Did Jimmy Carr just use the wrong vehicle?

Thanks to http://www.freedigitalphotos.net

A year on from when comedian Jimmy Carr apologised for using a legal tax avoidance scheme which enabled him to pay as little as 1% tax on his earnings, and with GAAR upon us, tax avoidance has rarely been out of the news headines.

Prime Minister David Cameron stated that “… some of these schemes we have seen are quite frankly morally wrong”, and Danny Alexander, chief secretary to the Treasury, suggested that tax avoiders are the “… moral equivalent of benefit cheats”.

Whether you feel that David Cameron has the moral high ground given the alleged source of his family’s wealth, and whether you feel he was right to name Jimmy Carr in this way, are discussions for another day, but what the comedian had done was entirely legal, so what is the real problem here?

Do we really think that the tax system is a level playing field and that there is a ‘right amount of tax’ we should be paying, and that everyone on similar earnings pays the same amount of tax?

Well think again, because it just ain’t so!

Let’s take for example three fictional friends in the 2012-13 tax year, each of whom receive an income of £25,000.

Tom works for an employer and receives a salary each month from which tax and Class 1 National Insurance is deducted under PAYE; from his £25,000 earnings he might expect to see £19,532 in his pocket, and additionally, the employer has had to pay a further £2,417 for the privilege of employing him.

Dick is a self-employed plumber and his £25,000 income has been calculated from the sales less the expenses of running his business; he would expect to see £19,917.65 in his pocket at the end of the year having paid the tax, and both Class 2 and Class 4 National Insurance due under ‘self assessment’.

Harry didn’t work during the year but was fortunate enough to sell an antique that had been ‘kicking around’ at home for years; after paying Capital Gains Tax he would expect his £25,000 income to be reduced to a net £22,408.

At these modest income levels even relatively small variations can be significant and whilst we can argue about the relative merits of whether the working men and women in the UK should be paying tax at a higher rate than those who can live off the proceeds of asset sales, the central issue here is that because the tax system creates such disparities it is a racing certainty that those who are having to pay tax will, if they are able, seek to arrange their affairs in such a way that they minimise their tax liability.

And it doesn’t stop there.

I have clients who have more than one source of income and because of the way the tax system is arranged into ‘schedules’ it is not automatic that income from once source can be offset against losses from another source, so there have been years in which the client has no overall income, or even a ‘net loss’, but will still be liable for tax on the income from a particular source.

I think we would have to conclude that HM Revenue and Customs are not so much on the side of fairness and equity as that of maximising tax receipts. Indeed in a recent informal conversation a retired tax inspector noted that the “… tax rules are complicated …”, and when HMRC uses those rules to maximise tax collections they are said to be “… applying the law …”, but when a taxpayer uses those same rules to minimise the tax he or she pays, they are said to be “… tax cheats …”, “… tax avoiders …”, or worse.

In Ayrshire Pullman Motor Services & Ritchie v IR Commrs (1929) 14 TC 754, Lord Clyde stated that ‘no man is under the smallest obligation, moral or other, to arrange his legal relations to his business as to enable the Inland Revenue to put the largest shovel into his stores’.

This was endorsed by Lord Tomlin in IR Commrs v Duke of Westminster [1936] 19 TC 490, in which he stated that ‘every man is entitled if he can, to order his affairs so that the tax attaching under the appropriate acts is less than it would otherwise be’.

There has been a good deal of legislation and case law in the intervening period but today we have a whole industry which has grown up around legally minimising the tax their clients need to pay, with HM Revenue and Customs playing catch up and introducing ever more and complex legislation to plug the loopholes that the legislation itself creates.

Anecdotally I believe there is evidence that as tax rates increase so do the number of taxpayers seeking help to minimise their tax liability, and that again would not be a great surprise to me if found to be true. It seems to me that the only real beneficiaries are the ranks of lawyers on both sides.

So how do we halt the madness?

The Office of Tax Simplification has identified various areas ripe for reform, but in my view at least this amounts to ‘tinkering round the edges’, and in the meantime, the 2012 Finance Bill has added almost 700 pages of legislation.

Perhaps we should look at real simplification such as a flat rate tax for all income in a period, from whatever source, with a few (very few) exemptions such as the profit on the sale of one’s family home?

Yes, I know that immediately we introduce exemptions and exceptions there will be opportunities for those seeking to avoid tax, but if the system is seen to be ‘simple’, and more importantly ‘fair’, my belief is that the incentive for avoidance will all but evaporate, and at the very least we might see a reduction in the cost of collecting tax.

Time for real change?

Paul Driscoll is a Chartered Management Accountant, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and AJ Tensile Fabrications Limited, and is a board level adviser to a variety of other businesses.

How do you do capital investment appraisal?

How can you decide whether to buy a fixed asset or to rent it? How do you evaluate and compare capital expenditure requests?

There are 4 key techniques used:

1. Pay Back Period – how many years does it take to get back your initial investment in profits – for normal investments anything less than 3 years is considered good

2. Average Rate of Return (ARR) – this method of appraisal takes the average of the profits made over say a 3 year period (or the life of an asset) and shows the result as a % of the initial investment

3. Net Present Value/Discounted Cash Flow – this method of appraisal takes into account the time value of returns, its often considered the best and most precise way to assess returns, to calculate the Net Present Value you create a cash flow table year 0, shows the investment as a cost, then the net profits are shown in the subsequent years and a factor is applied to remove the effect of inflation, the higher the NPV the better the investment

4. Internal Rate of Return – this is also described as the effective interest rate, to calculate this we increase the Discount Rate in the DCF (3 above) until the NPV equals zero and that produces the return rate

Many businesses will seek to match the funding of the asset to its useful economic life through either a loan or lease, as the life of the asset will normally exceed the pay back period, this should lead to increased profits compared to renting the asset.

Assets are depreciated in the business accounts

Depreciation means the cost of the asset is spread, so it is written off against the profits of several years rather than just the year of purchase. Depreciation is not allowable for tax. Instead you may be able to claim the cost of some assets against taxable income as capital allowances.

The most common methods of Depreciation are Straight Line (depreciation is the same amount in each year) and Reducing Balance (the amount of depreciation decreases each year and is a percentage of the net book balance).

In the Finance Bill 2013 it was announced that for 2 years from 1st January 2013 the Annual Investment Allowance will be increased from £25,000 to £250,000 (an increase of 10 times!).

This is fantastic news if you are planning asset purchases because it will reduce your tax bill.

Some examples of AIA qualifying expenditure

‘Plant or machinery’ actually covers almost every sort of asset a person may buy for the purposes of his/her business. Really the only business assets not covered are land, buildings and cars (which are excluded by one of the ‘general exclusions’). Typical examples of plant or machinery include:

– computers and all kinds of office furniture and equipment

– vans, lorries, trucks, cranes and diggers

– ‘integral features’ of a building or structure, see CA22320

– other building fixtures, such as shop fittings, kitchen and bathroom fittings

– all kinds of business machines, such as printing presses, lathes and tooling machines

– tractors, combine harvesters and other agricultural machinery

– gaming machines, amusement park rides

– computerised /computer aided machinery, including robotic machines

– wind turbines and fibre optic cabling.

Capital allowances are available to sole traders, self-employed persons or partnerships, as well as companies and organisations liable for Corporation Tax.

If you buy an asset, for example, a car, tools, machinery or other equipment for use in your business, you cannot deduct your expenditure on that asset from your trading profits. Instead, you may be able to claim a capital allowance for that expenditure if you haven’t claimed the Annual Investment Allowance for the same asset.

There will be a timing difference between Depreciation and Capital Allowances/Annual Investment Allowance and the Tax on the difference in rates is calculated and shown in the accounts as a Provision for Deferred Tax.

steve@bicknells.net

CIMA la difference?

For most clients the institute a qualified accountant is a member of isn’t a key factor, especially if they are only looking to have their accounts prepared and tax return done. Some simply look for a “Chartered” accountant, which most qualified accountants in practice are if they belong to one of the main professional bodies.

However there are some key differences between the skills and experience of a traditional “high street” accountant and a CIMA Member in Practice. Here are a few:

- A CIMA accountant will tend to look at the business from the inside, rather than just the numbers that make up statutory accounts.

- Their professional training placed a lot of emphasis on providing businesses with meaningful data to support the day to day running of the business, so called management accounts.

- They are likely to have been exposed to a variety of different software systems, and may think more in terms of business processes.

- They are less likely to have worked on statutory audits (which are usually only needed for companies that meet 2 out of the following requirements: turnover of over £6.5 million; assets of more than £3.26 million; has more than 50 employees) so for SME’s that tends not to be an issue.

- They will generally be less obsessed with timesheets and billable hours!

That’s not to say that hiring an accountant who has just emerged from a 30 year career in the Management Accounting department at a local shoe factory is going to be the best thing for a small business, but CIMA have thought about that. Before a CIMA member can get the Practising Certificate they need in order to provide services to the public they need to meet the institute’s skills and experience requirements.

Back to the beginning, many individuals and companies hire an accountant without checking if they are qualified at all. Unlike the financial services industry, accountancy is lightly regulated and anyone can set up shop. Indeed, there are many “qualified by experience” accountants out there giving a good service to their clients. However should things go wrong ……. we’ll look at “when accountants go bad” in a future blog.

Compare the market!

As a nation we seem obsessed with comparison websites and we readily switch insurers to save £50-100 on our car or home insurance. So why don’t businesses market test their accountant more often? Is it because they are happy enough with the basic service and see little differentiation between local firms, or do they think its a lot of hassle to change even if they are open to the idea? I often meet business owners who aren’t entirely happy with their accountant but can’t bring themselves to do much about it, so when I get the chance I explain how easy it is to change, at the right time.

Service and other benefits aside, businesses can often save significant amounts by shopping around. This particularly applies the more services you require. Take a look at your accountancy and bookkeeping costs over the last year. How many items were billed separately, or in addition to the core fee you had agreed? Was your personal tax on top of the fee for the accounts?

In a future blog I’ll look at how to go about changing accountants and the differences a CIMA accountant can bring.

Meanwhile if you can see some benefit in changing your accountant, go (and) compare!

How do you claim R&D Tax Credits?

Research and Development (R&D) tax relief (or credit) is a company tax relief that can either reduce a company’s tax bill or, for some small or medium sized (SME) companies, provide a cash sum. It is based on the company’s expenditure on R&D.

For there to be R&D for the purpose of the tax relief, a company must be carrying on a project that seeks an advance in science or technology. It is necessary to be able to state what the intended advance is, and to show how, through the resolution of scientific or technological uncertainty, the project seeks to achieve this.

http://www.hmrc.gov.uk/manuals/cirdmanual/cird80150.htm

These are the key questions that you will be asked when requesting an R&D Tax Credit from HMRC:

- How was it decided that R&D had taken place

- A description of the scientific & technological advance sought

- The uncertainties involved

- How and when the uncertainties were resolved

- Why the knowledge being sought was not readily deducible by a competent professional

- Were any grants, subsidies or contributions received for the project within the claim

- Who owns the Intellectual Property of the products resulting from the R&D

- Was the R&D carried out for others ie clients, this could mean your claim is rejected

Amount of relief

For expenditure incurred up to and including 31 July 2008 SMEs can deduct 150% in respect of their qualifying R&D expenditure and the payable tax credit can amount to £24 for every £100 of actual R&D expenditure. For expenditure incurred on or after 1 August 2008 SMEs can deduct 175% in respect of their qualifying R&D expenditure and the payable tax credit can amount to £24.50 for every £100 of actual R&D expenditure. The rate is further increased from 1 April 2011 to 200%, and a payable credit of £25 for every £100 of spend.

Large companies can deduct 125% in respect of qualifying expenditure incurred up to and including 31 March 2008 and can deduct 130% thereafter.

Here is a template (originally created by HMRC but updated by me) to help you calculate the value of your claim it has references to relevant HMRC guidance.

The claim is made on your corporation tax return (CT600) if you discover that you should have made a claim in a prior year its not too late, follow this link to find out how to correct prior year returns http://www.hmrc.gov.uk/ct/managing/company-tax-return/amend.htm

Case Studies and Examples

Here are some excellent examples http://www.bis.gov.uk/files/file36112.pdf

It is possible to claim for software http://www.bis.gov.uk/files/file34845.pdf

Software could be tool to enable the R&D or a goal in its own right, but simply modifying existing software isn’t R&D. It has to follow the same rules as other R&D and be an advance in science and technology.

Construction companies have claimed R&D for developing new building systems and new building technologies.

R&D could be a new process rather than an invention.

It doesn’t have to have a patent but there could be advantages to having one, such as patent box tax relief.

steve@bicknells.net

Have you claimed Pre-Trading Tax Relief?

By the time you actually start trading, you may have spent thousands of pounds on research and setting up the business.

Provided you have formally notified HM Revenue & Customs that you have started up a business, most of these costs are usually allowable as business expenses in the first year.

Income Tax (Trading and Other Income) Act 2005

Pre-trading expenses

(1)This section applies if a person incurs expenses for the purposes of a trade before (but not more than 7 years before) the date on which the person starts to carry on the trade (“the start date”).

(2)If, in calculating the profits of the trade—

(a)no deduction would otherwise be allowed for the expenses, but

(b)a deduction would be allowed for them if they were incurred on the start date,

the expenses are treated as if they were incurred on the start date (and therefore a deduction is allowed for them).

http://www.legislation.gov.uk/ukpga/2005/5/section/57

http://www.hmrc.gov.uk/manuals/bimmanual/bim46355.htm

VAT Paid Before VAT Registration

You can reclaim any VAT you are charged on goods or services that you use to set up your business.

Normally, this will include:

• VAT on goods you bought for your business within the last 4 years and which you have not yet sold.

• VAT on services, which you received not more than 6 months before your date of registration.

You should include this VAT on your first VAT return. (Notice 700/1 Oct 2012 4.2)

CIMA can help you make a success of your new business, here is a checklist Making a success of your business

steve@bicknells.net

So you think your mileage claims are ok……..get ready for a shock

According to Tom Tom 72% of businesses felt mileage claims were over stated and 50% of businesses don’t regularly check mileage claims.

How do you monitor mileage claims from your employees?

The news could be even worse for contractors…

Its probably fair to say that most contractors who have an office at their home claim business mileage when they visit clients, but things could be about to change for the worse….

In what could become a landmark decision in the interpretation of “wholly and exclusively” allowable expenditure, a doctor has lost a protracted battle with HMRC over his business mileage claims.

After an enquiry lasting more than seven years and three tribunal hearings, the First-tier Tribunal led by Judge Kevin Poole acknowledged Dr Samad Samadian had a dedicated office in his home which was necessary for his professional activity.

Potentially, the decision has wide implications for all professional self-employed activity, where the business owner undertakes substantive work at home, but also has another business base at which they deliver their expertise regularly.

http://www.taxation.co.uk/taxation/Articles/2013/02/13/53821/way-go-home

It is understood that Dr Samadian will be appealing.

But this could lead to Consultants paying back thousands of pounds in tax.

steve@bicknells.net

What are your KPI’s and why did you choose them?

Key Performance Indicators (KPI) are used by organisations to evaluate success and when you choose KPI’s you should follow the smart approach:

S pecific – a well defined goal that is clearly understood by everyone.

M easurable – can you track your progress towards the goal?

A greed – both employer and employee must agree on what the goals are.

R ealistic – can you achieve the goal with the resources provided?

T ime related – will there be enough time to complete the task?

Here are some examples of E Commerce KPI’s

Sales Key Performance Indicators:

- Hourly, daily, weekly, monthly, quarterly, and annual sales

- Average order size (sometimes called average market basket)

- Average margin

- Conversion rate

- Shopping cart abandonment rate

- New customer orders versus returning customer sales

- Cost of goods sold

- Total available market relative to a retailer’s share of market

- Product affinity (which products are purchased together)

- Product relationship (which products are viewed consecutively)

- Inventory levels

- Competitive pricing

Marketing Key Performance Indicators:

- Site traffic

- Unique visitors versus returning visitors

- Time on site

- Page views per visit

- Traffic source

- Day part monitoring (when site visitors come)

- Newsletter subscribers

- Texting subscribers

- Chat sessions initiated

- Facebook, Twitter, or Pinterest followers or fans

- Pay-per-click traffic volume

- Blog traffic

- Number and quality of product reviews

- Brand or display advertising click-through rates

- Affiliate performance rates

Customer Service Key Performance Indicators:

- Customer service email count

- Customer service phone call count

- Customer service chat count

- Average resolution time

- Concern classification

What do UK Businesses use?

What are your KPI’s and why did you choose them?

Having chosen your KPI’s this clip shows you how to create a dashboard in Excel

steve@bicknells.net

The dangers of illegal dividends

It can be illegal to pay dividends if:

1. There are insufficient retained profits to cover the dividend payments

2. Dividend payments may be illegal if the relevant paperwork has not been completed

- Board Minutes – which must be kept for 10 years http://www.companieshouse.gov.uk/about/gbhtml/gp3.shtml#ch4

- Dividend Vouchers

You can download free templates from

http://www.contractorcalculator.co.uk/declaring_dividends_paperwork.aspx

HMRC are increasingly contending dividends and arguing that they are in reality earnings under the s62 ITEPA 2003 (salary sacrifice) rules and to persuade them otherwise needs proof that a set procedure for the declaration of dividends has been followed.

An example of a board minute is as follows:

Minutes of a meeting of directors of bloggs limited Held at 14 the road, london, ir3 5nl On 31 march 2005

Present: J Bloggs – Director

It was resolved that the company pay a dividend of £9,000 per £1 ordinary share on 31 March 2005 to the shareholders registered on 31 March 2005.

……………………………………

J Bloggs – Director

http://www.ir35calc.co.uk/dividend_documentation.aspx

Companies pay you dividends out of profits on which they have already paid – or are due to pay – tax. The tax credit takes account of this and is available to the shareholder to offset against any Income Tax that may be due on their ‘dividend income’.

When adding up your overall taxable income you need to include the sum of the dividend(s) received and the tax credit(s). This income is called your ‘dividend income’.

The dividend you are paid represents 90 per cent of your ‘dividend income’. The remaining 10 per cent of the dividend income is made up of the tax credit. Put another way, the tax credit represents 10 per cent of the ‘dividend income’.

Dividend tax rates 2013-14

| Dividend income in relation to the basic rate or higher rate tax bands | Tax rate applied after deduction of Personal Allowance and any Blind Person’s Allowance |

|---|---|

| Dividend income at or below the £32,010 basic rate tax limit | 10% |

| Dividend income at or below the £150,000 higher rate tax limit | 32.5% |

| Dividend income above the higher rate tax limit | 37.5% |

So the 10% tax credit offsets the 10% basic rate savings tax

Dividends are not subject to National Insurance.

Can you claim the tax credit if you don’t normally pay tax?

No. You can’t claim the 10 per cent tax credit, even if your taxable income is less than your Personal Allowance and you don’t pay tax. This is because Income Tax hasn’t been deducted from the dividend paid to you – you have simply been given a 10 per cent credit against any Income Tax due.

http://www.hmrc.gov.uk/taxon/uk.htm#5

Declaring dividend income on your Self Assessment tax return

If you normally complete a tax return you’ll need to show the dividend income on it. See income boxes 3 and 4 http://www.hmrc.gov.uk/forms/sa100.pdf

If you don’’t complete a tax return, but you have higher rate of tax to pay on your dividend income, you should contact HMRC.

steve@bicknells.net

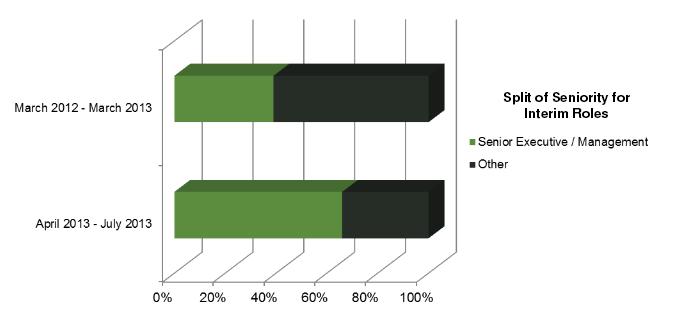

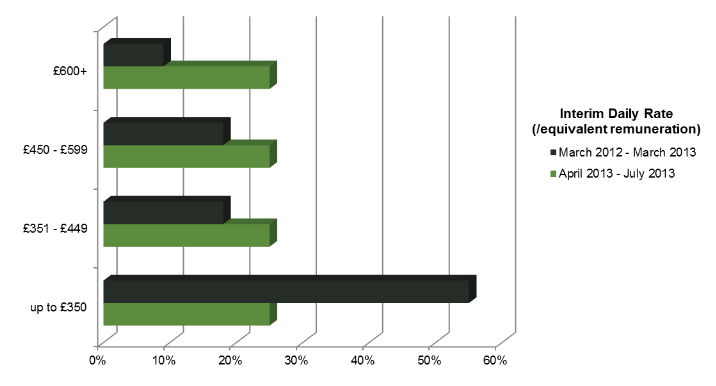

Why has demand for senior interim accountants doubled in April to July 2013?

Many companies that put projects on hold during the recession are now reinvigorating them as the market continues to show signs of recovery. This has created demand for experienced senior interims who can lead projects efficiently, ensuring that they run within budget and timescales. CIMA

The Interim market is estimated to be worth £1.5bn.

Key demand continues to be for experienced professionals who can ensure companies’ systems and processes are running as efficiently as possible. They will be challenged with the task of making any necessary improvements to achieve the project objectives. Their focus continues to be on commercial skills and profitability. Organisations want professionals who are able to make a calculated decision about things that will have an impact on how the business will run in the future.

Partner Financial Trend Survey July 2013 reported

steve@bicknells.net