Home » Closing a business

Category Archives: Closing a business

Is Striking Off a company the best solution?

- The Insolvency Practitioner will ask your Accountant to confirm that the clients tax affairs are inorder and that appropriate advice has been given

- Final Accounts will need to be prepared and creditors paid

- A Declaration of Insolvency will be signed – The declaration of insolvency demonstrates that the company will be able to settle or secure liabilities and the costs of liquidation within 12 months

- A meeting of Shareholders will appoint the Insolvency Practitioner

- Notices will be posted at Companies House and in the London Gazzette

- Then the MVL can be a carried out and funds distributed

- Arrangements can be put in place to allow the directors access to funds during the process

Here are my top 5 reasons why an MVL might be a good choice:

- The change in 2012 capped capital distributions on striking off at £25,000 but this cap does not apply to liquidations

- You want to retire and close your business and extract the net worth

- You created a Special Purpose Vehicle (SPV) for a specific project and the company is no longer needed

- Companies that are stuck off can be re-instated but that’s not the case with liquidated companies

- Entrepreneurs Tax Relief may be applicable meaning the capital distribution is taxed at 10%

Will your Share Buy Back pass the ‘trade benefit’ test?

Often as part of an exit strategy or succession planning companies will buy back shares.

Setting aside the mechanics, nicely explained in the ACCA Technical Factsheet 177 and the need for S1044 CTA 2010 clearance, the Buy Back has to be in the benefit of the trade not just the shareholder.

For example….

If the purpose is to ensure that an unwilling shareholder who wishes to end his association with the company does not sell his shares to someone who might not be acceptable to the other shareholders, the purchase will normally be regarded as benefiting the company’s trade.

Examples of unwilling shareholders are:

- an outside shareholder who has provided equity finance (whether or not with the expectation of redemption or sale to the company) and who now wishes to withdraw that finance

- a controlling shareholder who is retiring as a director and wishes to make way for new management

- personal representatives of a deceased shareholder, where they wish to realise the value of the shares

- a legatee of a deceased shareholder, where he does not wish to hold shares in the company

Assuming that the shares aren’t being bought back at Par Value, basic rate taxpayers will probably prefer dividends for any surplus where as higher rate taxpayer will want capital treatment.

Share Buy Back is complex, make sure you seek professional advice.

steve@bicknells.net

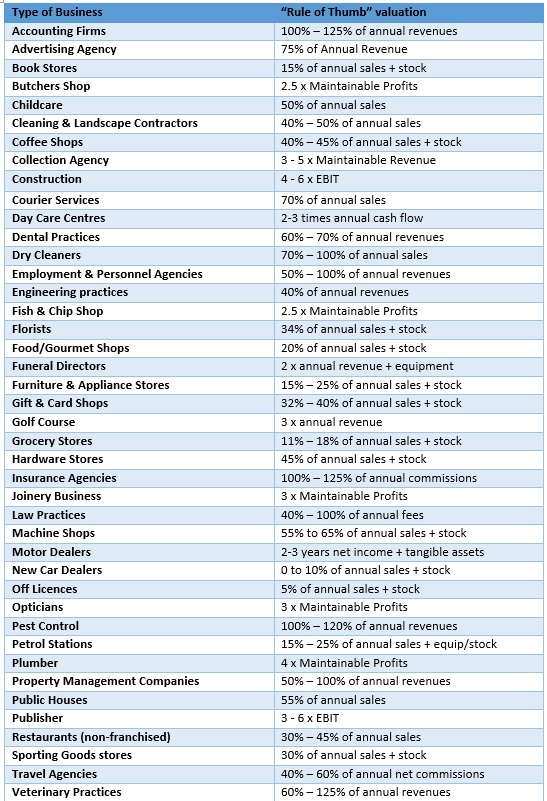

42 Business Valuation “Rules of Thumb” – are they right?

I often get asked for ‘Rules of Thumb’ for small businesses, so I have searched the internet and compiled this list, do you agree with the ‘Rules’?

Rules of Thumb are just a starting point and many other factors need to be considered in valuing a business, it also worth considering HMRC’s views (not so good for Chefs and Hairdressers)..

Any goodwill attributable to the personal skills of the proprietor, for example the personal skills of a chef or a hairdresser, will not be transferred to the new proprietor. Advice should be obtained from the CG Technical Group if it is claimed that the goodwill attributable to the personal skills of the proprietor have been transferred with the business because his/her services have been retained for the foreseeable future by means of an employment contract. All of the relevant facts and circumstances should be established before referral to the CG Technical Group.

http://www.hmrc.gov.uk/manuals/cgmanual/cg68010.htm

steve@bicknells.net

How do you tell HMRC a company is dormant or active?

Dormant is a term that HMRC and Companies House use for a company or organisation that is not active, trading or carrying on business activity. But HMRC and Companies House use the term dormant in slightly different ways.

For Corporation Tax purposes, HMRC views a dormant company as a company that’s not active, not liable for Corporation Tax or not within the charge to Corporation Tax.

A dormant company can be, for example:

- a new company that’s not yet trading

- an ‘off-the-shelf’ or ‘shell’ company held by a company formation agent intending to sell it on

- a company that will never be trading because it has been formed to own an asset such as land or intellectual property

- an existing company that has been – but is not currently – trading

- a company that’s no longer trading and destined to be removed from the Companies Register

Generally your company or organisation is considered to be active for Corporation Tax purposes when it is, for example:

- carrying on a business activity such as a trade or professional activity

- buying and selling goods with a view to making a profit or surplus

- providing services

- earning interest

- managing investments

- receiving any other income

This definition of being active for Corporation Tax purposes is not necessarily the same as that used by HMRC in relation to other tax areas such as VAT, or by other government agencies such as Companies House.

If your limited company has been dormant but is now active, you must tell HMRC within three months of starting your tax accounting period. The best way to do this is to use HMRC’s online registration service.

HMRC have further details on this link

To contact HMRC you will need your Company UTR number and the 3 digit tax office number, then you can use this link to find out contact details for you Corporation Tax Office

When you call, Option 3 is for Dormant Companies and Option 4 is for Active Companies.

Then you will need to write to HMRC to advise them of the change in activity status.

Companies House still require Annual Returns and Annual Accounts even if the company is dormant, but these are obviously easy as there are no changes from the previous year.

steve@bicknells.net

5 top reasons why you need to use an MVL

Members Voluntary Liquidations have been increasing in popularity

According to the official statistics from The Insolvency Service, over the last few (financial) years the number of MVLs has been:

| 2008/2009 | 3,727 |

| 2009/2010 | 3,266 |

| 2010/2011 | 3,270 |

| 2011/2012 | 3,644 |

Since the ESC C16 change came into effect on 1st March 2012, the number increased to:

| 2012/2013 | 4,695 |

Here are my top 5 reasons why an MVL might be a good choice:

- The change in 2012 capped capital distributions on striking off at £25,000 but this cap does not apply to liquidations

- You want to retire and close your business and extract the net worth

- You created a Special Purpose Vehicle (SPV) for a specific project and the company is no longer needed

- Companies that are stuck off can be re-instated but that’s not the case with liquidated companies

- Entrepreneurs Tax Relief may be applicable meaning the capital distribution is taxed at 10%

steve@bicknells.net

The most tax efficient way for a contractor to close their business

Consultants who work as contractors often build up funds their limited companies, they do this as a safe guard because being a contractor, there can be gaps between contracts and they will need cash to carry themselves through to the next contract.

But what if they decide to retire or they get offered their dream job as an employee, they may have lots of assets and cash in their company, perhaps more that £25,000.

They might even find that their main client insists they become employees for example

Some of the BBC’s biggest freelance stars could be asked to join the payroll or leave the corporation, as a new test aims to clear up tax issues.

It is part of a clampdown on the use of personal service companies (PSCs) and a move to tax more freelancers at source.

How could they close the company and use Entrepreneurs Tax Relief to pay 10% tax?

- The Insolvency Practitioner will ask the Contractor’s Accountant to confirm that the clients tax affairs are inorder and that appropriate advice has been given

- Final Accounts will need to be prepared and creditors paid

- A Declaration of Insolvency will be signed – The declaration of insolvency demonstrates that the company will be able to settle or secure liabilities and the costs of liquidation within 12 months

- A meeting of Shareholders will appoint the Insolvency Practitioner

- Notices will be posted at Companies House and in the London Gazzette

- Then the MVL can be a carried out and funds distributed

- Arrangements can be put in place to allow the directors access to funds during the process