Online traders targeted by HMRC

The Revenue has sent 14,000 letters to traders suspected of running a business and failing to declare this on their tax returns.

Of these, 1,000 letters are being sent to people where the taxman has already identified a shortfall on their self-assessment forms.

Some of those targeted make as little as £100 profit online.

It was reported in the Telegraph that eBay, Etsy, Amazon and Gumtree are being forced to hand over customer account details, including their selling activity, as part of the taxman’s legal powers that were extended last year.

The criteria used to assess if an activity is a hobby or a business are:

- The size and commerciality of the activity.

- The frequency of the activity and transactions

- The application of business principles.

- Whether there is a genuine profit motive.

- The amount of time devoted to the activities.

- The existence of arm’s-length customers (as opposed to just selling your wares to family and friends).

HMRC have some great examples to help you decided, for example

Gail is a full-time employee working for a stationery company. She pays her PAYE tax on this employment every month.

In her free time Gail makes cushions and uses most of them in her home. Occasionally she sells them to friends and work colleagues for an amount that just covers the cost of materials of £15. Sometimes she makes a loss. Any money she does make goes towards her holiday fund.

She decides to make extra cash by selling cushions on an Internet auction site and starts auctioning three or four to see how they go. They all sell for more than £50, a profit of at least £35 each.

She uses this money to buy more materials and within a month she is selling around ten cushions a week, always at a profit, and is considering setting up her own website.

Gail’s initial sales of cushions to friends are not classed as trading. It lacks commerciality and she does not set out to make a profit. The occasional sales are a by-product of her hobby. Once she begins to auction her cushions, she has moved into the realms of commerciality.

She is systematically selling her goods to make a profit. She will need to inform HMRC about her trade, and keep records of all her transactions. On the level of sales shown in the example the potential turnover of around £26,000 is well below the VAT annual threshold so Gail does not need to register for VAT.

Many traders start off in a small way and don’t realise that they need to register with HMRC, they assume their activity will be treated as a hobby, but things can grow quickly.

You should register as Self Employed as soon as your hobby becomes a commercial venture, even if you are losing money!

If you don’t register, HMRC will be looking for you and if you have an online business it won’t be hard for them to find you.

steve@bicknells.net

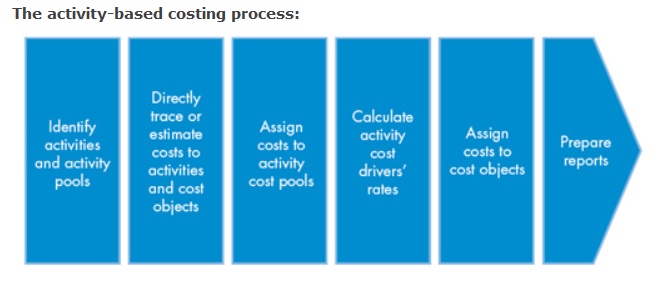

Overhead allocation using ABC

CIMA Official Terminology describes activity-based costing as an approach to the costing and monitoring of activities, which involves tracing resource consumption and costing final outputs. Resources are assigned to activities and activities to cost objects. The latter use cost drivers to attach activity costs to outputs.

What are Activity Pools and Cost Drivers?

Activity Pools

- Purchase Orders

- Machine Set Ups

- Packaging

Cost Drivers

- Number of Purchase Orders

- Number of Machine Set Ups

- Number of items to package

What would the traditional methods of allocation have been?

- Direct Labour Hours

- Machine Hours

- Floor Area

Using Activity Based Costing can produce very different results to Traditional Methods, click here for an example

steve@bicknells.net

Do you use the Employment Status Tool?

Determining whether a worker is Employed or Self Employed isn’t always easy.

HMRC updated and improved their tool in April 2015.

The Employment Status Indicator (ESI) tool enables you to check the employment status of an individual or group of workers – that is whether they are employed or self-employed for tax, National Insurance contributions (NICs) or VAT purposes.

The ESI tool is essential for anyone who takes on workers, such as employers and contractors. (The tool refers to anyone in this position as an engager.) Individual workers can also use the tool to check their own employment status.

The tool cannot, however, be used to check the employment status of certain workers:

- company directors or other individuals who hold office

- agency workers

- anyone providing services through an intermediary (sometimes referred to as IR35 arrangements)

The ESI tool is completely anonymous, so no personal details about the worker or engager are requested.

Click here to use the HMRC Tool

steve@bicknells.net

Have you accrued for Holiday Pay correctly? Section 28 FRS102

Most larger businesses, especially if they are audited probably already accrue for Holiday Pay but not every business has been accruing the cost. FRS102 Section 28.1 will require that holiday pay is accrued. Here is an example from the FRC.

Holiday pay isn’t always easy to calculate for example if you have part time employees or casual workers, Gov.uk have a calculator to help work out the entitlement – GOV.UK Holiday Calculator

The next issue is the rate of pay, for some employees with regular hours its easy but for those with fluctuating rates, bonuses etc a 12 week average is used as explained by ACAS

On 4 November, the Employment Appeal Tribunal (EAT) ruled that holiday pay should reflect non-guaranteed overtime. Non-guaranteed overtime is where there is no obligation by the employer to offer overtime but if they do then the worker is obliged by their contract to work that overtime.

The Government set up a taskforce to consider the possible impact of the EAT’s ruling on holiday pay. Regulations were laid out on 18th December 2014 to limit claims for unlawful deductions from wages to two years. The rules apply to Employment Tribunal claims made on or after 1 July 2015.

Further details at ACAS Calculating Holiday Pay

steve@bicknells.net

When can you make a Prior Year Adjustment?

Until FRS102 basically an error had to be Fundamental for a Prior Year adjustment to be justified

This position is about to change with arrival of FRS 102. Paragraph 10.21 states that ‘an entity shall correct a material prior period error retrospectively in the first financial statements authorised for issue after its discovery’. This means that, on adoption of FRS 102, the threshold for correcting an error by use of a prior period adjustment has reduced from fundamental to material (ICAEW)

Any excuse will do to avoid £100 Self Assessment Penalty

In June the BBC announced..

People who have filed late tax returns have been let off paying a £100 fine for missing the deadline, HM Revenue and Customs has confirmed.

steve@bicknells.net

Is my Grant Capital or Revenue?

A grant is an amount of money given to an individual or business for a specific project or purpose.

You can apply for a grant from the government, the European Union, local councils and charities.

Advantages include:

- you won’t have to pay a grant back or pay interest on it

- you won’t lose any control over your business

Financial assistance in the form of grants is subject to the normal taxation rules, as supplemented by S105 Income Tax (Trading and Other Income) Act 2005 and S102 Corporation Tax Act 2009 (see BIM40465). Under normal rules the tax treatment of grants will depend on whether they are capital or revenue.

Revenue grants

Grants which meet revenue expenditure, such as interest payable, are normally trading receipts.

See also Smart v Lincolnshire Sugar Co. Ltd [1937] 20TC643 and Burman v Thorn Domestic Appliances (Electrical) Ltd [1981] 55TC493.

Capital grants

Grants which meet capital expenditure are normally not trading receipts.

Grants that may be capital in nature include those paid to acquire capital assets or to facilitate the cessation of a trade or part of a trade.

See The Seaham Harbour Dock Co. v Crook [1931] 16TC333).

A capital grant reduces any qualifying capital expenditure for capital allowance purposes, see CA14100.

See BIM40451 for more details

The Accounting Rules are set out in section 24 of FRS102, neatly explained by Steve Collings in his blog, click here to read it

steve@bicknells.net

Have you reclaimed VAT on old unpaid supplier invoices?

Unless you have opted for Flat Rate or Cash Accounting, VAT is normally reclaimed when you get an invoice from your supplier.

However, some invoices will be disputed and the disputes can drag on for months. Its easy to spot old supplier invoices by looking at your Aged Creditors Report.

But having reclaimed the VAT you might not realise that after 6 months the VAT will need to reversed on your next VAT return. The rules are in VAT Notice 700…..

10.6A Repayment of input tax if you do not pay your supplier

For supplies received on or after 1 January 2003 you are required to repay any input tax you have reclaimed if you have not paid your supplier within 6 months of:

(a) the date of supply (usually taken as the invoice date), or if later (b) the due date for payment

Take a look at your Aged Creditors now and if you discover supplier debts older than 6 months provided the net value of errors is less than £10,000 you can simply correct it on your next return, if the error is more than £10,000 you will need to use Form VAT 652

There is a possible alternative, normally the 6 months is counted from the due date not the invoice date, so you could agree new terms on the disputed invoice and extend the due date.

steve@bicknells.net

What is Overlap Profit?

Overlap Profit affects Sole Traders and Partnerships, here are a couple of examples from BIM81080

Example 1 – one overlap period

A business commences on 1 October 2010. The first accounts are made up for the 12 months to 30 September 2011 and show a profit of £45,000.

The basis periods for the first three tax years are:

| 2010-2011 | Year 1 | 1 October 2010 to 5 April 2011 |

| 2011-2012 | Year 2 | 12 months to 30 September 2011 |

| 2012-2013 | Year 3 | 12 months to 30 September 2012 |

The period from 1 October 2010 to 5 April 2011 (187 days) is an `overlap period’.

Example 2 – more than one overlap period

The business in Example 1 continues. In 2015-2016 the accounting date is changed from 30 September to 30 April. The accounts for the 12 months to 30 September 2014 show a profit of £75,000. The relevant conditions for a change of basis period are met (see BIM81045).

The basis periods are:

| 2014-2015 | Year 5 | 12 months to 30 September 2014 |

| 2015-2016 | Year 6 | 12 months to 30 April 2015 |

| 2016-2017 | Year 7 | 12 months to 30 April 2016 |

The period from 1 May 2014 to 30 September 2014 (153 days) is an `overlap period’.

If the taxable profit for 2015-2016 is computed using days, it includes the profits for the `overlap period’ of 153 days (£75,000 x 153/365 = £31,438).

Adding together the overlap profits for the first overlap period of 187 days in Example 1 (£23,054) and the second overlap period of 153 days (£31,438), gives total overlap profits of £54,492 over 340 days.

Tax Cafe point out in their guide ‘Small Business Tax Saving Tactics‘

Why Hasn’t Everyone ‘Cashed In’ Their Overlap Relief Already?

There are two ways to gain access to your overlap relief: cease trading or change your accounting date.

Ceasing to trade is a drastic step: generally not something you are likely to do purely for tax planning purposes. However, it is worth noting that transferring your business to a company is also classed as ‘ceasing to trade’ for these purposes.

Changing your accounting date to access your overlap relief is less drastic, but the downside is that the relief only arises where you are being taxed on more than twelve months’ worth of profit. Despite this, however, there is still generally an overall saving to be made where current profits are at a lower level than the profits arising when the ‘overlap’ first arose. So, with the economy in the state it’s in, now could be a good time to ‘cash in’!

There is also some useful advice in Helpsheet HS222

steve@bicknells.net

Can you save tax by transferring your self employed losses to a company?

If you are self employed and your business makes losses you have the following options to use the losses:

- You can reduce your current year tax bill

- You can offset it against earlier years (up to 3 years)

- You can carry your loss forward

You can’t claim:

- if you use cash basis

- where you don’t run your business commercially for profit

- for part of a loss (you must claim the loss in full) – so it could wipe out your personal allowance

- if you are part of a limited liability partnership

- where your losses are tax-generated

If you transfer your business in exchange for shares to another company, you can use any unused losses against your income from the new company.

Further details in HS227

What this might mean is that as a sole trader you waste your personal allowance because your profits are offset to zero by losses, however, if you had a company that paid you £10,600 you would keep your personal tax free allowance and be able to use the losses against the remaining profit.

The rules for company losses are noted below.

Trading losses that you’ve not used in any other way will be offset against profits from the same trade in future accounting periods. You don’t have to make any claim for this to happen. It’s done automatically if you fill in your Company Tax Return.

Corporation Tax Act 2010, Section 45

Carry forward of trade loss against subsequent trade profits

(1)This section applies if, in an accounting period, a company carrying on a trade makes a loss in the trade.

(2)Relief for the loss is given to the company under this section.

(3)The relief is given for that part of the loss for which no relief is given under section 37 or 42 (“the unrelieved loss”).

(4)For this purpose—

(a)the unrelieved loss is carried forward to subsequent accounting periods (so long as the company continues to carry on the trade), and

(b)the profits of the trade of any such period are reduced by the unrelieved loss so far as that loss cannot be used under this paragraph to reduce the profits of an earlier period.

(5)In this section and section 46 references to profits of the trade are references to profits of the trade chargeable to corporation tax.

(6)Relief under this section is subject to restriction or modification in accordance with provisions of the Corporation Tax Acts.

steve@bicknells.net