Home » Posts tagged 'Auto Enrolment'

Tag Archives: Auto Enrolment

Accountants – Would an auto enrolment pre-assessment tool be useful?

Auto Enrolment is now in full swing and starting to affect small and micro employers. Many of these employers do not understand auto enrolment and do not want any ongoing involvement with the process. A key concern for small and micro employers is how much auto enrolment will actually cost their business.

With auto enrolment, employers are faced with additional ongoing costs, including the employer contributions each pay period. What is the easiest and most accurate way for an employer, or a bureau on their behalf, to calculate these costs?

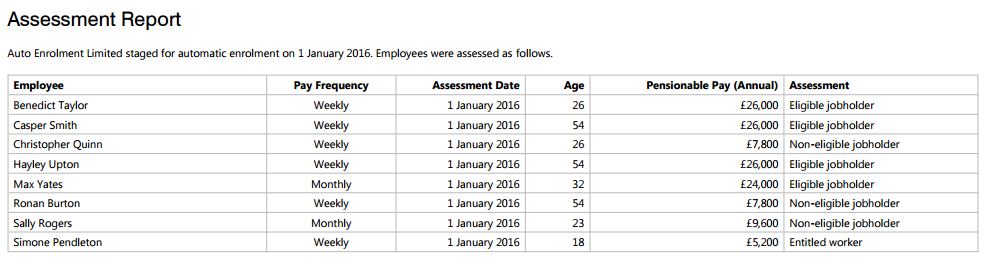

BrightPay have developed a pre-assessment tool, which enables users to automatically prepare a pre-assessment report. This report is useful to send to clients 6 months in advance of their staging date, giving the employer a preview of what auto enrolment will look like when they reach their staging date.

The pre-assessment tool uses employee details from the current pay period to provide an estimate of what auto enrolment might look like at the time of staging. The report will include details of each employee’s auto enrolment worker category, along with their pensionable pay, qualifying earnings, employee contributions and employer contributions. Watch BrightPay’s Pre-Assessment video.

PDF Example: Pre-assessment Report

The amounts are subject to change, depending on non-eligible or entitled workers choosing to join the scheme and fluctuations in employee pay.

The report can be exported to PDF and also includes some general information about employee assessment, including definitions of worker categories, qualifying earnings and minimum contribution rates.

This is an ideal document to send to clients in advance of their staging date, giving them an idea of how much auto enrolment will cost them at each pay period thus allowing them to plan accordingly. For example, the report may show that the employer has no eligible jobholders, and so is not required to set up a pension scheme.

BrightPay will also allow you to create a post-assessment report. After staging, the assessment report will give you a snapshot of what auto enrolment looked like on the staging date, highlighting the assessment date, the employee worker categories and postponed employees.

PDF Example: Post-assessment Report

Video: You can see how BrightPay’s pre-assessment tool works here.

![]()

BrightPay Payroll and Auto Enrolment Software

The Pensions Regulator introduces Auto Enrolment Toolkit for Basic PAYE Tools users

The Pensions Regulator estimates that 1.8 million small and micro employers will reach their staging date within the next two years. These employers include an estimated 200,000 HMRC Basic PAYE Tools (BPT) users.

To date, BPT users have not had access to software functionality that can help them carry out their auto enrolment duties. Assessing the workforce and calculating contributions manually could lead to errors, burden and non-compliance.

Although free and low cost software is available to support auto enrolment, a high volume of BPT users are unlikely to switch to commercial software as many are concerned that they will be persuaded to buy additional products and services. Whilst there is no legal obligation to have software in place, it is evident that it improves employer compliance.

Auto Enrolment Toolkit

The Pensions Regulator are working to release an auto enrolment toolkit by November 2015. As it is a government provided tool, some BPT users may assume that it is the most appropriate solution to use.

However, even though the tool will help BPT users with auto enrolment, it will not provide auto enrolment functionality. The toolkit is intended to be in the format of a downloadable excel spreadsheet that will:

● indicate who should be automatically enrolled into a pension scheme

● provide an employer/employee contribution value (where applicable)

Although the tool will assess the workforce and calculate contributions, the scope of the tool will be very limited. What it will not do:

● It will not support multiple pay frequencies.

● It will not support variable contribution levels.

● It will use a tax-based pay reference period only.

● It will assume that the legal minimum entitlement is being used.

● It will calculate contributions based on banded qualifying earnings only.

● It will only support up to 15 workers.

● It will only support entitled workers if they are placed in an auto enrolment scheme on the same basis as other employees.

● It will not have postponement functionality.

● It will not have the ability to support re-enrolment.

You can find a full breakdown of the limitations here.

The auto enrolment toolkit will reduce the risk of both initial and ongoing non-compliance among BPT users. However, will it actually make the auto enrolment process easier?

Integrated Software

The Pensions Regulator encourages employers to use an integrated payroll and auto enrolment solution that will simplify and streamline auto enrolment. An integrated system, such as BrightPay, will allow you to save time and reduce workload.

There is now a 50% discount for new customers who purchase a BrightPay 2015/16 standard licence when you switch from HMRC Basic PAYE Tools. A standard licence (normally £89 + VAT per tax year) includes unlimited employees, auto enrolment functionality and free support. Now you can get this for just £44.50 + VAT per tax year.

BrightPay also has a free licence for micro employers with up to three employees, including support and auto enrolment functionality.

You can now book a demo to see how BrightPay handles auto enrolment. The one-on-one online demo is done through an online screen sharing site and lasts approx. 20 minutes. Alternatively, you can download a 60 day free trial to try it out for yourself.

* Offer applies to new customers who switch to BrightPay from HMRC Basic tools or another payroll software provider for the first year subscription only. This offer applies to BrightPay 2015/16 employer licences only and cannot be used in conjunction with any other offer.

![]()

Written by Rachel Hynes for BrightPay Payroll and Auto Enrolment Software

Payroll Bureaus – Does Auto Enrolment Apply to your Director Clients?

Auto Enrolment is about to hit its peak with over 500,000 small and micro employer set to stage in 2016. With this high volume of micro employers staging early next year, it is important to know whether or not Auto Enrolment applies to your clients.

If your client has at least one member of staff who is paid via a PAYE scheme, Auto Enrolment duties will apply. The only exeption when Auto Enrolment duties does not apply is when a company or individual are not considered to be an employer.

You won’t have any duties if you meet one of the following criteria:

● you’re a sole director company, with no other staff

● your company has a number of directors, none of whom has an employment contract

● your company has a number of directors, only one of whom has an employment contract

● your company has ceased trading

● your company has gone into liquidation

● your company has been dissolved

Automatic enrolment will apply if more than one director has a contract of employment, be it a written or verbal contract. You can find out more about Automatic Enrolment for Directors here.

What if Auto Enrolment does not apply to my clients?

If your client receives a letter which includes their staging date and you believe that auto enrolment does not apply to them, you or the employer need to notify the Pensions Regulator.

To inform the Pensions Regulator, you must fill out an online form with your client’s PAYE Reference and Letter code. Notify the Pensions Regulator here.

Once you have notified the Pensions Regulator, you will receive a confirmation email and your client will no longer receive any further communications.

Change in Circumstances

Your client’s circumstance will change if a new member of staff is taken on other than a director, or if at least two directors started working for them under contracts of employment.

If this occurs, auto enrolment will now apply to your client and the employer, or you on their behalf, must notify the Pensions Regulator of the change.

However, if you do have auto enrolment duties to perform it will make it easier if you have suitable payroll software in place to automate the AE duties. BrightPay is a payroll solution that is free to employers with up to three employees or the bureau licence has unlimited employees and employers. Why not try our free 60 day trial to find out for yourself ?

Written by Rachel Hynes for BrightPay Payroll and Auto Enrolment Software

Employers – Will you process auto enrolment in-house or outsource to an Accountant/Bureau?

The Pensions Regulator continues to try to inform employers about their new automatic enrolment (AE) duties. There is so much information available it has lead to much confusion. For employers, there is no getting around AE either. It is here to stay whether you like it or not. Employers that have at least one member of staff now have specific, mandatory duties to perform. This includes enrolling those employers who are eligible into a workplace pension scheme and contributing towards it. There are also some duties that need to be completed for non-eligible and entitle employees.

Another consideration for employers is whether you have the time or staff resources to deal with AE in-house or outsource this to a payroll bureau or accountant?

Confused? Join BrightPay for a free webinar where we will take you through our step-by-step guide to automatic enrolment has been designed to help employers understand the processes involved in completing their automatic enrolment duties.

One of the subjects on the webinar will weigh up the advantages of processing auto enrolment in-house or will you look to outsource this job to an accountant, bookkeeper of bureau? See the webinar agenda below.

Agenda

• Auto Enrolment Overview

• Staging dates

• Assessing Employees

• Enrolling

• Option of Postponement

• Handling Opt-outs and Refunds

• Supporting Employee Communication

• Recording and Providing Reports

• Integration with various Pension Providers

• Payroll Software

• Process AE in house or outsource

Register here today

Don’t worry if you can’t make it on the day we will record the webinar and send it to you after the webinar, along with any questions and answers that were discussed on the day. By registering your details for the event we will automatically send the information to you.

Free Webinar for Employers

Free Webinar: The Essential Guide to Auto Enrolment for Employers

For employers auto enrolment is here to stay!!

If you are an employer who does not have payroll software or use the HMRC Basic PAYE tools to process your company’s payroll then this webinar is for you. This free webinar will take you through the main administration employer duties of auto enrolment including: an auto enrolment overview, staging, employee assessment, enrolment, postponement, opt in & opt outs, employee letters, reporting, choosing payroll software and processing auto enrolment in house or outsource it.

This webinar is specifically designed to help employers understand the processes involved in completing their automatic enrolment duties. Each and every employer with at least one member of staff has new obligations to carry out.

The webinar is ideal for employers who process their payroll in-house or are considering outsourcing it to a payroll professional. The session will help you understand what is involved for you and your business.

Places are limited.

![]()

For more information visit our website

Who cares what you think?

Are testimonials worth anything?

Many websites include “testimonials” from “customers”, but do they have any worth? If you want to attract new business it is good to be able to publish positive feedback, which helps demonstrate the value that other customers find in your service. The problem is that if reviews are obviously edited and self-selected they are not obviously representative of the views of your customers. Single line reviews taken out of context can be particularly misleading!

Use external review sites

One of the best-known review sites is tripadvisor. The greatest strength of these reviews is that hotels and restaurants etc have no control over the reviews. They have the opportunity to respond to criticism, but can’t cherry-pick the best reviews to give a false impression. The Pensions Regulator website is keen to point out that “private sector organisations we link to are not endorsed by Government and are provided for information only”; however it is worth noting that they include a link to VouchedFor on their advice page for individuals and in their guide to finding an advisor for Pension Auto Enrolment.

VouchedFor

If you are looking for a hotel you would probably prefer to check tripadvisor rather than lot of different websites for reviews. VouchedFor works along similar lines to tripadvisor, but for Accountants, Financial Advisors and Solicitors. Professionals who have a listing on the site must confirm that they recognise the name / email address of any reviewer before the review is posted online. Just like tripadvisor the professionals can’t read the review until is online so they can’t edit out any negative feedback and poor scores.

Tim Alter appeared in the guide in The Sunday Telegraph on March 29th. You can also read all his great client reviews on his VouchedFor profile!

Auto Enrolment

Many small businesses will need professional advice to help them set up a pension scheme to comply with Auto Enrolment regulations. If you are an employer and still need to prepare for your staging date, you can use an Accountant or Financial Adviser to guide you through the process. For help with setting up your payroll and preparing for your staging date, please contact Alterledger.

Related articles

Letters for under 21s

Changes for employees under 21

From 6th April 2015 employer national insurance contributions will be abolished for under 21s. If you employ anyone over 16 and under 21 years old you will need to use one of the new letters for under 21s in the national insurance category setting of your payroll software.

English: British National Insurance stamp. (Photo credit: Wikipedia)

Secondary contribution rates

This table shows how much employers pay towards employees’ National Insurance for tax year 2014 to 2015. The contribution rate calculated by your payroll software is set by the category letter.

| Category letter | £111 to £153

a week |

£153.01 to £770

a week |

£770.01 to £805

a week |

From £805.01

a week |

|---|---|---|---|---|

| A | 0% | 13.8% | 13.8% | 13.8% |

| B | 0% | 13.8% | 13.8% | 13.8% |

| C | 0% | 13.8% | 13.8% | 13.8% |

| D | 3.4% rebate | 10.4% | 13.8% | 13.8% |

| E | 3.4% rebate | 10.4% | 13.8% | 13.8% |

| J | 0% | 13.8% | 13.8% | 13.8% |

| L | 3.4% rebate | 10.4% | 13.8% | 13.8% |

National insurance categories

Most employees will have a category letter of A or D depending on whether or not they are in a contracted-out workplace pension scheme. There are categories for mariners and deep-sea fisherman; the more common categories are shown below:

Employees in a contracted-out workplace pension scheme

| Category letter | Employee group |

|---|---|

| D | All employees apart from those in groups E, C and L in this table |

| E | Married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| L | Employees who can defer National Insurance because they’re already paying it in another job |

Employees not in contracted-out pension schemes

| Category letter | Employee group |

|---|---|

| A | All employees apart from those in groups B, C and J in this table |

| B | Married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| J | Employees who can defer National Insurance because they’re already paying it in another job |

Employees in a money-purchase contracted-out scheme

This kind of scheme ended in April 2012 but some employees might still be part of one.

| Category letter | Employee group |

|---|---|

| F | Tax years before 2012 to 2013 only: all employees apart from the ones in groups G, C and S in this table |

| G | Tax years before 2012 to 2013 only: married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| S | Tax years before 2012 to 2013 only: employees who can defer National Insurance because they’re already paying it in another job |

How to claim zero rate of employer contributions

You should already have proof of age for all your employees. A copy of a passport, driving licence or birth certificate will be required to show that your employee qualifies for the new zero rate of employer’s contribution. The seven new categories are valid from 6th April and must be applied from the first salary payment after 5th April 2015 to benefit from the new zero contribution rate for employers.

What does this have to do with Auto Enrolment?

You need to have proof of age for all your employees aged under 21 to claim the zero contribution rate for employer’s National Insurance. By the time of your staging date you must assess all your workers, based on their earnings and age. To help you prepare for Pension Auto Enrolment you can make sure that all your employee records are up to date and that your payroll software has the full details for all workers including their date of birth. This is a good opportunity to clean up all your employee data.

Alterledger can help

For more information on saving employer’s national insurance and preparing for Pension Auto Enrolment, contact Alterledger or visit the website alterledger.com.

Related articles

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Common Auto Enrolment mistakes..

The Pensions Regulator (TPR) has recently highlight the following problem areas:

- Employer forgeting to do the declaration of compliance within 5 months of staging, many employers wrongly assumed that registering on the Government Gateway was enough.

- Confusion caused by running multiple payrolls for the same employer for example weekly and monthly

- Completing the declaration of compliance but without choosing a pension provider

- Omitting self employed workers who have a contract to provide work personally

steve@bicknells.net