Home » Charities

Category Archives: Charities

Job opportunity at Alterledger

Trainee Accountant Vacancy

We are pleased to announce that another job opportunity at Alterledger has opened up for a Trainee Accountant.

Training for Chartered Management Accountant

If you have graduated in the last year and are looking for your first job after university there are some fantastic opportunities in Glasgow including a position at Alterledger as Trainee Accountant.

Related articles

Alterledger moved to Legal House

New office for Alterledger

Alterledger has been growing consistently over the last few years and the time has come to move into new office premises. Alterledger is now based at Legal House, 101 Gorbals Street, Glasgow G9 5DW

Growing the business and the team

We are pleased to announce that Graham has joined the team as Trainee Accountant and will be working through his ACCA qualifiation. For more information, please visit the Alterledger website.

Related articles

New Childcare Vouchers from Autumn 2015

Childcare vouchers to be withdrawn for new employees

The existing benefits available in the form of childcare vouchers to employees will be withdrawn to new entrants in the Autumn of 2015. The current scheme saves National Insurance contributions for both employers and employees. Employees also save income tax.

English: British National Insurance stamp. (Photo credit: Wikipedia)

New scheme to start in Autumn 2015

The new scheme for childcare vouchers will not be as good for many employees who currently benefit from the current scheme, but where both parents work and are self employed, they can get the government to pay £2,000 towards registered childcare.

How do I set up childcare vouchers?

Childcare vouchers are set up through your payroll scheme and must be available to all eligible employees to receive the tax benefit.

Alterledger can help

For more information on saving employer’s national insurance and preparing for changes to childcare vouchers, contact Alterledger or visit the website alterledger.com.

Related articles

Who cares what you think?

Are testimonials worth anything?

Many websites include “testimonials” from “customers”, but do they have any worth? If you want to attract new business it is good to be able to publish positive feedback, which helps demonstrate the value that other customers find in your service. The problem is that if reviews are obviously edited and self-selected they are not obviously representative of the views of your customers. Single line reviews taken out of context can be particularly misleading!

Use external review sites

One of the best-known review sites is tripadvisor. The greatest strength of these reviews is that hotels and restaurants etc have no control over the reviews. They have the opportunity to respond to criticism, but can’t cherry-pick the best reviews to give a false impression. The Pensions Regulator website is keen to point out that “private sector organisations we link to are not endorsed by Government and are provided for information only”; however it is worth noting that they include a link to VouchedFor on their advice page for individuals and in their guide to finding an advisor for Pension Auto Enrolment.

VouchedFor

If you are looking for a hotel you would probably prefer to check tripadvisor rather than lot of different websites for reviews. VouchedFor works along similar lines to tripadvisor, but for Accountants, Financial Advisors and Solicitors. Professionals who have a listing on the site must confirm that they recognise the name / email address of any reviewer before the review is posted online. Just like tripadvisor the professionals can’t read the review until is online so they can’t edit out any negative feedback and poor scores.

Tim Alter appeared in the guide in The Sunday Telegraph on March 29th. You can also read all his great client reviews on his VouchedFor profile!

Auto Enrolment

Many small businesses will need professional advice to help them set up a pension scheme to comply with Auto Enrolment regulations. If you are an employer and still need to prepare for your staging date, you can use an Accountant or Financial Adviser to guide you through the process. For help with setting up your payroll and preparing for your staging date, please contact Alterledger.

Related articles

Letters for under 21s

Changes for employees under 21

From 6th April 2015 employer national insurance contributions will be abolished for under 21s. If you employ anyone over 16 and under 21 years old you will need to use one of the new letters for under 21s in the national insurance category setting of your payroll software.

English: British National Insurance stamp. (Photo credit: Wikipedia)

Secondary contribution rates

This table shows how much employers pay towards employees’ National Insurance for tax year 2014 to 2015. The contribution rate calculated by your payroll software is set by the category letter.

| Category letter | £111 to £153

a week |

£153.01 to £770

a week |

£770.01 to £805

a week |

From £805.01

a week |

|---|---|---|---|---|

| A | 0% | 13.8% | 13.8% | 13.8% |

| B | 0% | 13.8% | 13.8% | 13.8% |

| C | 0% | 13.8% | 13.8% | 13.8% |

| D | 3.4% rebate | 10.4% | 13.8% | 13.8% |

| E | 3.4% rebate | 10.4% | 13.8% | 13.8% |

| J | 0% | 13.8% | 13.8% | 13.8% |

| L | 3.4% rebate | 10.4% | 13.8% | 13.8% |

National insurance categories

Most employees will have a category letter of A or D depending on whether or not they are in a contracted-out workplace pension scheme. There are categories for mariners and deep-sea fisherman; the more common categories are shown below:

Employees in a contracted-out workplace pension scheme

| Category letter | Employee group |

|---|---|

| D | All employees apart from those in groups E, C and L in this table |

| E | Married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| L | Employees who can defer National Insurance because they’re already paying it in another job |

Employees not in contracted-out pension schemes

| Category letter | Employee group |

|---|---|

| A | All employees apart from those in groups B, C and J in this table |

| B | Married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| J | Employees who can defer National Insurance because they’re already paying it in another job |

Employees in a money-purchase contracted-out scheme

This kind of scheme ended in April 2012 but some employees might still be part of one.

| Category letter | Employee group |

|---|---|

| F | Tax years before 2012 to 2013 only: all employees apart from the ones in groups G, C and S in this table |

| G | Tax years before 2012 to 2013 only: married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| S | Tax years before 2012 to 2013 only: employees who can defer National Insurance because they’re already paying it in another job |

How to claim zero rate of employer contributions

You should already have proof of age for all your employees. A copy of a passport, driving licence or birth certificate will be required to show that your employee qualifies for the new zero rate of employer’s contribution. The seven new categories are valid from 6th April and must be applied from the first salary payment after 5th April 2015 to benefit from the new zero contribution rate for employers.

What does this have to do with Auto Enrolment?

You need to have proof of age for all your employees aged under 21 to claim the zero contribution rate for employer’s National Insurance. By the time of your staging date you must assess all your workers, based on their earnings and age. To help you prepare for Pension Auto Enrolment you can make sure that all your employee records are up to date and that your payroll software has the full details for all workers including their date of birth. This is a good opportunity to clean up all your employee data.

Alterledger can help

For more information on saving employer’s national insurance and preparing for Pension Auto Enrolment, contact Alterledger or visit the website alterledger.com.

Related articles

The tax incentive to lend to Social Enterprises?

Social Investment Tax Relief (SITR) came in on 6th April 2014.

Individuals making an eligible investment at any time from 6 April 2014 can deduct 30% of the cost of their investment from their income tax liability for 2014/15 (or the relevant later year in which the investment is made). The minimum period of investment is 3 years.

The income tax and capital gain tax reliefs provide a substantial incentive for investors. To make sure new investment is directed to the organisations which need it most and to meet EU regulations, the investment and the organisation receiving it must meet certain criteria.

Organisations must have a defined and regulated social purpose. Charities, community interest companies or community benefit societies carrying out a qualifying trade, with fewer than 500 employees and gross assets of no more than £15 million may be eligible.

The tax relief is available on unsecured loans as well as shares.

So basically, if you are a basic rate tax payer using SITR will be better than Gift Aid.

Not only do you get the tax relief but if you give a loan it will be repaid (after 3 years).

steve@bicknells.net

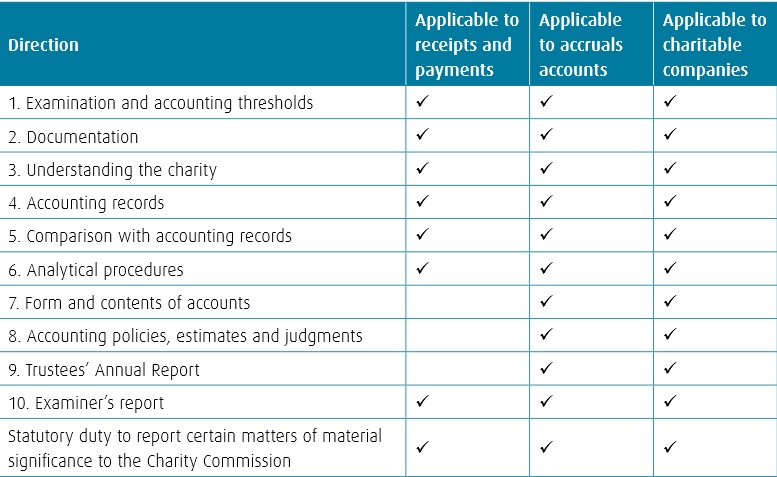

Are your charity accounts being correctly examined?

To maintain public confidence in the work of charities, charity law requires most charities (income over £10,000) to have an external scrutiny of their accounts. Provided a charity is not required by law or its governing document to have an audit then trustees may choose a simpler and less expensive form of external scrutiny called an independent examination.

Trustees may opt for an independent examination instead of an audit provided their charity’s gross income is not more than £500,000, or where gross income exceeds £250,000 its gross asset are not more than £3.26 million

Details in Charity notice CC31

Its estimated that approximately 90,000 UK charities require independent examination and that there are approximately 20,000 independent examiners.

The Charity Commission has a Framework in Notice CC32 to explain what the examiner needs to do

Common problems found by the charity commission include:

- The examiners report being signed by an organisation when in fact the must be signed by an individual

- Failing to address all the directives in the framework

- Insufficient scrutiny of the records

steve@bicknells.net

Maximising Gift Aid Donations

The end of the tax year is just a few weeks away.

Gift Aid donations are regarded as having basic rate tax deducted by the donor. Charities or CASCs take your donation – which is money you’ve already paid tax on – and reclaim the basic rate tax from HM Revenue & Customs (HMRC) on its ‘gross’ equivalent – the amount before basic rate tax was deducted.

Basic rate tax is 20 per cent, so this means that if you give £10 using Gift Aid, it’s worth £12.50 to the charity.

A Gift Aid declaration must include:

- your full name

- your home address

- the name of the charity

- details of your donation, and it should say that it’s a Gift Aid donation

If you pay higher rate tax, you can claim the difference between the higher rate of tax 40 and/or 45 per cent and the basic rate of tax 20 per cent on the total ‘gross’ value of your donation to the charity or CASC.

For example, if you donate £100, the total value of your donation to the charity is £125 – so you can claim back:

- £25 – if you pay tax at 40 per cent (£125 × 20%)

- £31.25 – if you pay tax at 45 per cent (£125 × 20%) plus (£125 × 5%)

You can make this claim on your Self Assessment tax return

If you are a higher rate tax payer donations made in 2013/14 will save tax at 45 percent, but in 2012/13 the rate was 50 per cent.

You can ask for Gift Aid donations to be treated as being paid in the previous tax year if you paid enough tax that year to cover both any Gift Aid gifts you made that year and the ones you want to backdate.

So if you want to donate now (before the end of the tax year) you could claim back extra tax by carrying it back into the previous tax year.

steve@bicknells.net

4 Things a charity needs to know about annual reporting

Image courtesy of Stuart Miles / FreeDigitalPhotos.net

Charities survive on their reputation.

Whether your charity is funded from voluntary donations, grant funding or commercial activities it is important that all funders can look up key information to check your organisation is working effectively. The annual reporting is time-consuming and potentially costly, but it is possible to restructure a charity to save on administrative costs.

1 – Charities must report to their regulator

Charities in England & Wales with an annual income of over £10,000 must report to the Charity Commission for England and Wales. Charities in Scotland must report to the Office of the Scottish Charity Regulator. The Charity Commission for Northern Ireland has recently been set up for the regulation of charities in Northern Ireland.

2 – Cross border charities must report multiple times

Under the Charities and Trustee Investment (Scotland) Act 2005 (the 2005 Act), bodies which represent themselves as charities in Scotland are required to register with OSCR. This requirement includes bodies which are established and/or registered as charities in other legal jurisdictions, such as England and Wales.

3 – Not all charities require an audit

Historically, the term ‘audit’ has been used loosely to describe any independent scrutiny of accounts. However, under the Charity Regulations if the term ‘audit’ is used in a charity’s constitution or governing document the charity must have its accounts audited by a registered auditor.

Charity Trustees may consider that the benefits of having an audit are outweighed by the costs. Trustees may wish to review their constitution and either:

- retain the term audit in their constitution or

- amend the constitution to require an independent examination of the accounts

Any change to the constitution must be carried out in accordance with the terms of the constitution and following professional advice. Notification of any change must also be sent to the charity’s regulator.

If an audit is not required by your members or governing document, an independent examination can be much more cost-effective than a full external audit and can be carried out by wider range of accountants and financial professionals including a member of the Chartered Institute of Management Accountants.

4 – Your current legal form may not be the best for you

Many charities have been set up with archaic governing documents and may be a Trust or Limited Company or other type of body, which is no longer suited to them. Trustees of Trusts and Unincorporated Associations are personally liable for the actions of a charity and expose themselves to a greater risk that Trustees of a Limited Company. Trustees of a Limited Company are required to report to Companies House as well as their charity regulator, increasing the administrative cost of the organisation.

A new legal form has been developed to allow charities to incorporate and report to just one body. Any Charitable Incorporated Organisation in England & Wales or Scottish Charitable Incorporated Organisation in Scotland is recognised as a corporate body which is a legal entity having, on the whole, the same status as a natural person.

This means it has many of the same rights, protections, privileges, responsibilities and liabilities that an individual would have under the law. As a legal entity, the CIO / SCIO may enter into the same type of transactions as a natural person, such as entering into contracts, employing staff, incurring debts, owning property, suing and being sued. As the transactions of the CIO / SCIO are undertaken by it directly, rather than by its charity trustees on its behalf, the charity trustees are in general protected from incurring personal liability in the same way company directors of a Limited Company.

In England and Wales you can:

- apply to register a completely new organisation as a CIO

- set up a CIO to replace an existing unincorporated association or trust

(You can’t currently convert a charitable company to a CIO)

In Scotland you can:

- apply to register a completely new organisation as a SCIO

- convert existing charitable companies, charitable industrial and provident societies and charities of any other legal form to a SCIO

For more information on an accountancy firm who can provide the statutory reporting, and also support you in the running of your charity please contact a member of the Chartered Institute of Management Accountants using the link to The Team above.

Useful links

| Charity Commission: | http://www.charitycommission.gov.uk/ |

| OSCR: | http://www.oscr.org.uk/ |

| Charity Commission NI: | http://www.charitycommissionni.org.uk/ |