Home » Tax (Page 3)

Category Archives: Tax

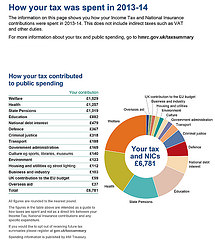

Have you had your annual tax statement?

Back in 2010 the Government promised every taxpayer an annual statement of their tax position – not just the income tax and National Insurance paid, but also where the money was spent.

During October these statement started to be sent out, see the example above.

If you’re registered for online self-assessment you’ll be able to access your statement digitally by logging on to the HMRC website in the usual format, selecting the tax summary option.

Initially the statements will only cover your tax position for 2012/2013 and at first only selected taxpayers will receive one.

Is this a positive step forward or a waste of time?

steve@bicknells.net

TOGC issues on Business Acquisitions

Normally the sale of the assets of a VAT registered or VAT registerable business will be subject to VAT at the appropriate rate. A transfer of a business as a going concern for VAT purposes (TOGC) however is the sale of a business including assets which must be treated as a matter of law, as ‘neither a supply of goods nor a supply of services’ by virtue of meeting certain conditions. Where the sale meets the conditions then the supply is outside the scope of VAT and therefore VAT is not chargeable.

It is important to be aware that the TOGC rules are mandatory and not optional. So it is important to establish from the outset whether the sale is or is not a TOGC.

The main conditions are:

- the assets must be sold as part of the transfer of a ‘business’ as a ‘going concern’

- the assets are to be used by the purchaser with the intention of carrying on the same kind of ‘business’ as the seller (but not necessarily identical)

- where the seller is a taxable person, the purchaser must be a taxable person already or become one as the result of the transfer

- in respect of land which would be standard rated if it were supplied, the purchaser must notify HMRC that he has opted to tax the land by the relevant date, and must notify the seller that their option has not been disapplied by the same date

- where only part of the ‘business’ is sold it must be capable of operating separately

- there must not be a series of immediately consecutive transfers of ‘business’

The TOGC rules are compulsory. You cannot choose to ‘opt out’. So, it is very important that you establish from the outset whether the business is being sold as a TOGC. Incorrect treatment could result in corrective action by HMRC which may attract a penalty and or interest.

Problem areas:

- Gap in trading – for TOGC to apply there must be no significant gap in trading between the sale and purchase

- VAT registration – If the vendor is VAT registered, there can only be a VAT-free TOGC if the purchaser is registered at or before the transfer

- Buying part of a business – the part being bought must be capable of separate operation

- A series of sales – it may not be possible for one of the parties to carry on the trade

- Staged Sales – As long as the overall result is that of business transfer these should qualify for TOGC

steve@bicknells.net

Why Doctors should use Salary Sacrifice for CPE

Doctors often agree to pay for their own continuing training personally because of a shortage of NHS funds but when they do pay for courses its unlikely they will be able to claim tax relief.

EIM32530 states that it is well established that employees are not entitled to an expenses deduction under Section 336 ITEPA 2003 for the expenses continuing professional education (CPE). The Commissioners and the Courts have traditionally held that the duties of trainee doctors, for the purpose of the expenses rule, are limited to the clinical work that they do for the NHS Trust by whom they are employed. Their training activities are not undertaken “in the performance of” those duties for the purpose of Section 336 . That is so even though the training activities may be compulsory, and failure to complete them may lead to the employee losing his or her professional qualifications, and/or their job.

The Commissioners and the Courts upheld that view in a number of cases, as follows:

Parikh v Sleeman (63TC75) – a hospital doctor was refused relief for the expenses of attending training courses during periods of study leave.

Snowdon v Charnock (SpC282) – a specialist registrar was refused relief for the expenses of undergoing mandatory personal psychotherapy.

Consultant Psychiatrist v CIR (SpC557) – an NHS consultant was refused relief for the expenses of CPE necessary to maintain her professional qualification.

Decadt v CRC (TL3792) – a specialist registrar was refused relief for the expenses of taking professional examinations, even though it was a condition of his employment that he should do so.

In the recent case of Revenue & Customs Commissioners v Dr Piu Banerjee ([2010] EWCA Civ. 843), the Court of Appeal accepted that a deduction for training costs incurred by an employee should be allowed if the employee was employed on a training contract where training was an intrinsic contractual duty of the employment (see also EIM32535 & EIM32546) and where any personal benefit, unlike most CPE courses, would be incidental and not therefore give rise to a dual purpose of the expenditure.

Salary Sacrifice solves this problem.

Salary sacrifice works particularly well for training because except in the most extreme cases, employees cannot claim a tax deduction for training costs that they pay personally but if the employer pays for training that is work-related:

- the employer gets the tax deduction

- the employee is not taxed on the cost and

- there is no National Insurance to pay.

EIM01210 confirms this.

steve@bicknells.net

Have you paid too much National Insurance?

Unlike Income Tax which is cumulative and assessed across all earnings, National Insurance starts from zero on each individual employment and you also pay National Insurance on Self Employed earnings.

So if you are a Director of multiple businesses paid as an employee its easy to see how you could over pay and you might not even realise because National Insurance is not shown on your Self Assessment Return.

You can also over pay National Insurance if you are a part time employee with multiple employers and irratic earnings, this because National Insurance is calculated on a weekly/monthly basis, not a cumulative basis and its by employer.

What you need to do

Write to HM Revenue and Customs confirming:

- your National Insurance number

- why you’ve overpaid

- the tax year(s) you’ve overpaid

You should include your P60 or a statement from your employer showing the tax and National Insurance for each year you’re claiming for.

You should apply within 6 years of the tax year you’re claiming for.

HM Revenue and Customs

Payment Reconciliation

National Insurance Contributions Office

Benton Park View

Newcastle upon Tyne

NE98 1ZZ

steve@bicknells.net

Musicians tax breaks

Will Scottish entertainers make more money with proposed musicians tax breaks?

One of the consequences of the Scottish Independence Referendum is a “Command Paper” to be produced by Lord Smith of Kelvin and the Scottish Devolution Commission. Among the proposals being put to the commission is copying an idea from Ireland to give artists and musicians tax breaks.

Special treatment for artists

The Republic of Ireland has given artists a tax exemption since 1969 which means the profits from the sale of works do not attract income tax up to a maximum of €40,000, or £31,500. Everyone agrees that the tax system should be simplified – except of course if it the complication benefits you. Is this a valid sign of support for artists or will everyone want “special treatment”?

Alterledger can help

Why wait for the law to favour your industry? Contact Alterledger or visit the website alterledger.com to see if you can organise yourself better and claim more expenses to cut your tax bill.

If I change my business activity what happens to my tax losses?

Let’s say your current business has been having a tough time and you want to change it to something new, can you carry forward the trading losses.

Probably not look at this example from BIM85050

For example, a publican who had owned a pub in Leeds for many years sold it and bought another in York. Although in the everyday sense the trader remains a publican throughout, the York pub is not the same trade as the Leeds pub.

Tax law requires any losses (including Corporation Tax Losses) carried forward to be offset against future trading profits from the same trade.

One solution to this may be Group Relief, companies which are part of the same Group can surrender losses within the Group.

The rules about which trading losses and other amounts may be surrendered are described at CTM80110. The company that transfers the losses, etc, is called the ‘surrendering company’. The company that claims the losses, etc, is called the ‘claimant company’.

Trading losses, excess capital allowances and non-trading deficits on loan relationships may be surrendered in full. This is irrespective of whether the surrendering company has other profits against which the loss etc might have been, but has not been, set off.

Alternatively it may be possible for the loss making business to sell services to the new business and in doing so reduce its loss.

steve@bicknells.net

Is it a Van or a Car?

It makes a big difference whether a double cab pick up is treated as Car or a Van for tax purposes, in summary:

- Benefit in Kind on Cars is linked to CO2 where as on a Van its Flat Rate (and could be zero if your private use is insignificant)

- Vans qualify for the Annual Investment Allowance, Cars have restricted Capital Allowances

- You can reclaim VAT on Vans but its much harder to reclaim VAT on cars

HMRC have some guidance in EIM23150….

Under this measure, a double cab pick-up that has a payload of 1 tonne (1,000kg) or more is accepted as a van for benefits purposes. Payload means gross vehicle weight (or design weight) less unoccupied kerb weight (care is needed when looking at manufacturers’ brochures as they sometimes define payload differently).

Under a separate agreement between Customs and the Society of Motor Manufacturers and Traders (SMMT), a hard top consisting of metal, fibre glass or similar material, with or without windows, is accorded a generic weight of 45kg. Therefore the addition of a hard top to a double cab pick-up with an ex-works payload of 1,010 kg will convert the vehicle into a car (net payload reduced to 965 kg). Under this agreement, the weight of all other optional accessories is disregarded. HMRC has also adopted this treatment.

http://www.hmrc.gov.uk/manuals/eimanual/eim23150.htm

A double cab with a payload in excess of 1000kg can still be classified as a car if the taxman dealing with the case decides it is a car. You may have to justify a genuine business need for the vehicle.

steve@bicknells.net

Are you ready for the OTS to check your employment status?

Contractor Weekly reported on th 29th July 2014…

As part of the ongoing mission to create a simpler and fairer tax system the Office of Tax Simplification (OTS) has been tasked with carrying out reviews of employment status and also tax penalties, with a view to producing a report in time for next year’s Budget.

According to the OTS, the boundary between employment and self-employment no longer reflects modern working patterns, particularly in recent years. Many people have multiple jobs and can be classed as employed in one whilst self-employed in another. The rise of the freelancing business model has also caused some to suggest this is a ‘third way’ between employment and self-employment.

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

It will be interesting to see the report that the Office of Tax Simplification (OTS) produce, especially if they find a ‘third way’

steve@bicknells.net

5 Creative Tax Reliefs

The Creative Industries have done rather well in the last couple of years as far as tax reliefs go and more are just about to come on stream.

Creative industry tax reliefs (CITR) are a group of 5 Corporation Tax reliefs that allow qualifying companies to claim a larger deduction, or in some circumstances claim a payable tax credit when calculating their taxable profits.

These reliefs work by increasing the amount of allowable expenditure. Where your company makes a loss, you may be able to ‘surrender’ the loss and convert some or all of it into a payable tax credit.

Film Tax Relief (FTR) was introduced in April 2007 and 2 additional reliefs were introduced in April 2013. These are Animation Tax Relief (ATR) and High-end Television Tax Relief (HTR). A fourth relief for Video Games Development was introduced from 1 April 2014. A fifth relief for Theatre Tax Relief is to be introduced in Autumn 2014. HMRC

Let’s take a look at the 5 tax reliefs:

Film Tax Relief (FTR)

Your company will be entitled to claim FTR on a film as long as:

- the film passes the culture test – it is considered a ‘British film’

- the film is intended for theatrical release

- at least 25% of the total production costs relate to activities in the UK

Animation Tax Relief (ATR)

Your company will be entitled to claim ATR on an animation programme if:

- the programme passes the cultural test – a similar test to that for FTR but within the European Economic Area

- the programme is intended for broadcast

- at least 51% of the total core expenditure is on animation

- at least 25% of the total production costs relate to activities in the UK

High-end Television Tax Relief (HTR)

Your company will be entitled to claim HTR on a programme if:

- the programme passes the cultural test – a similar test to that for FTR but within the European Economic Area

- the programme is intended for broadcast

- the programme is a drama, comedy or documentary

- at least 25% of the total production costs relate to activities in the UK

- the average qualifying production costs per hour of production length is not less than £1million per hour

- the slot length in relation to the programme must be greater than 30 minutes

Video Games Development

Your company will be entitled to claim VGTR as long as:

- the video game is British

- the video game is intended for supply

- at least 25% of core expenditure is incurred on goods or services that are provided from within in the European Economic Area (EEA)

Theatre Tax Relief

Details to follow in the Autumn of 2014

steve@bicknells.net

5 ways to pay less VAT

Many small businesses assume there is only one type of VAT scheme, the standard VAT scheme where you pay VAT on Sales and reclaim VAT on Purchases but in fact there are several schemes and they could save you money:

Cash Accounting

Using the Cash Accounting Scheme, you:

- pay VAT on your sales when your customers pay you

- reclaim VAT on your purchases when you have paid your suppliers

You can use the Cash Accounting Scheme if your estimated VAT taxable turnover during the next tax year is not more than £1.35 million.

Cash Accounting can improve your cashflow if your customers pay later than you need to pay your suppliers.

Flat Rate Scheme

You can join the Flat Rate Scheme for VAT and so pay VAT as a flat rate percentage of your turnover if:

- your estimated VAT taxable turnover – excluding VAT – in the next year will be £150,000 or less.

Generally you don’t reclaim any of the VAT that you pay on purchases, although you may be able to claim back the VAT on capital assets worth more than £2,000

There’s a one per cent reduction in the flat rate percentages for your first year of VAT registration.

You can get a list of Flat Rates by following this Link

Flat Rate is easy to use and can save you money if you have a lower than average level of VAT purchases.

Annual Accounting Scheme

Using the Annual Accounting Scheme, you make either nine interim payments at monthly intervals, or three quarterly interim payments, throughout the year. You only need to complete one return at the end of each year. At that point you must pay any outstanding amount. If you have overpaid, you will receive a refund.

You can use the Annual Accounting Scheme if your estimated VAT taxable turnover for the coming year is not more than £1.35 million.

This could save you money by saving time.

Retail Schemes

Using standard VAT accounting, if you are VAT-registered then you must record the VAT on each sale in your accounting records. But with the VAT retail schemes, you work out the value of your total VAT taxable sales for a period – for example, a day – and the proportions of that total that are taxable at different rates of VAT (standard, reduced and zero) according to the scheme you are using. You then apply the appropriate VAT fraction to that sales figure to calculate your VAT due.

You do not need to record VAT separately in your accounts for each and every retail sale you make. This is particularly beneficial if you make a number of low value and/or small quantity sales to the general public. This can save you a lot of time and record keeping.

Margin Schemes

Normally you charge VAT on your sales, and reclaim VAT on your purchases. However, if you sell second-hand goods, works of art, antiques or collectibles, there may have been no VAT for you to reclaim when you bought them. You may be able to use a VAT margin scheme. This enables you to account for VAT only on the difference between the price you paid for an item and the price at which you sell it – your margin. You won’t pay any VAT if you don’t make a profit on a deal. You can still use standard VAT accounting for other sales and purchases such as overheads.

steve@bicknells.net