Home » Posts tagged 'Auto Enrolment' (Page 2)

Tag Archives: Auto Enrolment

Automatic enrolment: large employers are all in

![]()

The Pension Regulator’s latest post…..

Our report on the impact of automatic enrolment reveals that 99% of all the UK’s largest employers met their legal duties without the need for us to use our statutory powers.

This is encouraging news as thousands of medium employers are currently reaching their staging dates. We will continue to work over the months ahead to ensure that medium and small employers understand their obligations, comply with their legal duties and continue to view non-compliance by other employers as unacceptable

Are you ready for Auto Enrolment?

steve@bicknells.net

10 of the Biggest Headaches of Auto Enrolment for Employers

According to Now Pensions the 10 biggest headaches faced by employers are:

- An administrative nightmare – it doesn’t have to be nightmare provided you plan ahead and get help if you need it, accountants are the most used source of help and advice.

- Will payroll be able to cope? Yes but it takes planning and preparation

- A Communication challenge – Employees find pensions complicated and auto enrolment could be the first long tem savings product they have, so simplicity is crucial. Auto Enrolment does require the right correspondence at the right time, so make sure you get it right!

- Future Liabilities – The Pension Regulator enforces compliance and employers must not encourage or put pressure on employees to opt out.

- Middleware – this is software that makes your IT systems talk to each other, many SME’s will not need middleware as the payroll software will do the job of reporting the data to the pension provider

- Responsibility – Make sure you know where the responsibilities fall on your team, mistakes can be costly

- Existing Schemes – Not all existing schemes will be suitable for auto enrolment, check that your scheme will comply or change it

- Investment – Most employees will have never invested in their lives so its important to choose an auto enrolment provider who can help them decide on which funds to invest in

- Value for Money – NEST, Now Pensions and The People Pensions have very low charging structures

- What will it cost – Don’t forget the internal management costs when you choose a scheme, how easy will it be to operate?

steve@bicknells.net

We hear many of the same concerns about auto enrolment being raised on a regular basis in our discussions with employers of all sizes. So you’re not alone with your auto enrolment concerns. That’s why we’ve addressed ten of the biggest headaches and their remedies below.

1: An administrative nightmare

Get all the help you can before the staging date. Employers can lighten the load by partnering with providers that will do much of the work for them. Some pension providers have invested in technology that can automate the administration of auto-enrolment. This includes assessing which sort of scheme is most suitable for your workforce, working out which employees need to be automatically enrolled and calculating contributions and issuing communications to your employees based on the outputs of the assessment.

Once a clear process is up and running, administering auto-enrolment is relatively easy – but to get to that point organisations need to put the right systems in place. That means selecting your implementation partners, establishing who is responsible for which parts of the process and ensuring clear access to your HR and payroll data. A robust project plan is essential.

Once a clear process is up and running, administering auto-enrolment is relatively easy – but to get to that point organisations need to put the right systems in place. That means selecting your implementation partners, establishing who is responsible for which parts of the process and ensuring clear access to your HR and payroll data. A robust project plan is essential.

2: Will payroll be able to cope?

Yes, provided you make sure the correct people at your payroll provider and your pension provider are talking to each other and exchanging data in the right format.

A strategic decision is necessary to decide on whether payroll will handle employee categorisation ensuring that your auto-enrolment obligations are met compliantly or whether your pension provider will do this. Larger payroll providers and pension providers such as ourselves have the capability to create a record to demonstrate to the Pension Regulator that you have fully complied with your auto-enrolment obligations.

3: A Communications challenge

Employees find pensions complicated, and for many individuals an auto-enrolment pension will be the first long-term savings product they have ever held. So simplicity is crucial.

Research has shown that messages work best when they speak to employees in a language they understand, through a medium via which they like to be communicated. Messages delivered in the run-up to auto-enrolment are particularly important as they will set the agenda for the entire project. So think about what will work best for your workforce. A wealth of compliant communication material that can be tailored to the needs of your workforce is available at no cost from quality pension providers.

4. Future liabilities

The Pensions Regulator enforces compliance with the auto-enrolment rules, and one of its top priorities is ensuring employers do not encourage or put pressure on employees to opt out of the pension scheme after they have been automatically enrolled into it. It will be scrutinising employers that have unusually high opt-out rates. Employers that persistently break the rules by inducing staff to opt-out can be fined up to £10,000 a day. The Pensions Regulator is hoping whistleblowers will report it of breaches of auto-enrolment regulations.

Using compliant communication materials can alleviate the risk of regulatory action. Employers that use pension providers with auto-enrolment middleware will also have a report that demonstrates to the Pensions Regulator that auto-enrolment obligations have been fulfilled, although it will only be as accurate as the information given by the employer.

5: What is ‘middleware’?

Middleware is software that glues different IT systems together. In the context of auto-enrolment, that means analysing the age and salary data of your workforce, working out the earnings upon which contributions are based, taking deductions through payroll and paying them over to the pension provider.

6: Responsibility

For auto-enrolment to run smoothly both your payroll and pensions departments need to talk to each other. Unfortunately the fact that auto-enrolment crosses both areas can lead to confusion over who is responsible for what part of the process. This is best addressed by assigning auto-enrolment to a corporate sponsor high enough up in your organisation to ensure that responsibility for tasks is clearly apportioned, and delegating someone to be involved through the implementation project phase and beyond.

7: Existing Schemes

This will depend on the sort of scheme you have and how you decide to include your  current non-pensioned staff. If your existing scheme already complies with the minimum criteria set for auto-enrolment, which relate to contribution rates, charges and default funds, then staff already in it will see no change.

current non-pensioned staff. If your existing scheme already complies with the minimum criteria set for auto-enrolment, which relate to contribution rates, charges and default funds, then staff already in it will see no change.

You will need to make some important decisions about how you design your pension offering for the rest of your staff. Do you want a single scheme for everyone in the organisation? Do you want a multifaceted scheme for your senior staff and a more basic scheme for other tiers of your workforce? You may choose to preserve your existing scheme for those already in it, while automatically enrolling those not currently in it into a new scheme. Independent Financial Advisers or Employee Benefit Consultants can provide information and advice in exchange for a fee or Providers like NOW: Pensions can help you to analyse your workforce and provide suggestions based on our previous experience.

8: Investment

Many employees will have never invested this way before in their lives. Poor performance will not only create disgruntled employees – it will also leave some staff with pensions so low they cannot afford to retire when they get older. So choosing the right default investment fund is crucial for an employer.

The performance of different pension providers’ default funds varies hugely. Pensions are long-term savings vehicles which means that even very small increases in performance can make a significant difference. For example, over a 40-year investment, an annual return of 7% will deliver a fund 30% higher than one achieving 6%.

Look for a default fund with a proven track record, one that has delivered stable returns over a long period of time and in different market conditions, and is unlikely to have changed as this may increase the associated communication costs with your employees.

9: Value for money

Charges are one of the biggest factors in determining how much pension employees ultimately receive. Sadly, pensions that charges as much as 1.5% of the fund value each year are common in the UK. We charge just 0.3% of fund value plus a monthly £1.50

Charges are one of the biggest factors in determining how much pension employees ultimately receive. Sadly, pensions that charges as much as 1.5% of the fund value each year are common in the UK. We charge just 0.3% of fund value plus a monthly £1.50

admin fee (£0.30 for low earners during the initial phasing process). For a 25-year-old earning £26,000 saving 8% of salary for 40 years, that can mean the difference between building up a pot of £716,000 rather than the £547,000* generated in a scheme charging 1.5%. Our low charge scheme gives the saver in this example 30% more pension for exactly the same contributions. It may sound hard to believe, but the more expensive provider takes an extra £169,000 in charges out of the saver’s pot.

*Assumes salary increases by 4% a year, fund increases by 7% a year.

10: What will it cost me?

The overall cost of auto enrolment will depend on where you go for your pension and what you need from your pension.

Costs not only include fees and charges but also, human resources and administration so it is important to bear the overall cost in mind when choosing a pension provider. With NOW: Pensions, the employer can either choose to pay nothing in the way of administration with the fees coming from the members or you may choose to pay these fees for your members (employees); on-going costs such as communications are minimal and there are no set-up fees.

It is important to get your provider right from the start as changing further down the line will incur many additional costs.

– See more at: http://www.nowpensions.com/blog/auto-enrolment-headaches/#sthash.HhCRbQuD.dpuf

My staff want to Opt Out of Auto Enrolment…

Not every employee will want to be in Auto Enrolment, for example they may have their own pension arrangements.

But be very careful that you don’t induce or encourage them to opt out.

Most employees will want to be IN

Once staff have been enrolled into the pension scheme, they have one calendar month during which they can opt out and get a full refund of any contributions. This is known as the ‘opt-out period’. It starts from the whichever date is the later of:

- the date active membership was achieved, or

- the date they received your letter with the enrolment information.

Staff can’t opt out before the opt-out period starts or after it ends. If they decide to leave the scheme outside this period, they will instead be ‘ceasing active membership’. Whether they get a refund of contributions will depend on the pension scheme rules.

Staff opt out by giving you an ‘opt-out notice’. The opt-out notice is provided by the pension scheme. This is to avoid any employer involvement in the decision to opt out, which could lead to a breach of the law.

If an employer does anything to encourage or induce an employee or potential employee (at interview) to opt out they will be subject to harsh penalties.

If an employee does Opt Out they will be re-enrolled every 3 years.

steve@bicknells.net

How does Auto Enrolment Postponement work?

You can choose to postpone automatic enrolment for up to three months for some or all of your staff. You must write to your staff to tell them you’re postponing automatic enrolment for them. One of the times you can postpone is from your staging date.

Key points

- You can postpone automatic enrolment for up to three months from certain dates.

- If you postpone from your staging date, your staging date does not change.

- If you choose to postpone from your staging date, you must write to tell the staff who will be postponed within six weeks of your staging date.

Why Postpone?

- Its unlikely that your payroll processing period will match your staging date, most staging dates are the 1st of the month but many payrolls are weekly, it makes sense to start auto enrolment on a pay processing date

- If you have short term staff or you are a temp agency you will probably postpone in order to avoid unnecessarily assessing staff who will leave within the postponement period

- You may also postpone to reduce auto enrolment pension payments and admin

- You can choose any business reason

When can you postpone?

You can only postpone automatic enrolment from:

- your staging date

- a staff member’s first day of employment

- the date a staff member first becomes eligible for automatic enrolment.

If you postpone from your staging date, it doesn’t change your staging date.

Staff whose automatic enrolment you’ve postponed can choose to opt in to your pension scheme during the postponement period.

The Pension Regulator has further details

Don’t mess this up, if you don’t get postponement right…..

- You will get a Warning

- Followed by a penalty of £400

- Followed by fines of £500 to £2,500 per day (depending on the number of employees)

Even the smallest business will get fines of £50 per day!

steve@bicknells.net

You will initially be given a warning, which will be followed by a fixed penalty of £400. Not too severe so far, but then the penalties shoot up for those companies who still fail to comply.

If you employ between 50 and 249 employees the fine for on-going non-compliance is a whopping £2,500 per day. For businesses with fewer employees, between five and 49 the penalty is still £500 per day and even the smallest of businesses will be fined £50 per day.

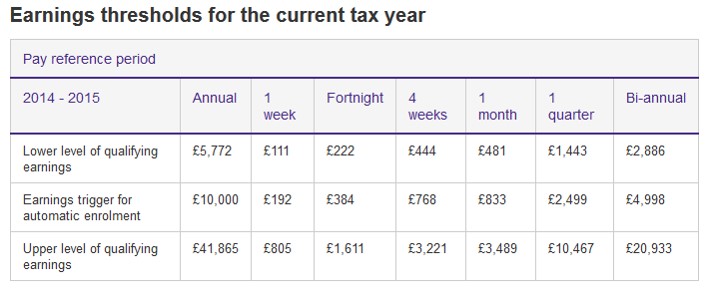

What are Qualifying Earnings for Auto Enrolment?

These are defined as sums which you pay to an employee in connection with his or her employment. They can be salary, wages, commission, bonuses, overtime. Statutory sick pay and maternity/paternity/adoption pay are included too. Benefits in kind (known as P11D benefits), for example, car and fuel, and tips and gratuities do not have to be included. In 2014/2015 Qualifying Earnings are earnings between £5772 and £41,865.

Employers are only required enrol employees earning over the Earnings Trigger of £10,000 (subject to age criteria) but employees can opt in once they earn above the lower level. According to Payroll and Benefits Magazine...

The AE process can be very administration-heavy and, unlike Real Time Information, employees and workers will have to be continually assessed. For example, employers will need to continuously monitor their workforce to identify when a jobholder must be automatically enrolled. In particular, the employer will need to monitor a worker’s age because this may trigger AE and opt-in activity.Although small employers will need at least six months before their staging date to prepare for AE, larger ones may need between 12 and 18 months.AE does not only apply to employees, but also to workers, including contractors who provide services on a personal basis but not as a company.

Can you cope with Auto Enrolment?

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was.

58% had not set up an auto-enrolment pension scheme.

90.5% of employers without an auto-enrolment pension scheme hadn’t even started researching one.

If you think you can ignore Auto Enrolment, think again, The Pensions Regulator will make you comply……..

Non-statutory action

We can issue guidance and instruction by telephone, email, letter and in person. Or we can send a warning letter confirming a set time frame for compliance with the duties.

Statutory notices

Statutory notices can direct you to comply with your duties and / or pay any contributions you have missed or are late in paying. We have further discretionary powers which allow us to estimate and charge interest on unpaid contributions and direct you to calculate and / or pay unpaid contributions.

Penalty notices

We can issue penalty notices to punish persistent and deliberate non-compliance.

A fixed penalty notice will be issued if you don’t comply with statutory notices, or if there’s sufficient evidence of a breach of the law. This is fixed at £400 and payable within a specific period.

We can also issue an escalating penalty notice for failure to comply with a statutory notice. This penalty has a prescribed daily rate of £50 to £10,000 depending on the number of staff you have.

We can issue a civil penalty for cases where you fail to pay contributions due. This is a financial penalty of up to £5,000 for individuals and up to £50,000 for organisations.

Where employers fail to comply with a compliance notice or there is evidence of a breach, we can issue a prohibited recruitment conduct penalty notice. This is currently set at a maximum fixed daily rate of £5,000 for organisations with over 250 staff. We aim to fully recover all the penalties that we issue.

Court action

We can take civil action through the court to recover penalties.

Employers who deliberately and wilfully fail to comply with their duties may be prosecuted.

We can also confiscate goods where there is a criminal conviction and restrain assets during criminal investigations.

The first case was Dunelm http://www.thepensionsregulator.gov.uk/docs/section-89-dunelm.pdf

Research shows that Accountants are most likely to be asked to help SME’s and Business Accountant (a service provided by CIMA Members in Practice) have created a booking service to assist SME’s in getting help https://business-accountant.com/auto-enrolment/

So don’t be scared by Auto Enrolment, don’t delay drawing up a project plan, take action now to avoid problems with the Pension Regulator later!

steve@bicknells.net

Auto Enrolment do you need help?

New research*, from workplace pensions provider NOW: Pensions reveals that four in ten (44%) small and medium sized companies haven’t given any thought to how they’ll go about finding a pension scheme to comply with the new auto enrolment legislation. But, a significant proportion, (14%) intend to get help from their accountant.

Of the 450 small and medium sized firms surveyed 5% are going to consult an IFA, 4% are going to search the market and do the research themselves. Only 2% have already made a decision and secured a scheme.

Over a fifth (22%) intend to use their existing pension provider for auto enrolment. This comes despite growing concern that some providers will not support smaller employers’ auto enrolment needs.

Despite a large proportion of SMEs admitting they are yet to think about their pension scheme, over half (57%) of firms surveyed think that their choice of pension provider is either important (33%) or very important (24%). Only 8% think it is unimportant.

Four in ten (40%) believe offering a good quality pension scheme will help with employee retention and nearly a third (32%) think it will help to improve the attractiveness of their company to potential employees.

Morten Nilsson, CEO of NOW: Pensions continues: “As auto enrolment gathers pace, accountants will play a key role in guiding small and medium sized companies through the complexities of the legislation. For those accountants that manage payroll, auto enrolment is unavoidable so getting to grips with it sooner rather than later is a must.”

Stephen Milne Chair of the CIMA Members in Practice Panel said: “With over 10,000 employers auto enrolling each month, support for SMEs is inevitably in short supply. Accountants are ideally placed to provide much needed help with the process from scheme selection to assessment and implementation.”

Through Business Accountant, a service provided by CIMA Members in Practice, companies facing auto enrolment can book a local CIMA Member in Practice by calling: 023 8064 3763.

*Research undertaken by BDRC Continental, an award-winning insight agency. Questions were put to 450 UK SMEs (up to and including 250 employees) via BDRC Continental’s monthly Business Opinion Omnibus. Telephone-based interviews with a nationally representative sample of senior financial decision makers across the UK, weighted by size, region and sector. Fieldwork dates 3rd to 13th March 2014

**Research conducted online with 264 advisers by Defaqto between 25th November and 5th December 2013.

3 ways to comply with Employer Auto Enrolment Obligations

Auto Enrolment has arrived and there is a lot to do……

The Pension Regulator website will help you create a stage by stage plan working back from the date when you need to start (staging date), it is a useful planning tool http://www.thepensionsregulator.gov.uk/employers/planning-for-automatic-enrolment.aspx

Most schemes will be set up with one of the following providers:

NEST – National Employment Savings Trust – NEST was originally created by the government – limited help for employers

The Peoples Pension – B&CE – B&CE is well known in the Construction world, they have online tools to help you

Now: Pensions – ATP (Denmark) – 45 year experience in pensions and many awards

You could use another provider and you should take independent expert advise, never give pension or investment advice unless you are qualified to do so.

If you are asked for advice remember to say ‘I know nothing’

But as an employer you do need to select a pension scheme for Auto Enrolment.

Then you need to consider how you will comply with your responsibilities and keep records for:

- Contributions

- Opting Out

- Opting In

- Earnings

- Employee Records

- Communication with Employees

Take a look at this video for middleware to get an understanding of how you could manage your compliance requirements

So here are your 3 basic ways to comply:

- Small Employers – you may decide to do it yourself using information on the Pension Regulators website and provider of your choice

- Pension Provider Portals – schemes like the Peoples Pension will have portals and tools to help you manage your auto enrolment pensions but it won’t cater for other benefits and other schemes

- Middleware – like the video above, this gives lots of functionality and will allow you incorporate other schemes and benefits but its not free

You might also find this blog worth reading ‘10 things you need to know about Pension Auto Enrolment’

steve@bicknells.net

10 important things to know about auto enrolment pensions

Here are 10 things that you need to know:

- A Worker may include Agency workers and Self Employed workers depending on the their contracts

- One Person companies are not subject to Auto Enrolment however, if the company takes on a second worker and the director and new employee have contracts of employment then both could become workers under auto enrolment.

- Eligible Job holders are aged between 22 and state pension age and earn over £9,440 and are automatically enrolled however Non Eligible Job holders could opt to join

- Employer contributions will be 1% from October 2012 till 2017 (2% total contributions), then 2% till 2018 (5% total contributions), then go to 3% (8% total contributions)

- The employer must register their scheme www.tpr.gov.uk/registration

- The scheme is being introduced over a 5 year period starting in 2012, to find out when it applies to your business click on this link http://www.thepensionsregulator.gov.uk/employers/staging-date-timeline.aspx

- Employees can opt out but new Employment Rights will prevent employers from offering inducements to opt out and prohibit employers from anti pension recruitment policies and unfair dismissal relating to pension enrolment

- If the employee opts out the employer must automatically re-enrol them every 3 years

- The Pensions Regulator will have powers to issue compliance notices and fixed and escalating penalties increasing on a daily basis. Employees who blow the whistle on their employer will be protected under the Public Interest Disclosure Act 1998

- The following types of scheme will qualify

- Defined Benefit Schemes

- Defined Contribution Schemes

- Hybrid Schemes

- Contract Based DC Schemes

- Stakeholder Pension Schemes

steve@bicknells.net