Did you know Life Cover is now classed as a business expense?

Life Insurance is now tax-free and classified as a business expense.

Offering death in service benefits to you or your employees ensures they don’t have to worry about their loved ones should the unthinkable happen. Whether you’re a company director who wants to offer it to you and your staff, or contractor who wants it for your own family, Life Insurance has always come with hefty tax implications. But that’s no longer the case.

Changes mean big savings.

As a director or a contractor you probably aren’t aware of ‘A Day’ and why would you be. Back in April 2006 there was a big change in legislation (known as ‘A Day’). Though this was over a decade ago many people still aren’t aware of the significant savings involved.

Here’s what ‘A Day’ means for you:

-

Life Insurance premiums are not taxed on the employee as a P11.

-

Premiums can be offset as a business expense.

More affordable for contractors and Directors.

Known as Relevant Life policies, they are much more generous tax-wise. If you are a self-employed contractor or Director, you probably pay for your premiums out of your own pocket. However, you can now put them down as a business expenses, thereby saving money on tax. In the unfortunate event that your loved one has to claim, then the lump sum received is also usually free of income and inheritance tax too (unlike traditional Life Insurance policies).

Better business sense for company directors.

If you’re a company director, the tax savings can be considerable and offer a great deal of flexibility. Not only can they be classed as a business expense, they can also be taken out as a single Relevant Life policy to cover all your employees. This is done in the form of a discretionary trust, with the company paying one premium each month to cover all the relevant families/dependents. The savings for doing it this way can be for significant for your business.

- Your current monthly premiums paid personally by you from your take-home pay are £50.00.

- With tax at 20% and NI of 12%, to net this amount your gross pay would need to be £73.53

- Including employers NI at 13.8% the total cost to your company to net this amount is £83.68

- This amounts to £1,004 annually, and with 25 years remaining on the policy the total is £25,103

- By having your company take over the payment of the premiums for you, you could reduce your salary by £73.53without it making any difference to your disposable income

- After 20% corporation tax relief, the cost to the company is only £12,000 instead of £25,103

- By switching to a Relevant Life Policy, the ONLY change to your circumstances is an extra £13,103 in your company profits

Standard rate taxpayers NI at 12%, higher rate taxpayers NI at 2%, employers NI at 13.8%

Providing you’re not a sole trader or an equity partner, Relevant Life Plans can offer almost all types of employees the benefits of Life Cover but with significant tax savings.

If you would like to know more about how you can become a Relevant Life Expert partner and accuratly inform your clients please email us: advice@relevantlifeexpert.co.uk or to speak to an adviser please call 01202 700053

Three reasons why Directors love Relevant Life cover

If you’re a Director, you may already have Life Insurance to look after your loved ones after you’re gone. In return for paying a monthly premium, it pays out a lump sum to help look after them. But many contractors are switching to a product called Relevant Life cover, because it is much more cost-effective. Here’s why.

- It’s classed as a business expense.

Unlike traditional Life Insurance, which you pay out of your own pocket, Relevant Life cover can be classed as a business expense. That means the monthly costs can be put through your books, making it eligible for tax savings.

- You can save up to 100% of the cost personally.

No matter what your tax bracket is, you could save 100% on the cost of your life cover by placing the plan on company expenses. Taken over 25 years this adds up to a considerable amount. For instance, if you pay a £50 premium each month, this makes a total of £15,000 over 25 years (average mortgage term). But by switching to a Relevant Life policy, you’d save 100% of this cost, enough for a very nice holiday…

- The lump sum isn’t taxed.

The problem with traditional Life Insurance is that when your loved one makes a claim, they may find that the sum paid out isn’t quite as much as they thought. This because it’s subject to inheritance tax. However, providing your Relevant Life policy is sent up correctly by an expert, the benefit paid out won’t be taxed, so they’ll get the full amount.

What to do next?

The benefits of Relevant Life cover are plain to see, but with any cover, factors can vary a great deal depending on who you are and your policy provider. It is important to choose a policy that fits you and the needs of your loved ones, and this is where we can help. We know all there is to know about getting you a policy that fits you down to the ground and saves you money.

If you are an accountant and have clients you think would be interested in Relevant Life why not drop us a line on how you can become a Relevant Life Expert partner.

Use our online calculator to find out how much you could save: http://www.relevantlifeexpert.co.uk/

To speak to and adviser today, please call 01202 700053

Send us an email: advice@relevantlifeexpert.co.uk

A Guide to Trusts and Tax Efficient Life Insurance

![]()

- Place 100% of the cost of your life cover on company expenses (even if you have existing plans in place to protect your mortgage or income – swap and save)

- Benefit from 20% corporation tax relief on the cost of the premium

- No alteration to your P11D status

- The policy is written into trust from outset

- Life cover and terminal illness benefit included

- The policy can be moved between businesses or converted into a policy paid from your personal account if circumstances change

- The average we save our clients is £15,000 over the lifetime of their plan simply by swapping to a Relevant Life Plan

Accountants are the key to small business success

Steve J Bicknell Tel 01202 025252

Last week the ICAS reported based on IFAC research..

SMEs were shown to traditionally rely on accountants as a main source of business advice. One study identified an 8.1% average increase in sales growth and a 29% decrease in likelihood of failure for businesses using an external accountant.

Also last week smallbusiness reported that 1.3 million britons want to start their own business.

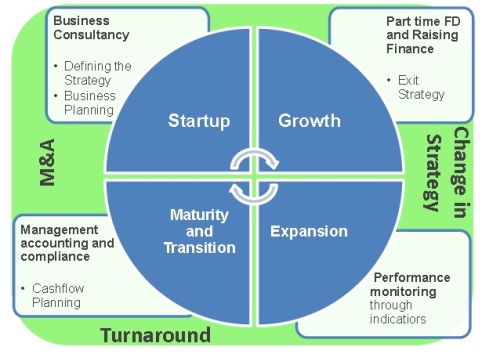

So when would a business need to contact an external accountant?

- Business Plans

- Budgeting and Forecasting

- Cash Flow Management

- Buy or Rent decisions

- Capital Investment Appraisal

- Accounting Procedures and Systems

- Business Strategy

- Busines Funding and Investment

- KPI’s

For start ups its particularly important to ask your accountant to help with:

- Choosing the right business structure for your business – most businesses start out as sole traders but once they start making profits convert to limited companies, this is because sole traders pay more tax than company structures

- Choosing the…

View original post 43 more words

Life Insurance isn’t as expensive as you might think – especially if your company pays for it with Relevant Life Expert.

So, whether you are already paying for life insurance out of taxed income or you have not yet got around to putting vital life insurance in place, a Relevant Life policy could be the most tax-efficient solution.

For more information, contact Relevant Life Expert on 01202 700053 or request your free impartial quote here: http://rlp.relevantlifeexpert.co.uk/relevant-life-expert/

“LIFE COVER WAS NOT SOMETHING I HAVE EVER THOUGHT ABOUT UNTIL I HAD CHILDREN. AS THE MAIN EARNER IN OUR FAMILY, I WAS CONSCIOUS THAT IF SOMETHING SHOULD HAPPEN TO ME, MY FAMILY WOULD BE LEFT IN A TRICKY FINANCIAL POSITION. WHEN I DISCOVERED I COULD ACCESS LIFE COVER IN SUCH A TAX-EFFICIENT WAY THROUGH RELEVANT LIFE EXPERT, I WAS SOLD!”

ABIGAIL WHITE

The plastic £5 is coming in September – what do you think? good or bad?

Steve J Bicknell Tel 01202 025252

The New Fiver was unveiled at Blenheim Palace on 2 June and will be shown to the public at a number of events across the UK this summer.

The New Fiver will enter circulation on 13 September. It will then take a few weeks for the notes to spread across the country to shops, businesses and banks.

In May 2017 paper £5 notes will cease to be legal tender and will no longer be accepted by shops and banks.

The three Scottish banks are also printing their next £5 and £10 notes on polymer. Clydesdale Bank will be issuing a polymer £5 on 15 September, the Bank of Scotland on 4 October and RBS in November 2016. The Royal Mint will be issuing a new £1 coin in March 2017.

Future banknotes

The New Fiver is the first of the Bank of England’s new series of…

View original post 170 more words

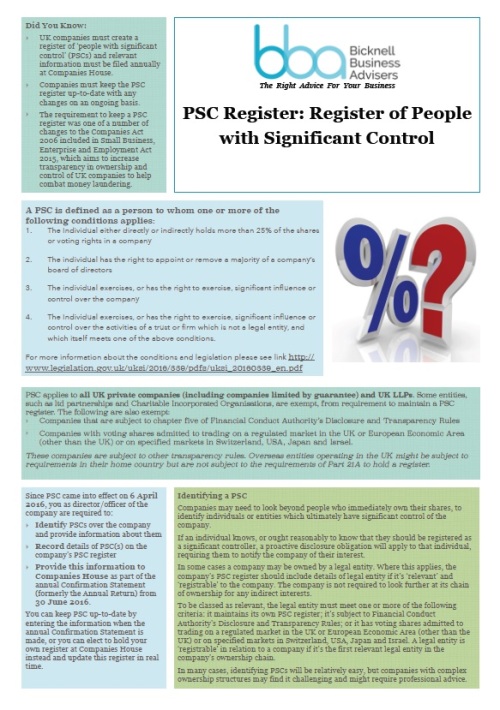

Are you PSC ready?

Steve J Bicknell Tel 01202 025252

From the 30th June 2016 all companies will be required to prepare a PSC Register.

You need to start keeping a register of your people with significant control (PSC).

A PSC is someone in your company who:

- owns more than 25% of the company’s shares

- holds more than 25% of the company’s voting rights

- holds the right to appoint or remove the majority of directors

- has the right to, or actually exercises significant influence or control

- holds the right to exercise or actually exercises significant control over a trust or company that meets any of the other 4 conditions.

You’ll need to keep your PSC as part of your company register, as these need to be available for inspection.

Failure to comply will result in fines and up to 2 years in prison!

steve@bicknells.net

HMRC have raised over £500m in unpaid tax and penalties!

Steve J Bicknell Tel 01202 025252

Taskforces are specialist teams that undertake intensive bursts of activity in specific high risk trade sectors and locations in the UK. The teams will visit traders to examine their records and carry out other investigations.

HM Revenue and Customs (HMRC) taskforces have recovered more than £500 million since they were launched five years ago.

The targeted bursts of enforcement activity have brought in progressively higher amounts every year, and the total now stands at more than £540 million. This includes nearly £250 million raised in 2015-16 alone, almost double the previous year’s yield.

Since 2011, HMRC has launched more than 140 taskforces targeting sectors that are at the highest risk of tax fraud including the retail sector, the tobacco industry and the adult entertainment industry.

Jennie Granger, Director-General for Enforcement and Compliance at HMRC, said:

The message is clear: if you try to cheat on your tax…

View original post 365 more words

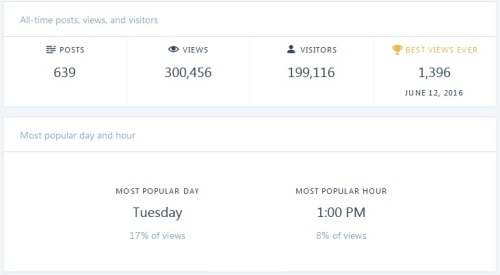

www.stevejbicknell.com blog smashes through 300,000 hits!

Steve J Bicknell Tel 01202 025252

http://www.stevejbicknell.com has now had over 300,000 views, nearly 200,000 unique visitors and on Sunday reached a new daily views high of 1,396 views in a single day!

I think that’s pretty impressive for a Tax and Accounting Blog!

We have over 7,000 followers and our most popular day is Tuesday and the best time is 1pm, which is interesting as last year it was Wednesday at 10am.

Our top 3 blogs of all time are:

- https://stevejbicknell.com/2012/04/07/a-quick-guide-to-vat-on-sandwiches-takeaway-food-cakes-and-pasties/

- https://stevejbicknell.com/2013/01/31/self-assessment-payment-shipley-or-cumbernauld/

- https://stevejbicknell.com/2012/12/15/when-should-you-charge-vat-on-inter-company-recharges/

January 2016 has had the highest monthly number of hits at 12,000

So why do people read my blog?

- Useful Content – I learned a long time ago that if you want followers and readers you have to write about things that will interest as wider audience as possible. My blog is about Accounting and Tax, which you might think is boring but it does affect everyone, we all pay tax! and…

View original post 207 more words

Photos can be bad for Business!

Steve J Bicknell Tel 01202 025252

Do you think photos are important? would you use a photo like this on Linked In?

What does your head shot say about you? Using a photo taken at a wedding or on holiday with a glass of wine in your hand, or one taken 20 years ago, maybe sending out the wrong message and costing you thousands in lost opportunties.

How you present yourself matters, with social media you are your own brand.

For example lets say you are an accountant.

- Accountants love Blue, 66% of accountants will choose blue and 55% of the top accounting practices use Blue in logos

- Accountants need to seen as experts

- They are reliable, organised, trustworthy and accurate

So would you choose this accountant? is being funny a skill you want in an accountant?

Or this accountant? Much more professional possibly a little too serious?

Your image really…

View original post 243 more words