2015 in review

The WordPress.com stats helper monkeys prepared a 2015 annual report for this blog.

Here’s an excerpt:

The concert hall at the Sydney Opera House holds 2,700 people. This blog was viewed about 14,000 times in 2015. If it were a concert at Sydney Opera House, it would take about 5 sold-out performances for that many people to see it.

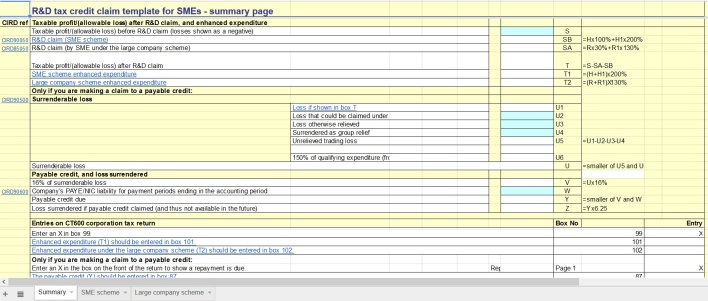

Why aren’t you claiming R&D Tax Credits?

R&D Relief is a Corporation Tax relief that may reduce your company or organisation’s tax bill.

Alternatively, if your company or organisation is small or medium-sized, you may be able to choose to receive a tax credit instead, by way of a cash sum paid by HM Revenue and Customs (HMRC)

But your company or organisation can only claim R&D Relief if it’s liable for Corporation Tax.

The Small and Medium-sized Enterprise Scheme

This scheme has higher rates of relief. Since 1 April 2015, the tax relief on allowable R&D costs is 230% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £130 on top of the £100 spent. It also includes a payable credit in some circumstances.

The Large Company Scheme

If your company isn’t small or medium-sized, then you can only claim under the Large Company Scheme.

Since 1 April 2008, the tax relief on allowable R&D costs is 130% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £30 on top of the £100 spent. If instead there’s an allowable trading loss for the period, this can be increased by 30% of the qualifying R&D costs – £30 for each £100 spent. This loss can be carried forwards or back in the normal way.

Government Statistics show a steady growth in claims

Construction Examples of R&D

- The investigation into the removal of contamination from sites, including land remediation

- Advancements in structural techniques that aid construction relating to unusual ground conditions

- The innovative use of green or sustainable methods and technology

- Development or adaptation of tools to improve efficiency

- The use of new or unique materials, e.g. recycled products

- Improvement on existing construction methods or development of new ideas to solve ongoing issues related to the site environment or project specifications

- Innovative architectural design

IT Systems Examples of R&D

- The design, construction and testing of systems, devices or processes e.g. new hardware or software components, digital interface and control systems

- Integration of legacy and new systems e.g. following a corporate merger or acquisition, the adoption of an Enterprise Architecture or externally with partners in joint ventures

- Advances in network management and operational tools, development of wired or wireless technologies, designing mobile and interactive services, evolution of new generation network switching and control systems

- Data intensive activities e.g. the collection, storage and analysis, distribution and retrieval. Defining or working with new or emerging data models and metadata standards, integration with third party content

These examples and more are shown on the Cost Care Website

There are also examples by Industry on the Alma CG website

http://www.taxdonut.co.uk/blog/2014/12/beginners-guide-claiming-rd-tax-credits-infographic

These are the key questions that you will be asked when requesting an R&D Tax Credit from HMRC:

- How was it decided that R&D had taken place

- A description of the scientific & technological advance sought

- The uncertainties involved

- How and when the uncertainties were resolved

- Why the knowledge being sought was not readily deducible by a competent professional

- Were any grants, subsidies or contributions received for the project within the claim

- Who owns the Intellectual Property of the products resulting from the R&D

- Was the R&D carried out for others ie clients, this could mean your claim is rejected

This HMRC Spreadsheet will help you calculate your Claim

steve@bicknells.net

Business Planning made easy with Apps

A business plan helps you to:

- clarify your business idea

- spot potential problems

- set out your goals

- measure your progress

The problem with Business Plans is that they are time consuming to produce, so business owners put off doing them.

But new Apps might change this and make it much easier to produce high quality Business Plans.

http://www.enloop.com/features

There are other Apps too for example..

steve@bicknells.net

What are the Pros and Cons of Limited Companies?

Click here to access the spreadsheet

What is a Limited Company?

A limited company is an organisation that you can set up to run your business – it’s responsible in its own right for everything it does and its finances are separate to your personal finances.

Any profit it makes is owned by the company, after it pays Corporation Tax. The company can then share its profits.

What is a Sole Trader?

If you start working for yourself, you’re classed as a self-employed sole trader – even if you’ve not yet told HM Revenue and Customs (HMRC).

As a sole trader, you run your own business as an individual. You can keep all your business’s profits after you’ve paid tax on them.

You can employ staff. ‘Sole trader’ means you’re responsible for the business, not that you have to work alone.

You’re personally responsible for any losses your business makes.

The key Advantages and Disadvantages of Companies are shown below.

How do you form a Limited Company?

You can form your company directly with Companies House for £15, it normally takes 24 hours

You’ll need:

- the company’s name and registered address

- names and addresses of directors (and company secretary if you have one)

- details of shareholders and share capital

Personally, I find it easier to use a formation agent such as Company Wizard for £16.99

Often using an agent will mean the company is formed quickly, sometime within a couple of hours.

What are the next steps?

Once your company has been formed you need to:

- Open a bank account for the Company, this can often take a couple of weeks

- Register for Corporation Tax

- Register for other taxes (if they apply to your business) – VAT, PAYE, CIS

- Appoint an accountant (recommended but not compulsory) – Form 64-8

- Set up your accounting software

- Create shareholder agreements, contracts and other legal documents (if required)

steve@bicknells.net

More than just accountants – Clients expectations are changing

There are 2 key reason why small businesses expect more from their accountant.

- In recent years we have seen a huge growth in Cloud Accounting Systems such as Sage One and Debitoor and automation of payments and bank feeds, its no longer enough for accountants just to provide book keeping or year end accounts and tax.

- Business owners want personalised, tailored partnerships with their accountant who need to be true business experts

So what are accountants doing differently?

The Virtual FD

According to Accounting Web….

Half the firms entering the Practice Excellence Awards this year (PEA15) offer management information as part of their service for business clients – up from 33% in 2014. One reason for this jump is that the approach has been shown to have a very beneficial effect on client satisfaction and practice profitability. Probably because it serves a fundamental client need.

Many smaller businesses and SME’s can’t afford a Full Time (or even in some cases a Part Time FD) but they need help with:

- Business Plans

- Budgeting and Forecasting

- Cash Flow Management

- Buy or Rent decisions

- Capital Investment Appraisal

- Accounting Procedures and Systems

- Business Strategy

- Business Funding and Investment

- KPI’s

Virtual FD’s fill this gap because:

- You only pay for what you need

- There is no employment contract

- It provides access to higher level of expertise (in theory)

But here is the key question you should ask your accountant – Have you actually ever worked in business or been an FD?

It seems bizarre to me that so many accountants offer this service and yet have no experience as an actual FD

Weekly Management Reports

Accounting Web reports…

While many practices are becoming the finance team that puts together monthly reporting packs for company managers, Receipt Bank founder and CEO Alexis Prenn argues that monthly management accounts are not the future of accountancy. Cloud technology has changed the dynamic of accounting so much that advisers should be thinking more creatively about what they could do with this information.

What if accountants and businesses could get their hands on transactional data even more quickly and efficiently? Why not produce weekly management accounts?

In a scenario that is familiar to accountants on the Australian accounting conference circuit, specialist bookkeepers are now doing this for Antipodean coffee houses and eateries. “Cafés can run up costs very quickly – if you have three unprofitable weeks, you’re sunk. With online tools and transaction capture, the café can close its books on Sunday and get the weekly management accounts by Tuesday,” Prenn said.

I can see this being of great value in some businesses and cost effective with cloud accounting.

Business Planning and Forecasting

steve@bicknells.net

Why it’s time to end Offshore and Contractor Loan Schemes?

There have been many creative schemes promoted to contractors, entertainers and sports stars, basically using a limited company to make loans to connected parties to avoid tax.

HMRC have been attacking these schemes for years, for example the Boyle case

Philip Boyle v HMRC [TC03103] 2013

On the 16th September HMRC published Spotlight 26: Contractor Loan Schemes – Too good to be true

Contractors and freelancers are bombarded by promoters who make claims that they can help individuals take home as much as 80% to 90% of their income. Sounds too good to be true, that’s because it is.

So why is this considered to be tax avoidance? These promoters use schemes to reduce the amount of tax you pay on your income by making payments which purport to be ‘loans’ from a trust or a company. Normally, a contractor would receive the contract income directly and pay tax on it. These arrangements artificially divert the income through a chain of companies, trusts or partnerships and pay the contractor in the form of a ‘loan’. The ‘loans’ are claimed to be non-taxable because they don’t form part of a contractor’s income. However, in reality the ‘loans’ aren’t repaid and the money is used by the contractor as if it were his or her income.

HM Revenue and Customs (HMRC) view is that these schemes don’t work and strongly advises any contractor or freelancer who has used such a scheme to withdraw and settle their tax affairs. People who settle with HMRC avoid the costs of investigation and litigation and minimise interest and penalty charges on the tax which should have been paid.

Don’t be fooled by promoter websites..

The promoters’ websites and promotional literature claim that they are fully compliant and are HMRC approved. HMRC doesn’t view these arrangements as compliant and never approves any schemes.

Contractor loan schemes, of the sort described above, must be declared under the Disclosure of Tax Avoidance legislation. The promoter is required to pass the scheme reference number (SRN) to all the users who must put this on their tax return. A failure to show the correct SRN on your tax return will lead to additional penalty charges.

Don’t be tempted, HMRC are closing in on unpaid tax, they will find you!

steve@bicknells.net

How do you become self employed?

The UK saw the fastest growth in self-employment in Western Europe in 2014, according to the Institute for Public Policy Research (IPPR).

The number of self-employed workers rose by 8%, faster than any other Western European economy, and outpaced by only a handful of countries in Southern and Eastern Europe.

The IPPR’s analysis shows that the UK – which had low levels of self-employment for many years – has caught up with the EU average. If this growth continues, it says, the UK will look more like Southern and Eastern European countries which tend to have much larger shares of self-employed workers.

Your responsibilities

You’re responsible for:

- keeping records of your business’s sales and expenses

- sending a Self Assessment tax return every year

- paying Income Tax on your profits and Class 2 and Class 4 National Insurance – use HMRC’s calculator to help you budget for this

- your business debts

- bills for anything you buy for your business

- registering for VAT if your turnover reaches the VAT threshold

- registering with the Construction Industry Scheme (CIS) if you’re a contractor or sub-contractor in the construction industry

Naming your business

You can use your own name or trade under a business name – read the rules for naming your business.

You must include your own name and business name (if you have one) on any official paperwork, like invoices and letters.

When should you get help from an Accountant?

Often business owners wait too long before they realise that they need help from an accountant.

Key reasons are:

– not understanding the difference between a book keeper and an accountant

– thinking that an accountant will just be an extra cost – the reality is that most accountants will save the business many times their cost

– thinking that accountants are just bean counters.

But if you choose a qualified and experienced accountant they can bring huge benefits: management tools to improve profitability, cost controls, tax savings, growth strategies, business planning, business structures and much more. So don’t wait too long – getting an accountant should be a priority for all businesses!

Common Mistakes

First off – not having a separate bank accounts. Many start ups try mixing business and personal transactions in their personal bank accounts, its a total nightmare, don’t do it, get a business bank account. Mixing things up will almost certainly have tax implications.

Not registering for tax or filing returns is another one. Getting things right at the beginning is extremely important and a CIMA Accountant can make sure that you choose the right business structure and will help you register for VAT, PAYE, CIS and other taxes. Choosing the right VAT scheme will save you tax. Not registering and filing returns will have severe consequences and lead to fines and penalties.

Also – contract mistakes. Ask your Accountant to review your contracts, they will be able to give you lots of useful tips.

Running out of cash: draw up a Budget and Cashflow and forecast how much cash you will need to run the business, looking at your cash cycle and managing it will be vital. If you need funding ask your Accountant for help, they will be able to look at all the options and help you choose the option that’s best for your business.

Accounting – many start ups fail to keep control of their accounting, by working with an accountant and using Debitoor or Sage One you can avoid this problem.

steve@bicknells.net

A SRIT idea

Will Scottish taxpayers pay less?

From 5th April 2016 a new Scottish Rate of Income Tax (SRIT) will come into force in Scotland. Although is it currently anticipated that taxpayers in Scotland and the rest of the UK will pay the same rate of tax next year, it is likely that the regions will diverge in coming years as more power is devolved to Scotland.

Who is Scottish?

The criteria applied to determine Scottish taxpayers are based on where the individual lives, and not where they work or their feeling of national identity. All of the following would be classed as a Scottish taxpayer:

- WILLIES (Working In London Living In Edinburgh)

- Scottish Parliamentarians (regardless of where they live)

- People living and working in Scotland

- People living in Scotland and working across the border in Carlisle / Newcastle etc

Who decides?

HMRC are responsible for assessing whether or not someone is a Scottish taxpayer. Anyone that HMRC deems to be Scottish based on their principal residence will be issued with a new S tax code. Your payroll software should automatically process the SRIT for anyone with a new S code. As with student loans, it is not for the employer to use their own judgement about applying the SRIT. If an employee disagrees with their tax code, it for the employee to resolve this with HMRC. Employers must act on instructions from HMRC.

Do English employers need to do anything?

Even if your business operates exclusively in England (or any other region of the UK outside Scotland) you will need to comply with regulations as they apply to any of your employees who live in Scotland. Surprisingly, there is no legal obligation to inform HMRC if you move and although employers really ought to know where their employees live, it might not always be obvious, especially if an employee has more than one residence.

Common misconceptions

It is common to think that any of the criteria below qualify for Scottish taxpayer status, but it isn’t the case.

- National identity

- Place of work

- Where income is generated (eg property income in Scotland)

- Regular travel to Scotland

Will Scots benefit?

The costs of the SRIT are to be borne by the Scottish Government. HMRC currently estimates that the total costs of implementing SRIT will be in the range of £30 million to £35 million over the seven-year period from 2012-13 to 2018-19. This is split between IT expenditure of between £10 million and £15 million, and non-IT expenditure of £20 million. The additional annual costs of operating the SRIT will be between £2m and £6m. The lower estimate corresponds to a SRIT where Scots pay the same rate as the rest of the UK. If the SRIT diverges from the neutral rate of 10%, the costs rise in administering the tax regime in the UK including pensions, gift aid and disputes over residence.

Why is the SRIT being introduced?

Scotland as a whole is likely to be worse off as any difference in tax raised is offset by an adjustment to the block grant from Westminster. It is estimated that 2.6m people will be issued with an S tax code. The annual running costs are therefore less that £3 per taxpayer but it is a valid question to ask if it is a good use of taxpayer’s money if tax rates are the same across the UK. It is anticipated that after additional powers are introduced in 2017 the SRIT could be more progressive, meaning that wealthier individuals would pay a higher proportion of tax. For anyone thinking about their residence status and still had a choice, now is a good time to get advice on the best situation for you!

More information

For more information on the SRIT and for guidance on operating your payroll scheme, please contact Alterledger.

Related articles

What are the tax implications if a company pays a Directors personal expenses?

It’s not uncommon for Directors personal expenses to get mixed up with business expenses, for example the director is out buying things for the company and picks up some items for themselves at the same time and it goes on the same bill.

In a perfect world the Director would just repay the cost of personal purchases to the company, but we don’t live in perfect world, so what are the options?

Directors Loan Account

You could post the cost to the Directors Loan Account. These accounts are normally repaid when the Director is paid either salary or dividends.

If the loan is not cleared by year end then the company will have to pay a temporary corporation tax charge of 25% and reclaim the tax when the loan is repaid using form L2P

There may also be a notional amount of interest (4%) charged as a benefit in kind on the loan.

Benefit In Kind

You could have the expenses as a benefit in kind, some benefits may even be tax free, here is a list of my favourite tax free benefits

- Pensions – Up to £40k can be paid in to you pension scheme by your employer (2015/16) and you can use carry forward to pay in even more

- Childcare – Up to £55 per week but check the rules to makesure your childcare complies (HMRC Leaflet IR115) – new rules coming soon

- Mobile Phone – One per employee

- Lunch – Tax Free Lunch Blog

- Cycle Schemes – Cycle to Work Blog

- Fitness – Fitness Blog

- Parties and Gifts – Christmas Blog

- Parking – Parking Blog

- Business Mileage Allowance – 45p for the first 10,000 miles then 25p

- Long Service Award – A bit restrictive as you need 20 years service, the tax free amount is £50 x the number of years

- Eye Tests and Spectacles – The Eye Test must be needed under the Health & Safety at Work Act

- Suggestion Schemes – Suggestion Scheme Blog

- Insurance such and Death in Service and Income Protection – Medical Insurance Blog

- Travel Expenses – Travel Blog

- Working From Home – Working from Home Blog

Private Use of Company Assets

It may also be worth considering private use of company assets.

- The cost of the asset is allowed against Corporation Tax and you can claim Capital Allowances and the Annual Investment Allowance.

- The Assets could be purchased from the Director but they must be transferred at Market Value.

- The Benefit In Kind is generally 20% of the market value

steve@bicknells.net

Will Small Businesses be exempted from VAT MOSS?

Before 1st January 2015 all businesses supplying telecommunications, broadcasting and e-services such as downloaded ‘apps’, music, gaming, e-books and similar services to private consumers located in other EU Member States (referred to as ‘B2C’ supplies) were taxed where the business supplier was established, which is simple to understand and implement.

Since 1st January 2015 VAT is now charged in the country where the customer has ‘use and enjoyment’ of the services.

So lets say you are an American (normally zero rated) on holiday in France, even though you pay with an American credit card and buy from a UK supplier because you are reading your ebook in France, French VAT will apply. Sounds like a nightmare, doesn’t it.

To help with this HMRC introduced the VAT MOSS (Mini One Stop Shop).

Overview

If your business supplies digital services to consumers in the EU, you can register with HM Revenue and Customs (HMRC) the VAT Mini One Stop Shop (VAT MOSS) scheme. There are 2 UK VAT MOSS schemes that operate in an almost identical way:

- Union VAT MOSS scheme for businesses established in the EU including the UK

- Non-Union VAT MOSS scheme for businesses based outside the EU (for example, the USA, Canada, China)

By using the VAT MOSS scheme, you won’t have to register for VAT in every EU member state where you make digital service supplies to consumers.

Once you register for a UK VAT MOSS scheme HMRC will set you up automatically for the online VAT MOSS Returns service.

You need to submit a single VAT MOSS Return and payment to HMRC each calendar quarter. HMRC will then forward the relevant parts of your return and payment to the tax authorities in the member state(s) where your consumers are located. This fulfils your VAT obligations.

Unless businesses opt to register for MOSS, businesses that make intra EU B2C supplies of telecommunications, broadcasting and e-services will be required to register and account for VAT in every Member State in which they have customers. MOSS will give these businesses the option of registering in just the UK and accounting for VAT on supplies to their customers in other Member States using a single online MOSS VAT return submitted to HMRC. This will significantly reduce their administrative burdens.

- Examples of telecommunications services include: fixed and mobile telephone services; videophone services; paging services; facsimile, telegraph and telex services; access to the internet and worldwide web.

- Examples of broadcasting services include: radio and television programmes transmitted over a radio or television network, and live broadcasts over the internet.

- Examples of e-services include: video on demand, downloaded applications (or “apps”), music downloads, gaming, e-books, anti-virus software and online auctions.

Fiscalis conference (7th to 9th September 2015)

Representatives from all EU finance ministries were at the Fiscalis conference in Dublin last week to discuss the implementation of the new EU VAT rules, and how they have been working since their introduction in January 2015.

Accounting Web reported …

One of the key takeaways from the consultation was a general agreement that there should be a threshold to exempt smaller businesses from the rules. The commission stated that it intends to propose legislation for a threshold beneath which companies will be VAT exempt, but did not confirm a figure.

There was also a general agreement that above this threshold there should be what many are calling a ‘soft landing’: A simplified version of the rule for businesses that does not create a financial cliff for those who hit the threshold.

Let’s hope that an exemption can be put in place very soon and ideally as proposed in the EU VAT Action Campaign below

EU VAT Action Campaign (started 28th August 2015)

Please circulate this article as widely as possible, as soon as possible, with as many of your business contacts and other networks.

Write to your national tax authority and finance ministry, to your MPs, MEPs, other elected representatives and to any business organisations which you belong to, insisting that the EU act immediately to:

1. Introduce a threshold of €100,000 for cross-border trade (i.e. based on how much you’re selling digitally to the rest of the EU, outside of your home country). As far as your domestic turnover is concerned, your own country’s VAT rules will still apply.

2. Simplify the rules for all micro businesses (i.e. sub-€2m turnover) to allow ONE piece of data as evidence of place of supply, instead of the current 2-3, with that piece of data being the customer location as supplied by the payment processor to businesses using all levels of their services, not just to those purchasing premium options.

3. Immediately suspend these rules for micro businesses, so that they can revert to their domestic VAT rules and pay taxes according to those regulations during the 2 years it could take for the agreed idea of a VATMOSS threshold to become law.

4. Amend the legislation so that all Member States are legally required to direct their VATMOSS communications through the business’s home tax authority for all micro businesses, to remove the threat and fear of receiving demands and ‘system error’ letters from 27 different tax authorities.

One last thing; please take the few extra minutes to contact these people direct rather than using a bulk-emailing service. These websites have become a victim of their own success in flooding inboxes, so letters coming via these routes are increasingly ignored. You can still send the same letter to them all but you will need to copy and paste and send it individually to be most effective.

steve@bicknells.net