Auto Enrolment – Free Webinars

Steve J Bicknell Tel 01202 025252

With the introduction of automatic enrolment, thousands of employers need to automatically enrol their eligible employees into a workplace pension scheme. Many small and micro employers will look to their bookkeeper, accountant or payroll advisor for help and advice. BrightPay is hosting a series of free Auto Enrolment Webinars specifically designed for bookkeepers, accountants and payroll advisors to make it easier to help payroll clients with their new obligations.

These webinars will include a number of guest speakers from the accounting and payroll industry. The topics covered will highlight various methods to streamline your auto enrolment processes and save you time handling these employer duties for payroll clients. Below is a list of each webinar with the guest speakers and topics that will be discussed. These are completely free webinars. Book your place today.

Webinars Dates

18th March

● Paul Byrne: Payroll Bureaus Guide to Profit from Auto Enrolment

●…

View original post 73 more words

Say goodbye to small earnings

Say hello to small profits

HMRC has changed the name of the threshold for paying Class 2 National Insurance from the Small Earnings Limit to the Small Profits Threshold. If you earn less than £5,965 in 2015-16 you won’t need to pay Class 2 NI, but if you do, it will be calculated as part of your 2015-16 tax return and due with the rest of your tax by 31st January 2017.

English: British National Insurance stamp. (Photo credit: Wikipedia)

Alterledger can help

For more information on filling in your tax return, contact Alterledger or visit the website alterledger.com to see if you can organise yourself better and cut your tax bill.

Related articles

What a difference a day makes

How about three extra days?

HMRC has relaxed the rules on “Real Time Information” for payroll reporting. UK employers are required to send electronic reports to HMRC with each payment of wages to employees. HMRC are now saying that you can submit your RTI report up to three days after the payment date without incurring a penalty.

Any employer who has received an in-year late filing penalty for the period 6 October 2014 to 5 January 2015 and filed within three days, should appeal online by completing the “Other” box and add “Return filed within 3 days”.

Outsource your payroll

Despite the relaxation provided by three extra days, the burden on employers is only likely to increase over the coming months. Auto enrolment is being rolled out to all UK employers over the next couple of years. With the new payroll year about to start on 6th April, now is a good time to consider using a payroll bureau – or at least checking that your current systems will deal effectively with auto enrolment pensions. For more information please and see how Alterledger can help please click here.

Related articles

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Are you as financially savvy as you need to be?

As business owners we need our businesses to make money.

In my opinion an established business which does not pay its owner(s) a decent wage is really a hobby. So given that we need our businesses to make money it follows that we need to be sufficiently au fe with business finances to understand if our business is running our finances, or whether we our running our business finances.

Unfortunately, a large numbers of business owners are not financially savvy enough.

If you would like to see if you are one of these, try answering the questions below:

Do you have a clear financial plan?

Do you know if your business is currently profitable?

At this point do you know how much money is in your bank and what money you can expect in and out of your bank account over the next month?

Do you know what customers/products/services are profitable?

Do you have a robust invoicing and debt collection system so clients pay you in a reasonable time (do you know what reasonable is?)?

Are you always able to pay your suppliers on time?

Can you always pay your salary/dividend/drawings?

Do you know how much you have to sell, and at what price, to provide the lifestyle you want?

If the answer to two or more of these questions is “no” you are probably not as financially savvy as you need to be to run your business effectively.

However, help is at hand and there are ways you can help yourself.

If you have an accountant/bookkeeper ask them questions about your financial position and what you could do to improve it

Talk to your business friends who seem to be financially sorted and ask them what they do

There are volumes of business books out there that can help you understand the basics

Take time to properly plan

You may want to go on a finance for non-financial managers course to learn the basics in a workshop setting.

Finally, I have written a series of FREE financial and business guides which you can download from my website http://www.fionabevanfinancialmanagement.co.uk/guides.php

You can download as many or as few of the guides as you like without registering so please do take advantage of them.

Fiona 🙂

Is Commonhold better than Leasehold for Flats?

Most residential flats are owned on Long Leasholds but this creates tax issues – Stamp Duty, Capital Gains, Income Tax/Corporation Tax.

Take a look at HMRC Helpsheet 292 and CG70700 to get an idea of Capital Gains Tax issues!

Fortunately ESC/D39 can be applied to Lease Extentions

In practice, the surrender of an existing lease and the grant of a new lease should not be treated as a disposal for Capital Gains Tax purposes if the taxpayer so wishes and all of the following conditions are satisfied:

- the transaction, whether made between connected or unconnected parties, is made on terms equivalent to those that would have been made between unconnected parties bargaining at arms length;

- the transaction is not part of or connected with a larger scheme or series of transactions;

- a capital sum is not received by the tenant;

- the extent of the property under the new lease is the same as that under the old lease;

- the terms of the new lease (other than its duration and the amount of rent payable) do not differ from those of the old lease. Trivial differences should be ignored.

The terms of a particular lease may provide for its extension if the tenant so requests. If such a request is made, the extension of the lease does not have any immediate Capital Gains Tax consequences.

In 2002, Commonhold was introduced in the Commonhold and Leasehold Reform Act 2002 (CLRA 2002). Commonhold can be applied to both Commercial and Residential buildings.

The advantage of commonhold is that it gets rid of the concept of the declining asset – sellers and purchasers of commonhold properties will no longer have to worry about how many years are left on the lease.

Under the commonhold system, all flat owners will automatically be members of a company – the Commonhold Association – that owns the freehold and thus the block.

This means that it should be easier to run the building for the benefit of the flat owners.

However, blocks of flats will still need to be managed.

And as a form of community ownership, commonhold brings with it various tensions.

To alleviate any possible problems, members will have to sign up to a “Commonhold Community Statement”.

This statement will set out all the rules and regulations you normally find in a lease, for example rules about subletting, pets, noise and use of gardens.

Which is better?

steve@bicknells.net

How do you account for Construction Retentions?

It’s a very common question, the client pays you and keeps a retention of 5% reducing to 2.5% on completion to be released after the end of the defects period.

You do the same with your sub-contractors.

The retentions need to be held in balance sheet accounts as they can’t be invoiced to client and aren’t due to the sub-contractors. But they should be included within sales and sub-contract costs.

HMRC’s guidance is in BIM51520

In the construction industry it is a common feature of construction contracts for the customer to retain part of the contract fee over a maintenance period pending the satisfactory completion of any remedial work required by the contractor. Typically this may be for a 12-month period between a Certificate of Completion being given and the issue of a Maintenance Certificate.

In their accounts, builders will generally deal with retentions in one of the following ways:

- include retentions within turnover, provide for the estimated cost of remedial work, and make provision for any debt impairment (see BIM42700 onwards), or

- defer recognition of retentions until their receipt becomes virtually certain.

Each of the above accords with generally accepted accounting practice and should be followed for tax purposes unless an unrealistically conservative view has been taken.

In recent years, construction industry customers have become increasingly reluctant to pay retention monies, irrespective of whether there are defects to be made good. It is now common for such monies never to get paid. Consequently, it will often be the case that, whichever of the above approaches is adopted, there will be little or no difference in the figure of net profit.

A challenge will only be appropriate in worthwhile cases. For example, where retentions are only recognised on receipt but, in practice, a large proportion is in fact consistently paid over to the builder and there is a significant tax effect (compared with the alternative provisions method).

There is guidance on VAT in VATTOS5170

……the tax point for retentions is delayed until either a VAT invoice is issued or payment of the retention is received, whichever is the earlier. It must be stressed that this only applies to the retained element of the contract price. The rest of the supply is subject to the normal tax point rules.

steve@bicknells.net

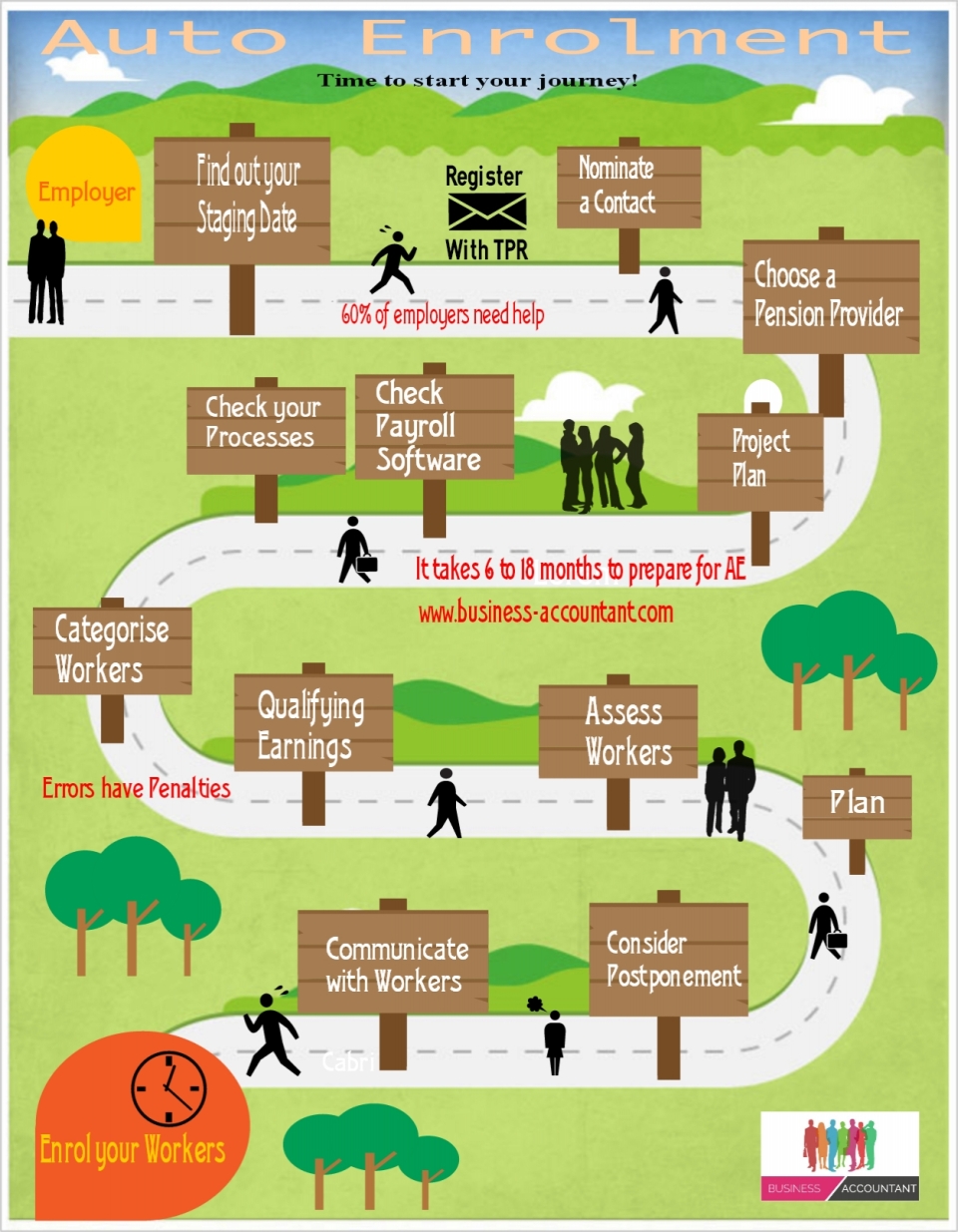

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Sole Traders lose Goodwill Tax Relief

Since 6th April 2008 and until 3rd December 2014 Sole Traders and Parternships were able to claim Entrepreneurs Tax Relief on Goodwill when becoming a Limited Company.

Until the 3rd December 2014 they would claim there Capital Gains Allowance

| Period | Tax-free allowance |

|---|---|

| 5 April 2013 to 6 April 2014 | £10,900 |

| 5 April 2014 to 6 April 2015 | £11,000 |

Then claim ER which reduced the rate of tax to 10% on the gain.

But from the 3rd December they will now pay Capital Gains at the normal rates of CGT which are 18% or 28% (for Higher Rate Income Tax Payers).

This doesn’t change the potential ability of the company to offset goodwill against their Corporation Tax Return.

There are still other benefits related to goodwill as explained in this blog

The tax benefits of goodwill on incorporation?

steve@bicknells.net

The Yacht that wasn’t a benefit in kind

This is the case of Gillian Rockall v HMRC (2014) HKFTT 643.

Mr Michael & Mrs Gillian Rockall were involved in running a hotel and conference centre and providing high-end residential courses, amongst the companies assets was a 140 foot ocean-going yacht costing $11.9 million called Masquerade of Sole.

HMRC issued assessments on Mr & Mrs Rockall for the tax years 2000-2001 to 2008-2009 on the basis of personal use (benefit is normally assessed as 20% of the market value).

The Yacht was used for:

- Business Networking

- Customer Training

- Exploring Business Opportunities in the Caribbean and Mediterranean

- Friends and Acquaintances were taken on occassional trips to provide a opinion on opportunities

The Yacht was also placed with an agent for charter when not required for the purposes above.

The First-Tier Tribunal took the view that the use of the Yacht was only for Business and not for private purposes.

However under S203 ITEPA 2003 a benefit in kind would arise because the asset was at the disposal of the employees.

The Rockalls appealed to the First-Tier Tax Tribunal, on the grounds that the use of the yacht was tax-deductible under s365 of the Income Tax (Earnings and Pensions) Act 2003 (ITEPA). This requires that the item comprising the benefit in kind was used ‘wholly, exclusively and necessarily in the performance of the duties of the employment’.

The tribunal has now ruled that the yacht was bought and operated purely for business purposes and thus was fully tax-deductible for both the Rockalls.

– See more at: http://www.step.org/yacht-used-impress-customers-were-legitimate-expense#sthash.dNRhVYmG.dpuf