Introducing BrightPay Payroll & Auto Enrolment – Online Training for Accountants

Auto enrolment is well on its way and it’s definitely here to stay. The vast majority of employers want help with the auto enrolment setup and ongoing duties. Here at BrightPay we have worked hard to automate and simplify the AE process for payroll bureaus. By streamlining AE with payroll technology you will make your life easy.

BrightPay is a powerful payroll and auto enrolment software that makes managing payroll easy. For bureaus, BrightPay is an easy to use solution with no limitations on the number of employees or employers that can be processed.

BrightPay automates automatic enrolment for you including employee assessment, batch enrolment, personalised tailored communications, postponement, opt-ins, opt-outs & refunds, ongoing monitoring, required reporting and calculations for AE pension providers and much more.

This training webinar will take you through the payroll process from setting up an employer to submitting your RTI submissions. Discover how easy it is to process auto enrolment for your payroll clients. You will learn how BrightPay can automate the AE duties and save you time in the process. Find out why BrightPay has a 99.3% customer satisfaction rate with 99.5% of customers describing our interface as user friendly.

NEST web services / API

This week, BrightPay will release the new NEST web services or API tool to their customers. This tool will be of significant use for accountants that process payroll for a number of clients. The NEST web services allows users to submit their data file from within the BrightPay interface directly to NEST. This process will be demonstrated on the training webinar.

Webinar Date: 8th December | 2.00 pm

Introducing BrightPay Payroll & Auto Enrolment – Online Training for Accountants

![]()

Website: http://www.brightpay.co.uk

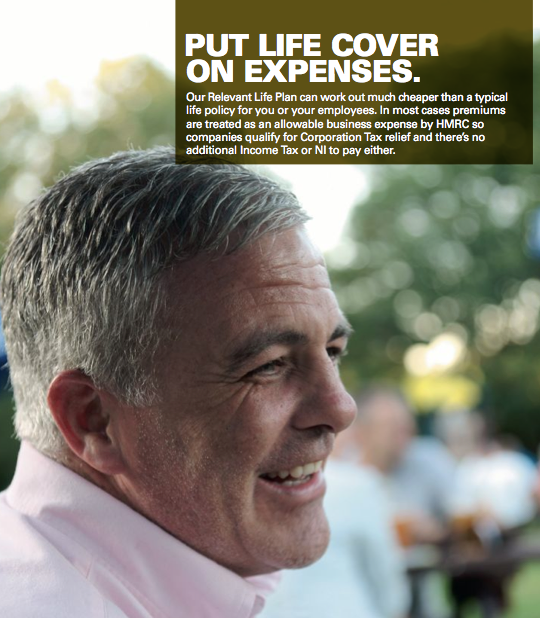

Ways a Relevant Life Plan can help you – let the tax man pay for your life cover…

If you are an accountant this could be great fit for you and your clients, if you have life insurance why not place that cost on company expenses. Either way anyone who pays for life cover out of their own account can now benefit if they are LTD company Director. Life is full of examples of people buying exactly the same thing but for very different reasons. A Relevant Life Plan is no different. We took a moment to ask a few of our clients why they chose to go with a Relevant Life Plan. A few of their responses are below:

- “I am a business owner and heard a shocking statistic that businesses in the UK are terrible at putting in place adequate business continuity plans. The result is that of those without plans, 70% will go out of business within two years if they were to lose a key person.

- I didn’t want my business to be one of the 70%, so I took out a tax-efficient Relevant Life Plan to ensure if the worst ever did happen, there would be the funds to support the business and its employees through a difficult time.”

- “Now we have kids, I was conscious how financially vulnerable my family would be if I was to die. I’m an IT contractor and the sole source of income for the family. We enjoy a very comfortable lifestyle now and I wanted to help secure the financial security of the family if something were to happen to me. A Relevant Life Plan was an incredibly tax-efficient way for me to achieve this.”

- “I am an employer running a small business. It is often difficult for us to compete with larger employers on salary and benefits to attract the best staff. When I heard about Relevant Life Plans and how tax-efficient they were, for both the business and employee, I immediately recognised here was an affordable opportunity for me to be able to offer our staff a benefit akin to the bigger companies.It was a no-brainer to help retain and attract the best people.”

- “As a business owner, I am always looking to save tax.When a client mentioned their Relevant Life Plan and how it allowed them to put their life insurance through their business, with no need to put it on their P11D, I couldn’t believe it. Not only did it save them personally tax and NI, it was also a fully tax-deductable business expense, thereby reducing the business’ Corporation Tax liability too. When I heard that it was all HMRC-approved I didn’t hesitate to get a policy in place for myself.”

You can see from the small sample of responses above the array of reasons that someone takes out a Relevant Life Policy. What they all had in common was the tax-efficient nature of the plan.

Whatever your motivation is for looking into a Relevant Life Plan, we can assure you that you’ll be as delighted as the 1000s of other people that have taken out a tax-efficient Relevant Life Policy already.

For more information on relevant life plans please contact Tom Hitchcock at Broadbench on 01202 978663.

![]()

|

Thomas Hitchcock

Director, Broadbench Ltd p:01202 978663 | m:07813142121 | e:tom.hitchcock@broadbench.co.uk | w:www.broadbenchglobalbenefits.com | a:2 Stanley Road, Poole, Dorset. BH15 1QY

|

What if you write off an inter company or directors loan?

Connected party loans are a problem area especially if the loan is impaired (ie the borrower may not be able to repay the debt)

Individual Loans written-off

If an individual makes a loan to a company and this is subsequently written-off, the company will have a non-trading loan relationship credit equal to the amount written off.

If the loan was made to an unquoted trading company, the individual will crystalise a capital loss equal to the amount of the loan written off. This will be available to set off against capital gains arising in the year of write-off or in subsequent years.ACCA

Loans swapped for Shares

Often Loans are swapped for equity and then subsequently a claim for negligible value is made.

A negligible value claim enables you to set a capital loss against your income (or against other capital gains if you have them) for earlier years and claim a tax refund.

Many negligible value claims are made by shareholder directors whose company has failed. Their claim is to offset the loss on the shares in their company against their directors’ wages for earlier tax years.

When a taxpayer owns shares which become of negligible value the taxpayer may make a claim under s24 TCGA 1992, resulting in a deemed disposal and reacquisition, which crystallises a capital loss.

Intercompany Loans

Accounting standards require companies to assess their assets at the end of each period to ascertain whether there is objective evidence that particular assets are impaired. So if a loan can’t be repaid it would be impaired and may require a provision for bad or doubtful debts at the year-end which may well lead to the eventual release of the loans in question.

The problem is that for connected businesses this can create a double whammy on tax! tax relief is denied in respect of the debit to the creditor company’s profit and loss account. The credit recognised in the debtor company’s accounts can be taxable.

Where the creditor and debtor are connected companies, the connected party rules will apply to the release. This means that the release debit in the creditor’s accounts will not be allowable, because of CTA09/S354. Similarly, the credit in the debtor company’s accounts will not be taxable, since CTA09/S358 applies, unless the release is a ‘deemed release’ as defined in CTA09/S358(3) (CFM35440) or a ‘release of relevant rights’ under CTA09/S358(4) (CFM35510).

Since the release is, for both parties, dealt with under loan relationships, the priority rule in CTA09/S464 means that the creditor’s loss cannot be claimed, nor the debtor’s profit taxed, under the normal provisions for trading income. Nor can the credit in the debtor’s accounts be taxed under CTA09/S94 (debts incurred and later released).

Trade debts or loans between companies within a group may not uncommonly be released when either the debtor or the creditor company (or both) is dormant, as part of a ‘tidying-up’ exercise to enable dormant companies to be struck off. If this is all that happens, HMRC would take the view that the recording of an accounts profit – which is not taxed – in a dormant debtor company does not result in that company starting to carry on a business, and therefore does not start an accounting period under CTA09/S9. HMRC CFM41070

Two companies are connected for an accounting period if one controls the other or both are under the control of the same person (s 466) and companies are connected for the whole of their respective accounting periods if the control test is met at any time during those periods.

One possible solution could be a Deed of Release or Waiver executed in the accounting period in which the loan is released, but this would need to be properly drafted. The credit to the debtor company’s profit and loss account will then be able to be treated as non-taxable and as such avoid the double tax treatment.

steve@bicknells.net

4 Tips for Choosing Cloud Accounting Software

There are lots of brilliant accounting solutions on the market, so how can you decide which one will work best for your business?

Features

The first thing you need to decide is what features you need:

- Projects

- Stock

- Construction Industry

- Payroll

- Invoicing

- Automated payments – PayPal etc

- Bank Feeds

- Quotes

- VAT Schemes

- Document Storage

- Accountant Access

- Access – Apps, Devices, Mac’s

- Contact Management

- Reports

Don’t pay for things you don’t need!

Future Proof

As your business grows, will the software grow with you

- Can you add users

- Can you set access levels

- Are there upgrade products

- Can you add in other products (Apps) such as scanned receipts

Cost

How much does it cost? Normally working with an accountant will reduce the overall cost and provide a package deal

- Monthly Software Subscription

- Accountancy Fees

- Book Keeping Costs

Ask for Help

Just because you have cloud based software it doesn’t mean you won’t need an accountant! you might think you don’t need help but an accountant will help you choose the right VAT Scheme, claim tax reliefs and comply with reporting requirements.

steve@bicknells.net

Why you should be part of Small Business Saturday #SmallBizSatUK

Steve J Bicknell Tel 01202 025252

Last year…

- 16.5 million People shopped in a small independent business on the day, representing a 20% increase in footfall on 2013 or 2.7 million more shoppers

- 64% of UK consumers were aware of the day, a 33% increase on 2013

- Over 3.5 million Facebook views and #SmallBizSatUK trending at number one all day on 6th December 2014

- 55% of Local Authorities and hundreds of MPs supported the campaign

If you have a small business register at https://www.smallbusinesssaturdayuk.com/

Local Chambers of Commerce are also supporting Small Business Saturday and many including Bournemouth Chamber of Trade and Commerce have Facebook campaigns.

steve@bicknells.net

Are you paying enough? New Minimum Wage

From the 1st October 2015 the new National Minimum Wages (NMW) came into force

| Year | 21 and over | 18 to 20 | Under 18 | Apprentice* |

|---|---|---|---|---|

| 2015 (from 1 October) | £6.70 | £5.30 | £3.87 | £3.30 |

| 2014 (current rate) | £6.50 | £5.13 | £3.79 | £2.73 |

With a further increase in April 2016 for over 25’s to £7.20 per hour. The April 2016 wage will be called the Living Wage.

Penalties for non compliance are already harsh and as reported by the BBC on 1st September 2015 they are getting tougher…

These include doubling penalties for non-payment and disqualifying employers from being a company director for up to 15 years.

The government also announced plans to double the enforcement budget for non-payment and to set up a new team in HMRC to pursue criminal prosecutions for employers who deliberately do not pay workers the wage they are due.

Penalties for non-payment will be doubled, from 100% of arrears owed to 200%, although these will be halved if paid within 14 days. The maximum penalty will remain £20,000 per worker.

Are you paying enough?

steve@bicknells.net

Breaking up is hard to do? (Demergers)

A demerger is a form of corporate restructuring in which the entity’s business operations are segregated into one or more components. (Wikipedia)

Demergers are not defined in Tax Law but can be successfully used by Trading Companies and do get special tax treatment.

CTA10/S1075 & TCGA92/S192

A demerger is a series of transactions which have the effect and purpose of dividing the trading activities carried on by a single company or group of companies between two or more companies or groups of companies. CTA10/S1075 and TCGA92/S192 provide special tax treatment if certain conditions are met. Companies may seek advance clearance under CTA10/S1091 that proposed transactions will be an exempt demerger. CTM17200 onwards gives further guidance on the action to be taken by local offices in dealing with demergers.

Basically there are 3 ways to do Demergers

- Distribution in specie – CTM17250

- Liquidation

- Reduction in Capital

Property Investment Companies are not trading companies so demergers are extremely complicated as explained in this article in Taxation

steve@bicknells.net

Will CIS apply to my property ‘refurb’? do Landlords need to register?

![fotolia_1931265[1]](https://business-accountant.com/wp-content/uploads/2013/09/fotolia_19312651.jpg)

Many small scale property developers don’t realise that the Construction Industry Scheme (CIS) applies to them.

HMRC are also looking very closely at Landlords (Investors) to see if they should register too…

Terrace Hill (Berkeley) Ltd v HMRC [2015] UKFTT 75 (TC) TC 04282

Until now property investment has been excluded from CIS but HMRC say this is under review

http://www.hmrc.gov.uk/manuals/cisrmanual/cisr12080.htm

For now let’s focus on Property Developers, here are a few facts:

- Property development is a trade it includes building new buildings and improving or refurbing existing buildings

- Property developers will be contractors because they employ subcontractors – bricklayer, carpenters, painters, electricians, plasterers etc

- There is no lower limit below which you do not have to operate CIS

- Subcontractors, especially Labour Only subcontractors need to have their employment status tested

- Subcontractors need to be verified with HMRC to determine their tax status before they can be paid

- Each month the Developer will need to file a return with HMRC of subcontractor deductions

- Each month the subcontractors must be given a deduction statement

- CIS applies to all types of Developer – Individuals, Partnerships and Companies

Failure to comply means big penalties

Here are some penalty horror stories!

Brian Parkinson a gardner and lanscaper who used occasional subcontractors and got £31,500 in CIS Penalties!

The FTT heard evidence that little or no loss of tax resulted from this omission, as the amount of tax Parkinson ought to have deducted under the CIS was put at £837.90. [Brian Parkinson and the Commissioners for Her Majesty’s Revenue & Customs TC04526; Appeal number: TC/2013/00224].

This comprised £6,000 (5 x the £1,200 maximum) charged under the Taxes Management Act 1970 (TMA 1970), s98A(2)(a) and also month 13 penalties of £25,500 charged under TMA 1970, s. 98A(2)(b). – See more at: https://www.accountancylive.com/partial-win-gardener-over-%E2%80%98excessive%E2%80%99-cis-penalties#sthash.zJA59Gjv.AfCNNGRJ.dpuf

INCOME TAX – subcontractors – appellant company contracted with a third party provider to supply “operatives” – third party provider “net” for CIS purposes – company’s failure to make CIS returns – fixed monthly penalties of £28,500 – Month 13 penalties of £56,500 – whether reasonable excuse – held, no – whether disproportionate as a breach of A1P1 – Tribunal’s jurisdiction and interaction with mitigation – Bosher followed – fixed penalties upheld – Month 13 penalties set aside as excessive – appeal allowed in part

If you’re a property developer make sure you register for CIS with HMRC!

If you need help contact us

steve@bicknells.net

Job opportunity at Alterledger

Trainee Accountant Vacancy

We are pleased to announce that another job opportunity at Alterledger has opened up for a Trainee Accountant.

Training for Chartered Management Accountant

If you have graduated in the last year and are looking for your first job after university there are some fantastic opportunities in Glasgow including a position at Alterledger as Trainee Accountant.

Related articles

Would you like to pay less VAT? have you tried Flat Rate?

Google Docs Link https://docs.google.com/spreadsheets/d/1NyVN2XW3hjpcAYFdjGPCrbeMa-HyfOcgy3eKnNj2wi0/edit#gid=68376799

Usually, how much VAT a business pays or claims back from HM Revenue and Customs (HMRC) is the difference between the VAT they charge customers and pay on their purchases.

With the Flat Rate Scheme:

- you pay a fixed rate of VAT over to HMRC

- you keep the difference between what you charge your customers and pay over to HMRC

- you can’t reclaim the VAT on your purchases – except for certain capital assets over £2,000

To join the scheme your VAT turnover must be less than £150,000 (excluding VAT) and you must apply to HMRC.

You can join the scheme:

- online – when you register for VAT

- by post – fill in VAT600 FRS and send it to the address on the form (or use VAT600 AA/FRS to apply for the Annual Accounting Scheme at the same time)

Confirmation you’ve joined the scheme is sent to your VAT online account (or in the post if you don’t apply online).

In your first year as a VAT-registered business the rate is reduced by 1% until the day before your registration anniversary.

The Flat Rate Scheme has its own Cash Basis and Retail Systems. (VAT Notice 733)

Try our calculator to see if you could save money!

steve@bicknells.net