To maintain public confidence in the work of charities, charity law requires most charities (income over £10,000) to have an external scrutiny of their accounts. Provided a charity is not required by law or its governing document to have an audit then trustees may choose a simpler and less expensive form of external scrutiny called an independent examination.

Trustees may opt for an independent examination instead of an audit provided their charity’s gross income is not more than £500,000, or where gross income exceeds £250,000 its gross asset are not more than £3.26 million

Details in Charity notice CC31

Its estimated that approximately 90,000 UK charities require independent examination and that there are approximately 20,000 independent examiners.

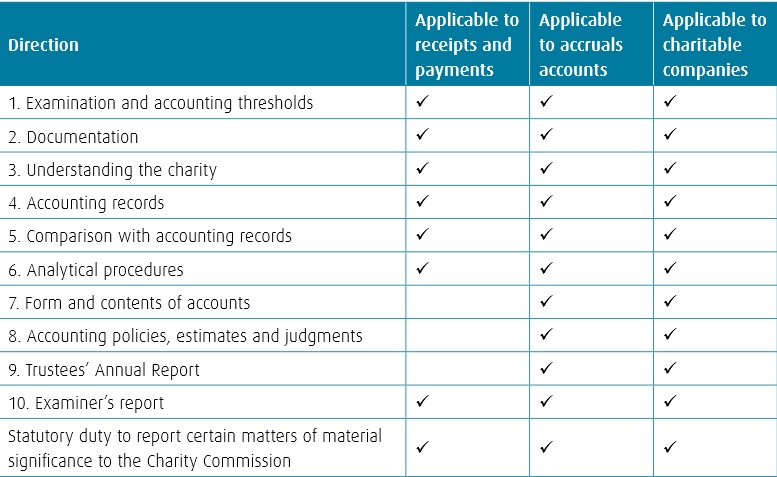

The Charity Commission has a Framework in Notice CC32 to explain what the examiner needs to do

Common problems found by the charity commission include:

- The examiners report being signed by an organisation when in fact the must be signed by an individual

- Failing to address all the directives in the framework

- Insufficient scrutiny of the records

steve@bicknells.net