Financial Reporting – Strategic Report – Part II

In the first part of this article we wrote about the statutory underpinnings of the new Strategic Report, as part of the enhanced disclosure regime promoted by international and national financial reporting standard setters.

Today we focus on the content and structure of the Strategic Report.

We start by emphasising that the standard setters and regulator do not want a formulaic report, but being realists we believe that is exactly what the outcome is going to be. The basic idea behind the report is to better inform investors of the business model and strategic intent of the business, together with how this is measured. In other words, where would accountability and responsibility for failure or a the very least, the key risks and uncertainties in the business or wider environment lie.

What is the purpose of the strategic report?

The basic intent is to bring together, in a cohesive and clear manner the most relevant information investors in a business would require – a ‘joined up story’ with the rest of the Financial Statements. As per the Deloitte practical guide it “provides context to the financial statements, an analysis of past performance and insight into the main objectives, strategies, risks – and how these might impact future performance“.

[Source: Deloitte:

- Objectives & implemented strategy

- Measured against KPIs

- Annual review and future (options)

- Principle Risks and uncertainties faced

- Further considerations

- Employees

- Environmental & CO2

- Human Rights

- Social & community issues

Business Model Canvas Poster download (http://www.businessmodelalchemist.com/tools) (Photo credit: Wikipedia)

Now that confidence is returning and the market and investors have a better, clearer and concise understanding of the direction and calculated risks and unavoidable uncertainties any organisation faces, then better outcomes, good, indifferent or bad can be expected.

©2014 – 3resource

Related articles

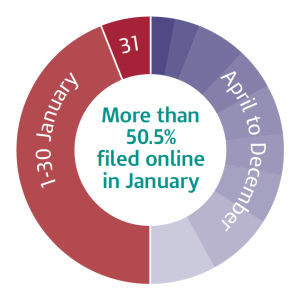

How did you get on with Self Assessment?

According to the Government…

This year, a record-breaking 8.48 million returns were filed online, representing 84.5% of all returns received. This meant that, of the 10.74 million tax returns due for the tax year 2012 to 2013, 93.4% met the SA deadlines for paper and online filing.

On 31 January we saw a final rush to file, with 569,847 online returns coming in on time – the highest percentage ever recorded. It shows that many of you and SA taxpayers now prefer to use our digital service, over paper.

How did you find self assessment, was it easy or nightmare?

steve@bicknells.net

CIMA MiPs have secured an exclusive partnership with Angels Den

With over 6,000 investors, Angels Den has already been successfully matching entrepreneurs and investors for the past six years. They have a great track record of successfully funding growing businesses through their unique SpeedFunding and Angel Club events and now offer entrepreneurs and business owners the opportunity to pitch online via their crowdfunding platform.

Angels Den only want to bring their investors the best deals so they spend quality time with each entrepreneur, pre-screening and giving feedback on their business. Those businesses that aren’t quite ready for funding will now be sent to a centralised booking line at CIMA Accountant. Tel 023 8064 3763.

CIMA Members in Practice will provide consultancy in order to assist businesses to present their funding and investment opportunities to Angels Den through its regional offices.

When CIMA Accountant feel they have a business that may be ready for funding, they can now pass these deals onto Piers Lawford at Angels Den.

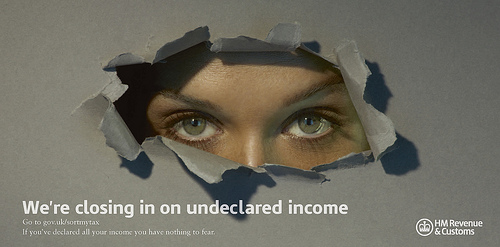

How HMRC use IT systems to seek out tax evaders

There is no doubting the resolve of HMRC to track down and prosecute tax evaders.

The Government has committed to spend £917m to tackle tax evasion and raise an additional £7bn each year by 2014/15.

HMRC are using 2,500 staff to tackle avoidance, evasion and fraud, there is also a website to help those who want to declare income https://www.gov.uk/sortmytax

In the search for tax evaders, HMRC have a £45m computer system called Connect which in 2011 delivered £1.4bn in tax revenue and the system is getting bigger and better all the time. According to Accounting Web:

It uses a mathematical technique to search previously unrelated information and detect otherwise invisible ‘relationship’ networks. Using Connect, HMRC sifts through information on property transactions at the Land Registry, company ownerships, loans, bank accounts, employment history, voting and local authority rates registers and compares with self-assessment records to spot taxpayers who might be under-declaring or not declaring income.

Last year Connect made links between tax records and third party data from hospitals, pharmaceutical companies, insurers and even gas SAFE registrations. DVLA records and the shipping and Civil Aviation Authority registers help identify owners of cars and planes who declare income that the computer suggests cannot support such purchases.

In addition HMRC have also identified 200 accountants, lawyers and professionals who advise on tax avoidance structures and its currently unclear how HMRC will be dealing with them and their clients.

It is important to remember that most people pay the correct tax, in fact HMRC calculate that 93% of tax due is paid correctly, its only a small minority who try to evade tax.

steve@bicknells.net

VAT on sponsoring amateur sports clubs

As accountants we learn the various concepts that ensure that accounts are correctly presented & we learn tax legislation that helps us to keep our clients compliant. Then something comes out of the blue which seems odd, but appears to be common. A case in point is sponsorship on clothing in non VAT registered sports clubs.

In reality what should happen is that the clubs buy clothing & sell sponsorship. There is an expense & there is income. But then a helpful sponsor volunteers to pay the clothing cost direct & so claim the VAT. But think about the implications:

- The accounts of the club could become misrepresented, with income from sponsorship being offset against the costs of clothing.

- As a result of (1) the sports club could be running at above the VAT threshold without realising.

- The organisation reclaiming the VAT has effectively purchased the sponsored clothing, eventhough they may not have been invoiced.

- Given the above the sponsoring organisation should then make a gift of the clothing to the club, where VAT will need to be declared . . . thereby closing the loop. However, it may not do so. Therefore, it may be under-declaring its VAT.

When something seems too good to be true, it often is!

5 ways to reduce the risk of a tax investigation

THE TAX YIELD derived from HM Revenue & Customs investigations into the affairs of small- and medium-sized companies rose by 31% over the last 12 months, according to UHY Hacker Young.

Compliance investigations into SMEs generated £565m for HMRC in 2012/13, up from £434m in 2011/12, with the year ending March 31. Accountancy Age

Some investigations are random and some as a result of HMRC task forces, but many are triggered by risk profiling.

What can you do to reduce your chances of being selected:

1. File your tax returns on time and pay what you owe – If you file late or at the last minute HMRC will think you are disorganised and as such there are more likely to be errors in the return

2. Declare all your income – HMRC get details of bank interest and other sources of income, sometimes they test them and match them to returns

3. Use an accountant – Unrepresented taxpayers are more likely to be looked at, mainly because many of them don’t know what they are doing

4. Trends – if your business doesn’t match the profile of similar business in the same sector or your results suddenly fluctuate it could raise concerns at HMRC, for example, if you suddenly request a VAT refund

5. Tax Avoidance Schemes – if you are using a tax avoidance scheme I am sure HMRC will be looking closely, if they can find a way to challenge the scheme then at some point they will

steve@bicknells.net

10 ways to get paid faster

Late payment kills businesses, it’s a fact.

Latest research shows that British SMEs are having to wait an average of 41 days longer than their original agreed payment terms before invoices are paid. (source: BACS)

So what can you do to get paid faster?

- Get payment upfront – It might sound obvious but do you ask for payment with order? or deposits? or to be paid on delivery?

- Get Stage Payments – on projects agree stages and collect payment before you do the next stage

- Raise the Invoice quickly – as soon as you can bill the client send out the invoice

- Agree Terms of Business and Payment Terms before you start any work

- Make sure you know who to bill and who to chase for payment

- Make your invoice stand out, use bright colours and send a copy by Post and E Mail

- Offer multiple payment methods – Credit Card, BACS, Cheques, PayPal – make it easy for your client to pay you

- Offer a discount for prompt payment

- Charge interest for late payment

- Deal with any disputes quickly

steve@bicknells.net

3 reasons why businesses are sold

When you think about it, there are really only 3 reasons why a business owner would want to sell their business:

Cashing In

Sometimes the the value of your business could be over inflated, remember the dot com bubble. Throughout history there have been times when the price that a buyer is prepared to pay is huge compared to normal business valuation models.

When: March 11, 2000 to October 9, 2002

Where: Silicon Valley (for the most part)

Percentage Lost From Peak to Bottom: The Nasdaq Composite lost 78% of its value as it fell from 5046.86 to 1114.11.

Imminent Threat

This can be caused by many things:

- New Legislation

- Loss of Resources

- Increased Competition

- Loss of Banking Facilities

Basically the seller will be aware that a problem is looming and they want to sell before the problem damages their business.

Life Changes

From a buyers perspective these are often the best businesses to buy, the key reason behind the sale being:

- Retirement

- Relocation

- Life Style

- Selling due to Illness

- New Business Opportunity

steve@bicknells.net

10 financial mistakes all new business should avoid

Starting a new business is always a challenge but there are some common financial mistakes that all start ups should avoid.

- Lack of Planning – Businesses normally start with a great idea but you need to have business model that works and to at least have a basic business plan and cash flow.

- Over Trading – this happens when a business expands too quickly for its working capital, when you start a new business its tempting to accept every order without considering whether you can have the resources and the cash to deliver.

- Wasted Marketing and Advertising – new businesses are an easy target for marketing companies but its important to stick to the essentials to start with, having a website, e mail and business cards are essential, magazine advertising and other things can be done as the business grows, in the early stages you are experimenting and finding your market so if you spend too much too soon you might promote the wrong things at the wrong price.

- Wrong Business Structure – Before you start your business get some advice from your accountant, its important to choose the right structure not just for tax reasons but also for investment and ownership.

- Wrong Staff – Choosing the right team is critical for business success, choose staff that have the right skills, the right attitude and are dedicated to the success of the business.

- Over Ambitious – All too often businesses plans are over ambitious with sales growing rapidly, often they prove to be unrealistic, when preparing a sales forecast start with your order book and be cautious in your assumptions.

- Overheads – Many businesses over spend on overheads for example renting premises too early, work from home, if you can, to minimise costs.

- Stock Problems – Buying the wrong stock, under or over stocking are also issues for start ups, try to adopt a ‘just in time’ stock policy.

- Getting Paid – A sale is only a sale if you get paid, any one can give things away, make sure you manage your clients and get paid on time.

- Competition – Keep an eye on your competitors, they will be watching you and responding to maintain their market share.

steve@bicknells.net

Trying to be a superhero?

Is this story familiar to you? A business person who is successful in their field but starting to get bogged down in the day to day running of their business. In particular, administration and bookkeeping are starting to grind and take the shine out of their enjoyment of their businesses?

This is a common story but one that has a simple solution – DELEGATION.

We may have many ‘good’ reasons why delegation is hard and why we should do all the ‘easy’ jobs in our businesses:

– it can be expensive to pay someone else

– perhaps they will do the job wrongly or prove unreliable

– it will take time for them to settle in and the process will be distracting

However, you cannot escape the truth that however much you try to ‘create’ time by managing it better, there will only ever be 24 hours in a day! We cannot, like Superman, create extra time just by wishing for it.

So I would answer each of the objections above like this:

– You are much more valuable to your business than you may credit. Your time is likely to be worth much more to your business per hour than the £15-£20 per hour you might need to pay an administrator/bookkeeper.

Also there are jobs which only you can do in your business. These undelegatable jobs include creating business strategy, and leading and managing your business (even if you work alone your business needs to be managed!). If administration and bookkeeping are keeping you so occupied you do not have time for strategy, or management, then your business will suffer considerably.

– Are you really sure you are the best bookkeeper/administrator anyway! Surely you did not start your own business to play around with the books or to file!

– If you engage a trained bookkeeper they will settle in very quickly. Also, because they already know what to do as a bookkeeper you won’t have to spend time showing them what to do.

So do yourself a favour. If you have too little time to do the important things in your business – DELEGATE!

Fiona 🙂