Home » Business Funding

Category Archives: Business Funding

Business Planning made easy with Apps

A business plan helps you to:

- clarify your business idea

- spot potential problems

- set out your goals

- measure your progress

The problem with Business Plans is that they are time consuming to produce, so business owners put off doing them.

But new Apps might change this and make it much easier to produce high quality Business Plans.

http://www.enloop.com/features

There are other Apps too for example..

steve@bicknells.net

Do you have a great business proposal and strategy that will work?

Sometimes even the best ideas don’t get funding at first….

But if you have the right strategy you can still succeed, that’s why a business plan is really important

Approximately a third of all SME’s in the UK don’t have a Business Plan, that’s about 1.5m businesses, so if you don’t have one, here are some reasons why you should prepare one….

- Research by Exact Software shows that SME’s with Business Plans make 20% more profit

- Having a business plan doubles your chances of increasing profits, increasing revenue, attracting new clients

- A well-researched business plan which includes the right figures and realistic forecasts will reassure potential investors you are a sensible investment opportunity

- A Business Plan will help you set out and achieve your goals

- It will help you set goals for your managers and staff

- The Business Plan will help you plan your cash flow and forecast Capital Expenditure

- A Business Plan will help you secure Business Finance and Loans

- You can plan your succession strategy or prepare the business for sale

- A Business Plan tests the feasibility of your business idea

- It will help you plan for the recruitment of Staff

steve@bicknells.net

Growth Vouchers – last few days!

Apply before 31st March to get up to £2,000 from the Government for professional business advice

• Growth Vouchers are a grant from the Government to help businesses like yours get business advice from accredited advisers.

• The voucher match-funds your investment in professional advice for your business so you could get a grant of up to £2,000 towards the cost of the advice.

You can use the voucher to get advice on:

• Finance – and how to manage your cash flow better

• Recruiting staff – how to develop their skills

• Improving management and leadership skills

• Marketing – attracting and keeping customers

• Technology – and how your business can make the most of it.

https://www.gov.uk/apply-growth-vouchers

https://marketplace.enterprisenation.com/

steve@bicknells.net

Top 15 points in the Small Business Bill

The Small Business, Enterprise and Employment Bill is going through parliment now

The Bill will open up new opportunities for small businesses to:

- compete

- get finance to create jobs

- grow

- innovate

- export

Here are my top 15 key points:

- For every piece of legislative brought in two pieces will be removed

- Prompt Payment

- Changes to Childcare Early Years and Child Minder Registrations

- Cheque imaging from smart phones (Presentment of Cheques)

- Banks will share data on Small Businesses with other Lenders

- Invalidating restrictive terms in business contracts to increase access to Invoice Discounting

- Company Transparency – Register of People with Significant Control

- Accelerated Strike Off

- Company filing changes

- Directors Disqualification – tougher rules

- Schools, Colleges, Higher Education to track students into the labour force

- Penalties for employers who fail to pay an Employment Tribunal award

- Penalties for non compliance with National Minimum Wage increased to 100% or upto £20,000

- Improved access to alternative finance

- Streamlined Company Registration

These are major changes that will affect us all!

steve@bicknells.net

Why alternative finance could be the key to growth

MarketInvoice is the leading online invoice trading platform. They offer fast, flexible cashflow solutions to help businesses grow. Piers Garthwaite from MarketInvoice talks us through the opportunities alternative finance provides growing businesses.

The problem of funding for growing businesses is an all too common one. For any company to grow it needs medium-term financial support to hire new staff, increase supply, buy more equipment, move to a larger office etc. In this blog, we look at the options your client has to fund their business and why alternative finance could be the key to growth.

There are several ways clients can fund growth for their business:

- invest previous profits back into the business

- take out a loan

- raise equity

- look for other sources of finance

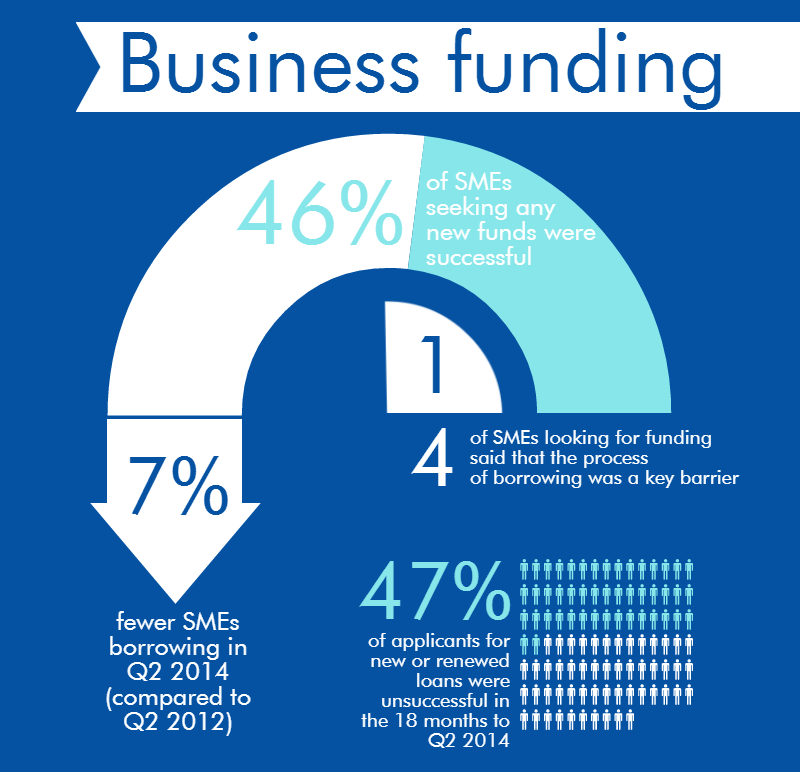

The majority of businesses’ first port of call will be to ask their bank for a loan. As we can see from the infographic, banks are not particularly keen on loans at the moment, given the economic environment.

52% of small businesses say that the availability of credit is “poor” or “very poor” and around half say that credit is unaffordable. In the same period, net lending to SMEs is down at -£400m.

This has been a long-term trend: businesses don’t want the products and banks aren’t keen on offering them. The banks’ policy of belt-tightening has affected growing businesses across the UK.

“So how,” we hear you ask, “am I to help my clients?”

Selling equity instead of a obtaining a loan is one option, but there are a number of disadvantages to this, chiefly your client giving up some control of their company.

Other sources of finance could be a grant, an overdraft (although this is unlikely to be big enough to cover any significant expense), leasing and asset finance, invoice factoring or discounting and, what we will be looking at in this blog, alternative finance.

Firstly, some statistics

The size of the alternative finance market is £1.74 billion. When compared with the banks this is, of course, a drop in the ocean. However, the market has been growing at over 150% year-on-year. The peer-to-peer (P2P) business lending market alone is £750 million and has grown at an average rate of 250% in the past three years. Online invoice trading sits at roughly £300 million, with a growth rate of 174%.

Alternative finance has now matured and is mounting an ever-growing assault on outdated, slow and fee-heavy traditional finance.

The industry-leading Nesta report backs up these findings. 33% of P2P business borrowers believed they would have been unlikely to get funds elsewhere. 63% also said that they saw a growth in profit and 53% saw an increase in employment.

What are the main draws?

For many, the main draws are what define alternative finance against the painful and outdated traditional banking experience:

- Speed: it can still take up to 6 weeks to get a loan. Alternative providers use technology to build automated credit scoring systems. With the amount of data available online, there is no reason for a business to have to wait more than 24 hours to be accepted (or declined) for finance.

- Simplicity and transparency: Standard contracts for bank finance are long and often have charges hidden in the Ts & Cs. Alternative finance tends to be more flexible and more transparent on everything, especially pricing. Most leading alternative finance providers have simple online tools to show how much your client will be charged dependent on the terms you choose.

- Service: Most alternative finance providers are run by entrepreneurs and so they have a natural propensity to understand the concerns and aspirations of small business owners looking to grow their business.

For a growing business to be able to access funding within 24 hours, instead of six weeks, could be crucial to its future success in the modern digital age. Additionally, being able to understand exactly what your clients are getting and at what price will help immensely with financial planning at such a critical stage of a business’ life.

Having explored some of the options available to your client, we hope it’s clear there is a plethora of funding opportunities on offer for small businesses.

You don’t need to be at a loss when considering funding options, even if the banks have said no. Financial support can be fast, simple and accessible and, therefore, the lifeline that a growing business needs at a crucial developmental stage.

If you’d like to find out more, visit MarketInvoice’s website or give them a call on 0845 548 0508.

Twitter: @MarketInvoice and @piersgarthwaite.

Government help to get new businesses started

The New Enterprise Allowance can provide money and support to help people start their own business if they get certain benefits and have a business idea that could work.

The scheme has resulted in:

- around 460 new businesses being set up each week – around 53,000 in total

- 12,360 businesses being started by people aged 50 or over

- 10,040 disabled people becoming their own boss

- 3,920 started by young people

People who don’t qualify for the scheme may be able to get other help with setting up a business.

Business Mentors have a key role to play

The New Enterprise Allowance is available to:

- people over 18 who are claiming Jobseeker’s Allowance

- lone parents on Income Support

- people on Employment and Support Allowance in the work-related activity group

People on the scheme get expert help and advice from a business mentor who will help them to develop their business idea and write a business plan. If the business plan is approved, they are eligible for financial support payable through a weekly allowance over 26 weeks up to a total of £1,274.

There are also Start Up Loans…

A government funded scheme to provide advice, business loans and mentoring to startup businesses

steve@bicknells.net

Would you borrow from PayPal?

The PayPal Working Capital fund will be trialled in the UK this autumn, with a more extensive rollout scheduled for 2015. Merchants (including eBay sellers) will be able to repay their advance with a share of their PayPal sales via card payments.

PayPal Working Capital is a loan of a fixed amount, with a single fixed fee. There are no due dates, minimum monthly payments, periodic interest charges, late fees, pre-payment fees, penalty fees, or any other fees. When you apply, simply select the amount you want — up to the maximum you qualify for. You choose the percentage of your sales that will be deducted from your PayPal account. (Deductions are made the day following each day of sales.) You’ll pay this percentage of your sales until your balance is repaid in full. You only make payments when you get paid.

PayPal Working Capital state that Working Capital offers major advantages compared with traditional ways of funding a business:

• Funding in minutes – PayPal’s strong relationship with its business customers means we can approve an advance based on their PayPal sales history. This means the customer completes a quick online application – there’s no need to spend hours gathering information about their business. And PayPal can make a decision and provide the funds in minutes.

• Pay when you get paid – Unlike traditional bank loans, PayPal Working Capital allows a business to repay the advance with a share of their PayPal sales. If they have a day without any PayPal sales that’s fine – they don’t repay anything that day.

• No credit check – PayPal Working Capital is a merchant cash advance against future sales – it’s not a loan – so no credit checks are needed and the advance does not impact on the customer’s business or personal credit record. There is a single, fixed fee that is displayed to the customer before they sign up. There are no interest charges or late payment fees.

Is this something your business will be able to use? or want to use?

steve@bicknells.net

SMEs reluctant to borrow…

High growth small and medium-sized enterprises (SMEs) are reluctant to seek finance from banks to fund growth, a study by the Institute of Chartered Accountants of Scotland (ICAS) has found.

The study found that high growth SMEs are “highly reluctant borrowers” because of their lack of trust in banks. Many firms also said they were unwilling to sacrifice their autonomy in order to access bank finance.

The study also found that high growth SMEs:

- are 9% more likely to seek bank finance than other SMEs but are no more or less likely to receive it

- prefer bank finance to equity finance

- are likely to use a ‘mixed cocktail’ of finance, including internal resources and debt.

The report, Funding issues confronting high growth SMEs in the UK, was launched to study the demand for finance among high growth SMEs and investigate the problems they encountered.

It focuses specifically on high growth SMEs because of their capacity for growth and employment.

To read more about the recommendations to increase the liquidity to SMEs http://www.grant-jonesaccountancy.com/news-item/smes-reluctant-borrow

Fiona@grant-jonesaccountancy.com

Would you like to borrow against a single invoice?

In August 2013, the UK Government became a Buyer of invoices on the MarketInvoice Platform, investing directly in UK SMEs looking to access working capital and grow their businesses.

Why is the Government investing funds through MarketInvoice?

The UK Government, via the Department of Business Innovation and Skills (‘BIS’) and as part of the ‘Business Finance Partnership’, has committed to using alternative finance providers to channel much needed growth funding to UK SMEs. The scheme is investing £1.2 billion into increasing lending to small and medium sized businesses from sources other than banks.

How does it work?

Any company can use MarketInvoice provided its sells goods or services to other large businesses.

Its a ‘pay as you go’ service and you can see the estimated costs by using their calculator

Companies are vetted and the invoice must be to a large corporate not to other SME’s.

Its confidential so your customer will not know you have used MarketInvoice, if the customer doesn’t pay you will have to refund the investor.

So far £163m of invoices have been funded by MarketInvoice.

Of course it would be better if customers always paid quickly!

steve@bicknells.net

65% of SME’s rejected for a loan want to try alternatives… would you

A government consultation ended last week into whether legislation should force banks to refer rejected loans to alternative sources of finance.

At present the largest four banks account for over 80% of UK SMEs’ main banking relationships. Many SMEs only approach the largest banks when seeking finance. Although a large number of these applications are rejected – in the case of first time SME borrowers the rejection rate is around 50% – a proportion of these are viable and are rejected simply because they don’t meet the risk profiles of the largest banks. There are often challenger banks and alternative finance providers with different business models that may be willing to lend to these SMEs.

Although the largest banks will sometimes refer these SMEs on, in many cases challenger banks and other providers of finance are unable to offer finance as they are not aware of their existence and the SMEs are not aware of the existence of these alternative sources of finance.

SME’s most trusted advisors are Accountants, according to Accountancy Age a fifth of SME’s are more open with their accountant than their bank manager and half believe that their Accountant is the most valuable source of business advice and just under half turn to their Accountant first for advise.

So why aren’t banks working more closely with accountants? I think its because its hard to work with individual accountants and build multiple relationships, its much easier to work with groups of accountants on a national basis such as www.business-accountant.com

Would you ask your accountant if you were looking for finance?

steve@bicknells.net