Home » Uncategorized (Page 2)

Category Archives: Uncategorized

What if you write off an intercompany or directors loan?

Steve J Bicknell Tel 01202 025252

Connected party loans are a problem area especially if the loan is impaired (ie the borrower may not be able to repay the debt)

Individual Loans written-off

If an individual makes a loan to a company and this is subsequently written-off, the company will have a non-trading loan relationship credit equal to the amount written off.

If the loan was made to an unquoted trading company, the individual will crystalise a capital loss equal to the amount of the loan written off. This will be available to set off against capital gains arising in the year of write-off or in subsequent years.ACCA

View original post 612 more words

HMRC continue to target small businesses – are you ready for a visit?

Steve J Bicknell Tel 01202 025252

According to recent reports HMRC has increased the number of small business investigations and they continue to be seen as soft targets.

About 7% of tax inspections are random, the majority are triggered because HMRC believes that something is wrong.

What can you do to reduce your chances of being selected:

1. File your tax returns on time and pay what you owe – If you file late or at the last minute HMRC will think you are disorganised and as such there are more likely to be errors in the return

2. Declare all your income – HMRC get details of bank interest and other sources of income, sometimes they test them and match them to returns

3. Use an accountant – Unrepresented taxpayers are more likely to be looked at, mainly because many of them don’t know what they are doing

4. Trends – if your business doesn’t…

View original post 58 more words

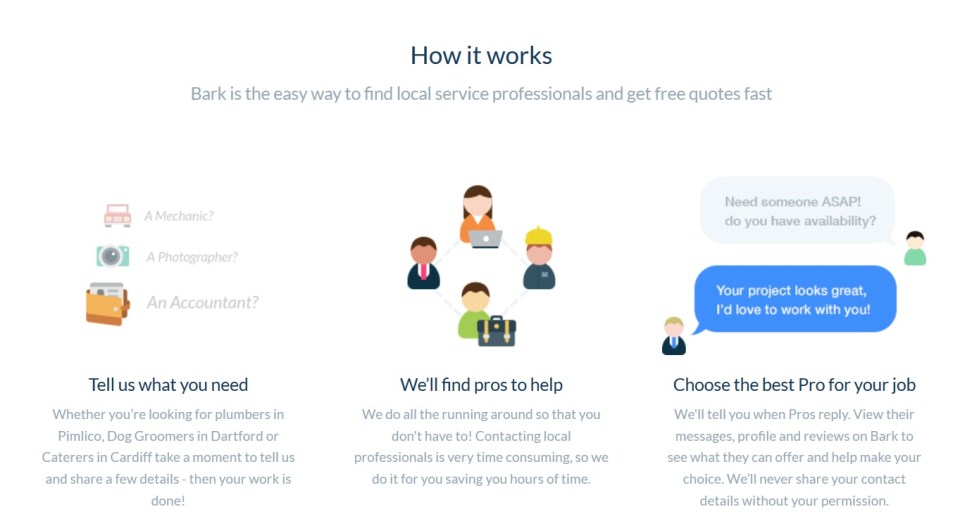

Where can you find a trusted professional?

Steve J Bicknell Tel 01202 025252

The internet is full of sites that allow you to search a list of ‘trusted’ experts and get quotes.

But you are choosing from a select few who have decided to pay for leads, that doesn’t necessarily mean they are the best choice.

Most organisations will have google recommendations and feedback which does help although some sites only show positive feedback.

I have recently came across http://www.bark.com

The Association of UK Accountants has recently partnered with Bark.

“People turn to Bark every day to find pros to help them with everything from lawn mowing to legal representation,” says Bark cofounder Kai Feller. “We’re committed to finding the highest quality professionals for our users, and this new partnership with the Association of UK Accountants will make it even easier for us to help entrepreneurs throughout the UK find quality business accountants.”

There are lots of great things about Bark

- It shows…

View original post 27 more words

Don’t forget to deduct expenses – common expenses that you can set against your rental income

The Chancellor appears to have it in for landlords at the moment. There is the stamp duty land tax supplement of 3% on purchases of second and subsequent residential properties where completion is on or after 1 April 2016, the restriction in interest rate relief from April 2017 onwards, and the failure to benefit from the cut in capital gains tax from 6 April 2016.

In this harsher climate, it is perhaps worthwhile making sure you have not overlooked any deductible expenses when working out your profit for your property rental business.

Wholly and exclusively

The wholly and exclusively rule applies to determine whether an expense is deductible – if it has been incurred wholly and exclusively for the purposes of the property rental business, it passes this test.

Revenue not capital

A deduction against profits is only available if the expenditure is revenue in nature rather than capital. Broadly, revenue expenses are those incurred in the day-to-day running of the business. By contrast, capital expenditure is that incurred in purchasing or improving an asset, and would include costs of extending or improving the property, a fitted kitchen or expenditure on office equipment or vehicles. However, a deduction is available for replacement furnishings from April 2016.

Expenses checklist

The following is a list of common expenses that may be deducted when computing profits (as long as the wholly and exclusively test is met):

- interest on loans to buy the property (but not capital repayments);

- letting agents’ fees;

- accountants’ fees;

- legal fees for lets of a year or less or for renewing a lease of 50 years or less;

- utility bills (e.g. gas, electricity);

- buildings and contents insurance;

- cleaning costs;

- maintenance costs (but not improvements);

- costs of a gardener;

- telephone calls;

- stationery and postage;

- advertising;

- staff costs;

- ground rent and service charges; and

- council tax.

This list is not exhaustive.

Replacement of furnishings

From April 2016 a deduction is available for the costs of replacing furniture, furnishings, appliances (including white goods) and kitchenware. The amount of the deduction is the cost of the replacement item (capped at the cost of an equivalent to the item replaced if the replacement is superior to the original) plus any incidental costs of acquiring the new item (such as delivery) or disposing of the old item, less anything received for the old item.

This deduction replaces the 10% wear and tear allowance but, unlike the wear and tear allowance, is not limited to furnished lets.

Need to know: Make sure you have taken out all of your deductible expenses when working out the tax on your property rental income.

The tax advantages of Furnished Holiday Lets

Steve J Bicknell Tel 01202 025252

There are special tax rules for rental income from properties that qualify as Furnished Holiday Lettings (FHLs).

If you let properties that qualify as FHLs:

- you can claim Capital Gains Tax reliefs for traders (Business Asset Rollover Relief, Entrepreneurs’ Relief, relief for gifts of business assets and relief for loans to traders)

- you are entitled to plant and machinery capital allowances for items such as furniture, equipment and fixtures

- the profits count as earnings for pension purposes

In addition:

- The Interest Rate Relief Restrictions don’t apply – these rules only affect Buy to Let Investors

- Losses can be set against total income and are not restricted to the rental business; PIM4200 onwards deals with normal rental business losses and PIM4130 deals with furnished holiday lettings losses.

The letting condition

You must let the property commercially as furnished holiday accommodation to the public for at least 105 days in the…

View original post 269 more words

Does your accountant use e signatures?

Steve J Bicknell Tel 01202 025252

The days of ‘wet’ signatures may be numbered, sending documents by post to get original ink signatures is slow process, times are changing.

The UK government divides electronic signature into three groups:

- Simple electronic signatures – these include scanned signatures and tick box declarations

- Advanced electronic signatures – can identify the user, is unique to them, is under the sole control of the user and is attached to a document in a way that it becomes invalidated if the contents are changed

- Qualified electronic signatures – an advanced electronic signature with a digital certificate encrypted by a secure signature creation device eg Smart Card

Here is the full government guidance https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/356786/bis-14-1072-electronic-signatures-guide.pdf

I am a big fan of Adobe who say….

View original post 133 more words

Are you ready for Auto Enrolment?

Steve J Bicknell Tel 01202 025252

The tidal wave of small businesses going through Auto Enrolment has now started with the peak being next year in 2016/17.

So what do you need to do before you stage?

- Find out your staging date, this the date when your obligation under Auto Enrolment will start, the Pension Regulator calculator is a good place to start

- Nominate a person to be the Pension Regulators key contact and register their name with the Regulator

- Draw up a Project Plan and consider whether you need help (60% of companies currently staging have decided they do need help! and most businesses will start by asking their accountant to help with project management)

- Choose a Pension Provider – Nest, Now Pensions and The Peoples Pension are the 3 largest

- Makesure your Payroll can provide the analysis needed – Brightpay works with the providers shown below, does your payroll?

In addition you will need…

View original post 20 more words

Overdrawn directors accounts will now cost 32.5%

Steve J Bicknell Tel 01202 025252

Directors often borrow from their companies and this incurs a temporary tax charge.

The rate of tax charged on loans to participators and other arrangements (currently 25%) is being specifically linked to the dividend upper rate, which will be 32.5% from 6 April 2016.

Section 455 CTA 2010 liabilities must be included in a company’s CT600 tax return. The S455 tax forms part of the calculation of tax payable by the company under Paragraph 8 Schedule 18 FA 1998.

A claim to relief under Section 458 is a claim for relief against the original tax charge for the AP in which the loan was made. The time limit for the claim is four years from the end of the financial year in which the loan is repaid, released or written off. COM53120

You must use form L2P to enable a close company which has paid tax on a loan to…

View original post 23 more words

What is the optimum salary for 2016/17?

Steve J Bicknell Tel 01202 025252

There have been several tax changes in the Budget:

- Changes to Personal Allowances –

The Personal Allowance is the amount of income you can earn before you start paying Income Tax. This is currently £10,600 – it will already rise to £11,000 in 2016, and will now increase further to £11,500 in April 2017.The point at which you pay the higher rate of Income Tax will increase from £42,385 to £43,000 in 2016 and to £45,000 in April 2017.

- Employment Allowance – The employment allowance is £3,000 but there is a restriction on it being used by single person companies.

- Dividend Tax -From April 2016 you’ll pay tax on any dividends you receive over £5,000 at the following rates:

- 7.5% on dividend income within the basic rate band

- 32.5% on dividend income within the higher rate band

- 38.1% on dividend income within the additional rate band

This simpler system…

View original post 242 more words

Travel and Subsistence tax restrictions starting in April 2016

Steve J Bicknell Tel 01202 025252

It’s estimated that 430,000 contractors will be affected by the new rules!

Under the new rules certain groups of workers will no longer be able to claim tax relief on travel and subsistence expenses, specifically:

- Those employed via umbrella companies (employment intermediaries).

- If you personally provide services to another person.

- The draft legislation confirms that limited company contractors are not affected by this new restriction, except for any contract work they carry out which is caught by the IR35 rules.

We expect that the new rules will prevent claims for routine travel but allow exceptional travel. For example say you normally work in London that would be excluded but they you have to go to a meeting in Birmingham, that trip should be allowed.