FRC figures show CIMA has fastest growth

The FRC have published their Key Facts and Trends in the Accountancy Profession – June 2015

The Financial Reporting Council is the UK’s independent regulator responsible for promoting high quality corporate governance and reporting to foster investment. We promote high standards of corporate governance through the UK Corporate Governance Code. We set standards for corporate reporting, audit and actuarial practice and monitor and enforce accounting and auditing standards. We also oversee the regulatory activities of the actuarial profession and the professional accountancy bodies and operate independent disciplinary arrangements for public interest cases involving accountants and actuaries.

You can download the full report here FRC Key Facts

It compared ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA and found CIMA grow its members by 16.9% between 2010 and 2014, well above the average of 10.3% and beating the growth rate of all the others.

23% (77,551 out of 335,552) UK accountants are CIMA members.

CIMA also had the biggest growth in Worldwide Students 28.8% between 2010 and 2014.

The sectorial employment data in figure 5 showed that 75,429 (97%) work in Industry & Commerce which is 28% of accountants in Industry & Commerce.

Great statistics!

steve@bicknells.net

The Pensions Regulator introduces Auto Enrolment Toolkit for Basic PAYE Tools users

The Pensions Regulator estimates that 1.8 million small and micro employers will reach their staging date within the next two years. These employers include an estimated 200,000 HMRC Basic PAYE Tools (BPT) users.

To date, BPT users have not had access to software functionality that can help them carry out their auto enrolment duties. Assessing the workforce and calculating contributions manually could lead to errors, burden and non-compliance.

Although free and low cost software is available to support auto enrolment, a high volume of BPT users are unlikely to switch to commercial software as many are concerned that they will be persuaded to buy additional products and services. Whilst there is no legal obligation to have software in place, it is evident that it improves employer compliance.

Auto Enrolment Toolkit

The Pensions Regulator are working to release an auto enrolment toolkit by November 2015. As it is a government provided tool, some BPT users may assume that it is the most appropriate solution to use.

However, even though the tool will help BPT users with auto enrolment, it will not provide auto enrolment functionality. The toolkit is intended to be in the format of a downloadable excel spreadsheet that will:

● indicate who should be automatically enrolled into a pension scheme

● provide an employer/employee contribution value (where applicable)

Although the tool will assess the workforce and calculate contributions, the scope of the tool will be very limited. What it will not do:

● It will not support multiple pay frequencies.

● It will not support variable contribution levels.

● It will use a tax-based pay reference period only.

● It will assume that the legal minimum entitlement is being used.

● It will calculate contributions based on banded qualifying earnings only.

● It will only support up to 15 workers.

● It will only support entitled workers if they are placed in an auto enrolment scheme on the same basis as other employees.

● It will not have postponement functionality.

● It will not have the ability to support re-enrolment.

You can find a full breakdown of the limitations here.

The auto enrolment toolkit will reduce the risk of both initial and ongoing non-compliance among BPT users. However, will it actually make the auto enrolment process easier?

Integrated Software

The Pensions Regulator encourages employers to use an integrated payroll and auto enrolment solution that will simplify and streamline auto enrolment. An integrated system, such as BrightPay, will allow you to save time and reduce workload.

There is now a 50% discount for new customers who purchase a BrightPay 2015/16 standard licence when you switch from HMRC Basic PAYE Tools. A standard licence (normally £89 + VAT per tax year) includes unlimited employees, auto enrolment functionality and free support. Now you can get this for just £44.50 + VAT per tax year.

BrightPay also has a free licence for micro employers with up to three employees, including support and auto enrolment functionality.

You can now book a demo to see how BrightPay handles auto enrolment. The one-on-one online demo is done through an online screen sharing site and lasts approx. 20 minutes. Alternatively, you can download a 60 day free trial to try it out for yourself.

* Offer applies to new customers who switch to BrightPay from HMRC Basic tools or another payroll software provider for the first year subscription only. This offer applies to BrightPay 2015/16 employer licences only and cannot be used in conjunction with any other offer.

![]()

Written by Rachel Hynes for BrightPay Payroll and Auto Enrolment Software

Holiday Pay – does it include Overtime?

Back in November 2014, the BBC reported..

Workers have won a ground-breaking case at the Employment Appeal Tribunal to include overtime in holiday pay.

This means some people working overtime could claim for additional holiday pay. Currently, only basic pay counts when calculating holiday pay.

Since then we have had further legislation, the Deduction from Wages (Limitation) Regulations 2014 (the Regulations), which impose the 2 year limit on any new holiday pay claims raised from 1st July 2015 onwards. Separately, a recent case from the Northern Ireland Court of Appeal (Patterson v Castlereagh Borough Council) suggests that voluntary overtime may – in some circumstances – have to be included in holiday pay calculations.

The Northern Ireland Court of Appeal has just held that there is no reason why voluntary overtime cannot be part of an individual’s normal working week and therefore could be included in holiday pay calculations.

This will be bad news for many employers and in Scotland there are now 21,000 holiday pay claims in the Scottish Tribunal system alone. [Law-Now]

Whilst I am sure may employees will welcome the decision, this will surely lead employers to reconsider whether using contractors would be cheaper? No Holiday Pay, No Auto Enrolment Pension, No Redundancy or Statutory Pay

Many already predict that by 2020 50% of workers will be self employed!

steve@bicknells.net

Does your team understand the business strategy? (Balanced Scorecard)

Created in 1992 by Drs. Robert S. Kaplan and David P. Norton, the Balanced Scorecard (BSC) is a revolutionary way to handle strategy management. Notably, it centers your vision and strategy around four distinct measures: Customer, Internal Processes, Financial, and Learning/Growth. Essentially, the Balanced Scorecard allows you to get your whole team on the same page with organizational goals in a clear and understandable way. Although it started out being used primarily in the private sector, you’ll now see the Balanced Scorecard in healthcare, non-profit, government organizations, and a number of other types of associations. [Clear Point Strategy]

Here are 10 examples for different types of businesses – click here

This the Balanced Scorecard for Barclays Bank

About half of major companies in the US, Europe and Asia are using Balanced Scorecard Approaches. The exact figures vary slightly but the Gartner Group suggests that over 50% of large US firms had adopted the BSC by the end of 2000. A study by Bain & Co finds that about 44% of organisations in North America use the Balanced Scorecard and a study in Germany, Switzerland, and Austria finds that 26% of firms use Balanced Scorecards. The widest use of the Balanced Scorecard approach can be found in the US, the UK, Northern Europe and Japan.

Even the most brilliant strategy is worth nothing if it isn’t executed well, especially by your front line — the employees who interact daily with your customers. Unfortunately, these employees are regularly asked to execute strategies that others developed and that they may not understand, never mind feel committed or connected to. In fact, according to Robert Kaplan and David Norton, the founders of the Balanced Scorecard, only 5% of employees understand their company’s strategy. This makes successful execution nearly impossible.

Watch this video, how well would your employees do if you asked them about strategy?

steve@bicknells.net

Why do your workers need to be in an office?

More and more office based workers are now working from home and the employers are focusing on Output rather than hours. For generations work has meant 8 hours per day at your desk but that’s changing.

Switching from office based to home based is best done in stages, starting with a couple of days home based and building up.

Increasing the numbers of UK employees working from home can cut costs by £3 billion a year for UK employers and employees and save over 3 million tonnes of carbon a year, according to a report released in May 2014 by the Carbon Trust.

Advances in technologies such as broadband internet, smart phones and cloud computing mean that many jobs can now be done effectively outside of traditional workplaces. This has resulted in a significant increase in the number of UK employees who work from home, with the total now standing at over 4 million out of a workforce of 30 million.

Investigating the potential environmental benefits of a further shift to homeworking, the new research concluded that, if adopted and encouraged by employers across the country, homeworking could result in annual savings of over 3 million tonnes of carbon and cut costs by £3 billion.

Over 40 per cent of UK jobs are compatible with working from home, but recent research by the Carbon Trust has found that only 35 per cent of companies have a policy allowing their employees to work from home. And where homeworking is offered by companies, between one-third and one-half choose not to accept it.

Homeworking reduces employee commuting, resulting in carbon, money and time savings. If office space is properly rationalised to reflect this, homeworking can also significantly reduce office energy consumption and rental costs.

It is estimated that UK employees save an average of £450 per year if they work from home for 2 days a week.

A UK employer could save around £280 per homeworker per year (according to Indicator).

Ian Foddering, Chief Technology Officer & Technical Director at Cisco UK & Ireland, said:

“By 2018, there will be over 10 billion mobile-connected devices globally, as such, telecommuting will not only become commonplace but is already in the progress of fast becoming the most natural way for people to work and collaborate globally. Cisco has aggressive targets to reduce greenhouse gas emissions from our operations and suppliers worldwide, and telecommuting is helping us to achieve these goals.

“The average Cisco employee telecommutes 2 days a week, and those using our Cisco Virtual Office technology typically work from home 3 days each week. In total, this amounts to avoiding 35 million miles of commuting per year. Not only is this great for the environment, reducing Cisco’s CO2 emissions by 17,000 tonnes annually, but it’s also great for business, with an estimated $333 million per year made in productivity savings.

“Although some organisations may experience cultural barriers in adopting telecommuting, we believe our experience at Cisco demonstrates the real benefits to the environment, the business and the individual employee.”

Employers are also saving £6k by opting for Freelancers…

A survey by PeoplePerHour has shown that the self-employed segment of the labour market in both the UK and USA is growing at a rate of 3.5% per year – faster than any other sector. Should this growth continue for the next five years, researchers predict that half of the working population could be self-employed freelancers by 2020.

The survey also suggests that small businesses that hire freelancers instead of full-time employees could save £6,297.17 per annum. The survey shows that the average waste or spare capacity for each employee in a SMEs is 1.9 hours per day.

The research identifies a number of key drivers behind the shift from employment to self-employment, including “the availability of ubiquitous and inexpensive computing power, sophisticated applications and cloud-based services“. [Lawdonut]

steve@bicknells.net

Would you use P2P Currency Exchange?

A P2P platform simply brings together people with complementary currency exchange requirements. So if User A wants to exchange dollars for euros and User B is looking to exchange euros for dollars, they can do so over a P2P currency exchange. By harnessing the power of the crowd, users are thus able to obtain much better exchange rates than they would get through traditional currency exchange mechanisms.

CurrencyFair Ltd, for instance, claims that it can save up to 90% on international currency transfer fees. While £2,000 transferred through a typical bank could cost as much as £100 (£40 in international transfer fees and £60 in exchange rate margin), the same amount sent through CurrencyFair would only cost about £9 (a fixed £3 transfer fee plus £6 exchange rate margin). CurrencyFair charges an average of 0.35% of the amount exchanged as its margin, while TransferWise Ltd charges 0.5%.

The mechanism for P2P currency exchange is straightforward. A client opens an account with a P2P exchange and deposits money into the account. He or she then converts the money into the desired currency by “matching” with other clients on the P2P exchange. The foreign currency is then transferred to an overseas bank account nominated by the client.

Some P2P companies are controlled by FCA rules for example Midpoint and Transferwise whilst other are covered by EU rules such as Currency Fair, so you might want to check who regulates the P2P that you choose.

It can take up to 48 hours to match a deal which could be an issue in some cases.

The cost is definitely cheaper but in addition on large deals you may be able to negotiate further savings.

steve@bicknells.net

Preregistration VAT confusion

When you register for VAT, there’s a time limit for backdating claims for VAT paid before registration. From your date of registration the time limit is:

- 4 years for goods you still have, or that were used to make other goods you still have

- 6 months for services

Accountingweb reported on 12th June that the goal posts seem to have moved, here is their example..

Ken has been a self-employed pest controller for many years. He registered for VAT with effect from 1 May 2015, at which point he held a van that cost him £24,000 on 1 May 2013, and equipment that he bought for £9,000 on 1 May 2012, both inclusive of VAT. He expects to use the van for eight years and the tools for five years.

Previously most VAT advisers would advise Ken to reclaim VAT of £4,000 in respect of the van and £1,500 paid on the equipment.

The new HMRC interpretation of EC VAT Directive 2006/112 article 289 (set out in VAT Input Tax Manual para 32000) is that as the van has been used for 2/8th of its life, just £3,000 (6/8 x 4000) of the input VAT can be reclaimed. For the equipment a similar calculation reduces the VAT reclaim to £600 (2/5 x1500).

Ken is obviously losing out by £1,900 of unrecoverable VAT.

Taxation Magazine also have an article pointing out the goal posts have moved

What is worrying is that as so many tax advisers will have given potentially incorrect advice based on the new interpretation by HMRC (which HMRC say isn’t a change), will this mean that we will see backdated enquiries and penalties for clients?

steve@bicknells.net

BrightPay: Now Supporting 14 Pension Providers

The introduction of automatic enrolment means that employers across the UK must enrol eligible jobholders into a workplace pension scheme.

Employers must choose a pension scheme that meets the qualifying criteria for auto enrolment. The Pensions Regulator recommends that you choose your pension provider 6 months before your staging date to allow enough time to make the right choice for you and your staff.

There are a number of things to consider when choosing a pension provider, one of the most important being compatibility with your payroll software. Each pension provider requires information in various formats and so it is essential that your payroll software supports your chosen pension provider.

Speak to your payroll provider and ask them if your chosen pension scheme will work with your software. If it doesn’t, you should consider updating your software.

BrightPay currently supports 14 different pension providers, with more constantly being added. If your chosen pension provider is not on the list below, feel free to let us know and we can look into making it available.

The pension provider support in BrightPay allows you to create customised enrolment and contribution files for each of the pension providers, where applicable. APIs with a number of the above pension providers are also in working progress. This means that there will be a direct link between BrightPay and the pension scheme provider.

Although BrightPay supports these pension providers, the software does not choose the pension scheme provider for you. It is the employer’s responsibility to choose a relevant pension provider for their workforce.

To assist with choosing a pension scheme, The Pensions Regulator has recently released a guide to selecting a pension scheme for automatic enrolment for employers. If you need extra guidance, you can also contact an Independent Financial Adviser, but ultimately, the choice of scheme is the responsibility of the employer.

![]()

Written by Rachel Hynes for BrightPay Payroll and Auto Enrolment Software

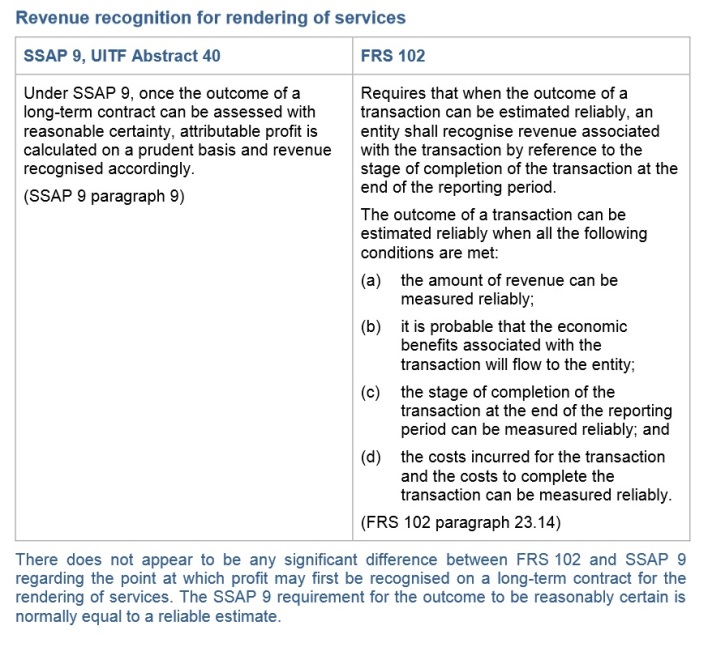

When should you recognise revenue on services provided?

The International Accounting Standard IAS 18 states

‘where the outcome of a transaction involving the rendering of services can be estimated reliably, associated revenue should be recognised by reference to the stage of completion of the transaction at the end of the reporting period’ . In other words, the revenue is recognised gradually, rather than all at one ‘critical point’, as is the case for revenue from the sale of goods. IAS 18 further states that the outcome of a transaction can be estimated reliably when all the following conditions are satisfied:

(a) The amount of revenue can be measured reliably.

(b) It is probable that the economic benefits associated with the transaction will flow to the seller.

(c) The stage of completion of the transaction at the end of the reporting period can be measured reliably.

(d) The costs incurred to date for the transaction and the costs to complete the transaction can be measured reliably.IAS 18 does not prescribe one single method that should be used for determining the stage of completion of a service transaction. However the standard does provide some examples of suitable methods:

(a) Surveys of work performed.

(b) Services performed to date as a percentage of total services to be performed.

(c) The proportion that costs incurred to date bear to the estimated total costs of the transaction.If it is not possible to reliably measure the outcome of a transaction involving the provision of services (perhaps because the transaction is in its very early stages) then revenue should be recognised only to the extent of costs incurred by the seller, assuming these costs are recoverable from the buyer.

In the UK UITF40 and SSAP9 defined the way we report revenue and profit in relation to Services, although accountants and lawyers were among the most high profile casualties of the new regime back in 2005, which forced them to re-catagorise WIP and Revenue, many other service providers also had to consider how they accounted for income. Professionals such as surveyors, architects, doctors and dentists all had to consider the impact of the new rules on their tax liabilities.

FRS102 has not changed the rules.

steve@bicknells.net

Do you know how FRS102 is changing Currency Conversion?

FRS102 affects many things and Section 30 sets out the rules on Currency Conversion.

FRS 102 states that

An entity can conduct foreign activities in two ways. It may have transactions in foreign currencies or it may have foreign operations. In addition, an entity may present its financial statements in a foreign currency

Entities will have a Functional Currency (a concept also used in IFRS) and it allows translation into a Presentation Currency

Reporting at the end of the subsequent reporting periods

30.9 At the end of each reporting period, an entity shall:

(a) translate foreign currency monetary items using the closing rate;

(b) translate non-monetary items that are measured in terms of historical cost in a foreign currency using the exchange rate at the date of the transaction; and

(c) translate non-monetary items that are measured at fair value in a foreign currency using the exchange rates at the date when the fair value was determined.

30.10 An entity shall recognise, in profit or loss in the period in which they arise, exchange differences arising on the settlement of monetary items or on translating monetary items at rates different from those at which they were translated on initial recognition during the period or in previous periods

That all sounds pretty familiar, however, as pointed out by Grant Thornton

Under SSAP 20 Foreign currency translation in current UK GAAP, where matching forward contracts are in place for a transaction, the contracted rate can be used for translation of the matched transaction. This option is not permitted under FRS 102. Instead, a foreign exchange forward contract will be recognised on the balance sheet as a financial instrument at fair value and the associated debtor or creditor will be retranslated at the year-end rate.

A key difference (FRS102) to note in comparison to SSAP 20 Foreign Currency Translation is that SSAP 20 regards consolidated goodwill as an asset of the parent company and not the subsidiary. [Steve Collings Blog]