Home » Selling a Business

Category Archives: Selling a Business

Sole Traders lose Goodwill Tax Relief

Since 6th April 2008 and until 3rd December 2014 Sole Traders and Parternships were able to claim Entrepreneurs Tax Relief on Goodwill when becoming a Limited Company.

Until the 3rd December 2014 they would claim there Capital Gains Allowance

| Period | Tax-free allowance |

|---|---|

| 5 April 2013 to 6 April 2014 | £10,900 |

| 5 April 2014 to 6 April 2015 | £11,000 |

Then claim ER which reduced the rate of tax to 10% on the gain.

But from the 3rd December they will now pay Capital Gains at the normal rates of CGT which are 18% or 28% (for Higher Rate Income Tax Payers).

This doesn’t change the potential ability of the company to offset goodwill against their Corporation Tax Return.

There are still other benefits related to goodwill as explained in this blog

The tax benefits of goodwill on incorporation?

steve@bicknells.net

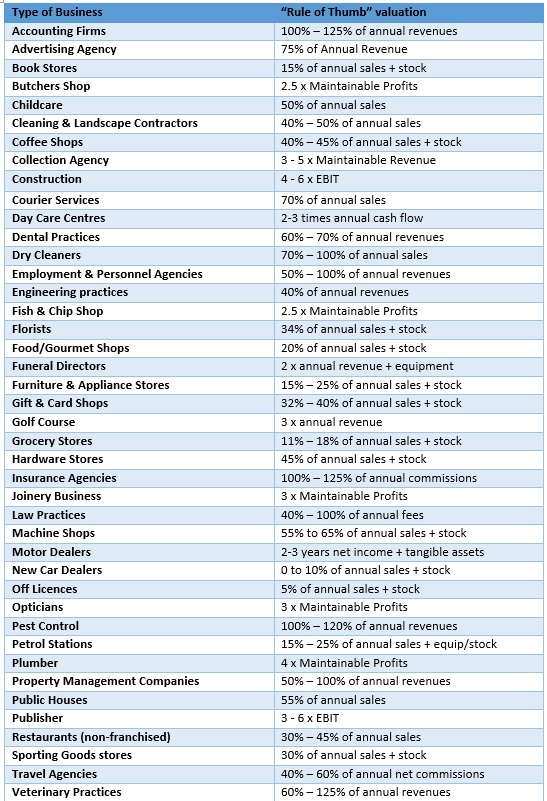

42 Business Valuation “Rules of Thumb” – are they right?

I often get asked for ‘Rules of Thumb’ for small businesses, so I have searched the internet and compiled this list, do you agree with the ‘Rules’?

Rules of Thumb are just a starting point and many other factors need to be considered in valuing a business, it also worth considering HMRC’s views (not so good for Chefs and Hairdressers)..

Any goodwill attributable to the personal skills of the proprietor, for example the personal skills of a chef or a hairdresser, will not be transferred to the new proprietor. Advice should be obtained from the CG Technical Group if it is claimed that the goodwill attributable to the personal skills of the proprietor have been transferred with the business because his/her services have been retained for the foreseeable future by means of an employment contract. All of the relevant facts and circumstances should be established before referral to the CG Technical Group.

http://www.hmrc.gov.uk/manuals/cgmanual/cg68010.htm

steve@bicknells.net

Free access to accounts filed at Companies House

60% of the 3.5 million companies in the UK now file accounts electronically and you can access those accounts free of charge via http://companies.corefiling.com/search

Paul Driscoll is a Chartered Management Accountant, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and AJ Tensile Fabrications Limited, and is a board level adviser to a variety of other businesses.

Planning to retire!

How many of us know what our business needs to achieve to deliver against our personal goals in the long term?

We all know that the state pension will be unlikely to meet our retirement needs in full. Most of us will be looking for our businesses to provide a safety net of income/capital value to make sure our retirements are secure.

However, as Steven Covey says you have to start with the end in mind. This means that you have to plan NOW to ensure you get out of your business what you need for the future.

If, like me, your business is largely centred on you as an individual your business is unlikely to be worth very much to someone else when you decide to stop. This means that your business needs to earn enough for you to make decent pension contributions now to fund your retirement.

If your business employs other people to deliver the product/service then you may be able to sell your business to realise value when you retire. However, you can only maximise this value if you start to plan several years ahead. It is vital that you can distance yourself from the business and that it can run without you, for example.

Whatever your goals it is never too early to start positioning your business so it is in the best position to meet them. If you don’t, you may find your retirement dreams end in cash strapped nightmares.

Fiona 🙂

The most tax efficient way for a contractor to close their business

Consultants who work as contractors often build up funds their limited companies, they do this as a safe guard because being a contractor, there can be gaps between contracts and they will need cash to carry themselves through to the next contract.

But what if they decide to retire or they get offered their dream job as an employee, they may have lots of assets and cash in their company, perhaps more that £25,000.

They might even find that their main client insists they become employees for example

Some of the BBC’s biggest freelance stars could be asked to join the payroll or leave the corporation, as a new test aims to clear up tax issues.

It is part of a clampdown on the use of personal service companies (PSCs) and a move to tax more freelancers at source.

How could they close the company and use Entrepreneurs Tax Relief to pay 10% tax?

- The Insolvency Practitioner will ask the Contractor’s Accountant to confirm that the clients tax affairs are inorder and that appropriate advice has been given

- Final Accounts will need to be prepared and creditors paid

- A Declaration of Insolvency will be signed – The declaration of insolvency demonstrates that the company will be able to settle or secure liabilities and the costs of liquidation within 12 months

- A meeting of Shareholders will appoint the Insolvency Practitioner

- Notices will be posted at Companies House and in the London Gazzette

- Then the MVL can be a carried out and funds distributed

- Arrangements can be put in place to allow the directors access to funds during the process

Why would you liquidate a solvent company?

If you have a company which is no longer needed you have the following options:

- You can just keep it as a Dormant company

- You could strike it off at Companies House

- You could carryout a Members Voluntary Liquidation

If the company has assets the shareholders will want to release the assets and get hold of the money, so keeping it Dormant isn’t going to help.

Since March 2012, in the case of Strike Offs, ESC C16 has allowed the distribution of up to £25,000 as a Capital Distribution rather than as Income.

However, if you have assets in excess of £25,000 distributions can only be treated a Capital if the distributions are made through a formal liquidation.

With Entrepreneur’s relief, money paid to shareholders will only be subject to tax at 10% on the capital gain.

There could also be other benefits too.

steve@bicknells.net

Not another accountant!

I was asked by a prospective client, “Why should I hire another accountant to work with me on this transaction when my firm already employs a qualified accountant and retains a firm of auditors?”

It was a good question and probably one that many SME owners would ask under similar circumstances. I was pretty sure of the answer, but wanted to avoid the usual clichés, such as “you only sell your business once”, “you have to get it right first time” and “there is too much money at stake to take a chance on inexperienced advice”, however they are the main reasons why and they did form part of the response.

I explained that not all accountants are experienced in all matters. An accountancy qualification provides an excellent introduction to the world of business, but accountants tend to specialise like any other profession, and this is one of my key areas of expertise.

The owner in question knew that his in-house accountant did a great job of running the day-to-day finances of the business, handling the sale and purchase transactions, managing the payroll and producing monthly reports. He also looked after most other things relating to the administration of the business, such as property and insurance, but the owner also knew in his heart that his accountant had never sold a business before and had no idea what it entailed. He also knew his auditors were competent at producing year-end accounts and preparing his tax returns, but they had no direct experience of preparing a business for sale or making important presentations to maximise its sale value from prospective acquirers.

The owner had talked to his corporate finance advisor and had listened carefully to the advice offered – the extraordinary workload, the amount of detail, the intrusive due diligence that would examine every part of the business, the negotiation of terms with seasoned acquirers and the potential impact of all of these on his time, the day-to-day running of the business and how much he might get out of the transaction.

The bottom line was that the owner knew that he needed to strengthen his team for the duration of the project and that was the reason he and I were having the discussion.

He listened carefully whilst I gave him my estimate of the value of the business based on its current earnings and the sort of multiples he could expect from trade and private equity buyers.

I compared and contrasted the different acquisition rationale of trade buyers and private-equity buyers, and I talked about the process and timescales, including the possibility of an extended timescale if the acquirer needs more time to make certain, i.e. to get another month’s or quarter’s trading on the slate.

I also explained how the owner might secure more money through an earn-out if the business did better than expected and I highlighted what the potential acquirers would be looking for, i.e.

- the quality of earnings,

- the relationships with customers,

- the market potential,

- the possibility for vertical or horizontal expansion,

- the geographic reach,

- the white space around existing markets and sectors

- the strength of the business model,

- the size of the pipeline,

- the skills of the people,

- the integrity of the business processes,

- the control over cash management,

- the robustness of financial forecasts,

- the performance against budgets,

- the treatment of expenditure,

- the cash conversion of sales and profits,

- the level of investment required to sustain and grow the business

We discussed these at length and I felt comfortable that we were having a fruitful discussion about important aspects of his business and I sensed that he was reassured by what I said and how I could help him address these issues.

I also said that I had looked at the company’s website and noted job vacancies, details of contracts secured, strategies for expansion etc., and I asked how these were going. I explained that everything in the public domain needed to be verified, so that there were no inconsistencies and no empty promises – everything needed to withstand scrutiny.

The owner made meticulous notes throughout, after all – it was sound advice – and free!

Business owners are savvy people, they know that good advice is important and a trusted advisor is something very special.

However, returning to the story.

Did I get the job? Yes, I did.

Did he make a lot of money? Yes, he did. He is a very happy client!

If you found the article interesting then maybe you would like to share it, or if you would like to comment then I would be delighted to hear from you either on this site or at mjones@finexec.co.uk

3 reasons why businesses are sold

When you think about it, there are really only 3 reasons why a business owner would want to sell their business:

Cashing In

Sometimes the the value of your business could be over inflated, remember the dot com bubble. Throughout history there have been times when the price that a buyer is prepared to pay is huge compared to normal business valuation models.

When: March 11, 2000 to October 9, 2002

Where: Silicon Valley (for the most part)

Percentage Lost From Peak to Bottom: The Nasdaq Composite lost 78% of its value as it fell from 5046.86 to 1114.11.

Imminent Threat

This can be caused by many things:

- New Legislation

- Loss of Resources

- Increased Competition

- Loss of Banking Facilities

Basically the seller will be aware that a problem is looming and they want to sell before the problem damages their business.

Life Changes

From a buyers perspective these are often the best businesses to buy, the key reason behind the sale being:

- Retirement

- Relocation

- Life Style

- Selling due to Illness

- New Business Opportunity

steve@bicknells.net