Home » Posts tagged 'Pension' (Page 2)

Tag Archives: Pension

My staff want to Opt Out of Auto Enrolment…

Not every employee will want to be in Auto Enrolment, for example they may have their own pension arrangements.

But be very careful that you don’t induce or encourage them to opt out.

Most employees will want to be IN

Once staff have been enrolled into the pension scheme, they have one calendar month during which they can opt out and get a full refund of any contributions. This is known as the ‘opt-out period’. It starts from the whichever date is the later of:

- the date active membership was achieved, or

- the date they received your letter with the enrolment information.

Staff can’t opt out before the opt-out period starts or after it ends. If they decide to leave the scheme outside this period, they will instead be ‘ceasing active membership’. Whether they get a refund of contributions will depend on the pension scheme rules.

Staff opt out by giving you an ‘opt-out notice’. The opt-out notice is provided by the pension scheme. This is to avoid any employer involvement in the decision to opt out, which could lead to a breach of the law.

If an employer does anything to encourage or induce an employee or potential employee (at interview) to opt out they will be subject to harsh penalties.

If an employee does Opt Out they will be re-enrolled every 3 years.

steve@bicknells.net

5 reasons to move business premises into your pension?

Often business premises are owned by the business, this could be for many reasons for example the business has multiple owners or it helps to increase the business net worth.

But in many cases it would be better for the premises to be owned by the business owners pension fund because:

- The object of the business is not to own its own property, the objective should be for the business to make profits from trading

- The business could use cash tied up in the premises to invest in trading activities

- Pensions are a very tax efficient method of ownership – no capital gains, no tax on rental profits

- Company Pension Contributions are Tax Deductible and Individual contributions get income tax refunds

- You may be able to use 3 year Carry Forward to get funds into your pension scheme

In summary to move your business premises from your business to a SIPP or SSAS pension you would do the following:

- Find a lender prepared to lend a third of the property value to your pension scheme (which will be half the value of the fund ie if the property was valued at £300k, your pension could borrow £100k which is 50% of the £200k which will need to be funded by your pension scheme)

- Have the premises independently valued and rent assessed and appoint solicitors

- Create a SSAS or SIPP pension (you can include other people in your SSAS or SIPP investments)

- Transfer into your SSAS or SIPP any funds you have in other pension schemes

- As you are the business owner and its your pension scheme your business could make a payment into your pension scheme, the maximum for the last 3 years would be £140k (£50k + £50k + £40k) see details of NRE

- The pension contribution from your company could be an In Specie payment (meaning its in kind not cash)

- You could make a personal payment to your pension and if you are a higher rate tax payer your will get a tax refund via your self assessment return

- Then your pension scheme buys the premises from your business and rents it back to the business

steve@bicknells.net

How does Auto Enrolment Postponement work?

You can choose to postpone automatic enrolment for up to three months for some or all of your staff. You must write to your staff to tell them you’re postponing automatic enrolment for them. One of the times you can postpone is from your staging date.

Key points

- You can postpone automatic enrolment for up to three months from certain dates.

- If you postpone from your staging date, your staging date does not change.

- If you choose to postpone from your staging date, you must write to tell the staff who will be postponed within six weeks of your staging date.

Why Postpone?

- Its unlikely that your payroll processing period will match your staging date, most staging dates are the 1st of the month but many payrolls are weekly, it makes sense to start auto enrolment on a pay processing date

- If you have short term staff or you are a temp agency you will probably postpone in order to avoid unnecessarily assessing staff who will leave within the postponement period

- You may also postpone to reduce auto enrolment pension payments and admin

- You can choose any business reason

When can you postpone?

You can only postpone automatic enrolment from:

- your staging date

- a staff member’s first day of employment

- the date a staff member first becomes eligible for automatic enrolment.

If you postpone from your staging date, it doesn’t change your staging date.

Staff whose automatic enrolment you’ve postponed can choose to opt in to your pension scheme during the postponement period.

The Pension Regulator has further details

Don’t mess this up, if you don’t get postponement right…..

- You will get a Warning

- Followed by a penalty of £400

- Followed by fines of £500 to £2,500 per day (depending on the number of employees)

Even the smallest business will get fines of £50 per day!

steve@bicknells.net

You will initially be given a warning, which will be followed by a fixed penalty of £400. Not too severe so far, but then the penalties shoot up for those companies who still fail to comply.

If you employ between 50 and 249 employees the fine for on-going non-compliance is a whopping £2,500 per day. For businesses with fewer employees, between five and 49 the penalty is still £500 per day and even the smallest of businesses will be fined £50 per day.

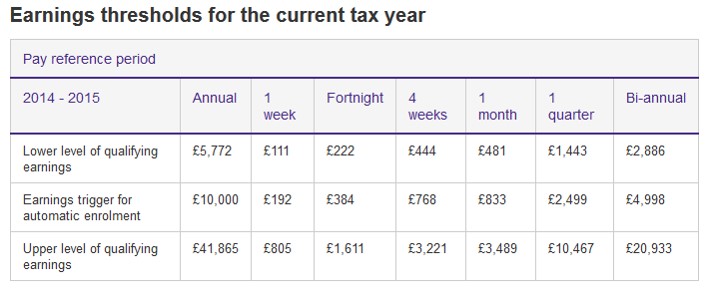

What are Qualifying Earnings for Auto Enrolment?

These are defined as sums which you pay to an employee in connection with his or her employment. They can be salary, wages, commission, bonuses, overtime. Statutory sick pay and maternity/paternity/adoption pay are included too. Benefits in kind (known as P11D benefits), for example, car and fuel, and tips and gratuities do not have to be included. In 2014/2015 Qualifying Earnings are earnings between £5772 and £41,865.

Employers are only required enrol employees earning over the Earnings Trigger of £10,000 (subject to age criteria) but employees can opt in once they earn above the lower level. According to Payroll and Benefits Magazine...

The AE process can be very administration-heavy and, unlike Real Time Information, employees and workers will have to be continually assessed. For example, employers will need to continuously monitor their workforce to identify when a jobholder must be automatically enrolled. In particular, the employer will need to monitor a worker’s age because this may trigger AE and opt-in activity.Although small employers will need at least six months before their staging date to prepare for AE, larger ones may need between 12 and 18 months.AE does not only apply to employees, but also to workers, including contractors who provide services on a personal basis but not as a company.

Can you cope with Auto Enrolment?

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was.

58% had not set up an auto-enrolment pension scheme.

90.5% of employers without an auto-enrolment pension scheme hadn’t even started researching one.

If you think you can ignore Auto Enrolment, think again, The Pensions Regulator will make you comply……..

Non-statutory action

We can issue guidance and instruction by telephone, email, letter and in person. Or we can send a warning letter confirming a set time frame for compliance with the duties.

Statutory notices

Statutory notices can direct you to comply with your duties and / or pay any contributions you have missed or are late in paying. We have further discretionary powers which allow us to estimate and charge interest on unpaid contributions and direct you to calculate and / or pay unpaid contributions.

Penalty notices

We can issue penalty notices to punish persistent and deliberate non-compliance.

A fixed penalty notice will be issued if you don’t comply with statutory notices, or if there’s sufficient evidence of a breach of the law. This is fixed at £400 and payable within a specific period.

We can also issue an escalating penalty notice for failure to comply with a statutory notice. This penalty has a prescribed daily rate of £50 to £10,000 depending on the number of staff you have.

We can issue a civil penalty for cases where you fail to pay contributions due. This is a financial penalty of up to £5,000 for individuals and up to £50,000 for organisations.

Where employers fail to comply with a compliance notice or there is evidence of a breach, we can issue a prohibited recruitment conduct penalty notice. This is currently set at a maximum fixed daily rate of £5,000 for organisations with over 250 staff. We aim to fully recover all the penalties that we issue.

Court action

We can take civil action through the court to recover penalties.

Employers who deliberately and wilfully fail to comply with their duties may be prosecuted.

We can also confiscate goods where there is a criminal conviction and restrain assets during criminal investigations.

The first case was Dunelm http://www.thepensionsregulator.gov.uk/docs/section-89-dunelm.pdf

Research shows that Accountants are most likely to be asked to help SME’s and Business Accountant (a service provided by CIMA Members in Practice) have created a booking service to assist SME’s in getting help https://business-accountant.com/auto-enrolment/

So don’t be scared by Auto Enrolment, don’t delay drawing up a project plan, take action now to avoid problems with the Pension Regulator later!

steve@bicknells.net

When will my business Stage for Auto Enrolment?

Your staging date is the date the new duties come into force for your business. It’s the date from when automatic enrolment activities must become ‘business as usual’, just like real-time PAYE.

You can find out your staging date using the Pension Regulators Calculator or this link provides a quick summary by number of employees.

Auto Enrolment isn’t easy, there is a lot to do before you Stage, here is a checklist (Pension Regulator) of activities you should do 6 months before Staging

Modified staging dates for some small employers

- You can change your staging date to a later date if you:

- had fewer than 50 staff on 1 April 2012, and

- had, or were part of, a PAYE scheme that has more than 50 people in it.

Bringing your staging date forward

All employers are able to bring their staging date forward. You may choose to do this to align it with other business practices, like the start of your financial year.

Or you might have several employers in a corporate group and want to align the smaller employers’ staging dates with the largest. If you plan to do this, you must notify The Pensions Regulator, which you can do online.

You can postpone assessing your workforce for up to 3 months, but this does not change your staging date and staff can choose to opt in during the postponement period.

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope with the preparation for Auto Enrolment and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was!

Did you know …. you can lend money to your own pension

If you have a SSAS or a SIPP Pension you will probably want to invest some of your funds in Commercial Property – Shops, Office, Industrial Units. Pension funds can borrow money and with the current interest rates low and yields as high as 10%, you can increase your return and use less cash by borrowing.

But one thing you may not know is that connected parties can lend to the fund…

Trustees of registered pension schemes may sometimes wish to borrow funds, for example to enable them to purchase an asset. There is no objection to a registered pension scheme borrowing funds for any purpose providing that the scheme administrator/trustees are satisfied that the borrowing will benefit the scheme and that the borrowing is within the rules laid down by the Department for Work and Pensions (DWP).

A registered pension scheme is treated as borrowing or having a liability of an amount, if that amount is to be repaid or met from cash or assets held for the purposes of the pension scheme.

A registered pension scheme may borrow funds from any individual, company or financial institution whether or not they are connected to the scheme, but any borrowing from a connected party which is not made on commercial terms will be subject to a tax charge – see RPSM04104020 .

http://www.hmrc.gov.uk/manuals/rpsmmanual/rpsm07104010.htm

This is useful where you have paid in the maximum allowed pension contributions but you still have cash, so you could lend to your pension to buy a property.

steve@bicknells.net

Do you think it should be compulsory to pay into a pension?

A government think thank, Policy Exchange, have urged the government to make it compulsory that people save for their retirement. Their proposal the ‘Help to Save’ Scheme is aimed at avoiding 11 million people ending up in ‘Pension Poverty’. In a BBC article….

James Barty, author of the report, said the lack of people saving for their retirement was putting an “intolerable burden on the state” which “needs to be addressed sooner rather than later”.

He said: “With an ageing population, putting money aside for later life should be seen in the same context as National Insurance contributions, taxes and even education – an obligation that falls on everyone in society.

“‘Help to Save’ will prevent the state from having to pick up the tab for people who haven’t put aside enough money for later life.”

Under the plans, the opt-out in the Government’s auto-enrolment scheme would be removed making it obligatory for people to save for their retirement

Individual pension contributions would also increase as incomes rise over time.

According to the report, someone earning the average wage – £27,000 – will need to save over six and a half times more than they currently do to generate the Government’s recommended retirement income of £16,200.

The average pension pot is estimated to be just £36,800, which on current annuity rates is enough to generate a retirement income of £1,340.

The paper said that an average earner would need a pot of £240,000, assuming they receive the full single tier pension.

Are you saving enough for your retirement? should saving be compulsory?

steve@bicknells.net

Will Temp Agencies avoid Auto Enrolment by using Postponement?

- Large employers (with 250 or more workers), have started automatically enrolling their workers and will continue to February 2014 (some employers may choose to start earlier)

- Medium employers (50 – 249 workers) will have to start automatically enrolling their workersfrom April 2014 to April 2015

- Small employers (49 workers or less) will have to start automatically enrolling their workers from June 2015 to April 2017

- New employers (established after April 2012) will have to start automatically enrolling their workers from May 2017 to February 2018

- Employers who chose to use Defined Benefit or Hybrid Schemes can delay their staging date until 30 September 2017

You can postpone the start of Auto Enrolment for up to 3 months and then re-test for eligibility using this method could mean that Temporary Staff Agencies could avoid Auto Enrolment for their temps. This also means that many agencies will use NEST because other pension schemes will not want to sign them up as they many not actually receive any contributions.

Pinsent Masons blogged:

Agency workers are different from other workers and so present particular challenges. Many are seeking work for only a short period. Many will register with a number of different agencies and will, in fact, only be ’employed’ by a particular agency for a short period. The auto-enrolment obligation applies to all workers who meet the age and earnings thresholds, but there are options which may assist those employing high churn groups of workers.

Employers can make workers wait up to three calendar months before enrolling them into a pension scheme. If the worker has left by the end of that three-month period, then there is no need to provide that worker with a pension.

If you do postpone, make sure you follow the rules otherwise there could be harsh penalties under the Pension Act 2008 Section 45

Offences of failing to comply(1)An offence is committed by an employer who wilfully fails to comply with—

(a)the duty under section 3(2) (automatic enrolment),

(b)the duty under section 5(2) (automatic re-enrolment), or

(c)the duty under section 7(3) (jobholder’s right to opt in).

(2)A person guilty of an offence under this section is liable—

(a)on conviction on indictment, to imprisonment for a term not exceeding two years, or to a fine, or both;

(b)on summary conviction to a fine not exceeding the statutory maximum.

steve@bicknells.net

3 ways to comply with Employer Auto Enrolment Obligations

Auto Enrolment has arrived and there is a lot to do……

The Pension Regulator website will help you create a stage by stage plan working back from the date when you need to start (staging date), it is a useful planning tool http://www.thepensionsregulator.gov.uk/employers/planning-for-automatic-enrolment.aspx

Most schemes will be set up with one of the following providers:

NEST – National Employment Savings Trust – NEST was originally created by the government – limited help for employers

The Peoples Pension – B&CE – B&CE is well known in the Construction world, they have online tools to help you

Now: Pensions – ATP (Denmark) – 45 year experience in pensions and many awards

You could use another provider and you should take independent expert advise, never give pension or investment advice unless you are qualified to do so.

If you are asked for advice remember to say ‘I know nothing’

But as an employer you do need to select a pension scheme for Auto Enrolment.

Then you need to consider how you will comply with your responsibilities and keep records for:

- Contributions

- Opting Out

- Opting In

- Earnings

- Employee Records

- Communication with Employees

Take a look at this video for middleware to get an understanding of how you could manage your compliance requirements

So here are your 3 basic ways to comply:

- Small Employers – you may decide to do it yourself using information on the Pension Regulators website and provider of your choice

- Pension Provider Portals – schemes like the Peoples Pension will have portals and tools to help you manage your auto enrolment pensions but it won’t cater for other benefits and other schemes

- Middleware – like the video above, this gives lots of functionality and will allow you incorporate other schemes and benefits but its not free

You might also find this blog worth reading ‘10 things you need to know about Pension Auto Enrolment’

steve@bicknells.net