Home » Employees (Page 4)

Category Archives: Employees

Are you ready for the OTS to check your employment status?

Contractor Weekly reported on th 29th July 2014…

As part of the ongoing mission to create a simpler and fairer tax system the Office of Tax Simplification (OTS) has been tasked with carrying out reviews of employment status and also tax penalties, with a view to producing a report in time for next year’s Budget.

According to the OTS, the boundary between employment and self-employment no longer reflects modern working patterns, particularly in recent years. Many people have multiple jobs and can be classed as employed in one whilst self-employed in another. The rise of the freelancing business model has also caused some to suggest this is a ‘third way’ between employment and self-employment.

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

It will be interesting to see the report that the Office of Tax Simplification (OTS) produce, especially if they find a ‘third way’

steve@bicknells.net

How do you prove ‘No Private Use’ of a company car?

I spotted this case on the HMRC website the other day…

Elm Milk Ltd 2006 STC 792

A business bought a car for its managing director. It recorded a resolution that the car was for business use only. The managing director had another car that was used for private journeys.

The Court held that there was no reason why a car could not be made unavailable for private use by suitable contractual restraints, and that a company could enter into a binding employment contract with its sole director. Therefore, on the facts of the case, the car was available for business use only and input tax could be reclaimed.

The court held that HMRC had given too much weight to the physical constraints and insurance and should have focused on contractual constraints, the employment contract and board minutes.

The following case is also very interesting…

The ‘Shaw’ case

In the Shaw case the taxpayer bought two BMW X5 vehicles together, one for use in his farm business, the other for use privately. Mr Shaw also owned two other cars privately as well. HMRC [again] argued the case based on the social and domestic cover on the insurance policy, but Mr Shaw rebutted this by showing how the insurance policy for his combine harvester had ‘social, domestic and pleasure’ cover too! He added that the premiums for both the X5s and the harvester were lower as a result.

If there is No Private Use then there is no benefit in kind and no fuel scale charges.

So what should you do to prove there is no private use:

- Keep the car on the company’s business premises

- Keep the keys at the company’s business premises

- Prepare a Board Minute

- Makesure your contract of employment bans private use

- Keep a mileage log

- Insure the car principally for business use

Unlike Pool Cars you don’t have to prove it was available to other employees

steve@bicknells.net

Doctor, Doctor, I think you should be an Employee

A report in the Telegraph on the 14th July 2014…

Dozens of NHS executives face possible investigation by HM Revenue and Customs after they refused to answer questions about their tax arrangements, it can be revealed.

An investigation has identified 86 senior health service officials paid off-payroll who have refused to give assurances to their employers that they are paying the correct level of income tax and national insurance.

They are paid through service companies – arrangements that allow public sector employees to be paid as contractors through private companies, potentially cutting their tax bills.

Monitor found 30 foundation trusts had issues to resolve in their report of the 10th July 2014:

- 20 foundation trusts have 1 or more senior employees paid through an off-payroll arrangement, and they are waiting for responses after asking those employees for assurance about their tax arrangements

- 23 foundation trusts (including some of the 20 above) still have at least 1 board member or senior member of staff with significant financial responsibility employed through an off-payroll arrangement

- of these 23 trusts, 9 are facing wider issues relating to their performance which they have explained is affecting their ability to recruit and retain permanent skilled staff; this resulted in the need to use interim off-payroll contracts to attract high-performing staff to help improve the foundation trust’s situation

- as a result of their performance issues, these 9 trusts are facing current enforcement action by Monitor, which is unrelated to their use of off-payroll employment

- out of those 23 trusts, the other 14 which are not facing enforcement action have plans to end off-payroll arrangements by the end of the year

Will this end the use of PSC’s in the NHS?

steve@bicknells.net

You could employ your spouse to help you do your job

Many micro business owners employ their spouse and as long as they perform a role in the business that’s fine and it can be very tax efficient.

But there are circumstances in larger businesses with several owners/directors where it isn’t practical to directly employ your spouse.

However, it could be possible to claim an expense for using your spouse as an assistant, take a look at EIM32415

A deduction can be given in the following circumstances:

- where the employee is paid solely by results so that, in taking on assistance, the employee can maximise his or her earnings from the employment.

- where it is actually part of the duties of the employment to engage and remunerate assistants to do some of the work.

So it may be possible to amend your employment contract to identify parts of your job that could be done by someone else and you could add a clause which says that you must ensure the work specified is done and that its your duty to employ an assistant to do it.

The duties could be anything – Admin, Secretarial, Market Research, Telesales…..

Depending on how much you pay your assistant you may need to account for PAYE and NI.

steve@bicknells.net

15 Benefits that won’t be on your P11D

It’s P11D time, but have you considered giving your employees benefits in kind that are tax free, here are some to choose from:

- Pensions – Up to £40k can be paid in to you pension schemem by your employer (2014/15) and you can use carry forward to pay in even more

- Childcare – Up to £55 per week but check the rules to makesure your childcare complies (HMRC Leaflet IR115)

- Mobile Phone – One per employee

- Lunch – Tax Free Lunch Blog

- Cycle Schemes – Cycle to Work Blog

- Fitness – Fitness Blog

- Parties and Gifts – Christmas Blog

- Parking – Parking Blog

- Business Mileage Allowance – 45p for the first 10,000 miles then 25p

- Long Service Award – A bit restrictive as you need 20 years service, the tax free amount is £50 x the number of years

- Eye Tests and Spectacles – The Eye Test must be needed under the Health & Safety at Work Act

- Suggestion Schemes – Suggestion Scheme Blog

- Insurance such and Death in Service and Income Protection – Medical Insurance Blog

- Travel Expenses – Travel Blog

- Working From Home – Working from Home Blog

steve@bicknells.net

My staff want to Opt Out of Auto Enrolment…

Not every employee will want to be in Auto Enrolment, for example they may have their own pension arrangements.

But be very careful that you don’t induce or encourage them to opt out.

Most employees will want to be IN

Once staff have been enrolled into the pension scheme, they have one calendar month during which they can opt out and get a full refund of any contributions. This is known as the ‘opt-out period’. It starts from the whichever date is the later of:

- the date active membership was achieved, or

- the date they received your letter with the enrolment information.

Staff can’t opt out before the opt-out period starts or after it ends. If they decide to leave the scheme outside this period, they will instead be ‘ceasing active membership’. Whether they get a refund of contributions will depend on the pension scheme rules.

Staff opt out by giving you an ‘opt-out notice’. The opt-out notice is provided by the pension scheme. This is to avoid any employer involvement in the decision to opt out, which could lead to a breach of the law.

If an employer does anything to encourage or induce an employee or potential employee (at interview) to opt out they will be subject to harsh penalties.

If an employee does Opt Out they will be re-enrolled every 3 years.

steve@bicknells.net

Can I have a Tax Free Lunch?

Let’s look at the options….

Exemption for Canteen Meals

Employees can be provided with free or subsidised meals provided generally to employees served on the business premises where the following 3 conditions are met:

- The meals are provided on a reasonable scale

- That all employees or all those at a specific location may obtain free or subsidised meals

- If the meals are provided in a restaurant or hotel at a time when meals are being served to guests/clients part of the dining area is designated for employees

Not everyone needs to use the facility they just need the option to use it and its is possible for senior management to have superior meals.

This exemption is not available where only select employees are able to get a free lunch.

HMRC are happy to accept Tea and Coffee as trivial benefits that can be ignored.

Benchmark Subsistance

Since April 2009 employers have been able to pay their employees HMRC approved flat rate allowances referred to as Benchmark Subsistance, the rates are:

- £5 if you buy a breakfast and start your business journey before 6am

- £5 if you’re out of the office on business for more than 5 hours, and buy one meal

- £10 if you’re out of the office on business for more than 10 hours, and buy 2 meals

- £15 if your business trip keeps you beyond 8pm, and you buy an evening meal

So £15 is the maximum

You can only claim if:

- travel is required as part of your dutues or you are working at a temporary work place

- you are away from your work place or home for more than 5 hours

- you are expected to pay for food and drink after starting your journey

Meal Vouchers

Vouchers can be issued tax free but only up to the value of 15p per working day and the voucher must be non-transferable and used for meal only.

Travel Expenses

I have separate blog on this topic http://stevejbicknell.com/2013/02/13/what-travel-expenses-will-the-taxman-allow/

steve@bicknells.net

How does Auto Enrolment Postponement work?

You can choose to postpone automatic enrolment for up to three months for some or all of your staff. You must write to your staff to tell them you’re postponing automatic enrolment for them. One of the times you can postpone is from your staging date.

Key points

- You can postpone automatic enrolment for up to three months from certain dates.

- If you postpone from your staging date, your staging date does not change.

- If you choose to postpone from your staging date, you must write to tell the staff who will be postponed within six weeks of your staging date.

Why Postpone?

- Its unlikely that your payroll processing period will match your staging date, most staging dates are the 1st of the month but many payrolls are weekly, it makes sense to start auto enrolment on a pay processing date

- If you have short term staff or you are a temp agency you will probably postpone in order to avoid unnecessarily assessing staff who will leave within the postponement period

- You may also postpone to reduce auto enrolment pension payments and admin

- You can choose any business reason

When can you postpone?

You can only postpone automatic enrolment from:

- your staging date

- a staff member’s first day of employment

- the date a staff member first becomes eligible for automatic enrolment.

If you postpone from your staging date, it doesn’t change your staging date.

Staff whose automatic enrolment you’ve postponed can choose to opt in to your pension scheme during the postponement period.

The Pension Regulator has further details

Don’t mess this up, if you don’t get postponement right…..

- You will get a Warning

- Followed by a penalty of £400

- Followed by fines of £500 to £2,500 per day (depending on the number of employees)

Even the smallest business will get fines of £50 per day!

steve@bicknells.net

You will initially be given a warning, which will be followed by a fixed penalty of £400. Not too severe so far, but then the penalties shoot up for those companies who still fail to comply.

If you employ between 50 and 249 employees the fine for on-going non-compliance is a whopping £2,500 per day. For businesses with fewer employees, between five and 49 the penalty is still £500 per day and even the smallest of businesses will be fined £50 per day.

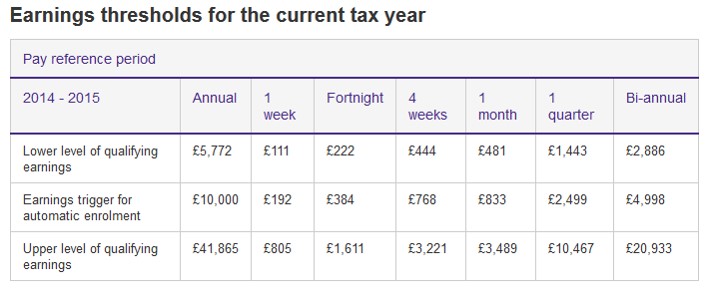

What are Qualifying Earnings for Auto Enrolment?

These are defined as sums which you pay to an employee in connection with his or her employment. They can be salary, wages, commission, bonuses, overtime. Statutory sick pay and maternity/paternity/adoption pay are included too. Benefits in kind (known as P11D benefits), for example, car and fuel, and tips and gratuities do not have to be included. In 2014/2015 Qualifying Earnings are earnings between £5772 and £41,865.

Employers are only required enrol employees earning over the Earnings Trigger of £10,000 (subject to age criteria) but employees can opt in once they earn above the lower level. According to Payroll and Benefits Magazine...

The AE process can be very administration-heavy and, unlike Real Time Information, employees and workers will have to be continually assessed. For example, employers will need to continuously monitor their workforce to identify when a jobholder must be automatically enrolled. In particular, the employer will need to monitor a worker’s age because this may trigger AE and opt-in activity.Although small employers will need at least six months before their staging date to prepare for AE, larger ones may need between 12 and 18 months.AE does not only apply to employees, but also to workers, including contractors who provide services on a personal basis but not as a company.

Can you cope with Auto Enrolment?

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was.

58% had not set up an auto-enrolment pension scheme.

90.5% of employers without an auto-enrolment pension scheme hadn’t even started researching one.

If you think you can ignore Auto Enrolment, think again, The Pensions Regulator will make you comply……..

Non-statutory action

We can issue guidance and instruction by telephone, email, letter and in person. Or we can send a warning letter confirming a set time frame for compliance with the duties.

Statutory notices

Statutory notices can direct you to comply with your duties and / or pay any contributions you have missed or are late in paying. We have further discretionary powers which allow us to estimate and charge interest on unpaid contributions and direct you to calculate and / or pay unpaid contributions.

Penalty notices

We can issue penalty notices to punish persistent and deliberate non-compliance.

A fixed penalty notice will be issued if you don’t comply with statutory notices, or if there’s sufficient evidence of a breach of the law. This is fixed at £400 and payable within a specific period.

We can also issue an escalating penalty notice for failure to comply with a statutory notice. This penalty has a prescribed daily rate of £50 to £10,000 depending on the number of staff you have.

We can issue a civil penalty for cases where you fail to pay contributions due. This is a financial penalty of up to £5,000 for individuals and up to £50,000 for organisations.

Where employers fail to comply with a compliance notice or there is evidence of a breach, we can issue a prohibited recruitment conduct penalty notice. This is currently set at a maximum fixed daily rate of £5,000 for organisations with over 250 staff. We aim to fully recover all the penalties that we issue.

Court action

We can take civil action through the court to recover penalties.

Employers who deliberately and wilfully fail to comply with their duties may be prosecuted.

We can also confiscate goods where there is a criminal conviction and restrain assets during criminal investigations.

The first case was Dunelm http://www.thepensionsregulator.gov.uk/docs/section-89-dunelm.pdf

Research shows that Accountants are most likely to be asked to help SME’s and Business Accountant (a service provided by CIMA Members in Practice) have created a booking service to assist SME’s in getting help https://business-accountant.com/auto-enrolment/

So don’t be scared by Auto Enrolment, don’t delay drawing up a project plan, take action now to avoid problems with the Pension Regulator later!

steve@bicknells.net