Home » Accountant (Page 8)

Category Archives: Accountant

Does your accountant understand Construction?

![fotolia_1931265[1]](https://business-accountant.com/wp-content/uploads/2013/09/fotolia_19312651.jpg)

Perhaps one of the most important things an individual can do when self-employed is to keep meticulous accounts. This means not only keeping a record of income and expenditure, but also work in progress at the end of the tax year. The case of Mark Smith v HMRC [2012] TC02321, which was an appeal heard in the First Tier Tribunal of the Tax Chamber illustrates the potential ramifications of failing to keep one’s accounts in sufficient order.

The appellant in this case was trading as a builder. He sought to appeal against assessments to tax and amendments to self-assessments in respect of the years ending 5 April 2001 to 5 April 2007 inclusive.

The central issue before the tribunal related to the appellant’s computation of profits. It was admitted that his accounts understated the profits gained in a particular tax year. However, it was his contention that this was a “one-off”. Nevertheless, in following years, his assessments were raised in an effort to make good the profits previously understated. The question was whether these assessments were justified.

In the construction industry, building projects can last for several months or years, generally, each month the contractor will submit an application for payment to the client based on their assessment of the work. When and if the client agrees they will certify the work and make payment, if they disagree a lower amount will be certified. The certification process can often take up to 3 weeks.

The Contractors Quantity Surveyor will prepare a report known as a Cost Value Reconciliation (CVR) or Cost Value Comparison (CVC). These will show the value of the work completed to a set date (whether certified or not) and the profit, here is an example

http://www.online-templatestore.com/store/Free/Cost%20vs%20Value%20Report.pdf

Often a CVR will list every sub-contract package and the materials ordered in great detail compared to the tender and stage of completion.

The underlying principle is that of ‘matching’ costs and revenue to allow the accountant to accrue for costs and adjust revenue (accruing Income).

The decision

The tribunal held that HMRC’s assessments were in fact justified. In relation to quantum, the tribunal confirmed that the burden of proving the amount assessed lay with the taxpayer. In this case, the appellant failed to adduce evidence sufficient to displace the assessments made by HMRC. Accordingly, the assessments were confirmed and the appeal was dismissed. The appellant therefore remained liable in the amount as assessed by HMRC.

The reason why HMRC were successful was that in the case of Mark Smith he based his income on certified revenue, this meant that the profit was understated, within Construction “UK GAAP” requires revenue to be reported on application based on the CVR matching approach.

The details of the additional profits and tax for each year are as follows:

(1)2000/01: additional profits of £43,189 giving rise to tax of £17,275.60

(2)2001/02: additional profits of £65,205 giving rise to tax of £24,972.02

(3)2002/03: additional profits of £73,889 giving rise to tax of £27,737.86

(4)2003/04:additional profits of £70,023 giving rise to tax of £27,503.41

(5)2004/05: additional profits of £70,000 giving rise to tax of 27,704.18

(6)2005/06: additional profits of £65,240 giving rise to tax of £26,735.44

(7)2006/07: additional profits of £45,541 giving rise to tax of £18,671.81

Who bears the burden of proving excessive assessments?

In establishing discovery assessments, HMRC bears the burden of demonstrating that they are valid. However, if an individual taxpayer believes the assessment to be excessive, the burden then shifts to that individual to prove that is the case.

Section 50(6) of the Taxes Management Act 1970 provides that:

“If, on an appeal notified to the tribunal, the tribunal decides—

[…]

(c) that the appellant is overcharged by an assessment other than a self- assessment, the assessment shall be reduced accordingly, but otherwise the assessment shall stand good.”

In other words, once HMRC makes an assessment, the amount of that assessment stands unless the individual taxpayer can prove on the balance of probabilities (through the production of evidence) that the assessment should be different.

In this instance, HMRC had substantially underestimated the appellant’s profits for the year 2004/05. The appellant submitted that his underestimation for profits in 2004/05 was a ‘one-off’, and therefore did not warrant any adjustment for other years. It was for him to prove this. He was unable to do so and failed to adduce any evidence. HMRC concluded that the appellant had been gravely negligent in the conduct of his tax affairs and that further assessments were therefore justified.

Additionally, the appellant seemed to provide no explanation to the Tribunal to account for the under-declaration. There may have been a legitimate reason for this, and had his accounts been kept consistently throughout the period in question, he would have perhaps had evidence capable of proving to the tribunal that the error was in fact a sole incident.

This is a joint blog between Rebecca Broadbent (Practice Manager, Chambers of Jason Elliott [Barristers]) and Steve Bicknell

4 Things a charity needs to know about annual reporting

Image courtesy of Stuart Miles / FreeDigitalPhotos.net

Charities survive on their reputation.

Whether your charity is funded from voluntary donations, grant funding or commercial activities it is important that all funders can look up key information to check your organisation is working effectively. The annual reporting is time-consuming and potentially costly, but it is possible to restructure a charity to save on administrative costs.

1 – Charities must report to their regulator

Charities in England & Wales with an annual income of over £10,000 must report to the Charity Commission for England and Wales. Charities in Scotland must report to the Office of the Scottish Charity Regulator. The Charity Commission for Northern Ireland has recently been set up for the regulation of charities in Northern Ireland.

2 – Cross border charities must report multiple times

Under the Charities and Trustee Investment (Scotland) Act 2005 (the 2005 Act), bodies which represent themselves as charities in Scotland are required to register with OSCR. This requirement includes bodies which are established and/or registered as charities in other legal jurisdictions, such as England and Wales.

3 – Not all charities require an audit

Historically, the term ‘audit’ has been used loosely to describe any independent scrutiny of accounts. However, under the Charity Regulations if the term ‘audit’ is used in a charity’s constitution or governing document the charity must have its accounts audited by a registered auditor.

Charity Trustees may consider that the benefits of having an audit are outweighed by the costs. Trustees may wish to review their constitution and either:

- retain the term audit in their constitution or

- amend the constitution to require an independent examination of the accounts

Any change to the constitution must be carried out in accordance with the terms of the constitution and following professional advice. Notification of any change must also be sent to the charity’s regulator.

If an audit is not required by your members or governing document, an independent examination can be much more cost-effective than a full external audit and can be carried out by wider range of accountants and financial professionals including a member of the Chartered Institute of Management Accountants.

4 – Your current legal form may not be the best for you

Many charities have been set up with archaic governing documents and may be a Trust or Limited Company or other type of body, which is no longer suited to them. Trustees of Trusts and Unincorporated Associations are personally liable for the actions of a charity and expose themselves to a greater risk that Trustees of a Limited Company. Trustees of a Limited Company are required to report to Companies House as well as their charity regulator, increasing the administrative cost of the organisation.

A new legal form has been developed to allow charities to incorporate and report to just one body. Any Charitable Incorporated Organisation in England & Wales or Scottish Charitable Incorporated Organisation in Scotland is recognised as a corporate body which is a legal entity having, on the whole, the same status as a natural person.

This means it has many of the same rights, protections, privileges, responsibilities and liabilities that an individual would have under the law. As a legal entity, the CIO / SCIO may enter into the same type of transactions as a natural person, such as entering into contracts, employing staff, incurring debts, owning property, suing and being sued. As the transactions of the CIO / SCIO are undertaken by it directly, rather than by its charity trustees on its behalf, the charity trustees are in general protected from incurring personal liability in the same way company directors of a Limited Company.

In England and Wales you can:

- apply to register a completely new organisation as a CIO

- set up a CIO to replace an existing unincorporated association or trust

(You can’t currently convert a charitable company to a CIO)

In Scotland you can:

- apply to register a completely new organisation as a SCIO

- convert existing charitable companies, charitable industrial and provident societies and charities of any other legal form to a SCIO

For more information on an accountancy firm who can provide the statutory reporting, and also support you in the running of your charity please contact a member of the Chartered Institute of Management Accountants using the link to The Team above.

Useful links

| Charity Commission: | http://www.charitycommission.gov.uk/ |

| OSCR: | http://www.oscr.org.uk/ |

| Charity Commission NI: | http://www.charitycommissionni.org.uk/ |

When the HMRC inspector visits get some extra help

HMRC campaigns and task forces are on going and Compliance checks are becoming common. As stated in the HMRC Infographic record compliance yielded £20.7bn.

So its worth knowing that you can appoint an extra adviser to help you answer the inspectors questions, its quick and easy to to arrange using this link

http://www.hmrc.gov.uk/forms/Comp1.pdf

Its a temporary authorisation that does not cancel or amend permanent authorisations ie your normal advisers/accountants

HMRC have also issued new Fact Sheets for Compliance Checks and Penalties

http://www.hmrc.gov.uk/compliance/factsheets.htm

Sometimes we all need a little help and specialist advice can be invaluable

steve@bicknells.net

CIMA la difference?

For most clients the institute a qualified accountant is a member of isn’t a key factor, especially if they are only looking to have their accounts prepared and tax return done. Some simply look for a “Chartered” accountant, which most qualified accountants in practice are if they belong to one of the main professional bodies.

However there are some key differences between the skills and experience of a traditional “high street” accountant and a CIMA Member in Practice. Here are a few:

- A CIMA accountant will tend to look at the business from the inside, rather than just the numbers that make up statutory accounts.

- Their professional training placed a lot of emphasis on providing businesses with meaningful data to support the day to day running of the business, so called management accounts.

- They are likely to have been exposed to a variety of different software systems, and may think more in terms of business processes.

- They are less likely to have worked on statutory audits (which are usually only needed for companies that meet 2 out of the following requirements: turnover of over £6.5 million; assets of more than £3.26 million; has more than 50 employees) so for SME’s that tends not to be an issue.

- They will generally be less obsessed with timesheets and billable hours!

That’s not to say that hiring an accountant who has just emerged from a 30 year career in the Management Accounting department at a local shoe factory is going to be the best thing for a small business, but CIMA have thought about that. Before a CIMA member can get the Practising Certificate they need in order to provide services to the public they need to meet the institute’s skills and experience requirements.

Back to the beginning, many individuals and companies hire an accountant without checking if they are qualified at all. Unlike the financial services industry, accountancy is lightly regulated and anyone can set up shop. Indeed, there are many “qualified by experience” accountants out there giving a good service to their clients. However should things go wrong ……. we’ll look at “when accountants go bad” in a future blog.

Compare the market!

As a nation we seem obsessed with comparison websites and we readily switch insurers to save £50-100 on our car or home insurance. So why don’t businesses market test their accountant more often? Is it because they are happy enough with the basic service and see little differentiation between local firms, or do they think its a lot of hassle to change even if they are open to the idea? I often meet business owners who aren’t entirely happy with their accountant but can’t bring themselves to do much about it, so when I get the chance I explain how easy it is to change, at the right time.

Service and other benefits aside, businesses can often save significant amounts by shopping around. This particularly applies the more services you require. Take a look at your accountancy and bookkeeping costs over the last year. How many items were billed separately, or in addition to the core fee you had agreed? Was your personal tax on top of the fee for the accounts?

In a future blog I’ll look at how to go about changing accountants and the differences a CIMA accountant can bring.

Meanwhile if you can see some benefit in changing your accountant, go (and) compare!

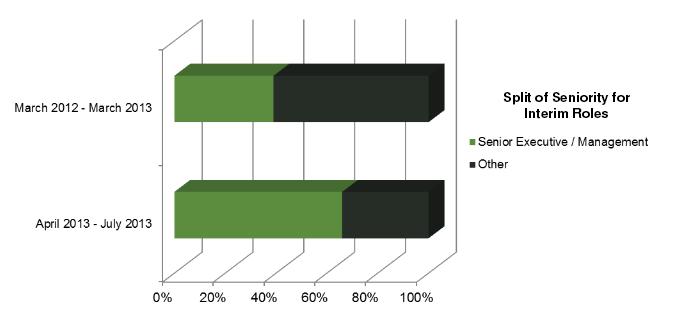

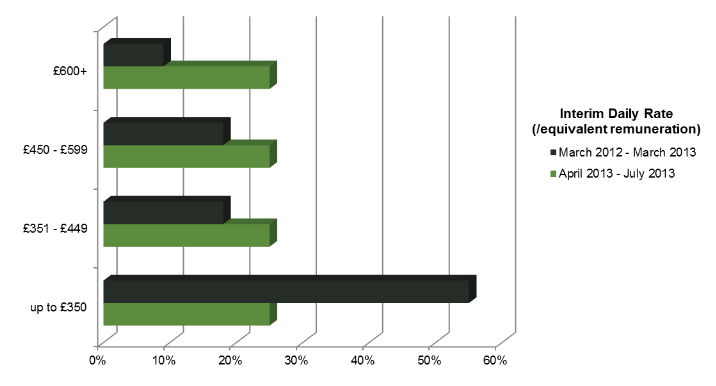

Why has demand for senior interim accountants doubled in April to July 2013?

Many companies that put projects on hold during the recession are now reinvigorating them as the market continues to show signs of recovery. This has created demand for experienced senior interims who can lead projects efficiently, ensuring that they run within budget and timescales. CIMA

The Interim market is estimated to be worth £1.5bn.

Key demand continues to be for experienced professionals who can ensure companies’ systems and processes are running as efficiently as possible. They will be challenged with the task of making any necessary improvements to achieve the project objectives. Their focus continues to be on commercial skills and profitability. Organisations want professionals who are able to make a calculated decision about things that will have an impact on how the business will run in the future.

Partner Financial Trend Survey July 2013 reported

steve@bicknells.net

Does your accountant work for you?

The role of an accountant in a business.

Many small businesses do not have an accountant on the payroll and hire external consultants to fulfil their financial needs. In too many cases the accountant is only working for the benefit of external stakeholders such as Companies House and HMRC. This role is described as financial accounting, with a focus on historical information prepared for people outside the organisation.

To be in control of your business you need to have up to date and forward-looking information. This role is fulfilled by a Management Accountant.

What is a management accountant?

The definition from Wikipedia at the time of writing:

[Management accounting] is concerned with the provisions and use of accounting information to managers within organizations, to provide them with the basis to make informed business decisions that will allow them to be better equipped in their management and control functions.

The summary definition from the Chartered Institute of Management Accountants:

Management accounting combines accounting, finance and management with the leading edge techniques needed to drive successful businesses.

Working together.

To get the best value out of your accountant and to deliver the best return from your business, you and your accountant need to work in concert. Accountants hate the dreaded shoebox moment where a whole year’s transactions are delivered months after the financial year end. This approach costs the client more as the accountant will be charging for sifting through pieces of paper. The value to the business of the accounts is reduced as any analysis is out of date.

With cloud software systems you and your accountant can work in real time. Cash transactions can be entered into the system automatically from your online banking meaning that you are not taking up your accountant’s time or yours with inputting figures from paper statements. This also means that your accountant can see the business in real time and is able to support you and perform a leading role.

Leading or following?

If your accountant is someone you hear from once a year, the service they provide is passive and follows your business. It may be time for a change to a firm with a focus on leading your organisation and being active throughout the year.

For more information on an accountancy firm who can provide the statutory accounting, but focuses on leading your business to greater success please contact a member of the Chartered Institute of Management Accountants using the link to The Team above.

Useful links

| CIMA: | http://www.cimaglobal.com/About-us/What-is-management-accounting/ |

| Wikipedia: | http://en.wikipedia.org/wiki/Management_accounting |