Home » Accountant (Page 4)

Category Archives: Accountant

What flavour is your Accountant?

Thanks to http://www.freedigitalphotos.net

One of the great joys of working as a ‘CIMA MiP’ (“Chartered Institute of Management Accountants, Member in Pratice”) is that we are generally dealing with ‘small’ and ‘micro’ client firms (micro defined by EU regulations as firms with less than 10 employees/ £2m turnover; small defined as firms with less than 50 employees/ £10m turnover) and that we become involved in an enormous breadth and depth of subjects.

One of the less welcome challenges however is that as far as most small and micro business owners and managers are concerned, one accountant is the same as any other and this includes the myriad unqualified accountants who practice their particular brand of accounting services at rock-bottom rates. Indeed it is rare that I have been asked whether I am a ‘qualified’ accountant, and is rarer still that I am asked what that qualification is (in fact I cannot ever recall being asked that question by a client). The client generally assumes that because one calls oneself an ‘accountant’ then one can ‘do accounts’ and that accountants are all the same.

We’re not.

My particular practice specialises in manufacturing clients and most new clients have come from existing client referrals. Fortunately I do not need to be a great sales person to convert a prospect into a new client when (a). there is a recommendation from an existing client and (b). we appear to ‘speak the same language’. Clients generally put this down to my having owned and run manufacturing firms and to some degree that is true, but is is also because of my CIMA training.

If you’re looking for year end accounts, audit, or tax computation then you will likely be talking to a ‘Certified Accountant’ or ‘Chartered Accountant’, but where they will be reporting back to you on how well (or otherwise) you did overall last year and what your tax liability is, the CIMA ‘Chartered Management Accountant’ will be working with you to establish what activities made money and why, and whether you can do more of it, and of course which did not and how to avoid this in future; indeed the focus is very much ‘future’ as much as ‘past’.

In terms of the client business, it’s not difficult to see that helping the client to understand their business is a valuable element in managing, changing, and improving the business, and this is something which CIMA qualified people have to offer any business, so it’s a great shame that Chartered Management Accountants tend to be employed by big businesses who understand the difference between the different accounting disciplines.

None of this is to say that a Certified Accountant or Chartered Accountant could never do what the Chartered Management Accountant does, but it is not what they have been trained to do and equally as a Chartered Management Accountant in practice for twenty-two years I provide a ‘full service’ including year end accounts and tax returns for my clients, albeit the main focus remains helping them to improve their business.

I would urge Chartered Management Accountants to seriously consider a career in the small and micro business sector which accounts for 99.3% of the 4.7 million businesses in the UK (source: BIS 2013) and 47% of private sector employment (source: FSB 2013) and which is a vital part of the UK economy: whether in practice servicing a number of clients, or a full-time employee of a particular firm, I am sure that you will find the experience very rewarding

I would equally urge owners and managers in that sector to become aware of the differences between the main accounting bodies and the relative strengths of each, and to be sure that whoever they engage with will meet the needs of their particular business.

Paul Driscoll is a Chairman of CIMA MiPs in South West England and South Wales, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and a number of manufacturing companies, and is a board level adviser to a variety of other businesses.

Simple Tax – a great way to file your return

I read about Simple Tax in an article in the Express…

Backed by venture capital investors including EC1 Capital, Seedcamp and Charlotte Street Capital, SimpleTax was set up to help customers find ways to save money on their tax bills and file returns online with HMRC in minutes.

SimpleTax’s users have so far cut a total of £2.5 million from their tax bills

So I tried it out, it’s great and it’s free.

You will need your HMRC Online filing details if you want to file your return alternatively you can just print out the return.

For taxpayers who have very straightforward returns Simple Tax should make it quicker and easier to complete and file online.

As you prepare the return Simple Tax gives you tips on things you can claim and ways to save tax.

Take a look and see what you think https://www.gosimpletax.com/

For those with more complicated tax returns get advice from a CIMA Accountant.

steve@bicknells.net

Automatic enrolment: large employers are all in

![]()

The Pension Regulator’s latest post…..

Our report on the impact of automatic enrolment reveals that 99% of all the UK’s largest employers met their legal duties without the need for us to use our statutory powers.

This is encouraging news as thousands of medium employers are currently reaching their staging dates. We will continue to work over the months ahead to ensure that medium and small employers understand their obligations, comply with their legal duties and continue to view non-compliance by other employers as unacceptable

Are you ready for Auto Enrolment?

steve@bicknells.net

Don’t forget your 31 July Payment on Account!

The 31 July 2014 is the date that you should make your second payment on account to HMRC.

For example on 31 July 2014, you’d make your second payment on account for the 2013-14 tax year.

From the 31 July you will have to pay interest on anything you owe and haven’t paid, including any unpaid penalties, until HMRC receives your payment.

As well as the 4.54 million self-employed people in the UK, higher rate taxpayers, company directors and anyone with more than one income are required to make a payment on account – part of their annual tax payment.

Don’t forget to pay!

steve@bicknells.net

5 ways to pay less VAT

Many small businesses assume there is only one type of VAT scheme, the standard VAT scheme where you pay VAT on Sales and reclaim VAT on Purchases but in fact there are several schemes and they could save you money:

Cash Accounting

Using the Cash Accounting Scheme, you:

- pay VAT on your sales when your customers pay you

- reclaim VAT on your purchases when you have paid your suppliers

You can use the Cash Accounting Scheme if your estimated VAT taxable turnover during the next tax year is not more than £1.35 million.

Cash Accounting can improve your cashflow if your customers pay later than you need to pay your suppliers.

Flat Rate Scheme

You can join the Flat Rate Scheme for VAT and so pay VAT as a flat rate percentage of your turnover if:

- your estimated VAT taxable turnover – excluding VAT – in the next year will be £150,000 or less.

Generally you don’t reclaim any of the VAT that you pay on purchases, although you may be able to claim back the VAT on capital assets worth more than £2,000

There’s a one per cent reduction in the flat rate percentages for your first year of VAT registration.

You can get a list of Flat Rates by following this Link

Flat Rate is easy to use and can save you money if you have a lower than average level of VAT purchases.

Annual Accounting Scheme

Using the Annual Accounting Scheme, you make either nine interim payments at monthly intervals, or three quarterly interim payments, throughout the year. You only need to complete one return at the end of each year. At that point you must pay any outstanding amount. If you have overpaid, you will receive a refund.

You can use the Annual Accounting Scheme if your estimated VAT taxable turnover for the coming year is not more than £1.35 million.

This could save you money by saving time.

Retail Schemes

Using standard VAT accounting, if you are VAT-registered then you must record the VAT on each sale in your accounting records. But with the VAT retail schemes, you work out the value of your total VAT taxable sales for a period – for example, a day – and the proportions of that total that are taxable at different rates of VAT (standard, reduced and zero) according to the scheme you are using. You then apply the appropriate VAT fraction to that sales figure to calculate your VAT due.

You do not need to record VAT separately in your accounts for each and every retail sale you make. This is particularly beneficial if you make a number of low value and/or small quantity sales to the general public. This can save you a lot of time and record keeping.

Margin Schemes

Normally you charge VAT on your sales, and reclaim VAT on your purchases. However, if you sell second-hand goods, works of art, antiques or collectibles, there may have been no VAT for you to reclaim when you bought them. You may be able to use a VAT margin scheme. This enables you to account for VAT only on the difference between the price you paid for an item and the price at which you sell it – your margin. You won’t pay any VAT if you don’t make a profit on a deal. You can still use standard VAT accounting for other sales and purchases such as overheads.

steve@bicknells.net

5 key questions you need to ask your FD

As businesses grow, their needs increase. The person steering the finances needs to be someone who can take on a broad commercial role. Forecasting, IT, tax issues, insurance and back office functions – all these need to run smoothly. But a fast-growth business needs someone who can anticipate both future opportunities and potential problems.

A good financial director will help owner-managers understand which aspects of the business are the most profitable, as well as forecasting ways to exploit other opportunities. (Santander)

So what key questions should you regularly ask your FD…..

- What is our cash cycle and how can we improve it – Cash Cycle Blog

- What Key Performance Indicators should we use and what are they telling us – KPI Blog

- How can we improve profitability – 15 ways to improve profitability Blog

- What is our Business Plan and is it the right plan – Business Plan Blog

- Can we reduce Overheads – 10 creative ways to reduce overheads Blog

steve@bicknells.net

Is your accountant qualified?

The ACCA issued a warning in May after research from cloud accounting software provider ClearBooks showed just 8 per cent of small businesses considered an accountant’s qualifications when choosing one. There is no law preventing anyone from calling themselves an accountant, and that as a result small businesses could be unknowingly paying someone without the necessary skills to handle their finances and help their business grow, who isn’t regulated or insured against risk.

CIMA (Chartered Institute of Management Accountants) Members in Practice are monitored by CIMA for:

- Continuous Professional Development

- Anti Money Laundering Compliance

- Professional Indemnity Insurance

- Continuity Agreements

- Letters of engagement

- Ethical conduct

CIMA operates a Masters degree standard scheme of qualifying examinations for prospective members. It is active in promoting local education, training and management development operations, the promotion of new techniques through its research foundation and the dissemination of management accounting practices through publications and other media related activities. WIKIPEDIA

You can find out more at www.business-accountant.com and www.cimaglobal.com

steve@bicknells.net

10 of the Biggest Headaches of Auto Enrolment for Employers

According to Now Pensions the 10 biggest headaches faced by employers are:

- An administrative nightmare – it doesn’t have to be nightmare provided you plan ahead and get help if you need it, accountants are the most used source of help and advice.

- Will payroll be able to cope? Yes but it takes planning and preparation

- A Communication challenge – Employees find pensions complicated and auto enrolment could be the first long tem savings product they have, so simplicity is crucial. Auto Enrolment does require the right correspondence at the right time, so make sure you get it right!

- Future Liabilities – The Pension Regulator enforces compliance and employers must not encourage or put pressure on employees to opt out.

- Middleware – this is software that makes your IT systems talk to each other, many SME’s will not need middleware as the payroll software will do the job of reporting the data to the pension provider

- Responsibility – Make sure you know where the responsibilities fall on your team, mistakes can be costly

- Existing Schemes – Not all existing schemes will be suitable for auto enrolment, check that your scheme will comply or change it

- Investment – Most employees will have never invested in their lives so its important to choose an auto enrolment provider who can help them decide on which funds to invest in

- Value for Money – NEST, Now Pensions and The People Pensions have very low charging structures

- What will it cost – Don’t forget the internal management costs when you choose a scheme, how easy will it be to operate?

steve@bicknells.net

We hear many of the same concerns about auto enrolment being raised on a regular basis in our discussions with employers of all sizes. So you’re not alone with your auto enrolment concerns. That’s why we’ve addressed ten of the biggest headaches and their remedies below.

1: An administrative nightmare

Get all the help you can before the staging date. Employers can lighten the load by partnering with providers that will do much of the work for them. Some pension providers have invested in technology that can automate the administration of auto-enrolment. This includes assessing which sort of scheme is most suitable for your workforce, working out which employees need to be automatically enrolled and calculating contributions and issuing communications to your employees based on the outputs of the assessment.

Once a clear process is up and running, administering auto-enrolment is relatively easy – but to get to that point organisations need to put the right systems in place. That means selecting your implementation partners, establishing who is responsible for which parts of the process and ensuring clear access to your HR and payroll data. A robust project plan is essential.

Once a clear process is up and running, administering auto-enrolment is relatively easy – but to get to that point organisations need to put the right systems in place. That means selecting your implementation partners, establishing who is responsible for which parts of the process and ensuring clear access to your HR and payroll data. A robust project plan is essential.

2: Will payroll be able to cope?

Yes, provided you make sure the correct people at your payroll provider and your pension provider are talking to each other and exchanging data in the right format.

A strategic decision is necessary to decide on whether payroll will handle employee categorisation ensuring that your auto-enrolment obligations are met compliantly or whether your pension provider will do this. Larger payroll providers and pension providers such as ourselves have the capability to create a record to demonstrate to the Pension Regulator that you have fully complied with your auto-enrolment obligations.

3: A Communications challenge

Employees find pensions complicated, and for many individuals an auto-enrolment pension will be the first long-term savings product they have ever held. So simplicity is crucial.

Research has shown that messages work best when they speak to employees in a language they understand, through a medium via which they like to be communicated. Messages delivered in the run-up to auto-enrolment are particularly important as they will set the agenda for the entire project. So think about what will work best for your workforce. A wealth of compliant communication material that can be tailored to the needs of your workforce is available at no cost from quality pension providers.

4. Future liabilities

The Pensions Regulator enforces compliance with the auto-enrolment rules, and one of its top priorities is ensuring employers do not encourage or put pressure on employees to opt out of the pension scheme after they have been automatically enrolled into it. It will be scrutinising employers that have unusually high opt-out rates. Employers that persistently break the rules by inducing staff to opt-out can be fined up to £10,000 a day. The Pensions Regulator is hoping whistleblowers will report it of breaches of auto-enrolment regulations.

Using compliant communication materials can alleviate the risk of regulatory action. Employers that use pension providers with auto-enrolment middleware will also have a report that demonstrates to the Pensions Regulator that auto-enrolment obligations have been fulfilled, although it will only be as accurate as the information given by the employer.

5: What is ‘middleware’?

Middleware is software that glues different IT systems together. In the context of auto-enrolment, that means analysing the age and salary data of your workforce, working out the earnings upon which contributions are based, taking deductions through payroll and paying them over to the pension provider.

6: Responsibility

For auto-enrolment to run smoothly both your payroll and pensions departments need to talk to each other. Unfortunately the fact that auto-enrolment crosses both areas can lead to confusion over who is responsible for what part of the process. This is best addressed by assigning auto-enrolment to a corporate sponsor high enough up in your organisation to ensure that responsibility for tasks is clearly apportioned, and delegating someone to be involved through the implementation project phase and beyond.

7: Existing Schemes

This will depend on the sort of scheme you have and how you decide to include your  current non-pensioned staff. If your existing scheme already complies with the minimum criteria set for auto-enrolment, which relate to contribution rates, charges and default funds, then staff already in it will see no change.

current non-pensioned staff. If your existing scheme already complies with the minimum criteria set for auto-enrolment, which relate to contribution rates, charges and default funds, then staff already in it will see no change.

You will need to make some important decisions about how you design your pension offering for the rest of your staff. Do you want a single scheme for everyone in the organisation? Do you want a multifaceted scheme for your senior staff and a more basic scheme for other tiers of your workforce? You may choose to preserve your existing scheme for those already in it, while automatically enrolling those not currently in it into a new scheme. Independent Financial Advisers or Employee Benefit Consultants can provide information and advice in exchange for a fee or Providers like NOW: Pensions can help you to analyse your workforce and provide suggestions based on our previous experience.

8: Investment

Many employees will have never invested this way before in their lives. Poor performance will not only create disgruntled employees – it will also leave some staff with pensions so low they cannot afford to retire when they get older. So choosing the right default investment fund is crucial for an employer.

The performance of different pension providers’ default funds varies hugely. Pensions are long-term savings vehicles which means that even very small increases in performance can make a significant difference. For example, over a 40-year investment, an annual return of 7% will deliver a fund 30% higher than one achieving 6%.

Look for a default fund with a proven track record, one that has delivered stable returns over a long period of time and in different market conditions, and is unlikely to have changed as this may increase the associated communication costs with your employees.

9: Value for money

Charges are one of the biggest factors in determining how much pension employees ultimately receive. Sadly, pensions that charges as much as 1.5% of the fund value each year are common in the UK. We charge just 0.3% of fund value plus a monthly £1.50

Charges are one of the biggest factors in determining how much pension employees ultimately receive. Sadly, pensions that charges as much as 1.5% of the fund value each year are common in the UK. We charge just 0.3% of fund value plus a monthly £1.50

admin fee (£0.30 for low earners during the initial phasing process). For a 25-year-old earning £26,000 saving 8% of salary for 40 years, that can mean the difference between building up a pot of £716,000 rather than the £547,000* generated in a scheme charging 1.5%. Our low charge scheme gives the saver in this example 30% more pension for exactly the same contributions. It may sound hard to believe, but the more expensive provider takes an extra £169,000 in charges out of the saver’s pot.

*Assumes salary increases by 4% a year, fund increases by 7% a year.

10: What will it cost me?

The overall cost of auto enrolment will depend on where you go for your pension and what you need from your pension.

Costs not only include fees and charges but also, human resources and administration so it is important to bear the overall cost in mind when choosing a pension provider. With NOW: Pensions, the employer can either choose to pay nothing in the way of administration with the fees coming from the members or you may choose to pay these fees for your members (employees); on-going costs such as communications are minimal and there are no set-up fees.

It is important to get your provider right from the start as changing further down the line will incur many additional costs.

– See more at: http://www.nowpensions.com/blog/auto-enrolment-headaches/#sthash.HhCRbQuD.dpuf

Setting up business finances – Do’s and Don’ts

For any business owner getting the right financial advice when you start the business is critical, here are some Do’s and Don’ts

Separate your bank accounts

Many start ups try mixing business and personal transactions in their personal bank accounts, its a total nightmare, don’t do it, get a business bank account.

Mixing things up will almost certainly have tax implications.

Get help and register for Tax

Getting things right at the beginning is extremely important and a CIMA Accountant can makesure you choose the right business structure and help you register for VAT, PAYE, CIS and other taxes. Choosing the right VAT scheme will save you tax – take a look at this blog

Not registering and filing returns will have severe consequences and lead to fines and penalties.

Contracts

Ask your Accountant to review you contracts, they will be able to give you lots of useful tips.

Funding

Draw up a Budget and Cashflow and forecast how much cash you will need to run the business, looking at your cash cycle and managing it will be vital.

If you need funding ask your Accountant for help, they will be able to look at all the options and help you choose the option thats best for your business.

Accounting

Many start ups fail to keep control of their accounting, by working with an accountant you can avoid this problem and they can help you choose the best accounting solutions for your business.

steve@bicknells.net

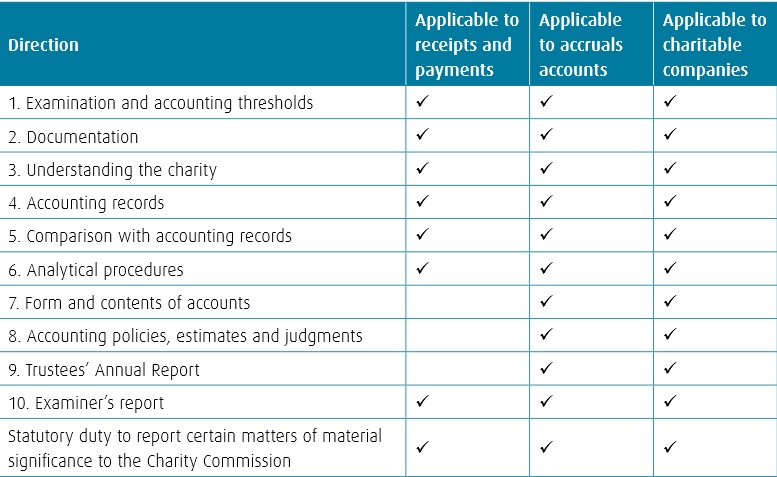

Are your charity accounts being correctly examined?

To maintain public confidence in the work of charities, charity law requires most charities (income over £10,000) to have an external scrutiny of their accounts. Provided a charity is not required by law or its governing document to have an audit then trustees may choose a simpler and less expensive form of external scrutiny called an independent examination.

Trustees may opt for an independent examination instead of an audit provided their charity’s gross income is not more than £500,000, or where gross income exceeds £250,000 its gross asset are not more than £3.26 million

Details in Charity notice CC31

Its estimated that approximately 90,000 UK charities require independent examination and that there are approximately 20,000 independent examiners.

The Charity Commission has a Framework in Notice CC32 to explain what the examiner needs to do

Common problems found by the charity commission include:

- The examiners report being signed by an organisation when in fact the must be signed by an individual

- Failing to address all the directives in the framework

- Insufficient scrutiny of the records

steve@bicknells.net