Home » Posts tagged 'Tax' (Page 3)

Tag Archives: Tax

Sole Traders lose Goodwill Tax Relief

Since 6th April 2008 and until 3rd December 2014 Sole Traders and Parternships were able to claim Entrepreneurs Tax Relief on Goodwill when becoming a Limited Company.

Until the 3rd December 2014 they would claim there Capital Gains Allowance

| Period | Tax-free allowance |

|---|---|

| 5 April 2013 to 6 April 2014 | £10,900 |

| 5 April 2014 to 6 April 2015 | £11,000 |

Then claim ER which reduced the rate of tax to 10% on the gain.

But from the 3rd December they will now pay Capital Gains at the normal rates of CGT which are 18% or 28% (for Higher Rate Income Tax Payers).

This doesn’t change the potential ability of the company to offset goodwill against their Corporation Tax Return.

There are still other benefits related to goodwill as explained in this blog

The tax benefits of goodwill on incorporation?

steve@bicknells.net

The Yacht that wasn’t a benefit in kind

This is the case of Gillian Rockall v HMRC (2014) HKFTT 643.

Mr Michael & Mrs Gillian Rockall were involved in running a hotel and conference centre and providing high-end residential courses, amongst the companies assets was a 140 foot ocean-going yacht costing $11.9 million called Masquerade of Sole.

HMRC issued assessments on Mr & Mrs Rockall for the tax years 2000-2001 to 2008-2009 on the basis of personal use (benefit is normally assessed as 20% of the market value).

The Yacht was used for:

- Business Networking

- Customer Training

- Exploring Business Opportunities in the Caribbean and Mediterranean

- Friends and Acquaintances were taken on occassional trips to provide a opinion on opportunities

The Yacht was also placed with an agent for charter when not required for the purposes above.

The First-Tier Tribunal took the view that the use of the Yacht was only for Business and not for private purposes.

However under S203 ITEPA 2003 a benefit in kind would arise because the asset was at the disposal of the employees.

The Rockalls appealed to the First-Tier Tax Tribunal, on the grounds that the use of the yacht was tax-deductible under s365 of the Income Tax (Earnings and Pensions) Act 2003 (ITEPA). This requires that the item comprising the benefit in kind was used ‘wholly, exclusively and necessarily in the performance of the duties of the employment’.

The tribunal has now ruled that the yacht was bought and operated purely for business purposes and thus was fully tax-deductible for both the Rockalls.

– See more at: http://www.step.org/yacht-used-impress-customers-were-legitimate-expense#sthash.dNRhVYmG.dpuf

Why working with accounting is about to get so much better

Anyone who works with businesses is fully aware of how important accounting is for the success of a company. Yet many business owners have a negative attitude towards accounting. A high percentage of entrepreneurs see accounting as a necessary evil and often a hindrance to starting a new company.

How is that possible? Wasn’t accounting invented to help companies manage their business?

The IT industry has brought us computers and the ability to create software to automate bookkeeping. While there is no doubt that accounting software has been a great help, when we look at the usage of it, something is wrong. More than half of the businesses in the UK keep track of their finances by using a combination of spreadsheets and word processors rather than using accounting software. In an age where computing power is ubiquitous and virtually never too far from our pocket, we should be able to do better than this.

In 2013, international accounting software provider e-conomic was considering what its next generation accounting software should look like. And decided to take a different approach. What would happen if we created a piece of accounting software for people who had no knowledge of accounting? And what if we made the basic functions free for people to use? We hoped that it would make accounting approachable by virtually anybody.

That’s how the Debitoor invoicing and accounting software was born.

Introducing simple accounting to the world

Today, more than 33,000 people in the UK and almost 300,000 people worldwide have signed up for Debitoor and have given us the privilege of approaching accounting in a different way. Debitoor is used in more than 30 countries, from the UK to South Africa, from Colombia to Australia and New Zealand.

Debitoor is an accounting package for very small businesses. It allows them to manage their customers, create quotes and invoices. It allows them to register their purchases, deal with bank and payments and helps them report their VAT directly to HMRC at the click of a button. Debitoor helps those small companies manage their assets and keep track of what’s on their balance sheet in a very simple manner. Finally, Debitoor helps business owners collaborate with their accountants by allowing them to share their data with them.

Debitoor’s mission is to make accounting cool to work with. Two years after we started, the typical reaction we get from accountants is: “Wow, convincing my clients to use this is going to be super easy!”. We have captured the essence of Debitoor in this video.

Letting users shape accounting software

But what have we done to make this possible? The most important ingredient has been a clear focus. Our mission has always been to make accounting easy for small business owners who know very little about accounting.

Here are some of the key principles we followed to build the Debitoor invoicing and accounting software:

– Approachable: We have removed any obstacles to getting started. There is no setup needed, we do not ask questions, users can start on the free package, the program is ready to go.

– Natural: We have eliminated all technical lingo. You will not find the words “debit” and “credit” in Debitoor. The workflows in the program follow the natural flows of a user with no accounting knowledge and the program uses the typical words he’d use.

– Forgiving: People make mistakes; and accounting systems typically make it quite complicated to correct mistakes. In Debitoor, actions can be undone and mistakes can easily be corrected.

– Instructive: We assume people do not know much about accounting, so we have structured the entire program to let users learn along the way. This is not just functionality but it encompasses the entire packaging of the product.

– User-driven: In an open forum, users can give their feedback and suggest new features, vote for their own or others’ suggestions and influence the further development of the software. This transparency is super important for us to develop a truly user-driven program.

– Collaborative: Most of our users share their data with their accountants in order to get help with taxes, reporting and ensuring quality.

We also had the privilege of building the product with the technology which was available in 2013. This has huge benefits for our users because it allows us to provide them with a service which is reliable, improving at a fast pace and very secure. Having a modern architecture also ensures that Debitoor is very easy to connect to other popular cloud services.

Debitoor’s user base is very diverse as its appeal is quite broad. Many of our users are freelancers, artists, consultants, designers or other creative people, but we have also small artisans and shop keepers or owners of clinics and small distributors. They all have missions and purposes in their lives and we try to help them with their accounting.

Check out the stories of Felicia Matheson from Prohibition Drinks in Newscastle, Northern Ireland and the story of Esther from The Roasting Shed in London.

Changing how an industry works

As with any change in technology, this brings great opportunities to the industry it affects. The introduction of new technology, however, takes a bit of time to mature. When television started to gain mass adoption in the 1950s, broadcasters used it as it was radio. The first shows had older men with glasses reading papers in front of a microphone. This was how it used to be with radio programs.

The availability of cloud software has created a set of providers who simply made traditional accounting software available on the internet. This, we believe, will change and we will see more and more software which is transformational in nature. That is what we are trying to do with Debitoor.

We are only at the beginning of this journey. The roadmap for Debitoor will focus on three main aspects:

1. Continue to add simple flows to support what today are very difficult accounting scenarios

2. Introduce more and more automation and intelligence to enable our users to do more with less knowledge

3. Strengthen the collaboration between users and their accountants by facilitating the sharing of data between them.

What will this mean for accountants and the accounting industry? This is what our users are telling us: They love doing their invoices and keeping track of their costs in Debitoor. It gives the nice feeling of being in control, it keeps them organized and allows them to focus on their business going forward.

At the same time, they also tell us that they need help from their accountants. They need help with taxes, they need help with reporting to authorities and a lot of them need a quality check from the experts. In addition, most of them need legal and financial advice on ad hoc issues they encounter in their life as entrepreneurs.

The biggest change for accountants is to be prepared to embrace the possibilities that technology gives us. Things like cloud storage and online applications will substitute manual processes, paper and data disks. Everything is now available via a web browser on your computer or on your phone.

In order to be successful, accountants will have focus on services that draw on their knowledge and experience and they will need to be prepared to serve their customers as they move towards those new technologies.

Increased access will not be limited to technology but also to services. This will also mean increased competition. The best thing an accountant can do is embrace change and be ahead of the curve, start small but start early. The customers are already going there.

10 ways save tax on your Self Assessment Tax Return

It’s Self Assessment season, most people who are required to do self assessment will submit their returns in December and January.

You must always send a tax return if you’re:

- a self-employed sole trader

- a partner in a business partnership

- a company director (unless it’s for a non-profit organisation, eg a charity, and you don’t get any pay or benefits, like travel expenses or a company car)

- Don’t miss the deadline of 31st January or you will get penalties and interest

- If you are new to Self Assessment makesure you get your HMRC log in details early and know your NI and UTR numbers otherwise you won’t be able to file online which could lead to penalties

- Claim all your expenses for example a self employed worker will claim for travel , protective clothing (PPE), home office expenses

- Don’t forget Pension Contributions if the tax hasn’t been claimed by your pension provider or you are a higher rate tax payer

- Don’t forget Donations to Charity if you are a higher rate tax payer

- Have you included out of pocket expenses for example parking

- If you are employee could you claim a tax allowance for clothing?

- Does your company pay mileage below the HMRC rates, you could claim a tax allowance on the difference

- Check you have all your motoring expenses included

- Makesure you have claimed all your costs on Buy to Let

steve@bicknells.net

What is the Foster Care Allowance?

All Foster Carers are classed as Self Employed and can choose whether to be taxed using one of two methods – the Simplified or Profit methods.

Simplified Method

This is the most common method.

Your ‘qualifying amount’ for a tax year consists of two parts:

- Your Annual Fixed Amount per household of £10,000

- Plus your Weekly/Part Week Amount of £200 (under 11 years old) or £250 (over 11 years old)

If your income exceeds this level under the Simplified Method your are taxed on the difference.

Profit Method

This method works best if you have high expenses, to use this method you need to keep detailed records of all your expenses including capital expenditure.

Using the Profit Method you don’t use the allowances but prepare detailed accounts on which you are taxed.

National Insurance

Foster Carers are subject to Class 2 and Class 4 National Insurance.

Further details are in HMRC Helpsheet 236

steve@bicknells.net

Is your act theatrical enough to have tax deductible agents fees?

Actors, singers, musicians, dancers and theatrical artists are permitted to make a deduction for agents fees under ITEPA 2003 S352.

But its more complicated than you might think based on recent cases…

Richard Madeley and Judy Finnegan (2006) SpC 547 it was only on appeal that the Special Commissioner agreed that their chat show was considered theatrical.

The Special Commissioners also thought that Bruce Forsyth and Ant and Dec qualified.

But that Quiz shows were borderline, for example they felt Jeremy Paxman (University Challenge) and John Humphry (Mastermind) didn’t qualify, but Anne Robinson (The Weakest Link) did qualify and Chris Tarrant (Who wants to be a Millionaire) was borderline.

So do you think the special commissioners would see your act as Theatrical?

steve@bicknells.net

Pool Cars – Do you have a ‘no private use’ Policy?

The latest case Vinyl Design Ltd v HMRC [2014] TC 03345 highlights why policies and mileage records are important.

Here are the facts of the case:

- The company’s only 2 employees were the directors

- They had different cars for private use

- They argued the Pool car was only for Business Use

- They had no policy

- They had no Mileage Records

- Pool Cars kept at home due to risk of vandelism

Not surprisingly HMRC won the case !!

So what should you do to prove there is no private use:

- Keep the car on the company’s business premises

- Keep the keys at the company’s business premises

- Prepare a Board Minute

- Make sure your contract of employment bans private use

- Keep a mileage log

- Insure the car principally for business use

HMRC have specific rules on keeping vehicles at home in EIM23465

Even if you do meet the 60% rule you still have to prove ‘no private use’

steve@bicknells.net

The tax incentive to lend to Social Enterprises?

Social Investment Tax Relief (SITR) came in on 6th April 2014.

Individuals making an eligible investment at any time from 6 April 2014 can deduct 30% of the cost of their investment from their income tax liability for 2014/15 (or the relevant later year in which the investment is made). The minimum period of investment is 3 years.

The income tax and capital gain tax reliefs provide a substantial incentive for investors. To make sure new investment is directed to the organisations which need it most and to meet EU regulations, the investment and the organisation receiving it must meet certain criteria.

Organisations must have a defined and regulated social purpose. Charities, community interest companies or community benefit societies carrying out a qualifying trade, with fewer than 500 employees and gross assets of no more than £15 million may be eligible.

The tax relief is available on unsecured loans as well as shares.

So basically, if you are a basic rate tax payer using SITR will be better than Gift Aid.

Not only do you get the tax relief but if you give a loan it will be repaid (after 3 years).

steve@bicknells.net

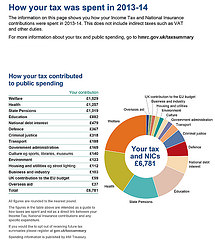

Have you had your annual tax statement?

Back in 2010 the Government promised every taxpayer an annual statement of their tax position – not just the income tax and National Insurance paid, but also where the money was spent.

During October these statement started to be sent out, see the example above.

If you’re registered for online self-assessment you’ll be able to access your statement digitally by logging on to the HMRC website in the usual format, selecting the tax summary option.

Initially the statements will only cover your tax position for 2012/2013 and at first only selected taxpayers will receive one.

Is this a positive step forward or a waste of time?

steve@bicknells.net

Why Doctors should use Salary Sacrifice for CPE

Doctors often agree to pay for their own continuing training personally because of a shortage of NHS funds but when they do pay for courses its unlikely they will be able to claim tax relief.

EIM32530 states that it is well established that employees are not entitled to an expenses deduction under Section 336 ITEPA 2003 for the expenses continuing professional education (CPE). The Commissioners and the Courts have traditionally held that the duties of trainee doctors, for the purpose of the expenses rule, are limited to the clinical work that they do for the NHS Trust by whom they are employed. Their training activities are not undertaken “in the performance of” those duties for the purpose of Section 336 . That is so even though the training activities may be compulsory, and failure to complete them may lead to the employee losing his or her professional qualifications, and/or their job.

The Commissioners and the Courts upheld that view in a number of cases, as follows:

Parikh v Sleeman (63TC75) – a hospital doctor was refused relief for the expenses of attending training courses during periods of study leave.

Snowdon v Charnock (SpC282) – a specialist registrar was refused relief for the expenses of undergoing mandatory personal psychotherapy.

Consultant Psychiatrist v CIR (SpC557) – an NHS consultant was refused relief for the expenses of CPE necessary to maintain her professional qualification.

Decadt v CRC (TL3792) – a specialist registrar was refused relief for the expenses of taking professional examinations, even though it was a condition of his employment that he should do so.

In the recent case of Revenue & Customs Commissioners v Dr Piu Banerjee ([2010] EWCA Civ. 843), the Court of Appeal accepted that a deduction for training costs incurred by an employee should be allowed if the employee was employed on a training contract where training was an intrinsic contractual duty of the employment (see also EIM32535 & EIM32546) and where any personal benefit, unlike most CPE courses, would be incidental and not therefore give rise to a dual purpose of the expenditure.

Salary Sacrifice solves this problem.

Salary sacrifice works particularly well for training because except in the most extreme cases, employees cannot claim a tax deduction for training costs that they pay personally but if the employer pays for training that is work-related:

- the employer gets the tax deduction

- the employee is not taxed on the cost and

- there is no National Insurance to pay.

EIM01210 confirms this.

steve@bicknells.net