAS 18 does not prescribe one single method that should be used for determining the stage of completion of a service transaction. However the standard does provide some examples of suitable methods:

(a) Surveys of work performed.

(b) Services performed to date as a percentage of total services to be performed.

(c) The proportion that costs incurred to date bear to the estimated total costs of the transaction.If it is not possible to reliably measure the outcome of a transaction involving the provision of services (perhaps because the transaction is in its very early stages) then revenue should be recognised only to the extent of costs incurred by the seller, assuming these costs are recoverable from the buyer.

In the UK UITF40 and SSAP9 defined the way we report revenue and profit in relation to Services, although accountants and lawyers were among the most high profile casualties of the new regime back in 2005, which forced them to re-catagorise WIP and Revenue, many other service providers also had to consider how they accounted for income. Professionals such as surveyors, architects, doctors and dentists all had to consider the impact of the new rules on their tax liabilities.

FRS102 has not changed the rules.

steve@bicknells.net

Who will takeover if the controlling shareholder dies?

What happens in the event of serious illness or death of a controlling shareholder?

Every business should have a plan in place. Normally illness and capacity will not change the voting rights but death will.

Usually the companies articles of association will contain rules which authorise the executors of a deceased shareholder to register as the share owners until they transfer them to the beneficiaries. This is often not the best solution.

A better way is to prepare a shareholders agreement which sets out what will happen.

Its worth considering:

- pre-emption rights – these arrange automatic transfer to named shareholders

- purchase rights – these will allow the company to buy back the shares from the beneficiaries

If you haven’t got a plan, make one before its too late

steve@bicknells.net

The Beauty of a well Designed and Executed Process

Whilst consulting down in London for a client, I pop out quite frequently for lunch at a small local Cafe / ‘Wrap- bar’. The establishment is only about 8.5 square metres in size, and customers queue outside in long lines sometimes to get served. Obviously the wraps they serve up at lunch time are very good, but it the process that the proprietor has established, that has struck me as so novel.

R&D – impact on director remuneration

Example

You are the sole director in a company that undertakes some R&D. The annual profit is estimated at £140,000 for the year ended 31 March 2016 before taking into account the director’s remuneration.

You might think that the most tax-efficient remuneration package is £10,600 for 2015/16 to cover the personal allowance and then net dividends of £28,606 to take the director up to the basic rate band. You also need to consider whether the company can make an R&D relief claim and, if it can, how this might affect your decision.

Salary vs Dividends

If the director takes a typical remuneration package, then the net tax and NI savings over taking a salary of £39,206 would be £5,265, assuming the £2,000 employment allowance is available. This saving is made because dividends received within the basic rate band attract no further income tax plus no NI for the director or the company. This more than outweighs the additional corporation tax suffered on profits retained for dividends.

Taking R&D relief into account

From 1 April 2015 the R&D tax credit for SMEs increased from 225% to 230%. There is no R&D uplift on dividends received – only on salary. This means that paying a £39,206 salary would actually result in a saving over taking a small salary and dividends of £1,208.

What about a larger salary? In fact, if the client wanted to take out more than the basic rate band, then the salary may become even more tax efficient. A £70,000 salary would result in net tax/NI due of £1,366 after the R&D relief (assuming there was sufficient profit to offset the CT relief), whereas a salary of £10,600 and net dividends of £59,400 would result in net tax/NI of £5,883 – so the saving by taking a salary over dividends is £4,517.

HMRC will generally not accept 100% of a director’s salary costs within the R&D claim unless it can be clearly demonstrated that the director was exclusively involved in R&D activity.

Pension contributions

While dividends don’t qualify as eligible staff costs for R&D claims, company pension contributions do. New pension freedoms make pension contributions a much more attractive option, so you might want to consider this as part of your remuneration package.

If a company makes pension contributions of £40,000 for the director and they spend 60% of their time on R&D, the R&D relief on this will be £55,200 (£40,000 x 60% x 230%). This means that the overall CT saving on the pension contribution will be £14,240 (((£40,000 x 40%) + £55,200) x 20%). As there’s no NI due on pension contributions, this is an even more efficient option than taking additional salary.

Get the best deal for yourself

For advice on the best split between salary and dividends or help with setting up a limited company and registering for VAT, please contact Alterledger.

Related articles

Hobby Trading Losses

Losses and profits

You might think that HMRC is being unfair in refusing loss relief, but if your activity is a hobby you won’t have to pay tax on profits either. This rule can be tricky as revealed in the case of P, when HMRC dismissed his claim for loss relief.

Trade or personal loss?

HMRC challenged P’s claim at a tribunal because in its view it related to non-business transactions and so was a personal financial loss and not one arising from a trade. Non-trading losses can’t be set against taxable income and it’s not just HMRC being difficult.

Trading tests

HMRC and tax specialists refer to the so-called “badges of trade” to decide if a trade exists. These tests were set out in a court judgment decades ago, but remain valid today. One of the tests to establish if a trade exists is that there must be an intention to make profit from a business. In P’s case the tribunal extended this test a little further.

Incapable of making a profit

P started two “businesses”, neither of which made a profit because, in the tribunal’s view, he was inexperienced and couldn’t devote enough time to them. Neither venture was capable of making a profit without P reducing the hours he spent in his main job. In essence P didn’t have the business acumen or time to devote to making his business profitable.

Putting the boot on the other foot

The ruling in P’s case is useful, not just for guidance on when losses are deductible, but for countering HMRC if it claims money you make from a hobby is taxable. Its view has always been that if you advertise your hobby in a newspaper or online you’re probably trading. But the tribunal’s judgment, supported by HMRC, dispelled that idea. If you don’t have the time or intention to carry on a trade, profit you make from isolated sales isn’t liable to income tax.

Turn your hobby into a business

For advice on converting your hobby to a profitable business, including help with setting up a limited company or registering for VAT, please contact Alterledger.