Home » Posts tagged 'Pension'

Tag Archives: Pension

Can my Pension buy shares in my company?

A pension scheme can buy quoted or unquoted shares in a company based either in the UK or overseas.

An occupational pension scheme can buy shares in one or more of the employers participating in the scheme as long as both the following conditions are met:

- the total value of the scheme funds invested is less then 20% of the net value of the pension scheme funds

- the amount invested by the scheme in the shares of any one employer participating in the scheme is less than 5% of net value of the pension scheme funds

Any investment larger than this will be an unauthorised payment and both the scheme employer and scheme administrator will have to pay a tax charge on the amount above the limit.

https://www.gov.uk/pension-trustees-investments-and-tax

So in theory, yes, it is possible, but in reality its likely to fail because:

- An independent ‘Arms Length’ valuation will be required, for an unquoted small business or start up this is extremely difficult as establishing a market value for the shares will be difficult and often a start up will have losses in the first few years

- The HMRC’s rules which govern all registered pension schemes (in particular the sections covering both taxable property and tangible moveable property) dictate that the combined shareholding in the unquoted company held between the pension fund, the member personally and any other connected persons must never exceed 19%, otherwise there would be enormous tax consequences for all concerned

- The company concerned must not (and never should be in the future) controlled by the trustees of the pension fund in conjunction with connected parties

If the business needs the money to buy commercial premises for its trade it would be easier for the pension scheme (SSAS) to lend the money, a SSAS can lend up to 50% of net scheme assets as explained in in this fact sheet from Curtis Banks

If you are over 55, you could also consider drawing down funds from your pension, the first 25% will be tax free.

steve@bicknells.net

Have you been over taxed on your pension withdrawal?

You should be able to withdraw 25% of your pension tax free, but your pension provider will tax you on payments above this level.

If they don’t hold a current P45, the pension provider will apply an emergency tax code on a month 1/week 1 basis, which could mean you pay too much tax.

You will need these forms to reclaim the tax

Form P50Z – if the client has chosen to empty all their pension pot in one go and they have no other PAYE or pension income (other than the state pension);

Form P53Z – if the client has chosen to empty all their pension pot in one go and they do have other PAYE or pension income other than the state pension;

Form P55 – where the client has taken a lump sum payment which doesn’t use up all of their pension pot, they have only taken a single payment and don’t intend to take further payments in that tax year.

steve@bicknells.net

Will you be taxed if you inherit a Pension Fund?

IHT only applies if the pension company has to pay the value of your scheme to your estate, in which case it becomes like any other asset, but generally the pension pot is held in a discretionary trust, which means it isn’t taxed on death.

You can now nominate anyone not just dependents to be the beneficiary.

Since 6th April 2015 anyone who inherits a pension fund from a person who dies before the age of 75 is entitled to receive it tax free and the you can take the money as a lump sum or income. Once over 75 a special tax of 45% applies (previously 55%), you could reduce this by taking a regular income.

From 6th April 2016 the 45% tax is likely to be scrapped and income tax rates will be applied.

The BBC website has a useful post which explains the changes in 10 questions, click here to read it

steve@bicknells.net

Will cashing in your annuity lead to a better pension?

The chancellor George Osborn has announce that he plans to allow pensioners to cash in their annuities.

Before the pension reforms….

Individuals saved into a pension during their working life and so built up a pension pot.

At some point during the first years of retirement, they used the money to buy an annuity from an insurance company.

This is a transaction that occurs once, and only once.

An annuity is an annual retirement income that is paid to them for the rest of their life.

From April 2016 the proposal is to allow pensioners to swap an annuity for a fixed lump sum.

But will pensioners be able to find investments which are better than the annuity they currently have?

steve@bicknells.net

Who cares what you think?

Are testimonials worth anything?

Many websites include “testimonials” from “customers”, but do they have any worth? If you want to attract new business it is good to be able to publish positive feedback, which helps demonstrate the value that other customers find in your service. The problem is that if reviews are obviously edited and self-selected they are not obviously representative of the views of your customers. Single line reviews taken out of context can be particularly misleading!

Use external review sites

One of the best-known review sites is tripadvisor. The greatest strength of these reviews is that hotels and restaurants etc have no control over the reviews. They have the opportunity to respond to criticism, but can’t cherry-pick the best reviews to give a false impression. The Pensions Regulator website is keen to point out that “private sector organisations we link to are not endorsed by Government and are provided for information only”; however it is worth noting that they include a link to VouchedFor on their advice page for individuals and in their guide to finding an advisor for Pension Auto Enrolment.

VouchedFor

If you are looking for a hotel you would probably prefer to check tripadvisor rather than lot of different websites for reviews. VouchedFor works along similar lines to tripadvisor, but for Accountants, Financial Advisors and Solicitors. Professionals who have a listing on the site must confirm that they recognise the name / email address of any reviewer before the review is posted online. Just like tripadvisor the professionals can’t read the review until is online so they can’t edit out any negative feedback and poor scores.

Tim Alter appeared in the guide in The Sunday Telegraph on March 29th. You can also read all his great client reviews on his VouchedFor profile!

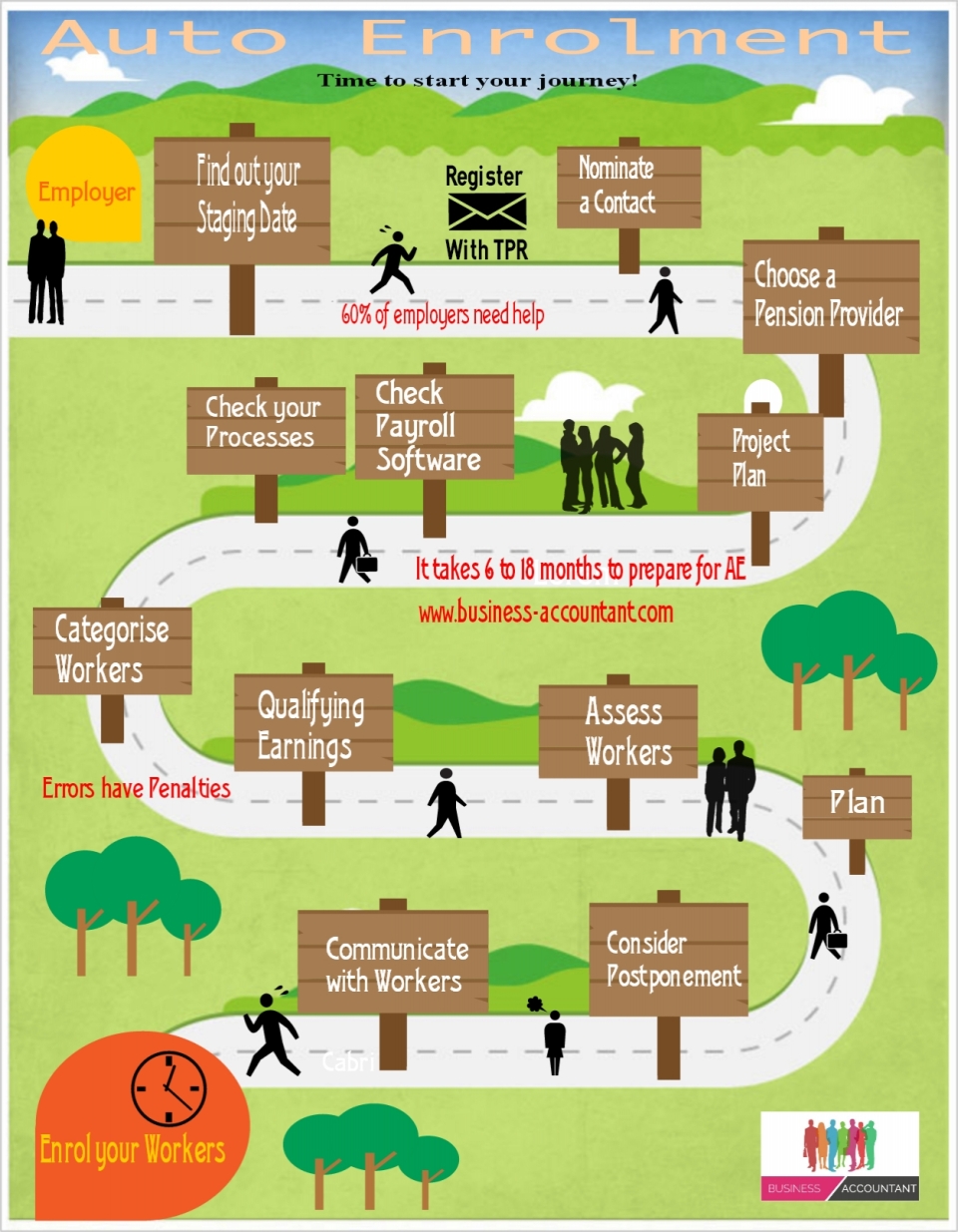

Auto Enrolment

Many small businesses will need professional advice to help them set up a pension scheme to comply with Auto Enrolment regulations. If you are an employer and still need to prepare for your staging date, you can use an Accountant or Financial Adviser to guide you through the process. For help with setting up your payroll and preparing for your staging date, please contact Alterledger.

Related articles

Will you pay Class 3A NI to top up your Pension?

From 12 October 2015 to 5 April 2017 you’ll be able to make a ‘Class 3A voluntary contribution’ to top up your State Pension by up to £25 per week.

You can choose to top up your State Pension by between £1 and £25 per week. How much you’ll need to contribute depends on:

- how much extra pension you want to get each week

- how old you are when you make the contribution

Example You are 68 years old in October 2015. You decide that you want to get an extra £5 per week (£260 a year) on top of your pension.

The cost of an extra £1 per week for a 68 year old is £827, so you multiply £827 by 5.

You’ll make a lump sum payment of £4,135.

You can use this calculator to see how it works…

https://www.gov.uk/state-pension-topup

Here is a link to the legislation…

http://www.legislation.gov.uk/ukdsi/2014/9780111121689/contents

steve@bicknells.net

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Common Auto Enrolment mistakes..

The Pensions Regulator (TPR) has recently highlight the following problem areas:

- Employer forgeting to do the declaration of compliance within 5 months of staging, many employers wrongly assumed that registering on the Government Gateway was enough.

- Confusion caused by running multiple payrolls for the same employer for example weekly and monthly

- Completing the declaration of compliance but without choosing a pension provider

- Omitting self employed workers who have a contract to provide work personally

steve@bicknells.net

5 Key Tests the employer must pass to borrow from a Pension Scheme

There are five key tests that a loan from a Pension Scheme must satisfy to qualify as an authorised employer loan. If a loan fails to meet one or more of these tests an unauthorised payment charge will apply.

The five key tests are

- security

- interest rates

- term of loan

- maximum amount of loan and

- repayment terms.

Security [S179, Sch 30]

If a registered pension scheme makes a loan to an employer the amount of the loan must be secured throughout the full term as a first charge on any asset either owned by the sponsoring employer, or some other person, which is of at least equal value to the face value of the loan including interest.

If the asset used as security is taxable property then there may be additional tax charges under the taxable property provisions if the registered pension scheme is an investment regulated pension scheme.

Taxable property consists of residential property and most tangible moveable assets. Residential property can be in the UK or elsewhere and is a building or structure, including associated land, that is used or suitable for use as a dwelling. Tangible moveable property are things that you can touch and move. It includes assets such as art, antiques, jewellery, fine wine, classic cars and yachts.

Interest Rates [S179, Sch 30]

All loans made by registered pension schemes to employers must charge interest at least equivalent to the rate specified in The Registered Pension Schemes (Prescribed Interest Rates for Authorised Employer Loans) Regulations 2005 (SI 2005/3449). This is to ensure that a commercial rate of interest is applied to the loan.

The minimum interest rate a scheme may charge is calculated by reference to 1% above the average of the base lending rates of the following 6 leading high street banks:

- The Bank of Scotland

- Barclays Bank plc

- HSBC plc

- Lloyds TSB plc

- National Westminster plc and

- The Royal Bank of Scotland plc.

The average rate calculated should be rounded up as necessary to the nearest multiple of ¼%.

Term of Loan [S179, Sch 30]

The repayment period of the loan must not be longer than 5 years from the date the loan was advanced. The total amount owing (including interest) must be repaid by the loan repayment date.

Maximum Amount of Loan [S179, Sch 30]

Section 179 (1)(a) of Finance Act 2004 restricts the amount of a loan which can be made to a sponsoring employer to 50% of the aggregate of the amount of the cash sums held and the net market value of the assets of the registered pension scheme valued immediately before the loan is made. These restrictions are necessary because although such loans provide a useful source of business funding, there may be liquidity problems for the scheme if there is a sudden requirement to provide scheme benefits. It may also not be prudent to lend scheme funds to one company.

Repayment Terms [S179, Sch 30]

All loans to employers must be repaid in equal instalments of capital and interest for each complete year of the loan, beginning on the date that the loan is made and ending on the last day of the following 12 month period – known as a loan year.

Often Land and Commercial Property are used as the security for Pension Scheme loans but the problem is having first charge over the asset!

steve@bicknells.net