Home » Articles posted by Steve Bicknell (Page 24)

Author Archives: Steve Bicknell

How does Auto Enrolment Postponement work?

You can choose to postpone automatic enrolment for up to three months for some or all of your staff. You must write to your staff to tell them you’re postponing automatic enrolment for them. One of the times you can postpone is from your staging date.

Key points

- You can postpone automatic enrolment for up to three months from certain dates.

- If you postpone from your staging date, your staging date does not change.

- If you choose to postpone from your staging date, you must write to tell the staff who will be postponed within six weeks of your staging date.

Why Postpone?

- Its unlikely that your payroll processing period will match your staging date, most staging dates are the 1st of the month but many payrolls are weekly, it makes sense to start auto enrolment on a pay processing date

- If you have short term staff or you are a temp agency you will probably postpone in order to avoid unnecessarily assessing staff who will leave within the postponement period

- You may also postpone to reduce auto enrolment pension payments and admin

- You can choose any business reason

When can you postpone?

You can only postpone automatic enrolment from:

- your staging date

- a staff member’s first day of employment

- the date a staff member first becomes eligible for automatic enrolment.

If you postpone from your staging date, it doesn’t change your staging date.

Staff whose automatic enrolment you’ve postponed can choose to opt in to your pension scheme during the postponement period.

The Pension Regulator has further details

Don’t mess this up, if you don’t get postponement right…..

- You will get a Warning

- Followed by a penalty of £400

- Followed by fines of £500 to £2,500 per day (depending on the number of employees)

Even the smallest business will get fines of £50 per day!

steve@bicknells.net

You will initially be given a warning, which will be followed by a fixed penalty of £400. Not too severe so far, but then the penalties shoot up for those companies who still fail to comply.

If you employ between 50 and 249 employees the fine for on-going non-compliance is a whopping £2,500 per day. For businesses with fewer employees, between five and 49 the penalty is still £500 per day and even the smallest of businesses will be fined £50 per day.

I need an accountant for my business!

Often business owners wait too long before they realise that they need help from an accountant.

Key reasons are:

- They don’t understand the difference between a book keeper and an accountant

- They think an accountant will just be an extra cost – the reality is that most accountants will save the business many times their cost

- They think they accountants are just bean counters

But if you choose a qualified and experienced accountant they can bring huge benefits….

- Management tools to improve profitability

- Cost Controls

- Tax Savings

- Identifying Cash Flow needs and funding solutions

- Growth Strategies

- Business Planning

- Budgeting

- Business Structures

- Business Accounting and Reporting Systems

- Maximise Credit Scores to win more business

So don’t wait too long, getting an accountant should be a priority for all businesses!

steve@bicknells.net

Is an SME really exempt from the ‘Arms Length’ inter company pricing?

You might think you can charge related companies whatever you want, but is that true?

First a quick lesson in Transfer/Internal Pricing ….

SME’s do have tax exemptions….

There’s an exemption that will apply for most small and medium sized enterprises. The conditions attached to this exemption can be found in HMRC’s International Manual.

A business is a ‘small’ enterprise if it has no more than 50 staff and either an annual turnover or balance sheet total of less than €10 million.

A business is a ‘medium sized’ enterprise if it has no more than 250 staff and either an annual turnover of less than €50 million or a balance sheet total of less than €43 million.

There are some exceptions:

- Transactions with Parties in Non Qualifying territories

- Where HMRC have issued a notice to Medium Sized enterprise

- Election to remain subject to transfer pricing rules

- Patent Box

steve@bicknells.net

65% of SME’s rejected for a loan want to try alternatives… would you

A government consultation ended last week into whether legislation should force banks to refer rejected loans to alternative sources of finance.

At present the largest four banks account for over 80% of UK SMEs’ main banking relationships. Many SMEs only approach the largest banks when seeking finance. Although a large number of these applications are rejected – in the case of first time SME borrowers the rejection rate is around 50% – a proportion of these are viable and are rejected simply because they don’t meet the risk profiles of the largest banks. There are often challenger banks and alternative finance providers with different business models that may be willing to lend to these SMEs.

Although the largest banks will sometimes refer these SMEs on, in many cases challenger banks and other providers of finance are unable to offer finance as they are not aware of their existence and the SMEs are not aware of the existence of these alternative sources of finance.

SME’s most trusted advisors are Accountants, according to Accountancy Age a fifth of SME’s are more open with their accountant than their bank manager and half believe that their Accountant is the most valuable source of business advice and just under half turn to their Accountant first for advise.

So why aren’t banks working more closely with accountants? I think its because its hard to work with individual accountants and build multiple relationships, its much easier to work with groups of accountants on a national basis such as www.business-accountant.com

Would you ask your accountant if you were looking for finance?

steve@bicknells.net

Why do I need a Forensic Accountant?

Forensic accountants are called upon to help in many situations:

- Shareholder and partnership disputes

- Divorce Cases – assessing assets and liabilities

- Professional Negligence claims

- Personal Injury Claims

- Insurance Claims – Business interruption and loss of profit

- Fraud Investigations

- Criminal Investigations

Often Solicitors will appoint Forensic Accountants and obtain quotes from several accountants before making a recommendation to their client.

CIMA Accountants are well suited to Forensic Accounting because of their business experience and analytical skills.

Divorce is a growth area for Forensic Accounting as its common for both parties to value assets and liabilities in different ways, to resolve this in some cases accountants will be jointly appointed by both parties.

The process is normally as follows:

- The Solicitor issues instructions to the Accountant

- The Accountant reads the brief, investigates the information supplied and searches for undisclosed information (for example Land Registry, Companies House, Internet etc)

- The Accountant requests further information via the solicitor

- Appropriate calculations are carried out

- A report is prepared which can be presented to the Court

steve@bicknells.net

What are Qualifying Earnings for Auto Enrolment?

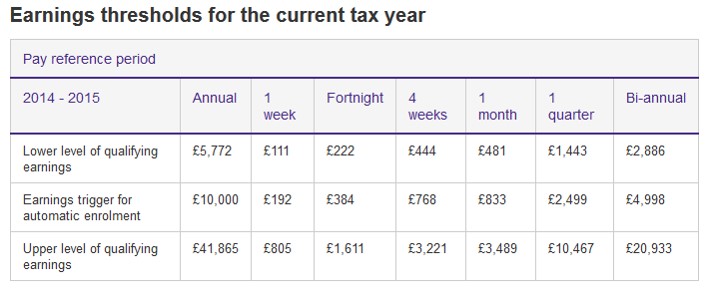

These are defined as sums which you pay to an employee in connection with his or her employment. They can be salary, wages, commission, bonuses, overtime. Statutory sick pay and maternity/paternity/adoption pay are included too. Benefits in kind (known as P11D benefits), for example, car and fuel, and tips and gratuities do not have to be included. In 2014/2015 Qualifying Earnings are earnings between £5772 and £41,865.

Employers are only required enrol employees earning over the Earnings Trigger of £10,000 (subject to age criteria) but employees can opt in once they earn above the lower level. According to Payroll and Benefits Magazine...

The AE process can be very administration-heavy and, unlike Real Time Information, employees and workers will have to be continually assessed. For example, employers will need to continuously monitor their workforce to identify when a jobholder must be automatically enrolled. In particular, the employer will need to monitor a worker’s age because this may trigger AE and opt-in activity.Although small employers will need at least six months before their staging date to prepare for AE, larger ones may need between 12 and 18 months.AE does not only apply to employees, but also to workers, including contractors who provide services on a personal basis but not as a company.

Can you cope with Auto Enrolment?

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was.

58% had not set up an auto-enrolment pension scheme.

90.5% of employers without an auto-enrolment pension scheme hadn’t even started researching one.

If you think you can ignore Auto Enrolment, think again, The Pensions Regulator will make you comply……..

Non-statutory action

We can issue guidance and instruction by telephone, email, letter and in person. Or we can send a warning letter confirming a set time frame for compliance with the duties.

Statutory notices

Statutory notices can direct you to comply with your duties and / or pay any contributions you have missed or are late in paying. We have further discretionary powers which allow us to estimate and charge interest on unpaid contributions and direct you to calculate and / or pay unpaid contributions.

Penalty notices

We can issue penalty notices to punish persistent and deliberate non-compliance.

A fixed penalty notice will be issued if you don’t comply with statutory notices, or if there’s sufficient evidence of a breach of the law. This is fixed at £400 and payable within a specific period.

We can also issue an escalating penalty notice for failure to comply with a statutory notice. This penalty has a prescribed daily rate of £50 to £10,000 depending on the number of staff you have.

We can issue a civil penalty for cases where you fail to pay contributions due. This is a financial penalty of up to £5,000 for individuals and up to £50,000 for organisations.

Where employers fail to comply with a compliance notice or there is evidence of a breach, we can issue a prohibited recruitment conduct penalty notice. This is currently set at a maximum fixed daily rate of £5,000 for organisations with over 250 staff. We aim to fully recover all the penalties that we issue.

Court action

We can take civil action through the court to recover penalties.

Employers who deliberately and wilfully fail to comply with their duties may be prosecuted.

We can also confiscate goods where there is a criminal conviction and restrain assets during criminal investigations.

The first case was Dunelm http://www.thepensionsregulator.gov.uk/docs/section-89-dunelm.pdf

Research shows that Accountants are most likely to be asked to help SME’s and Business Accountant (a service provided by CIMA Members in Practice) have created a booking service to assist SME’s in getting help https://business-accountant.com/auto-enrolment/

So don’t be scared by Auto Enrolment, don’t delay drawing up a project plan, take action now to avoid problems with the Pension Regulator later!

steve@bicknells.net

Would your Suppliers like to be paid faster?

Yes of course they would, silly question, everyone wants to be paid faster but how can it be done?

Santander may have the answer, they are offering a facility to SME’s called Supplier Payments and its part of the Funding for Lending Scheme.

Supply Chain Finance has been around for a while, this an extract from an article in the Telegraph in October 2012

Supply-chain finance, which is sometimes known as “reverse factoring”, allows big businesses to notify a bank as soon as a supplier’s invoice has been approved. The bank, armed with the assurance the bill will be paid, will then extend a full, immediate advance of the bill to the supplier at a low interest rate.

The Prime Minister hailed the technique as “win-win” because large companies get greater protection from small suppliers going bust, while the small business avoids having to wait for payment and, since the invoice is approved, avoids any risk of non-payment.

Most of the main banks have solutions for large businesses but it isn’t normally available to SME’s.

Is this an option for your suppliers?

steve@bicknells.net

When will my business Stage for Auto Enrolment?

Your staging date is the date the new duties come into force for your business. It’s the date from when automatic enrolment activities must become ‘business as usual’, just like real-time PAYE.

You can find out your staging date using the Pension Regulators Calculator or this link provides a quick summary by number of employees.

Auto Enrolment isn’t easy, there is a lot to do before you Stage, here is a checklist (Pension Regulator) of activities you should do 6 months before Staging

Modified staging dates for some small employers

- You can change your staging date to a later date if you:

- had fewer than 50 staff on 1 April 2012, and

- had, or were part of, a PAYE scheme that has more than 50 people in it.

Bringing your staging date forward

All employers are able to bring their staging date forward. You may choose to do this to align it with other business practices, like the start of your financial year.

Or you might have several employers in a corporate group and want to align the smaller employers’ staging dates with the largest. If you plan to do this, you must notify The Pensions Regulator, which you can do online.

You can postpone assessing your workforce for up to 3 months, but this does not change your staging date and staff can choose to opt in during the postponement period.

A survey by AutoenrolSME found that 6 out 10 businesses can’t cope with the preparation for Auto Enrolment and hired additional staff to manage the process!

A Poll in April 2014 of 200 businesses with 62 to 249 employees found:

63% of the employers didn’t know when their staging date was!

Do you have a Second Income? own up now!

On the 9th April 2014 HMRC launched the Second Income Campaign….

A second income could come from:

- consultancy fees, eg for providing training

- organising parties and events

- providing services like taxi driving, hairdressing or fitness training

- making and selling craft items

- buying and selling goods, eg at market stalls or car boot sales

You need to tell HM Revenue and Customs (HMRC) if your additional income hasn’t been taxed through either:

- your main job

- another Pay As You Earn (PAYE) scheme

- Self Assessment

This is called a ‘voluntary disclosure’. To get the best possible terms you need to tell HMRC that you want to take part in the campaign.

You’ll have 4 months to calculate and pay what you owe.

You can find out about the campaign and how to make a disclosure here

The criteria used to assess if an activity is a hobby or a business are:

- The size and commerciality of the activity.

- The frequency of the activity and transactions

- The application of business principles.

- Whether there is a genuine profit motive.

- The amount of time devoted to the activities.

- The existence of arm’s-length customers (as opposed to just selling your wares to family and friends).

If you have a Second Income its better to disclose it now rather than wait till HMRC find you.