Self Employed National Insurance

Changes to payment of National Insurance

HMRC has announced changes to the way that the self-employed will pay their Class 2 and Class 4 National Insurance Contributions (NIC). This is not the first time the process has changed. Some people still refer to paying their stamp – in days of old you had to buy special stamps for your NIC!

English: British National Insurance stamp. (Photo credit: Wikipedia)

No new direct debits

Until recently I would have encouraged the self-employed to set up a Direct Debit Instruction (DDI) with HMRC to pay their Class 2 NIC. From April 2015 HMRC will calculate the NIC due from your self-assessment tax return.

Deferment of National Insurance Contributions

If you currently defer NIC, you don’t need to re-apply to do so. HMRC will be sending out letters in December to everyone who currently defers NIC to confirm this. Any new applications to defer NIC will not be processed. For more information on National Insurance for the Self Employed please go to my blog post here: Class 2 NIC.

Alterledger can help

For more information on filling in your tax return, contact Alterledger or visit the website alterledger.com to see if you can organise yourself better and cut your tax bill.

Related articles

Take time to chill!

As a business owner the festive period can be a challenge.

Our families have a set of agendas for Christmas we are expected to fall in with, and at the same time we are trying to ensure that our business does not struggle because of the reduced working days at the end of December.

However, with a little planning it can be possible to keep everyone happy.

Firstly, it is important to manage your business issues.

A key part of this is managing customer expectations of what can be accomplished before Christmas. If you are a service provider you may often be set Christmas deadlines for projects you are working on. This deadline is generally arbitary and there is no business reason why a deadline of 24th December, or 31st December, is necessary. So make sure you have the conversation with your client from the outset to find out what their ‘real’ deadline is. This will take the pressure off you without inconveniencing your client.

One aspect of the Christmas shut down is that companies, particularly large ones, use it as an excuse for not paying their suppliers. If you have invoices which are due for payment just before the holiday period make sure you contact your customers to ensure you are on the last payment run before they shut down. If payment is due over the holiday period see if you can persuade them to pay you a little earlier, so it will hit your bank over the three working days after Christmas.

If you plan to shut down your business over the festive period make sure all your customers are well aware of the fact in advance, so they can contact you if there is anything they need before you close.

For many business owners it is possible to take a break from their business completely. If you fall into this category I would definitely advise you to do – you will return to work refreshed and raring to go in the new year. In any case, most businesses find their customers are on holiday anyway and so taking the break has very little negative impact on the business.

If you do have to work try to compress the work you have to do into as small a time as possible to maximise the time you can have off.

Secondly, it is important to manage your family’s expectations.

If you have to work, make sure your family are aware of your committments so that they plan key events at times you are available to participate. Do not overcommit yourself or you will find the Christmas period very stressful indeed.

If you have staff it is also important that you balance their needs for a break with their families with your own. Many business owners will allow their staff to have a break over the whole Christmas period and then fill any gaps themselves. This means their staff are happy but their own family is not so happy. Your need for a break is as important as your staff’s – as long as you adopt a fair approach to who can take holiday, on which days, you should prevent any big problems.

Fiona 🙂

Share Buy Back Multiple Completion Checklist

Exit planning is critical if you want to save tax.

Typically when a shareholder wants to leave a business, the company will buy back the shares, but often the company wants to pay in stages to ease the cashflow.

The problem is that buy back in stages generally means that Entrepreneurs Tax Relief can’t be used and to make things worse the buybacks will be tax as a distribution.

The Companies Act prohibits buy back by instalment, however HMRC Tax Bulletin 21 says…

The Board can only consider a request relating to a transaction which appears to be a valid PoS. The Companies Act 1985 lays down certain procedural rules which must be followed. Also, the consideration for the shares must be paid immediately and must be paid in money. The first of these requirements means that payment by instalments is not possible. It is, however, possible to make a contract under which successive tranches of shares are to be purchased on specified dates.

So here is checklist of things to consider to create a multiple completion:

- Ask HMRC for advance clearance – the buy back will be treated as a single event and subject to Entrepreneurs Tax Relief on the whole amount on day one

- Make sure your solicitor draws up an agreement that transfers beneficial interest on day one whilst retaining a legal interest

- Whilst the shares still exist beneficial interest has been disposed of

- Voting rights can no longer be exercised

- The creditor for deferred completion must not be loan capital

Clearly you will need professional advice from your solicitor and accountant to create a multiple completion contract.

steve@bicknells.net

Would an online IR35 test help?

The Term “IR35” became established following a Budget press release issued by the Inland Revenue on 23rd September 1999. That press release was called “IR35”. At its simplest, IR35 is the way in which the taxman closed a loophole that was allowing many contractors and freelance professionals to avoid paying large amounts of Tax and National Insurance.

In 2012 HMRC put forward the Business Tests but they haven’t been as successful as first thought.

Here are the 12 tests, scores shown in()

- Business premises (10)

- PII (2)

- Efficiency (10)

- Assistance (35)

- Advertising (2)

- Previous PAYE (minus 15)

- Business plan (1)

- Repair at own expense (4)

- Client risk (10)

- Billing (2)

- Right of substitution (2)

- Actual substitution (20)

A score less than 10 is high risk and a score more than 20 is low risk. Fail the test and it could cost you a great deal in tax.

In general the key test tend to be:

- Substitution

- Control

- Financial Risk

HMRC launched the ESI (Employment Status Indicator) a while ago.

The recently published Minutes of the IR35 Forum’s last meeting held on 24th July reveal that HMRC are keen for contractors to be able to assess their employment status by way of the Employment Status Indicator (ESI) tool.

Will this resolve the IR35 Status problems?

steve@bicknells.net

Orchestra Tax Relief

New Creative Industries Tax Relief

The 2014 Autumn Statement from the UK Chancellor included a proposal for a new Orchestra Tax Relief.

FHM-Orchestra-mk2006-01 (Photo credit: Wikipedia)

Orchestra Tax Relief

Many orchestras are charities and therefore don’t pay Corporation Tax, but any that do pay tax may qualify for a future Orchestra Tax Relief. The tax break proposed yesterday will be going through a consultation process, so if you have an interest get involved!

Other Creative Industries Tax Reliefs

For more information on the tax reliefs for Orchestras, Theatres, Animation, Video Games and High End TV please go to my blog post here: Orchestra Tax Relief.

Alterledger can help

Why wait for the law to favour your industry? Contact Alterledger or visit the website alterledger.com to see if you can organise yourself better and claim more expenses to cut your tax bill.

Related articles

A reminder to book your place!

This is a reminder that you only have a couple of weeks to book your place at the BEST Christmas party for small business owners! Interested? Read on.

Are you a business owner who works on their own or with just one other person?

Do you miss the traditional office Christmas party, where everyone let’s their hair down and has a fantastic laugh?

If so the Billy No Mates Christmas bash is for you – so if you haven’t already booked now is the time to do so!

The ‘Bash’ is on 19th December (so the Friday before Christmas) from 12pm onwards at Beah, Union Street, Wells, Somerset.

For just £22 for a three course meal with wine the ‘Bash’ is great value – and great fun.

But don’t just take my word for it:

Kim Robinson who is a Billy No Mates stallwart said: “The only thing missing is the photocopier!”

To book your place or simply to find out more go to:

http://billynomates.info/events/wells-christmas-bash-3/

Fiona 🙂

Pool Cars – Do you have a ‘no private use’ Policy?

The latest case Vinyl Design Ltd v HMRC [2014] TC 03345 highlights why policies and mileage records are important.

Here are the facts of the case:

- The company’s only 2 employees were the directors

- They had different cars for private use

- They argued the Pool car was only for Business Use

- They had no policy

- They had no Mileage Records

- Pool Cars kept at home due to risk of vandelism

Not surprisingly HMRC won the case !!

So what should you do to prove there is no private use:

- Keep the car on the company’s business premises

- Keep the keys at the company’s business premises

- Prepare a Board Minute

- Make sure your contract of employment bans private use

- Keep a mileage log

- Insure the car principally for business use

HMRC have specific rules on keeping vehicles at home in EIM23465

Even if you do meet the 60% rule you still have to prove ‘no private use’

steve@bicknells.net

Will your Share Buy Back pass the ‘trade benefit’ test?

Often as part of an exit strategy or succession planning companies will buy back shares.

Setting aside the mechanics, nicely explained in the ACCA Technical Factsheet 177 and the need for S1044 CTA 2010 clearance, the Buy Back has to be in the benefit of the trade not just the shareholder.

For example….

If the purpose is to ensure that an unwilling shareholder who wishes to end his association with the company does not sell his shares to someone who might not be acceptable to the other shareholders, the purchase will normally be regarded as benefiting the company’s trade.

Examples of unwilling shareholders are:

- an outside shareholder who has provided equity finance (whether or not with the expectation of redemption or sale to the company) and who now wishes to withdraw that finance

- a controlling shareholder who is retiring as a director and wishes to make way for new management

- personal representatives of a deceased shareholder, where they wish to realise the value of the shares

- a legatee of a deceased shareholder, where he does not wish to hold shares in the company

Assuming that the shares aren’t being bought back at Par Value, basic rate taxpayers will probably prefer dividends for any surplus where as higher rate taxpayer will want capital treatment.

Share Buy Back is complex, make sure you seek professional advice.

steve@bicknells.net

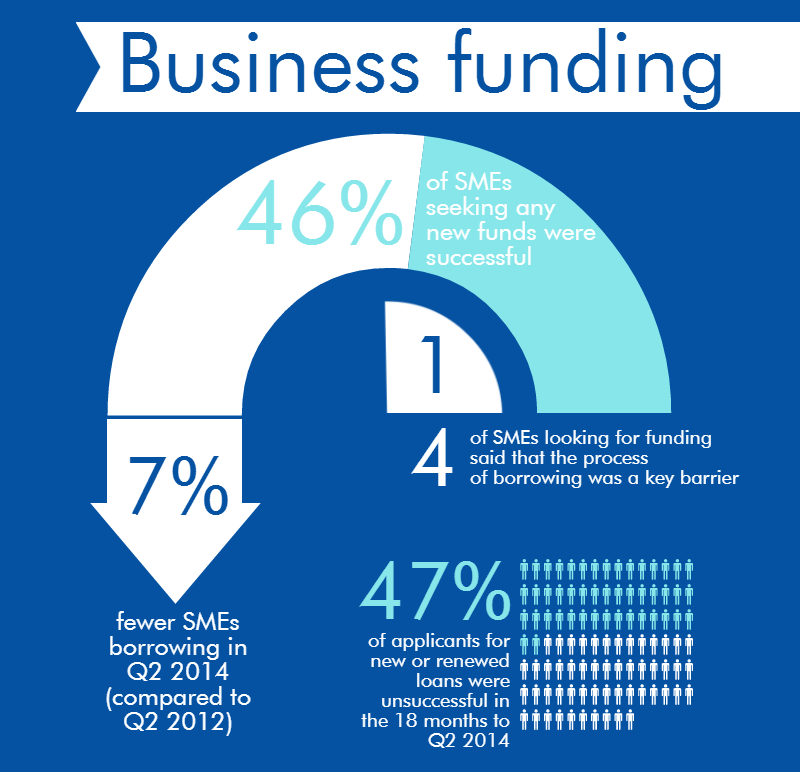

Why alternative finance could be the key to growth

MarketInvoice is the leading online invoice trading platform. They offer fast, flexible cashflow solutions to help businesses grow. Piers Garthwaite from MarketInvoice talks us through the opportunities alternative finance provides growing businesses.

The problem of funding for growing businesses is an all too common one. For any company to grow it needs medium-term financial support to hire new staff, increase supply, buy more equipment, move to a larger office etc. In this blog, we look at the options your client has to fund their business and why alternative finance could be the key to growth.

There are several ways clients can fund growth for their business:

- invest previous profits back into the business

- take out a loan

- raise equity

- look for other sources of finance

The majority of businesses’ first port of call will be to ask their bank for a loan. As we can see from the infographic, banks are not particularly keen on loans at the moment, given the economic environment.

52% of small businesses say that the availability of credit is “poor” or “very poor” and around half say that credit is unaffordable. In the same period, net lending to SMEs is down at -£400m.

This has been a long-term trend: businesses don’t want the products and banks aren’t keen on offering them. The banks’ policy of belt-tightening has affected growing businesses across the UK.

“So how,” we hear you ask, “am I to help my clients?”

Selling equity instead of a obtaining a loan is one option, but there are a number of disadvantages to this, chiefly your client giving up some control of their company.

Other sources of finance could be a grant, an overdraft (although this is unlikely to be big enough to cover any significant expense), leasing and asset finance, invoice factoring or discounting and, what we will be looking at in this blog, alternative finance.

Firstly, some statistics

The size of the alternative finance market is £1.74 billion. When compared with the banks this is, of course, a drop in the ocean. However, the market has been growing at over 150% year-on-year. The peer-to-peer (P2P) business lending market alone is £750 million and has grown at an average rate of 250% in the past three years. Online invoice trading sits at roughly £300 million, with a growth rate of 174%.

Alternative finance has now matured and is mounting an ever-growing assault on outdated, slow and fee-heavy traditional finance.

The industry-leading Nesta report backs up these findings. 33% of P2P business borrowers believed they would have been unlikely to get funds elsewhere. 63% also said that they saw a growth in profit and 53% saw an increase in employment.

What are the main draws?

For many, the main draws are what define alternative finance against the painful and outdated traditional banking experience:

- Speed: it can still take up to 6 weeks to get a loan. Alternative providers use technology to build automated credit scoring systems. With the amount of data available online, there is no reason for a business to have to wait more than 24 hours to be accepted (or declined) for finance.

- Simplicity and transparency: Standard contracts for bank finance are long and often have charges hidden in the Ts & Cs. Alternative finance tends to be more flexible and more transparent on everything, especially pricing. Most leading alternative finance providers have simple online tools to show how much your client will be charged dependent on the terms you choose.

- Service: Most alternative finance providers are run by entrepreneurs and so they have a natural propensity to understand the concerns and aspirations of small business owners looking to grow their business.

For a growing business to be able to access funding within 24 hours, instead of six weeks, could be crucial to its future success in the modern digital age. Additionally, being able to understand exactly what your clients are getting and at what price will help immensely with financial planning at such a critical stage of a business’ life.

Having explored some of the options available to your client, we hope it’s clear there is a plethora of funding opportunities on offer for small businesses.

You don’t need to be at a loss when considering funding options, even if the banks have said no. Financial support can be fast, simple and accessible and, therefore, the lifeline that a growing business needs at a crucial developmental stage.

If you’d like to find out more, visit MarketInvoice’s website or give them a call on 0845 548 0508.

Twitter: @MarketInvoice and @piersgarthwaite.

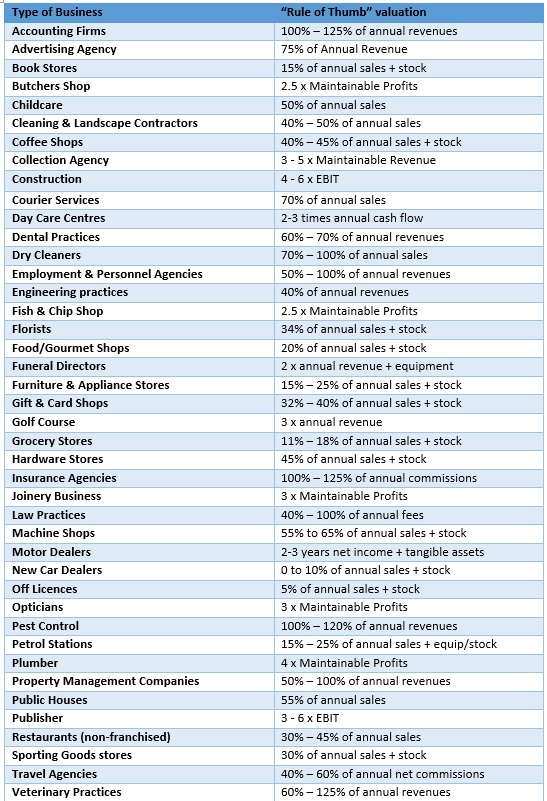

42 Business Valuation “Rules of Thumb” – are they right?

I often get asked for ‘Rules of Thumb’ for small businesses, so I have searched the internet and compiled this list, do you agree with the ‘Rules’?

Rules of Thumb are just a starting point and many other factors need to be considered in valuing a business, it also worth considering HMRC’s views (not so good for Chefs and Hairdressers)..

Any goodwill attributable to the personal skills of the proprietor, for example the personal skills of a chef or a hairdresser, will not be transferred to the new proprietor. Advice should be obtained from the CG Technical Group if it is claimed that the goodwill attributable to the personal skills of the proprietor have been transferred with the business because his/her services have been retained for the foreseeable future by means of an employment contract. All of the relevant facts and circumstances should be established before referral to the CG Technical Group.

http://www.hmrc.gov.uk/manuals/cgmanual/cg68010.htm

steve@bicknells.net