Home » Posts tagged 'Tax' (Page 6)

Tag Archives: Tax

Karren likes the Employment Allowance – £2000 will be very NIC(E)

This is what Karren Brady said…..

She has a point, £2,000 will be a big help to many SME’s.

The Employment Allowance is available from 6 April 2014. If you are eligible you can reduce your employer Class 1 NICs by up to £2,000 each tax year.

You can claim the Employment Allowance if you are a business or charity (including Community Amateur Sports Clubs) that pays employer Class 1 NICs on your employees’ or directors’ earnings.

If your company belongs to a group of companies or your charity is part of a charities structure, only one company or charity can claim the allowance. It is up to you to decide which company or charity will claim the allowance.

You can only claim the £2,000 Employment Allowance against one PAYE scheme – even if your business runs multiple schemes.

You cannot claim the Employment Allowance, for example if you:

- employ someone for personal, household or domestic work, such as a nanny, au pair, chauffeur, gardener, care support worker

- already claim the allowance through a connected company or charity

- are a public authority, this includes; local, district, town and parish councils

- carry out functions either wholly or mainly of a public nature (unless you have charitable status), for example:

- NHS services

- General Practitioner services

- the managing of housing stock owned by or for a local council

- providing a meals on wheels service for a local council

- refuse collection for a local council

- prison services

- collecting debt for a government department

You do not carry out a function of a public nature, if you are:

- providing security and cleaning services for a public building, such as government or local council offices

- supplying IT services for a government department or local council

Personal and Managed Service Companies who pay contract fees instead of a wage or salary, may not be able to claim the Employment Allowance, as you cannot claim the allowance for any deemed payments of employment income.

Service companies can only claim the allowance, if you pay earnings and have an employer Class 1 NICs liability on these earnings.

You can use your own payroll software (see your software provider’s instructions), or HM Revenue and Customs’ (HMRC’s) Basic PAYE Tools to claim the Employment Allowance.

When you make your claim (using the software of your choice), you must reduce your employer Class 1 NICs payment by an amount of Employment Allowance equal to your employer Class 1 NICs due, but not more than £2,000 per year.

You can read the full guidance here

Will the Employment Allowance be NICE for your business?

steve@bicknells.net

Have you claimed capital allowances on your building? time is running out…

FA2008 introduced a new classification of integral features of a building or structure, expenditure on the provision or replacement of which qualifies for WDAs at the 10% special rate. The new classification applies to qualifying expenditure incurred on or after 1 April 2008 (CT) or 6 April 2008 (IT).

http://www.hmrc.gov.uk/manuals/camanual/CA22300.htm

The rules on integral features apply where a person carrying on a qualifying activity incurs expenditure on the provision or replacement of an integral feature for the purposes of that qualifying activity. Each of the following is an integral feature of a building or structure –

- an electrical system (including a lighting system),

- a cold water system,

- a space or water heating system, a powered system of ventilation, air cooling or air purification, and any floor or ceiling comprised in such a system,

- a lift, an escalator or a moving walkway,

- external solar shading

Only assets that are on the list are integral features for PMA purposes; if an asset is not one of those included in the list, the integral features rules are not in point.

However, Plant and Machinery includes….

other building fixtures, such as shop fittings, kitchen and bathroom fittings

Many businesses have never claimed capital allowances for these items.

Paragraph 13 of Schedule 10 FA2012 introduced transitional provisions for making claims.

The provisions mean that where the current owner incurs expenditure on acquiring fixtures from a past owner before 1 (or 6) April 2014 and the past owner has not claimed allowances or pooled their expenditure in respect of a qualifying fixture, the current owner may claim PMA on the part of the price the paid which is attributable to that fixture….. CA26470

It is possible for the buyer to use apportionment of the sale price (usually done by an RICS Surveyor) to determine the value of the fixtures. But this risks clawback of balancing charges for the seller.

A alternative option is to claim a Section 198 election which can be entered into within 2 years of the date of the property sale. It must be signed by the buyer and the seller and must identify the items covered. The elected value can be between £1 and the price paid, but makesure you undertand the implications of the price choosen.

As a Section 198 requires agreement you may wish to take legal advice.

The Section 198 needs to made in writing to HMRC.

The following can’t claim a Section 198:

- Property Traders

- Developers

- Pension Funds

- Charities

But if you can claim you need to claim now as there are only a few weeks left until April 2014.

steve@bicknells.net

First there was Fair Trade, now there is Fair Tax……

![]()

The Fair Trade Mark is now common place on goods we buy ensuring that workers aren’t exploited, but now there is a new mark, the Fair Tax Mark.

The Fair Tax Mark Criteria assess the quality of a business’ publicly available information on key tax and transparency issues. In this context, publicly available information primarily means a full set of accounts available to all via Companies House or the company website. However, it can also include the company website and/or any other freely available printed material.

For every business type, the criteria are divided into two main categories that assess a business on:

-

Transparency

-

Tax rate, disclosure and avoidance

Will your business be applying to use the Fair Tax Mark? would you buy more from a business that uses the Mark?

steve@bicknells.net

How changing your year end can help cash flow

Basically if your company makes a loss you carry it forward.

The amount of trading loss available to be carried forward is the loss sustained less any loss relieved in the current year or surrendered as group relief.

Carry forward a corporation tax loss is automatic, therefore as no claim is required there is no time limit.

The legislative reference for a trading loss carried forward is: CTA 2010 s45) [old reference ICTA 1988 s393(1)].

You can also make a claim to carry a loss back 12 months.

The legislative reference for carry back loss relief is: CTA 2010 s37(s)(b)(6)(8) and s38 [old reference ICTA 1988 s393A(1)(b)(2)-(2C)].

But there is another option, to help improve your cash flow, lets say you have been making profits and you have just come to the end of your accounting period, the next few months are going to be tough and you will make a loss. If you change your year end by extending it or having a shorter period you could help your cash flow.

Corporation Tax is payable 9 months and 1 day after your year end, so you will have a return for 12 months and have tax to pay but if you had a 6 month return to follow it you could reduce the time before you claim relief for the loss.

If you extended your accounting period to 18 months the figures might even look better for credit rating.

You can shorten as much as you want but not beyond the start date of the accounting period being changed.

You can only extend once every 5 years.

See the Companies House Checklist for details

steve@bicknells.net

Will HMRC help you get over the Floods?

Will it ever stop raining!

But help is at hand, HMRC launched their helpline (12/2/14)

The helpline will enable anyone affected to get fast, practical help and advice on a wide range of tax problems they may be facing.

HM Revenue and Customs (HMRC) will also:

- agree instalment arrangements where taxpayers are unable to pay as a result of the floods;

- agree a practical approach when individuals and businesses have lost vital records to the floods;

- suspend debt collection proceedings for those affected by the floods;

- cancel penalties when the taxpayer has missed statutory deadlines.

The helpline is in addition to other HMRC telephone contact numbers.

The helpline is 0800 904 7900. Opening hours are Monday to Friday, 8.00 am to 8.00 pm; Saturday and Sunday, 8.00 am to 4.00 pm, excluding bank holidays.

I hope the weather improves soon and your business can keep going and survive the storms.

steve@bicknells.net

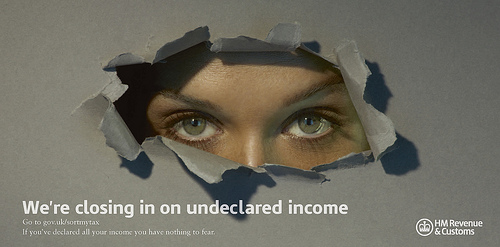

How HMRC use IT systems to seek out tax evaders

There is no doubting the resolve of HMRC to track down and prosecute tax evaders.

The Government has committed to spend £917m to tackle tax evasion and raise an additional £7bn each year by 2014/15.

HMRC are using 2,500 staff to tackle avoidance, evasion and fraud, there is also a website to help those who want to declare income https://www.gov.uk/sortmytax

In the search for tax evaders, HMRC have a £45m computer system called Connect which in 2011 delivered £1.4bn in tax revenue and the system is getting bigger and better all the time. According to Accounting Web:

It uses a mathematical technique to search previously unrelated information and detect otherwise invisible ‘relationship’ networks. Using Connect, HMRC sifts through information on property transactions at the Land Registry, company ownerships, loans, bank accounts, employment history, voting and local authority rates registers and compares with self-assessment records to spot taxpayers who might be under-declaring or not declaring income.

Last year Connect made links between tax records and third party data from hospitals, pharmaceutical companies, insurers and even gas SAFE registrations. DVLA records and the shipping and Civil Aviation Authority registers help identify owners of cars and planes who declare income that the computer suggests cannot support such purchases.

In addition HMRC have also identified 200 accountants, lawyers and professionals who advise on tax avoidance structures and its currently unclear how HMRC will be dealing with them and their clients.

It is important to remember that most people pay the correct tax, in fact HMRC calculate that 93% of tax due is paid correctly, its only a small minority who try to evade tax.

steve@bicknells.net

5 ways to reduce the risk of a tax investigation

THE TAX YIELD derived from HM Revenue & Customs investigations into the affairs of small- and medium-sized companies rose by 31% over the last 12 months, according to UHY Hacker Young.

Compliance investigations into SMEs generated £565m for HMRC in 2012/13, up from £434m in 2011/12, with the year ending March 31. Accountancy Age

Some investigations are random and some as a result of HMRC task forces, but many are triggered by risk profiling.

What can you do to reduce your chances of being selected:

1. File your tax returns on time and pay what you owe – If you file late or at the last minute HMRC will think you are disorganised and as such there are more likely to be errors in the return

2. Declare all your income – HMRC get details of bank interest and other sources of income, sometimes they test them and match them to returns

3. Use an accountant – Unrepresented taxpayers are more likely to be looked at, mainly because many of them don’t know what they are doing

4. Trends – if your business doesn’t match the profile of similar business in the same sector or your results suddenly fluctuate it could raise concerns at HMRC, for example, if you suddenly request a VAT refund

5. Tax Avoidance Schemes – if you are using a tax avoidance scheme I am sure HMRC will be looking closely, if they can find a way to challenge the scheme then at some point they will

steve@bicknells.net

HMRC demand payment from Landlords

HMRC launched the ‘Let Property Campaign‘ on the 10th December 2013.

If you’re a landlord who has undisclosed income you must tell HMRC about any unpaid tax now. You will then have 3 months to calculate and pay what you owe.

The Let Property Campaign is an opportunity open to all residential property landlords with undisclosed taxes. This includes:

- those that have multiple properties

- landlords with single rentals

- specialist landlords with student or workforce rentals

- holiday lettings

- anyone renting out a room in their main home for more than £4,250 per year, or £2,125 if the property was let jointly, but has not told HMRC about this income

- those who live abroad or intend to live abroad for more than 6 months and rent out a property in the UK as you may still be liable to UK taxes

According to the Telegraph….

Fewer than 500,000 taxpayers are registered with HMRC as owning properties other than their home. And yet other sources put the number of Britain’s growing army of landlords at between 1.2million and 1.4million.

Why the discrepancy? No one can say for sure, but the taxman has his answer: not enough people are declaring – and paying tax on – their property incomes and gains.

HMRC will identify those who they believe should have made a disclosure by:

- comparing the information already in their possession with customers’ UK tax histories

- continuing to use their powers to obtain further detailed information about payments made to and from landlords

Where additional taxes are due HMRC will usually charge higher penalties than those available under the Let Property Campaign. The penalties could be up to 100% of the unpaid liabilities, or up to 200% for offshore related income.

If you owe tax, you must tell HMRC of your intention to make a disclosure. You need to do this as soon as you become aware that you owe tax on your letting income.

At this stage, you only need to tell HMRC that you will be making a disclosure.

You do not need to provide any details of the undisclosed income or the tax you believe you owe.

steve@bicknells.net

Are you coding your VAT entries correctly?

When you enter transactions its important to use the right tax code otherwise your VAT returns are likely to either need adjustment or contain errors, but often when entering transactions your software won’t tell you what the codes mean, here is a list of Sage codes:

| T0 | Zero rated transactions |

| T1 | Standard rate |

| T2 | Exempt transactions |

| T4 | Sales of goods to VAT registered customers in EC |

| T5 | Lower rate |

| T7 | Zero-rated purchases of goods from suppliers in EC |

| T8 | Standard-rated purchases of goods from suppliers in EC |

| T9 | Transactions not involving VAT |

| T20 | Sales and purchases of reverse charges |

| T22 | Sales of services to VAT registered customers in EC |

| T23 | Zero-rated purchases of services from suppliers in EC |

| T24 | Standard-rated purchases of services from suppliers in EC |

| T25 | Flat rate accounting scheme, purchase and sale of individual capital items > £2,000 |

There are different rates of VAT, depending on the type of goods or services your business provides. At the moment there are three different rates. They are:

- standard rate – 20 per cent

- reduced rate – 5 per cent

- zero rate – 0 per cent

You can check which rate to use on the HMRC Website http://www.hmrc.gov.uk/vat/forms-rates/rates/rates.htm

UK supplier who aren’t VAT registered would use T9 in Sage.

steve@bicknells.net

Garden bagging – profit from property development in your back yard

The rate of new housing required to meet demand in England is now estimated at between 240,000 and 245,000 units a year, an increase of 10,000 new homes annually on previously accepted figures.

Gazumping and other nasties that flourished in the last property boom are making a return, as competition for homes increases with the bringing forward of the second phase of Help to Buy.

So now could be the time to sell off your garden:

- Its a way of building homes without building on the Green Belt

- It can be a zero risk way to make money if you sell the plot

Garden Bagging works as follows:

- Home Owners with suitable land approach a local builder

- The builder buys the right to seek planning permission for a nominal fee

- If the application is successful the builder will pay up to 85% of the open market value of the consented plot less his costs

Alternatively you could develop the plot yourself for a typical self build its estimated that 35% would be the land cost, 40% build cost and 25% profit margin.

steve@bicknells.net