Home » Small Business (Page 8)

Category Archives: Small Business

‘Bean counter’ view of accountants is holding back entrepreneurs

Some entrepreneurs and small businesses may be holding themselves back by refusing to share information with their accountants who they sometimes regard as little more than “bean counters”, according to a new study.

There is a tendency for UK businesses, to make decisions without adequate financial information or analysis, there is often poor cash flow management and time and opportunities are being wasted because some owner-managers don’t want anyone else to know their business, it concludes.

The report, funded by the Chartered Institute of Management Accountants (CIMA) and compiled by Dr Michael Lucas of the Open University along with Professor Malcolm Prowle and Glynn Lowth, from Nottingham Business School, part of Nottingham Trent University urges accountants to improve their image by refuting bean counter accusations and promoting themselves in business partnering roles.

“Given the importance of financial issues and the increasing need for enterprises to operate economically, efficiently, effectively, efficaciously and ethically, management accounting has potentially a crucial role to play in improving the quality of planning, control and decision-making,” says the CIMA report called Management Accounting Practices of UK SME’s.

The authors also call for further research into the way small and medium-sized enterprises (SMEs) reach critical decisions and into the psychological profile of executives, particularly owner managers.

Dr Lucas said: “While most business owners are good at using accounting services for monitoring cash flow and costs they do not always appreciate that management accountants can add a great deal to decision making in the management of the business. Accountants were sometimes regarded as little more than bean counters, rather than potentially having a business partnering role where they can advise and improve efficiency

“Some entrepreneurs, in particular, are reluctant to employ management accountants, expressing a desire to maintain control and have exclusive access to information they consider sensitive.This could lead to higher costs in terms of management time which is turn can put constraints in time spend in growing the business.”

The report says its exploratory findings give important insights which should inform the development of further large-scale survey research into whether accounting tools were used and, if not, why not.

These tools include: Product costing; budgets for planning and control; standard costing variance analysis; cost-volume-profit analysis; responsibility centres; capital expenditure appraisal techniques; working capital measures; and strategic management accounting.

Dr Lucas is Senior Lecturer in Accounting at the Open University Business School, Professor Prowle is professor of business performance at Nottingham Business School and Mr Lowth, who is a former President of CIMA, is a visiting fellow at the Nottingham business school.

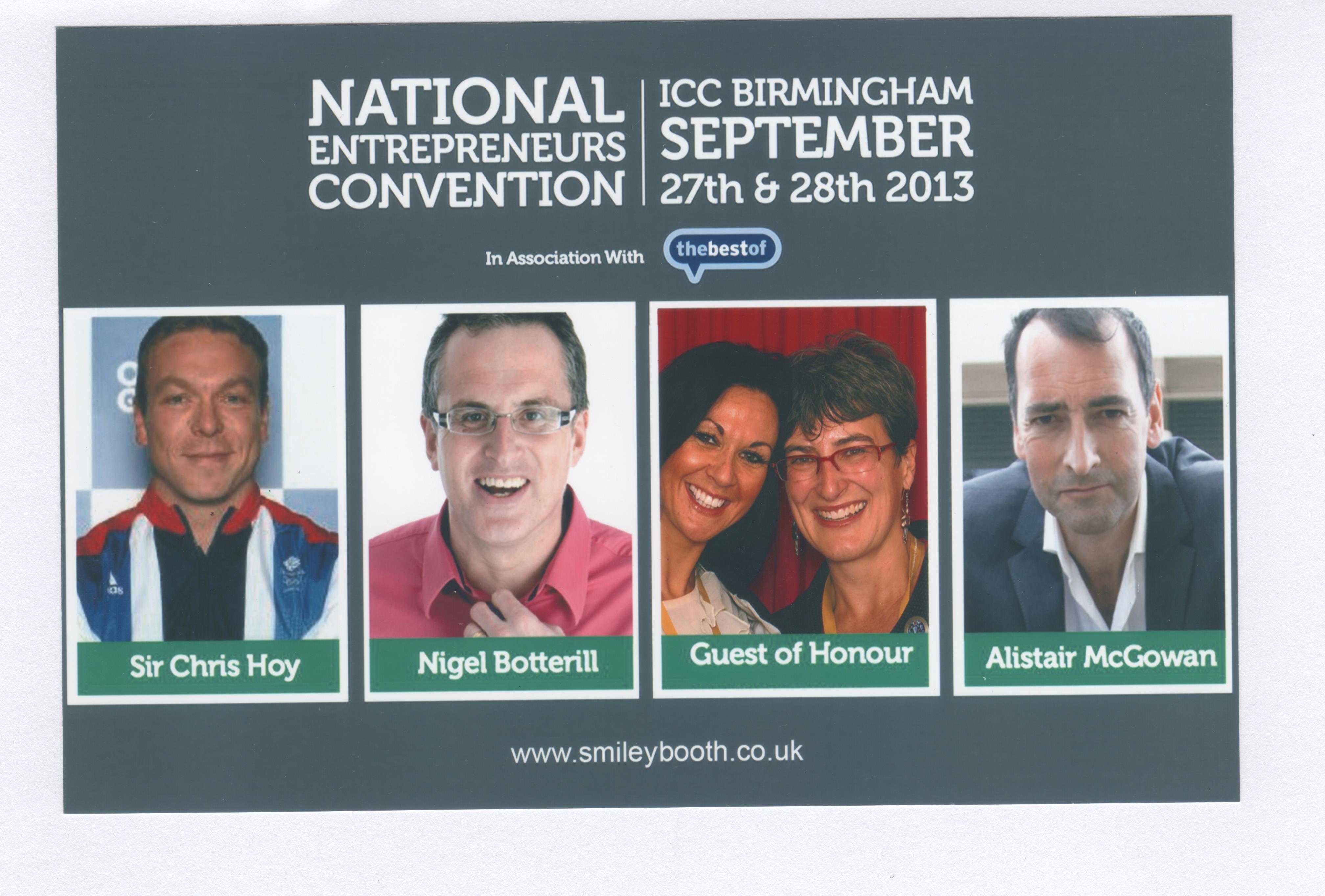

It ain’t what you do, it’s the way that you do it!

We are guests of honour!

These are the immortal words of Bananarama (or Nigel Botterill this weekend).

27th-28th September saw the first annual Entrepreneurs’ Convention at Birmingham’s International Convention Centre. Conference organiser Nigel Botterill is by any definition a very successful entrepreneur himself and the aim of the convention was to impart some of the knowledge and tools which have helped him build 8 £1m businesses in 7 years.

I went with Helen Lacey of Redberry Recruitment and we came back incredibly motivated with a box of tools we can implement in our businesses straight away. My new newsletter – Bright Business Bulletin – is a direct result of this new found zeal.

Nigel himself is a little like marmite (I am sure he won’t mind me saying that his approach is either inspiring or irritating), but it is hard to deny the relevance and effectiveness of his message to business owners who truly want to build the best businesses they can.

In Nigel’s words ‘Entrepreneurship is living a few years of your life like most people won’t…so you can spend the rest of your life like most people can’t.’

Whether we think of ourselves as ‘entrepreneurs’ or not, if we employ people or if we want our business to have a value, even when we are not working in it ourselves, we do need to think entrepreneurially.

I was also pleasantly surprised to see so many familiar faces. In a hall of over 1300 entrepreneurs from all over the country, there were 11 people I already knew. So Kim, Antony, Jonathan, Helen, Carly, Sanjeev, Fiona, Liz, Mary, Mark, John and Cynthia I hope you are all working on the nuggets you took away.

A key nugget for me was that speed is the key to growing a business. Money loves speed, speed attracts talent, talent drives innovation and innovation drives value. As the key is to minimise the gap between the idea and the action, I need to be quicker to get started on, and implement, the ideas I have for my business.

The highlight of the convention was Sir Chris Hoy. He gave an excellent talk about what it took for him to win 6 gold medals over 3 Olympic Games (not to mention world championships and Commonwealth gold medals). The type of dedication he needed, and the physical training he had to put his body through, to get to his end goals was truly inspiring.

We will certainly be going to next year’s convention and I recommend it to any business owner who is serious about growing their business. The dates for your diary are 21st-22nd October 2014.

fiona 🙂

The Cash Cycle – What is it? what is your Cycle? How can you improve it?

As the saying goes, Sales are Vanity, Profit is Sanity and Cash is King. The Cash Cycle also known as the Working Capital Cycle helps you to quickly understand how much cash you need to run your business.

Here is a great example from Steve Grice for an average business

| Average time to collect payment from customers | 60 days | Add |

| Average days sales held in stock | 25 days | Add |

| Average days taken to pay suppliers | 35 days | Subtract |

| Cash cycle | 50 days |

http://stevegrice.wordpress.com/2012/02/06/working-capital-cycle/

Here is a brilliant Cash Flow Improvement Tool from NAB http://oms.nab.com.au/media/10/power_of_one/CF.html

This model quickly and easily calculates your cash cycle but also shows the effect of making improvements.

Having discovered what the cashflow cycle is, what can you do to improve it? well that depends, assuming you have agreed the best possible terms with your suppliers, you need to find ways to speed up cash received from Customers, if your business Sells to other businesses the first thing to look at is Credit Management.

CIMA have produce a comprehensive guide http://www.cimaglobal.com/Documents/ImportedDocuments/cid_improving_cashflow_using_credit_mgm_Apr09.pdf.pdf

But Credit Management may not be enough on its own, perhaps Invoice Finance might help?

Invoice discounting is an excellent, cost-effective way for certain businesses to improve their cashflow position.

- Invoice discounting is most suitable for businesses with good financial controls in place and a strong financial background.

- Invoice Discounting is ideal if you have an annual turnover above £500,000

- Invoice discounting is suitable for business with an established credit control department.

- Invoice Discounting is suitable for a wide range of businesses including manufacturers, wholesalers, transport firms, employment agencies and providers of some business services.

- Suitable businesses for invoice discounting are growing businesses because the level of funding grows in line with increasing sales.

If your business sells to end customers you might consider Card Processing Advances.

You must be masterful. Managing cash flow is a skill and only a firm grip on the cash conversion process will yield

results.

steve@bicknells.net

Associates don’t have to be taxing

The small companies rate of Corporation Tax is 20% compared to main rate of 23% (2013/14). The small company rate is applied if your profits are below £300k, however, if you have associate companies, the £300k is spread between them equally.

For the purposes of CTA10/S25 (4), formerly ICTA88/S13 (4), a company is an associated company of another at a given time if at that time:

- one of the companies has control of the other, or

- both of the companies are under the control of the same person or persons

http://www.hmrc.gov.uk/manuals/ctmanual/CTM03710.htm

But what some businesses forget is that if you have a subsidiary that has become dormant it stops being associated

an associated company which has not carried on any trade or business at any time during the accounting period is disregarded – if it is an associated company for part only of the accounting period, the rule applies to any time during that part.

http://www.hmrc.gov.uk/manuals/ctmanual/ctm03580.htm

steve@bicknells.net

Related Parties and Conflicts of Interest – Directors Responsibilities

The disclosure requirements for Related Party Transactions in published accounts are a common cause of confusion, on the face of it, its sounds easy but getting it right is often a balance between compliance and relevance. The rules are set out in the Companies Act 2006, FRS8 and for smaller companies FRSSE (April 2008). The rules apply to both Full and Abbreviated Accounts.

- FRS 8 defines a related party to include an entity’s subsidiaries, associates, joint venture interests, directors and close family members of directors.

- The standard requires an entity’s transactions with related parties, regardless of whether a price is charged, to be disclosed in that entity’s financial statements.

FRS 8 section 3 and FRSSE section 15.7 states that disclosure of the following is not required:

- Pension contributions paid to a pension fund

- Emoluments in respect of services as an employee or the reporting entity

- Transactions with parties simply because of their role as:

- Providers of Finance

- Utility Companies

- Government Departments

- Customer, Supplier, Franchiser, Distributor or Agent

The disclosure under FRS8 and FRSSE should include:

(a) the names of the transacting related parties

(b) a description of the relationship between the parties

(c) a description of the transactions

(d) the amounts involved

(e) any other elements of the transactions necessary for an understanding of the financial statements

(f) the amounts due to or from related parties at the balance sheet date and provisions for doubtful debts due from such parties at that date

(g) amounts written off in the period in respect of debts due to or from related parties.

Dividends to directors do meet the definition of related party transactions and are disclosable as such.

Trival items don’t require disclosure and the principle of materiality should be applied.

An item of information is material to the financial statements if its misstatement or omission might reasonably be expected to

influence the economic decisions of users of those financial statements, including their assessments of management’s stewardship.

The Companies Act 2006 places a statutory duty on directors in relation to potential conflicts of interest:

A director must “avoid a situation in which he has, or can have, a direct or indirect interest that conflicts, or possibly may conflict, with the interests of the company”.

Related Party Transactions will often create a potential conflict of interest.

Authorisation may be given by the directors—

(a)where the company is a private company and nothing in the company’s constitution invalidates such authorisation, by the matter being proposed to and authorised by the directors; or

(b)where the company is a public company and its constitution includes provision enabling the directors to authorise the matter, by the matter being proposed to and authorised by them in accordance with the constitution.

The authorisation is effective only if—

(a)any requirement as to the quorum at the meeting at which the matter is considered is met without counting the director in question or any other interested director, and

(b)the matter was agreed to without their voting or would have been agreed to if their votes had not been counted.

So it is vital that Directors disclose any potential conflict of interest and seek authorisation from the Board of Directors.

steve@bicknells.net

Salary Sacrifice was “clarified” in April, does your scheme comply?

Salary Sacrifice is a very tax efficient way to give your employees benefits and the most popular benefits are Pensions and Childcare. I wrote a blog back in 2011 which explained how it can save 45.8% in tax and NI

HMRC decided on 9th April 2013 that it was time to “clarify” in their Manuals what are successful and unsuccessful salary sacrifice schemes and have added some further guidance. Their Staff are instructed not to approve schemes (Employment Income Manual EIM42772)….

You (HMRC) may get requests for advice:

- on how to set up a salary sacrifice arrangement, or

- on whether draft documentation will achieve a successful salary sacrifice.

You (HMRC) should not comment on either of these areas. Salary sacrifice is a matter of employment law, not tax law. The nature of an employee’s contract of employment is a matter for the employer and employee.

The specific updates are:

EIM42750 – Salary Sacrifice – updated – this contains the examples of schemes

EIM42777 – Contractual arrangements – this has interesting comments on childcare and pensions

- If the scheme involves childcare or childcare vouchers then the conditions for exemption must be met. (See EIM21905 and EIM16057). Is the agreement to provide childcare between the employee and the childminder or nursery. If so the employer by paying the cost directly is meeting the employee’s personal liability. (See EIM00580).

- For a registered pension scheme the amount which can be contributed to the scheme is normally linked to the employee’s chargeable earnings. In consequence if the salary sacrifice results in some of the employee’s income no longer being taxable, then the amount of contribution, which can be made to the scheme, will also drop.

EIM42778 – Exemption from Tax/NIC – basically stating that exemption may require that the sacrifice may be available to all employees but that the sacrifice must not reduce the employees wages below National Minimum Wages

The following is an example of an unsuccessful Childcare Salary Sacrifice:

The pay slip for the month ended 31 July 2006 gives monthly pay as £2000 plus overtime of £100, deductions for tax of £355 and NIC. The pay slip for the following month shows monthly pay of £2000 plus overtime of £100, deductions for NIC, childcare vouchers of £200 and tax of £310. The code number operated on the salary has not changed.

The situation is not clear from the payslip. When asked, the employer explains that for August, because childcare vouchers of £55 a week are exempt, £220 of vouchers has been deducted from the gross pay of £2100 and tax charged on the net figure of £1880. Further information is needed, for example a copy of the employment contract and any variations agreed by the employer and employee to that contract.

It is established that in July the employee bought childcare vouchers. The employer was not involved. The employer accepts that as the childcare in July was not provided by him, no tax exemption is available. In August the employee asked the employer to buy the childcare vouchers to take advantage of the exemption. The employer did this and deducted the cost from the monthly salary. The contract of employment shows that the employee is entitled to a base salary of £24000 to be paid monthly. This contract has not been varied. As the employee’s entitlement has remained the same, this is not a successful sacrifice. (See EIM42766).

If you operate salary sacrifice schemes its worth checking that your schemes comply, the tax consequences of failure to comply could be substantial.

steve@bicknells.net

How does Overlap Relief work?

Overlap Relief applies to Sole Traders and Partnerships.

Where 5 April is used as the annual accounting date throughout the entire life of a business, there will be no overlaps between basis periods. In such cases the total profits assessed to income tax will automatically equal the total profits made during the life of the business.

In any other case there will be one or more years in which the basis periods for two successive tax years overlap. These overlaps may occur:

- In years 2 or 3 during the period in which the basis periods and accounting periods are brought into alignment; or

- During the period of realignment following a change of accounting date.

To ensure that the total profits assessed to income tax exactly equal the total profits made during the life of the business, “overlap relief” is given.

The amount available to be given as overlap relief is the amount of profits which arise in any overlap periods. An overlap period is a period which falls within two basis periods. Guidance on computing overlap relief is at BIM71080.

Overlap relief is given as a deduction in calculating the profits of the trade for the tax year:

- in which the trade ceases (see BIM71095), and / or

- an earlier tax year in which a change of accounting date occurs if the basis period for that tax year is longer than 12 months (see BIM71090).

Here is an example:

A business commences on 1 October 2010. The first accounts are made up for the 12 months to 30 September 2011 and show a profit of £45,000.

The basis periods for the first 3 tax years are:

| 2010-2011 | Year 1 | 1 October 2010 to 5 April 2011 |

| 2011-2012 | Year 2 | 12 months to 30 September 2011 |

| 2012-2013 | Year 3 | 12 months to 30 September 2012 |

The period from 1 October 2010 to 5 April 2011 (187 days) is an “overlap period”.

steve@bicknells.net

Head in the cloud …… feet very much on the ground!

I’m a director of a software development business which develops ‘cloud’ based applications. Of course, when we started in 2005, I was quite unaware of this, but then the marketing men seized on the ‘latest idea’, gave it a label so that they could sell it more easily, and hey-presto, ‘the cloud’ was born.

So if we set aside all the marketing hype, what exactly is ‘cloud computing’?

I’m not an ‘IT Professional’ so forgive me if I reduce this to more simplistic terms but actually it is quite straightforward, and in many ways something of a natural progression in a trend that has gained momentum over the last few decades.

If I can go back further for a moment, I can recall managing the new IT department of a large manufacturing operation in the early 1980’s (the directors didn’t really know where it should sit within the organisation so they gave it to the accountant because it had something to do with ‘information’). In those days, data was input by cards or paper tape, and we had a department of ‘punch card operators’, and an air conditioned room in which sat a ‘mainframe computer’ which was the size of a small car, and had various attendant tape drives for storage of data and programmes.

Users had a screen and keyboard and a wired connection to the mainframe to and from which they could send and retrieve data using application programmes which controlled how that data should be input and processed or presented when retrieved. All the processing was done by the mainframe as it was the only computer in this network of users and machines.

The advantages were clear and immediate: instead of having to walk to the other end of the factory to speak with a colleague who kept a written record of the information we were looking for, a user could now sit at his or her desk and look at the data which that colleague had input only moments earlier.

We then saw the explosion in availability of the personal computer (PC), cheaper and more flexible yes, but a backward step in productivity since written records were replaced by computerised records, but now held on desktop machines. And so we were back to walking the corridors to speak with a colleague who kept a computerised record of the information we were looking for, but this time carrying a floppy disk to write that information on rather than a pad and pencil.

Hence the advent in networking these PCs to a central ‘file server’ which, as the name suggests, is designed to store our files. Again this enabled us to work more collaboratively and more productively, by working on the same files and data, and indeed more securely as protection and regular backups of centralised data is far easier to achieve than for a myriad different personal computers.

The only real difference between this model and the early mainframes is that whereas the mainframe computer did all the work – stored the data, retrieved the data, ran the software applications, and so on – now the work was shared between the server which largely stored and retrieved data only, and the PCs which ran the applications to process that data, so overall processing speeds reduced dramatically whilst achieving a significant cost saving over a mainframe investment – a real ‘win-win’.

The development of ‘data warehouses’ where the centralised data storage was taken away from ‘in-house’ networks, and to more secure remote locations with ‘thin client’ access to data and business applications, was essentially a return to the mainframe model, and with much more powerful modern servers, overall processing speeds reduced still further.

However the real driver for this change was again an economic one – why spend money on lots of expensive PCs and a server, and all the attendant network paraphernalia and maintenance, when one very powerful central server could do it all, and all the users would need would be a screen, a keyboard, a mouse, and a telephone line (hence the thin client)!

I would have to say that this latter development probably by-passed most small and medium sized enterprises (SMEs) and still remains the reserve of larger firms who can afford the fees charged by vendors of large ‘enterprise’ (organisation wide) applications.

However, cloud computing is really little different to the thin client arrangement in that it enables access to data stored on a remote centralised server, and the applications to process that data. Our own cloud based applications store data on servers in the North of England, with backups in Docklands, and whilst most of the processing takes place on the server, some is done on the user’s PC, so that we can harness as much processing power as we need to ensure fast response times.

At its best, the cloud can provide access to software applications and services previously available only to larger enterprises, to smaller firms, and at a very economic cost, often on a ‘pay-as-you-go’ or rental basis instead of outright purchase – this is often termed ‘Software as a Service’ (SaaS).

And so to the inevitable questions: is cloud computing safe, and is it reliable enough to use to run my business?

Most small and medium sized enterprises do not have a dedicated IT team at their disposal, and as a result, backups may not be made reliably, firewalls and anti-virus software may not be the best (or as I have seen, not exist at all), and network access may require nothing more than a password written down on countless sticky notes attached to keyboards and monitors around the office.

The level of security employed in a cloud environment is likely to be significantly higher on average then the security of a typical SME, but it really is for prospective users to verify this for themselves: where is the server physically? What do you know about the firm that runs and maintains the server?

And is the application you plan to run secure? I would not claim that any application or network is one hundred percent secure (there have been too many high profile news stories to the contrary) but for example our accounting/ ERP application includes encryption between user and server so that even if the data transmission is intercepted by a hacker, they will have nothing more than a string of gobbledygook – a whole lot better than someone being able to hack into your in-house network and steal files, or even physically break into your office and steal a laptop with confidential data on it, or indeed losing your in-house data in a fire, all of which have happened to clients in the past.

That said, there are draw-backs, and in particular, reliability: do you have a reliable connection to the Internet, and does the cloud service provider give any guarantee of service availability?

I have sometimes advised prospective customers to look at ‘in-house’ software applications rather than our cloud based ERP application where they have poor or unreliable broadband, though this is becoming less of an issue as the infrastructure improves, indeed we even see our clients taking and processing customer orders directly into their system at trade shows using just a tablet computer.

And our experience with the firm who warehouses our servers has been good to date in that in five years we, and therefore our clients, have experienced only twenty minutes loss of service on a Saturday just before Christmas 2010 due to an attack by hackers on one of the other servers located in the same facility (this was dealt with effectively by the server centre staff without any need for our becoming involved), and this compares favourably to all the hours work lost previously when our in-house network has failed because one-or-other component or machine had stopped working (often following a software ‘upgrade’).

So is cloud computing for you?

A first step might be offsite backup and storage of your valuable data either by way of a simple copy and paste routine using Dropbox or Google Drive, or one of many providers that enable you to schedule regular data backups without any intervention from the system user.

You might also consider having your e-mail accounts hosted by an external provider, perhaps the same one that hosts your web site?

And what about your accounts/ ERP, or other business critical applications?

In June 2013 Larry Ellison of Oracle essentially endorsed cloud for such business applications; the article states “Oracle’s Larry Ellison is the epitome of the old guard. He built an empire on traditional enterprise software, purchased by a central IT department that worked through expensive and lengthy implementations to ultimately foist it on workers. But now he admits times have changed. ‘When you move to the cloud, companies don’t expect a multi hundred million dollar project to make their CRM from Salesforce work with ERP from Oracle.’”

Ultimately only you can decide – for me, as an accountant, this is just a normal investment proposition – what are the pros and cons for my particular organisation and what are the relative costs? Having actioned all the above in our accounting practice several years ago we immediately saved c.£3.5k when it came to replace out onsite server, quite apart from time and money on maintenance, servicing, and updates.

Will your experience be as good as ours to date?

I really can’t say. All I would suggest is that you check out the supplier of cloud services in the same way as you would anyone that is offering you any other service: Who are they? Do they have a good reputation, have they been recommended?

All I can hope is that this article has helped you to better understand what the cloud is about, and to therefore make a more informed decision.

Paul Driscoll is a Chartered Management Accountant, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and AJ Tensile Fabrications Limited, and is a board level adviser to a variety of other businesses.

The tax advantages of Troncmasters

If your employees receive tips directly from your customers and are allowed to keep them, then you do not need to do anything for PAYE tax or NICs. There are no NICs due on the money, and the tax due is the employee’s responsibility. Your employees should declare the money to HMRC, who will usually adjust their tax code to collect any tax due.

A tronc is an arrangement for pooling and distributing tips and service charges and the person who operates the tronc is known as a troncmaster. If your employees use a tronc you must tell HMRC who the troncmaster is so that they can set up a PAYE scheme for the tronc.

http://www.hmrc.gov.uk/helpsheets/e24.pdf

Tips are outside the scope of VAT when genuinely freely given. This is so regardless of whether:

• the customer requires the amount to be included on the bill

• payment is made by cheque or credit/debit card

• or not the amount is passed to employees.

Restaurant service charges are part of the consideration for the underlying supply of the meals if customers are required to pay them and are therefore standard rated.

If customers have a genuine option as to whether to pay the service charges, it is accepted that they are not consideration (even if the amounts appear on the invoice) and therefore fall outside the scope of VAT.

Further information is available from: Notices 700 The VAT guide and 709/1 Catering and takeaway food

steve@bicknells.net

Odd VAT rules for Hotels

Tax is made up of bizarre and complicated rules and for accountants that’s a good thing, keeps us in work, but why tax can’t be simplified is beyond me, its a crazy tax world out there.

Here are some VAT examples for Hotels – HMRC Reference:Notice 709/3 (October 2011) :

The Long Stay Rule

If a guest stays in your establishment for a continuous period of more than 28 days, then from the 29th day of the stay you should charge VAT only on that part of the payment that is not for accommodation.

A guest’s stay must be continuous to qualify for the reduced value rule. For example, if a guest stays for three weeks every month, you must always charge them VAT in full. If another guest stays for five weeks, leaves for a week, and returns to stay for five more weeks, the reduced value rule applies only to the fifth week of each separate stay.

However, a guest’s departure is not seen to end their stay provided the guest:

- is a long-term resident and leaves for an occasional weekend or holiday,

- is a student who leaves during the vacation but returns to the same accommodation for the following term, or

- pays a retaining fee

In these cases the time away is ignored and you only have to charge VAT in full for the first 28 days of the overall stay.

It does not matter whether the guest returns to the same room or not.

VAT Exempt Meeting Rooms and Refreshments

Hiring a room for a meeting, or letting of shops and display cases are generally exempt, but you may choose to standard-rate them by opting to tax, see Notice 742A Opting to tax land and buildings.

If you make an exempt supply such as providing a room for a meeting or a conference and you provide minimal refreshments such as tea, coffee and biscuits, the room and the incidental catering will be treated as a single exempt supply. But, if you serve substantial refreshments such as a meal or buffet, the catering should be treated as a separate supply and you must account for VAT based on the normal charges you would make for such catering.

VAT on Deposits

Most deposits serve as advanced payments, and you must account for VAT in the return period in which you receive the payment. If you have to refund a deposit, you can reclaim any VAT you have accounted for in your next return.

Normally, if you make a cancellation charge to a guest who cancels a booking, VAT is not due, because it is compensation. This includes amounts debited from credit cards using details provided at the time of the booking. Where the cancellation charge takes the form of a retained deposit, you can reclaim any VAT already accounted for as an adjustment to your next return.

Reclaim Overpaid VAT

If you have overpaid VAT you can now go back up to 4 years and reclaim it.

steve@bicknells.net