Home » Posts tagged 'Charity'

Tag Archives: Charity

Can you Zero Rate Charity adverts?

The supply of advertising to a charity is zero-rated. The zero-rating covers advertisements on any subject, including staff recruitment. A charity can also purchase pre-printed collecting boxes, envelopes and appeal letters at the zero rate. Low cost lapel stickers, emblems and badges that a charity gives in acknowledgement of a donation can also be zero-rated. More information can be found in Notice 701/58 Charity advertising and goods connected with collecting donations.

In what media can charities advertise VAT free?

Any medium which communicates with the public. This includes all the conventional advertising media such as television, cinema, billboards, the sides of vehicles, newspapers and printed publications. The important factor is whether the advertisement is placed on someone else’s time or space. If it is not there will be no scope for zero-rating.

If space is sold to a charity for advertising on other items, such as beer mats, calendars, or the reverse of till rolls, this will also be covered by the zero rate. The sale of the items themselves will not be VAT free, unless they qualify for other reliefs for example as books or children’s clothing.

Recently I was asked if a website would be able to zero rated, but its specifically excluded under UK Law VCHAR11000

10B None of items 8 to 8C includes a supply used to create, or contribute to, a website that is the charity’s own.For this purpose a website is a charity’s own even though hosted by another person. 10C Neither of items 8 to 8C includes a supply to a charity that is used directly by the charity to design or produce an advertisement.

steve@bicknells.net

Are your charity accounts being correctly examined?

To maintain public confidence in the work of charities, charity law requires most charities (income over £10,000) to have an external scrutiny of their accounts. Provided a charity is not required by law or its governing document to have an audit then trustees may choose a simpler and less expensive form of external scrutiny called an independent examination.

Trustees may opt for an independent examination instead of an audit provided their charity’s gross income is not more than £500,000, or where gross income exceeds £250,000 its gross asset are not more than £3.26 million

Details in Charity notice CC31

Its estimated that approximately 90,000 UK charities require independent examination and that there are approximately 20,000 independent examiners.

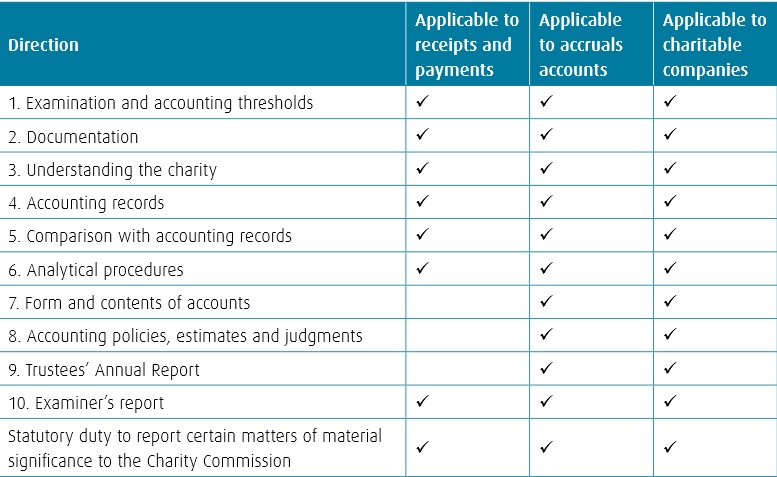

The Charity Commission has a Framework in Notice CC32 to explain what the examiner needs to do

Common problems found by the charity commission include:

- The examiners report being signed by an organisation when in fact the must be signed by an individual

- Failing to address all the directives in the framework

- Insufficient scrutiny of the records

steve@bicknells.net

4 Things a charity needs to know about annual reporting

Image courtesy of Stuart Miles / FreeDigitalPhotos.net

Charities survive on their reputation.

Whether your charity is funded from voluntary donations, grant funding or commercial activities it is important that all funders can look up key information to check your organisation is working effectively. The annual reporting is time-consuming and potentially costly, but it is possible to restructure a charity to save on administrative costs.

1 – Charities must report to their regulator

Charities in England & Wales with an annual income of over £10,000 must report to the Charity Commission for England and Wales. Charities in Scotland must report to the Office of the Scottish Charity Regulator. The Charity Commission for Northern Ireland has recently been set up for the regulation of charities in Northern Ireland.

2 – Cross border charities must report multiple times

Under the Charities and Trustee Investment (Scotland) Act 2005 (the 2005 Act), bodies which represent themselves as charities in Scotland are required to register with OSCR. This requirement includes bodies which are established and/or registered as charities in other legal jurisdictions, such as England and Wales.

3 – Not all charities require an audit

Historically, the term ‘audit’ has been used loosely to describe any independent scrutiny of accounts. However, under the Charity Regulations if the term ‘audit’ is used in a charity’s constitution or governing document the charity must have its accounts audited by a registered auditor.

Charity Trustees may consider that the benefits of having an audit are outweighed by the costs. Trustees may wish to review their constitution and either:

- retain the term audit in their constitution or

- amend the constitution to require an independent examination of the accounts

Any change to the constitution must be carried out in accordance with the terms of the constitution and following professional advice. Notification of any change must also be sent to the charity’s regulator.

If an audit is not required by your members or governing document, an independent examination can be much more cost-effective than a full external audit and can be carried out by wider range of accountants and financial professionals including a member of the Chartered Institute of Management Accountants.

4 – Your current legal form may not be the best for you

Many charities have been set up with archaic governing documents and may be a Trust or Limited Company or other type of body, which is no longer suited to them. Trustees of Trusts and Unincorporated Associations are personally liable for the actions of a charity and expose themselves to a greater risk that Trustees of a Limited Company. Trustees of a Limited Company are required to report to Companies House as well as their charity regulator, increasing the administrative cost of the organisation.

A new legal form has been developed to allow charities to incorporate and report to just one body. Any Charitable Incorporated Organisation in England & Wales or Scottish Charitable Incorporated Organisation in Scotland is recognised as a corporate body which is a legal entity having, on the whole, the same status as a natural person.

This means it has many of the same rights, protections, privileges, responsibilities and liabilities that an individual would have under the law. As a legal entity, the CIO / SCIO may enter into the same type of transactions as a natural person, such as entering into contracts, employing staff, incurring debts, owning property, suing and being sued. As the transactions of the CIO / SCIO are undertaken by it directly, rather than by its charity trustees on its behalf, the charity trustees are in general protected from incurring personal liability in the same way company directors of a Limited Company.

In England and Wales you can:

- apply to register a completely new organisation as a CIO

- set up a CIO to replace an existing unincorporated association or trust

(You can’t currently convert a charitable company to a CIO)

In Scotland you can:

- apply to register a completely new organisation as a SCIO

- convert existing charitable companies, charitable industrial and provident societies and charities of any other legal form to a SCIO

For more information on an accountancy firm who can provide the statutory reporting, and also support you in the running of your charity please contact a member of the Chartered Institute of Management Accountants using the link to The Team above.

Useful links

| Charity Commission: | http://www.charitycommission.gov.uk/ |

| OSCR: | http://www.oscr.org.uk/ |

| Charity Commission NI: | http://www.charitycommissionni.org.uk/ |