Home » Accounting Records (Page 2)

Category Archives: Accounting Records

Will Small Businesses be exempted from VAT MOSS?

Before 1st January 2015 all businesses supplying telecommunications, broadcasting and e-services such as downloaded ‘apps’, music, gaming, e-books and similar services to private consumers located in other EU Member States (referred to as ‘B2C’ supplies) were taxed where the business supplier was established, which is simple to understand and implement.

Since 1st January 2015 VAT is now charged in the country where the customer has ‘use and enjoyment’ of the services.

So lets say you are an American (normally zero rated) on holiday in France, even though you pay with an American credit card and buy from a UK supplier because you are reading your ebook in France, French VAT will apply. Sounds like a nightmare, doesn’t it.

To help with this HMRC introduced the VAT MOSS (Mini One Stop Shop).

Overview

If your business supplies digital services to consumers in the EU, you can register with HM Revenue and Customs (HMRC) the VAT Mini One Stop Shop (VAT MOSS) scheme. There are 2 UK VAT MOSS schemes that operate in an almost identical way:

- Union VAT MOSS scheme for businesses established in the EU including the UK

- Non-Union VAT MOSS scheme for businesses based outside the EU (for example, the USA, Canada, China)

By using the VAT MOSS scheme, you won’t have to register for VAT in every EU member state where you make digital service supplies to consumers.

Once you register for a UK VAT MOSS scheme HMRC will set you up automatically for the online VAT MOSS Returns service.

You need to submit a single VAT MOSS Return and payment to HMRC each calendar quarter. HMRC will then forward the relevant parts of your return and payment to the tax authorities in the member state(s) where your consumers are located. This fulfils your VAT obligations.

Unless businesses opt to register for MOSS, businesses that make intra EU B2C supplies of telecommunications, broadcasting and e-services will be required to register and account for VAT in every Member State in which they have customers. MOSS will give these businesses the option of registering in just the UK and accounting for VAT on supplies to their customers in other Member States using a single online MOSS VAT return submitted to HMRC. This will significantly reduce their administrative burdens.

- Examples of telecommunications services include: fixed and mobile telephone services; videophone services; paging services; facsimile, telegraph and telex services; access to the internet and worldwide web.

- Examples of broadcasting services include: radio and television programmes transmitted over a radio or television network, and live broadcasts over the internet.

- Examples of e-services include: video on demand, downloaded applications (or “apps”), music downloads, gaming, e-books, anti-virus software and online auctions.

Fiscalis conference (7th to 9th September 2015)

Representatives from all EU finance ministries were at the Fiscalis conference in Dublin last week to discuss the implementation of the new EU VAT rules, and how they have been working since their introduction in January 2015.

Accounting Web reported …

One of the key takeaways from the consultation was a general agreement that there should be a threshold to exempt smaller businesses from the rules. The commission stated that it intends to propose legislation for a threshold beneath which companies will be VAT exempt, but did not confirm a figure.

There was also a general agreement that above this threshold there should be what many are calling a ‘soft landing’: A simplified version of the rule for businesses that does not create a financial cliff for those who hit the threshold.

Let’s hope that an exemption can be put in place very soon and ideally as proposed in the EU VAT Action Campaign below

EU VAT Action Campaign (started 28th August 2015)

Please circulate this article as widely as possible, as soon as possible, with as many of your business contacts and other networks.

Write to your national tax authority and finance ministry, to your MPs, MEPs, other elected representatives and to any business organisations which you belong to, insisting that the EU act immediately to:

1. Introduce a threshold of €100,000 for cross-border trade (i.e. based on how much you’re selling digitally to the rest of the EU, outside of your home country). As far as your domestic turnover is concerned, your own country’s VAT rules will still apply.

2. Simplify the rules for all micro businesses (i.e. sub-€2m turnover) to allow ONE piece of data as evidence of place of supply, instead of the current 2-3, with that piece of data being the customer location as supplied by the payment processor to businesses using all levels of their services, not just to those purchasing premium options.

3. Immediately suspend these rules for micro businesses, so that they can revert to their domestic VAT rules and pay taxes according to those regulations during the 2 years it could take for the agreed idea of a VATMOSS threshold to become law.

4. Amend the legislation so that all Member States are legally required to direct their VATMOSS communications through the business’s home tax authority for all micro businesses, to remove the threat and fear of receiving demands and ‘system error’ letters from 27 different tax authorities.

One last thing; please take the few extra minutes to contact these people direct rather than using a bulk-emailing service. These websites have become a victim of their own success in flooding inboxes, so letters coming via these routes are increasingly ignored. You can still send the same letter to them all but you will need to copy and paste and send it individually to be most effective.

steve@bicknells.net

What if you write off an inter company or directors loan?

Connected party loans are a problem area especially if the loan is impaired (ie the borrower may not be able to repay the debt)

Individual Loans written-off

If an individual makes a loan to a company and this is subsequently written-off, the company will have a non-trading loan relationship credit equal to the amount written off.

If the loan was made to an unquoted trading company, the individual will crystalise a capital loss equal to the amount of the loan written off. This will be available to set off against capital gains arising in the year of write-off or in subsequent years.ACCA

Loans swapped for Shares

Often Loans are swapped for equity and then subsequently a claim for negligible value is made.

A negligible value claim enables you to set a capital loss against your income (or against other capital gains if you have them) for earlier years and claim a tax refund.

Many negligible value claims are made by shareholder directors whose company has failed. Their claim is to offset the loss on the shares in their company against their directors’ wages for earlier tax years.

When a taxpayer owns shares which become of negligible value the taxpayer may make a claim under s24 TCGA 1992, resulting in a deemed disposal and reacquisition, which crystallises a capital loss.

Intercompany Loans

Accounting standards require companies to assess their assets at the end of each period to ascertain whether there is objective evidence that particular assets are impaired. So if a loan can’t be repaid it would be impaired and may require a provision for bad or doubtful debts at the year-end which may well lead to the eventual release of the loans in question.

The problem is that for connected businesses this can create a double whammy on tax! tax relief is denied in respect of the debit to the creditor company’s profit and loss account. The credit recognised in the debtor company’s accounts can be taxable.

Where the creditor and debtor are connected companies, the connected party rules will apply to the release. This means that the release debit in the creditor’s accounts will not be allowable, because of CTA09/S354. Similarly, the credit in the debtor company’s accounts will not be taxable, since CTA09/S358 applies, unless the release is a ‘deemed release’ as defined in CTA09/S358(3) (CFM35440) or a ‘release of relevant rights’ under CTA09/S358(4) (CFM35510).

Since the release is, for both parties, dealt with under loan relationships, the priority rule in CTA09/S464 means that the creditor’s loss cannot be claimed, nor the debtor’s profit taxed, under the normal provisions for trading income. Nor can the credit in the debtor’s accounts be taxed under CTA09/S94 (debts incurred and later released).

Trade debts or loans between companies within a group may not uncommonly be released when either the debtor or the creditor company (or both) is dormant, as part of a ‘tidying-up’ exercise to enable dormant companies to be struck off. If this is all that happens, HMRC would take the view that the recording of an accounts profit – which is not taxed – in a dormant debtor company does not result in that company starting to carry on a business, and therefore does not start an accounting period under CTA09/S9. HMRC CFM41070

Two companies are connected for an accounting period if one controls the other or both are under the control of the same person (s 466) and companies are connected for the whole of their respective accounting periods if the control test is met at any time during those periods.

One possible solution could be a Deed of Release or Waiver executed in the accounting period in which the loan is released, but this would need to be properly drafted. The credit to the debtor company’s profit and loss account will then be able to be treated as non-taxable and as such avoid the double tax treatment.

steve@bicknells.net

4 Tips for Choosing Cloud Accounting Software

There are lots of brilliant accounting solutions on the market, so how can you decide which one will work best for your business?

Features

The first thing you need to decide is what features you need:

- Projects

- Stock

- Construction Industry

- Payroll

- Invoicing

- Automated payments – PayPal etc

- Bank Feeds

- Quotes

- VAT Schemes

- Document Storage

- Accountant Access

- Access – Apps, Devices, Mac’s

- Contact Management

- Reports

Don’t pay for things you don’t need!

Future Proof

As your business grows, will the software grow with you

- Can you add users

- Can you set access levels

- Are there upgrade products

- Can you add in other products (Apps) such as scanned receipts

Cost

How much does it cost? Normally working with an accountant will reduce the overall cost and provide a package deal

- Monthly Software Subscription

- Accountancy Fees

- Book Keeping Costs

Ask for Help

Just because you have cloud based software it doesn’t mean you won’t need an accountant! you might think you don’t need help but an accountant will help you choose the right VAT Scheme, claim tax reliefs and comply with reporting requirements.

steve@bicknells.net

Are you too busy to do your accounts?

When you start a business its because you have a skill or product that clients want and most small businesses put off the accounting because they find it boring, time consuming and unproductive. This often causes huge problems with tax, cash and business management.

What if it wasn’t boring, what if it was easy and quick to do?

- Apps for invoicing

- Available every where all the time on all your devices

- Automatic bank feeds to reduce data entry

- Dashboards of key data

- Easy access for you and your accountant

That’s why cloud accounting systems are the future. Take a look at this infographic produced by Sage.

Obi Wan Kanobi might not be you’re only hope, cloud accounting could save your business.

steve@bicknells.net

HMRC to get access to your bank account

If you owe more than £1,000 to HMRC the Summer Finance Bill will give HMRC the power to take it from your bank account!

According to an article on accounting web…

HMRC have said they will contact the taxpayer at least four times about the debt before commencing the DRD procedure. One of those occasions will be a face to face meeting with the taxpayer to establish that they have found the right debtor and calculated the debt correctly. This should avoid the situation where the HMRC letters have failed to arrive, or the taxpayer has not understood the liability.

There are penalties for banks who fail to comply with the notices issued by HMRC.

steve@bicknells.net

Preregistration VAT confusion

When you register for VAT, there’s a time limit for backdating claims for VAT paid before registration. From your date of registration the time limit is:

- 4 years for goods you still have, or that were used to make other goods you still have

- 6 months for services

Accountingweb reported on 12th June that the goal posts seem to have moved, here is their example..

Ken has been a self-employed pest controller for many years. He registered for VAT with effect from 1 May 2015, at which point he held a van that cost him £24,000 on 1 May 2013, and equipment that he bought for £9,000 on 1 May 2012, both inclusive of VAT. He expects to use the van for eight years and the tools for five years.

Previously most VAT advisers would advise Ken to reclaim VAT of £4,000 in respect of the van and £1,500 paid on the equipment.

The new HMRC interpretation of EC VAT Directive 2006/112 article 289 (set out in VAT Input Tax Manual para 32000) is that as the van has been used for 2/8th of its life, just £3,000 (6/8 x 4000) of the input VAT can be reclaimed. For the equipment a similar calculation reduces the VAT reclaim to £600 (2/5 x1500).

Ken is obviously losing out by £1,900 of unrecoverable VAT.

Taxation Magazine also have an article pointing out the goal posts have moved

What is worrying is that as so many tax advisers will have given potentially incorrect advice based on the new interpretation by HMRC (which HMRC say isn’t a change), will this mean that we will see backdated enquiries and penalties for clients?

steve@bicknells.net

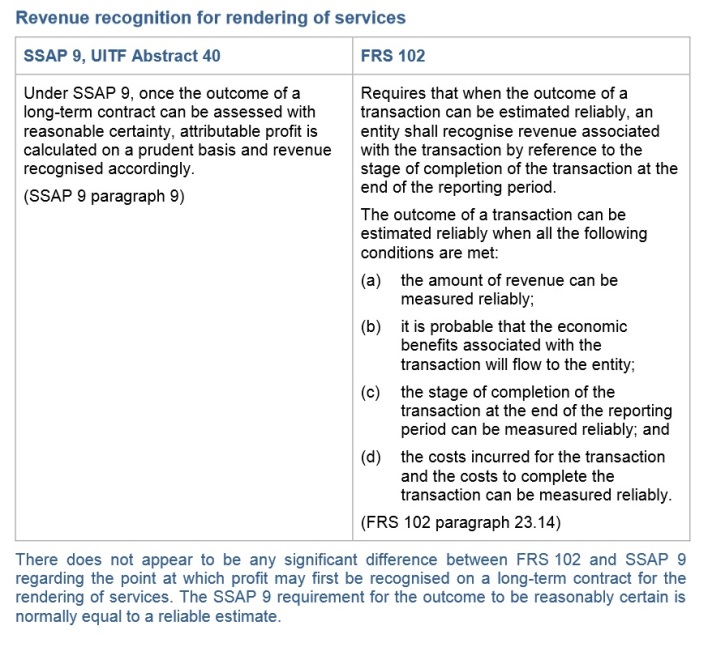

When should you recognise revenue on services provided?

The International Accounting Standard IAS 18 states

‘where the outcome of a transaction involving the rendering of services can be estimated reliably, associated revenue should be recognised by reference to the stage of completion of the transaction at the end of the reporting period’ . In other words, the revenue is recognised gradually, rather than all at one ‘critical point’, as is the case for revenue from the sale of goods. IAS 18 further states that the outcome of a transaction can be estimated reliably when all the following conditions are satisfied:

(a) The amount of revenue can be measured reliably.

(b) It is probable that the economic benefits associated with the transaction will flow to the seller.

(c) The stage of completion of the transaction at the end of the reporting period can be measured reliably.

(d) The costs incurred to date for the transaction and the costs to complete the transaction can be measured reliably.IAS 18 does not prescribe one single method that should be used for determining the stage of completion of a service transaction. However the standard does provide some examples of suitable methods:

(a) Surveys of work performed.

(b) Services performed to date as a percentage of total services to be performed.

(c) The proportion that costs incurred to date bear to the estimated total costs of the transaction.If it is not possible to reliably measure the outcome of a transaction involving the provision of services (perhaps because the transaction is in its very early stages) then revenue should be recognised only to the extent of costs incurred by the seller, assuming these costs are recoverable from the buyer.

In the UK UITF40 and SSAP9 defined the way we report revenue and profit in relation to Services, although accountants and lawyers were among the most high profile casualties of the new regime back in 2005, which forced them to re-catagorise WIP and Revenue, many other service providers also had to consider how they accounted for income. Professionals such as surveyors, architects, doctors and dentists all had to consider the impact of the new rules on their tax liabilities.

FRS102 has not changed the rules.

steve@bicknells.net

Do you know how FRS102 is changing Currency Conversion?

FRS102 affects many things and Section 30 sets out the rules on Currency Conversion.

FRS 102 states that

An entity can conduct foreign activities in two ways. It may have transactions in foreign currencies or it may have foreign operations. In addition, an entity may present its financial statements in a foreign currency

Entities will have a Functional Currency (a concept also used in IFRS) and it allows translation into a Presentation Currency

Reporting at the end of the subsequent reporting periods

30.9 At the end of each reporting period, an entity shall:

(a) translate foreign currency monetary items using the closing rate;

(b) translate non-monetary items that are measured in terms of historical cost in a foreign currency using the exchange rate at the date of the transaction; and

(c) translate non-monetary items that are measured at fair value in a foreign currency using the exchange rates at the date when the fair value was determined.

30.10 An entity shall recognise, in profit or loss in the period in which they arise, exchange differences arising on the settlement of monetary items or on translating monetary items at rates different from those at which they were translated on initial recognition during the period or in previous periods

That all sounds pretty familiar, however, as pointed out by Grant Thornton

Under SSAP 20 Foreign currency translation in current UK GAAP, where matching forward contracts are in place for a transaction, the contracted rate can be used for translation of the matched transaction. This option is not permitted under FRS 102. Instead, a foreign exchange forward contract will be recognised on the balance sheet as a financial instrument at fair value and the associated debtor or creditor will be retranslated at the year-end rate.

A key difference (FRS102) to note in comparison to SSAP 20 Foreign Currency Translation is that SSAP 20 regards consolidated goodwill as an asset of the parent company and not the subsidiary. [Steve Collings Blog]

Online traders targeted by HMRC

The Revenue has sent 14,000 letters to traders suspected of running a business and failing to declare this on their tax returns.

Of these, 1,000 letters are being sent to people where the taxman has already identified a shortfall on their self-assessment forms.

Some of those targeted make as little as £100 profit online.

It was reported in the Telegraph that eBay, Etsy, Amazon and Gumtree are being forced to hand over customer account details, including their selling activity, as part of the taxman’s legal powers that were extended last year.

The criteria used to assess if an activity is a hobby or a business are:

- The size and commerciality of the activity.

- The frequency of the activity and transactions

- The application of business principles.

- Whether there is a genuine profit motive.

- The amount of time devoted to the activities.

- The existence of arm’s-length customers (as opposed to just selling your wares to family and friends).

HMRC have some great examples to help you decided, for example

Gail is a full-time employee working for a stationery company. She pays her PAYE tax on this employment every month.

In her free time Gail makes cushions and uses most of them in her home. Occasionally she sells them to friends and work colleagues for an amount that just covers the cost of materials of £15. Sometimes she makes a loss. Any money she does make goes towards her holiday fund.

She decides to make extra cash by selling cushions on an Internet auction site and starts auctioning three or four to see how they go. They all sell for more than £50, a profit of at least £35 each.

She uses this money to buy more materials and within a month she is selling around ten cushions a week, always at a profit, and is considering setting up her own website.

Gail’s initial sales of cushions to friends are not classed as trading. It lacks commerciality and she does not set out to make a profit. The occasional sales are a by-product of her hobby. Once she begins to auction her cushions, she has moved into the realms of commerciality.

She is systematically selling her goods to make a profit. She will need to inform HMRC about her trade, and keep records of all her transactions. On the level of sales shown in the example the potential turnover of around £26,000 is well below the VAT annual threshold so Gail does not need to register for VAT.

Many traders start off in a small way and don’t realise that they need to register with HMRC, they assume their activity will be treated as a hobby, but things can grow quickly.

You should register as Self Employed as soon as your hobby becomes a commercial venture, even if you are losing money!

If you don’t register, HMRC will be looking for you and if you have an online business it won’t be hard for them to find you.

steve@bicknells.net

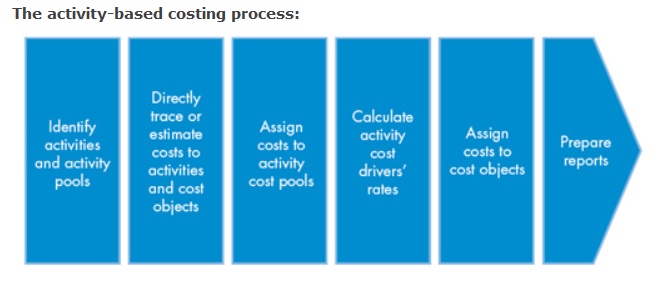

Overhead allocation using ABC

CIMA Official Terminology describes activity-based costing as an approach to the costing and monitoring of activities, which involves tracing resource consumption and costing final outputs. Resources are assigned to activities and activities to cost objects. The latter use cost drivers to attach activity costs to outputs.

What are Activity Pools and Cost Drivers?

Activity Pools

- Purchase Orders

- Machine Set Ups

- Packaging

Cost Drivers

- Number of Purchase Orders

- Number of Machine Set Ups

- Number of items to package

What would the traditional methods of allocation have been?

- Direct Labour Hours

- Machine Hours

- Floor Area

Using Activity Based Costing can produce very different results to Traditional Methods, click here for an example

steve@bicknells.net