Home » Posts tagged 'Tax'

Tag Archives: Tax

Don’t forget to deduct expenses – common expenses that you can set against your rental income

The Chancellor appears to have it in for landlords at the moment. There is the stamp duty land tax supplement of 3% on purchases of second and subsequent residential properties where completion is on or after 1 April 2016, the restriction in interest rate relief from April 2017 onwards, and the failure to benefit from the cut in capital gains tax from 6 April 2016.

In this harsher climate, it is perhaps worthwhile making sure you have not overlooked any deductible expenses when working out your profit for your property rental business.

Wholly and exclusively

The wholly and exclusively rule applies to determine whether an expense is deductible – if it has been incurred wholly and exclusively for the purposes of the property rental business, it passes this test.

Revenue not capital

A deduction against profits is only available if the expenditure is revenue in nature rather than capital. Broadly, revenue expenses are those incurred in the day-to-day running of the business. By contrast, capital expenditure is that incurred in purchasing or improving an asset, and would include costs of extending or improving the property, a fitted kitchen or expenditure on office equipment or vehicles. However, a deduction is available for replacement furnishings from April 2016.

Expenses checklist

The following is a list of common expenses that may be deducted when computing profits (as long as the wholly and exclusively test is met):

- interest on loans to buy the property (but not capital repayments);

- letting agents’ fees;

- accountants’ fees;

- legal fees for lets of a year or less or for renewing a lease of 50 years or less;

- utility bills (e.g. gas, electricity);

- buildings and contents insurance;

- cleaning costs;

- maintenance costs (but not improvements);

- costs of a gardener;

- telephone calls;

- stationery and postage;

- advertising;

- staff costs;

- ground rent and service charges; and

- council tax.

This list is not exhaustive.

Replacement of furnishings

From April 2016 a deduction is available for the costs of replacing furniture, furnishings, appliances (including white goods) and kitchenware. The amount of the deduction is the cost of the replacement item (capped at the cost of an equivalent to the item replaced if the replacement is superior to the original) plus any incidental costs of acquiring the new item (such as delivery) or disposing of the old item, less anything received for the old item.

This deduction replaces the 10% wear and tear allowance but, unlike the wear and tear allowance, is not limited to furnished lets.

Need to know: Make sure you have taken out all of your deductible expenses when working out the tax on your property rental income.

Dividend Tax – Good or bad news??

It’s early March and spring is in the air. The spring flowers are coming out into bloom – our garden is filled with snowdrops and daffodils. But then again last week we couldn’t see them because of snow! The start of spring though means not just the end of winter but also the end of one tax year and the start of another. This year, on the 6th April, though brings with it the start of a brand new tax – the dividend tax.

You may have seen lots of hype, but just what is it all about. For many of you David or I will already have had a chat, but we wanted to put a few thoughts down on paper for you!

Let’s have a brief look at what it’s all about.

What are the changes?

Change 1 –Grossing up of dividends is scrapped (believe it or not this little change is good news)

Currently all net dividends (this is same as the cash you receive) are grossed up by 100/90 before they are taxed. The 10% difference is a tax credit which is added to reflect the fact that the company paying the dividend has already paid corporation tax. Don’t worry if you don’t get this what it really means for most of us is that this ‘adjustment’ has the effect of reducing how much in terms of dividends taxpayers can really earn before they go into a higher tax band.

So for many company shareholder/directors the scrapping of this rule is good news as it

- Removes an area of tax which many tax payers find confusing as they grapple with gross and net dividends.

- It increases how much cash dividends they can take before they fall into a higher tax band.

Change 2 – Dividend Tax (This is the bad news for most Small & Micro business owner’s)

This new tax is applied to dividend income received in a year which is more than £5,000. The two groups of taxpayers who will be affected and therefore pay more tax in 2016/17 than they did in 2015/16 are:-

- Company directors who take a modest a salary and the rest of their income as dividends

- Taxpayers who have sizeable share portfolios which generate sizeable amounts of income

And when is an allowance not really an allowance?

Everyone will be entitled to a £5,000 tax free dividend allowance. This sounds very generous – after all its tax free. Well it’s not generous and that’s because it’s not really an allowance it’s a new 0% tax band has been created. The net result, is that it reduces a taxpayer’s basic rate tax band.

How much more tax could I pay?

Let’s have a look at the numbers (well I am an Accountant). This should make it easier to understand how the changes are likely to affect you!

The following table summarises the extra income tax which will be payable next year (2016/17) compared to this year (2015/16). Or put in simple terms for any Dividends you take from 6th April 2016 onwards!

| Cash Dividend | 2015/16 Tax | 2016/17 Tax | Increase |

| £ | £ | £ | £ |

| 15,000 | 0 | 455 | 455 |

| 30,000 | 0 | 1,655 | 1,655 |

| 50,000 | 4,777 | 6,920 | 2,143 |

| 75,000 | 11,027 | 15,045 | 4,018 |

| 100,000 | 20,843 | 24,615 | 3,772 |

The dividend tax is particularly punitive for the many family owned businesses where both the shares and income is split between both the husband and wife. In these cases the tax increases (as shown above) are doubled. So now coupled with increased operating costs in your business as a result of Auto Enrolment and the National Living Wage you can see why I am concerned that this is all too much for many small business owners. 2016 is the year of going backwards for many business owners’ in terms of PROFITABILITY unless they act now!

When will I be paying the extra tax for 2016/17?

Under the usual self-assessment rules then this extra tax would be payable in one lump sum payment by 31/1/2018. That gives taxpayers time to put some money aside each month and can budget accordingly.

It appears though that HMRC doesn’t want to wait that long for the extra tax. We understand that HMRC is in the process of amending tax codes for many company directors so that the lower ‘new’ code reflects the estimated amount of tax due on dividend income.

If you are a taxpayer where cashflow is challenging then this change will be bad news as you will be required an extra monthly tax payment to HMRC potentially as early as May this year. This doesn’t give much time to plan and budget.

How will it work?

Every taxpayer is notified of their tax code via a P2 (PAYE coding notice) and those affected the estimated amount of dividend tax will be shown within the notes.

Tip: If you get one of these tax coding notices it’s advisable to check the figures – an incorrect tax code could mean you unwittingly pay way too much or too little tax.

If you are unsure that the code is correct get in touch with your accountant.

What Can I do?

Everyone’s situation is different which I’m afraid mean the possible tax saving options that are available will also be different. That said here are a few ideas:-

Maximise the annual tax free dividend allowance

Everyone is entitled to the new £5,000 allowance. Married couples can spread their share portfolios in order to spread their dividend income and thereby use the whole of their allowance.

Use an ISA

ISA dividends are tax free and will be not be subject to the new dividend tax. You can transfer up to £15,240 worth of shares and investments into ISAs this year.

Maximise a spouse’s income tax allowance and tax band

Married couples should use the whole of their personal allowances and basic rate tax bands, where applicable, so that any dividends that paid to the spouse who pays the lowest rate of tax.

Invest in VCTs

VCT (Venture Capital Trust) are for taxpayers who are willing to take higher risks. Exactly like ISAs VCTs will give a taxpayer tax free dividends. Also like ISAs when the investment is sold the gain or profit is also tax free as it’s not subject to Capital Gains Tax.

Kim KMA Accountancy

Disclaimer

This article is for general information only and no action should be taken, or refrained from, as a result of this information. Professional advice should be taken based on specific circumstances in each individual case. Whilst we endeavor to ensure that the information contained in this article is correct, no liability will be accepted by KMA Accountancy for damages of any kind arising from the contents of this communication, or for any action or decision taken as a result of using any such information.

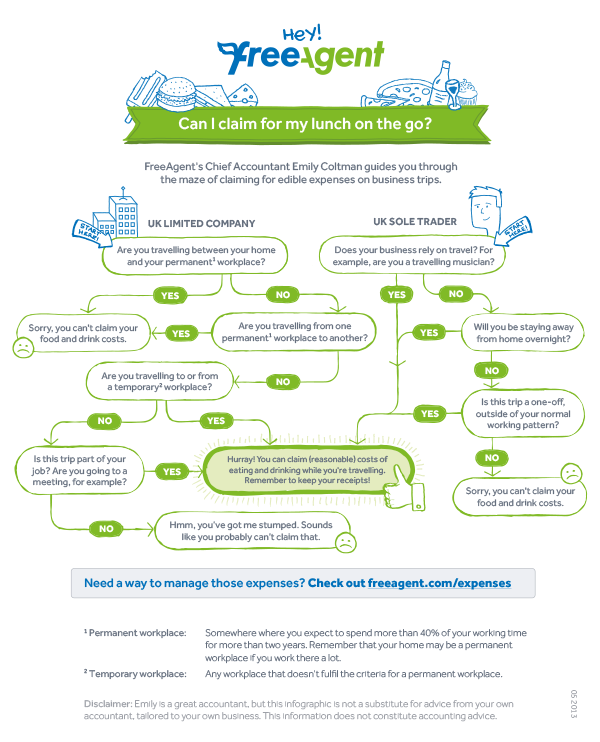

2016/17 rules on the tax free allowance for Sandwiches

What are business journeys (HMRC definition)

You can only get tax relief on the cost of business journeys. These are when, as part of your job:

- you have to travel from one workplace to another – this includes travelling between your main ‘permanent workplace’ and a temporary workplace

- you’ve got to travel to or from a certain workplace because your job requires you to

But business journeys don’t include:

- ordinary commuting – when you travel between your home (or anywhere that is not a workplace) and a place which counts as a permanent workplace

- private journeys – which have nothing to do with your job

steve@bicknells.net

10 ways to pay less VAT

Here are my top 10 ways to pay less VAT

1 Choose the best VAT Scheme for your business

Standard VAT Scheme – on this scheme the VAT is based on tax points from invoices

Flat Rate Scheme – try our calculator

VAT Cash Accounting Scheme – if your turnover is below £1.35m you can account for VAT on a Cash basis, this is particularly helpful if your customers pay you on slower terms than you pay your suppliers

Annual Accounting Scheme for VAT – if your turnover is below £1.35m you could join the Annual Scheme and complete one return for the year but you make either 9 interim payments or 3 quarterly interim payments

Retail VAT Schemes – These are specific schemes aimed at mainly at shops and help to overcome the issues of mixed vat rate goods

VAT Margin Scheme – The margin scheme relates to second hand goods and accounts for VAT on the margin, for example on the sale of cars

2 Claim Pre-registration VAT

When you register for VAT, there’s a time limit for backdating claims for VAT paid before registration. From your date of registration the time limit is:

- 4 years for goods you still have, or that were used to make other goods you still have

- 6 months for services

Be careful not to over claim – see this blog for details http://stevejbicknell.com/2015/06/24/preregistration-vat-confusion/

3 Property Investors might benefit from a Development Company

Property Development is a trade, where as Property Investment isn’t – renting out a residential property is a VAT exempt supply.

If you are planning significant building work, setting up a Development Company or using a building contractor might save VAT.

Assuming you employ a builder…

The VAT Rules are in VAT Notice 708 Buildings & Construction

Your builder may be able to charge you VAT at the reduced rate of 5 per cent if you are converting premises into:

- a ‘single household dwelling’

- a different number of ‘single household dwellings’

- a ‘multiple occupancy dwelling’, such as bed-sits, or

- premises intended for use solely for a ‘relevant residential purpose’

As your builder will be VAT registered, they reclaim the VAT they are charged and then charge you VAT at 5%.

If your business is property rental and you do the work yourself, you can’t take advantage of the 5% rate.

If your Development Company is VAT registered you can reclaim all the VAT.

4 Do you need to charge VAT on Intercompany Charges

There are situations where one company is VAT registered and other related companies are either partially exempt or not registered for VAT, so in these circumstances not charging VAT is an advantage.

The following are not Taxable supplies for VAT:

Common Directors – Notice 700/34 (May 2012)

Joint Employment – Notice 700/34 (May 2012)

Paying a Bill on behalf of an associated business

Insurance

5 Use VAT Groups for Business Acquisition Costs

Basically HMRC disallow Input VAT relating to Investments.

The most well known example of this was when BAA purchased Airport Development Investments Limited in June 2006, the decision was upheld by the Court of Appeal in February 2013.

The BAA VAT group sought to recover the VAT (£6.7m) incurred on the acquisition costs but recovery was refused by HMRC on the basis that they considered ADIL had not made onward taxable supplies, had not demonstrated any intention to make taxable supplies and was not a member of the VAT group at the time costs were incurred.

BAA used an SPV (Ferrovial) to purchase ADIL but did not bring the SPV into the BAA VAT Group until September 2006, 3 months after the acquisition.

The lessons to learn from this are:

- Once you have successfully made the acquisition join a VAT Group immediately and make it clear in correspondence that the SPV intends to join the VAT Group at the earliest opportunity

- Consider not using an SPV

- Buy the Assets instead of the Shares

- Show that the SPV will make taxable management charges

- Consider the scope of the advisors work, HMRC may disallow advice focussed on passively holding shares

6 How Hotels save VAT

Here are some VAT examples for Hotels – HMRC Reference:Notice 709/3 (October 2011) :

The Long Stay Rule

If a guest stays in your establishment for a continuous period of more than 28 days, then from the 29th day of the stay you should charge VAT only on that part of the payment that is not for accommodation.

VAT Exempt Meeting Rooms and Refreshments

Hiring a room for a meeting, or letting of shops and display cases are generally exempt, but you may choose to standard-rate them by opting to tax, see Notice 742A Opting to tax land and buildings.

VAT on Deposits

Most deposits serve as advanced payments, and you must account for VAT in the return period in which you receive the payment. If you have to refund a deposit, you can reclaim any VAT you have accounted for in your next return.

Normally, if you make a cancellation charge to a guest who cancels a booking, VAT is not due, because it is compensation.

7 VAT on Pool Cars

When you buy a car you generally can’t reclaim the VAT. There are some exceptions – for example, when the car is used mainly as one of the following:

- a taxi

- for driving instruction

- for self-drive hire

If you lease a car for business purposes you’ll normally be able to reclaim 50 per cent of the VAT you pay. But you can reclaim 100 per cent of the VAT if the car is used exclusively for a business purpose.

8 Use a Tronc for Tips

Tips are outside the scope of VAT when genuinely freely given. This is so regardless of whether:

• the customer requires the amount to be included on the bill

• payment is made by cheque or credit/debit card

• or not the amount is passed to employees.

Restaurant service charges are part of the consideration for the underlying supply of the meals if customers are required to pay them and are therefore

standard rated.

If customers have a genuine option as to whether to pay the service charges, it is accepted that they are not consideration (even if the amounts appear on the invoice) and therefore fall outside the scope of VAT.

Further information is available from: Notices 700 The VAT guide and 709/1 Catering and takeaway food

9 Get your TOGC right – Transfer of a Going Concern

Normally the sale of the assets of a VAT registered or VAT registerable business will be subject to VAT at the appropriate rate. A transfer of a business as a going concern for VAT purposes (TOGC) however is the sale of a business including assets which must be treated as a matter of law, as ‘neither a supply of goods nor a supply of services’ by virtue of meeting certain conditions. Where the sale meets the conditions then the supply is outside the scope of VAT and therefore VAT is not chargeable.

It is important to be aware that the TOGC rules are mandatory and not optional. So it is important to establish from the outset whether the sale is or is not a TOGC.

The main conditions are:

- the assets must be sold as part of the transfer of a ‘business’ as a ‘going concern’

- the assets are to be used by the purchaser with the intention of carrying on the same kind of ‘business’ as the seller (but not necessarily identical)

- where the seller is a taxable person, the purchaser must be a taxable person already or become one as the result of the transfer

- in respect of land which would be standard rated if it were supplied, the purchaser must notify HMRC that he has opted to tax the land by the relevant date, and must notify the seller that their option has not been disapplied by the same date

- where only part of the ‘business’ is sold it must be capable of operating separately

- there must not be a series of immediately consecutive transfers of ‘business’

The TOGC rules are compulsory. You cannot choose to ‘opt out’. So, it is very important that you establish from the outset whether the business is being sold as a TOGC. Incorrect treatment could result in corrective action by HMRC which may attract a penalty and or interest.

10 Choose the best time to register for VAT

You may decide to voluntarily register to reclaim VAT you have paid out to set up you business or you might decide to wait till you have to register to gain a competitive advantage.

You must register for VAT if:

- your VAT taxable turnover is more than £82,000 (the ‘threshold’) in a 12 month period

- you receive goods in the UK from the EU worth more than £82,000

- you expect to go over the threshold in a single 30 day period

steve@bicknells.net

Why it’s time to end Offshore and Contractor Loan Schemes?

There have been many creative schemes promoted to contractors, entertainers and sports stars, basically using a limited company to make loans to connected parties to avoid tax.

HMRC have been attacking these schemes for years, for example the Boyle case

Philip Boyle v HMRC [TC03103] 2013

On the 16th September HMRC published Spotlight 26: Contractor Loan Schemes – Too good to be true

Contractors and freelancers are bombarded by promoters who make claims that they can help individuals take home as much as 80% to 90% of their income. Sounds too good to be true, that’s because it is.

So why is this considered to be tax avoidance? These promoters use schemes to reduce the amount of tax you pay on your income by making payments which purport to be ‘loans’ from a trust or a company. Normally, a contractor would receive the contract income directly and pay tax on it. These arrangements artificially divert the income through a chain of companies, trusts or partnerships and pay the contractor in the form of a ‘loan’. The ‘loans’ are claimed to be non-taxable because they don’t form part of a contractor’s income. However, in reality the ‘loans’ aren’t repaid and the money is used by the contractor as if it were his or her income.

HM Revenue and Customs (HMRC) view is that these schemes don’t work and strongly advises any contractor or freelancer who has used such a scheme to withdraw and settle their tax affairs. People who settle with HMRC avoid the costs of investigation and litigation and minimise interest and penalty charges on the tax which should have been paid.

Don’t be fooled by promoter websites..

The promoters’ websites and promotional literature claim that they are fully compliant and are HMRC approved. HMRC doesn’t view these arrangements as compliant and never approves any schemes.

Contractor loan schemes, of the sort described above, must be declared under the Disclosure of Tax Avoidance legislation. The promoter is required to pass the scheme reference number (SRN) to all the users who must put this on their tax return. A failure to show the correct SRN on your tax return will lead to additional penalty charges.

Don’t be tempted, HMRC are closing in on unpaid tax, they will find you!

steve@bicknells.net

Do you need help with HMRC?

HMRC aren’t easy to speak to and unless you know the tax rules its easy to make mistakes, that’s why HMRC allow you to appoint agents to help you with your tax affairs.

To appoint an agent you use form 64-8

Form 64-8 covers authorisation for individual tax affairs (partnerships, trusts, tax credits and individuals under PAYE) and business taxes (VAT, PAYE for employers and Corporation Tax). If you’re a personal representative you can use form 64-8 in certain circumstances to ask HMRC to deal directly with an agent.

There are times when you might want extra help for example with an HMRC Compliance Visit and you can appoint a temporary agent using form COMP1.

The Comp1 relates only to the appointment of an adviser to deal with a compliance check. It does not authorise us to deal with that adviser for anything outside that check. Form Comp1 does not replace or amend any existing authorisation made using form 64-8 or the online authorisation facility, or in CITEX cases a letter giving authority for the agent to act.

The temporary authorisation can be used to:

- extend an existing authorisation, for example where there is an adviser acting for one tax under a form 64-8, and the customer wants that adviser to act for more taxes just for the purpose of the compliance check

- appoint an adviser to deal solely with the compliance check where there is no existing adviser authorisation

- appoint a ‘specialist’ tax adviser, for example in Specialist Investigation cases, just to deal with a compliance check. In such cases this will allow the existing adviser to continue to act for the customer in their day to day tax matters.

[HMRC CH201550]

Do you need help?

steve@bicknells.net

Will I get £30,000 tax free? Termination Payments

Basically the current situation is that the first £30,000 of a payment which is paid in connection with the termination of employment is tax free, as long as it is not otherwise taxable as earnings. It sounds simple but can be complicated, here is a government example

The Office of Tax Simplication are currently consulting (until 16th October 2015) on changing the rules one solution is to make it more like redundancy payments, take a look at these examples

There will also be some anti avoidance rules that if you are re-engaged within 12 months in similar job with the same company the payments previously made would become subject to tax and NI.

It looks like we are in for some major changes, its not too late for you to have your say, click on this link

steve@bicknells.net

HMRC to get access to your bank account

If you owe more than £1,000 to HMRC the Summer Finance Bill will give HMRC the power to take it from your bank account!

According to an article on accounting web…

HMRC have said they will contact the taxpayer at least four times about the debt before commencing the DRD procedure. One of those occasions will be a face to face meeting with the taxpayer to establish that they have found the right debtor and calculated the debt correctly. This should avoid the situation where the HMRC letters have failed to arrive, or the taxpayer has not understood the liability.

There are penalties for banks who fail to comply with the notices issued by HMRC.

steve@bicknells.net

Online traders targeted by HMRC

The Revenue has sent 14,000 letters to traders suspected of running a business and failing to declare this on their tax returns.

Of these, 1,000 letters are being sent to people where the taxman has already identified a shortfall on their self-assessment forms.

Some of those targeted make as little as £100 profit online.

It was reported in the Telegraph that eBay, Etsy, Amazon and Gumtree are being forced to hand over customer account details, including their selling activity, as part of the taxman’s legal powers that were extended last year.

The criteria used to assess if an activity is a hobby or a business are:

- The size and commerciality of the activity.

- The frequency of the activity and transactions

- The application of business principles.

- Whether there is a genuine profit motive.

- The amount of time devoted to the activities.

- The existence of arm’s-length customers (as opposed to just selling your wares to family and friends).

HMRC have some great examples to help you decided, for example

Gail is a full-time employee working for a stationery company. She pays her PAYE tax on this employment every month.

In her free time Gail makes cushions and uses most of them in her home. Occasionally she sells them to friends and work colleagues for an amount that just covers the cost of materials of £15. Sometimes she makes a loss. Any money she does make goes towards her holiday fund.

She decides to make extra cash by selling cushions on an Internet auction site and starts auctioning three or four to see how they go. They all sell for more than £50, a profit of at least £35 each.

She uses this money to buy more materials and within a month she is selling around ten cushions a week, always at a profit, and is considering setting up her own website.

Gail’s initial sales of cushions to friends are not classed as trading. It lacks commerciality and she does not set out to make a profit. The occasional sales are a by-product of her hobby. Once she begins to auction her cushions, she has moved into the realms of commerciality.

She is systematically selling her goods to make a profit. She will need to inform HMRC about her trade, and keep records of all her transactions. On the level of sales shown in the example the potential turnover of around £26,000 is well below the VAT annual threshold so Gail does not need to register for VAT.

Many traders start off in a small way and don’t realise that they need to register with HMRC, they assume their activity will be treated as a hobby, but things can grow quickly.

You should register as Self Employed as soon as your hobby becomes a commercial venture, even if you are losing money!

If you don’t register, HMRC will be looking for you and if you have an online business it won’t be hard for them to find you.

steve@bicknells.net

Would a Partial Capital Allowance Claim reduce your tax bill?

It is not necessary to claim the maximum capital allowances available or even claim them at all, crazy as it might sound there are situations when not claiming capital allowances can reduce your tax bill!

Sole Trader Example

The personal tax allowance is currently £10,600 (2015/16)

Lets assume profits are £15,000 and Capital Allowances available are £5,000, so that would reduce taxable profits to £10,000 which would waste £600 of the personal tax allowance.

It would therefore be better to only claim £4,400 in capital allowances and claim the remaining £600 in the following year.

Company Example

Companies within a Group can only offset losses in corresponding tax periods, so if the the capital allowances increase the loss in one part of the group beyond the profits of the rest of the group then there would be no benefit to claiming them in that period.

Companies can claim capital allowances in any of the following 3 tax years.

There is an excellent example of this in the following blog http://taxnotes.co.uk/a-basic-introduction-to-capital-allowances/

steve@bicknells.net