Home » Posts tagged 'tax avoidance'

Tag Archives: tax avoidance

HMRC aims to raise further £5bn in tax revenue

Thanks to http://www.freedigitalphotos.net

Her Majesty’s Revenue & Customs (“HMRC”) are seeking new powers as follows:

1. Advance Payment – basically in any dispute between HMRC and a tax payer HMRC would be able to assess what tax they believe is due and require the tax payer to pay this as a sort of ‘refundable deposit’ until such time as the dispute is resolved through arbitration or court. Perhaps more importantly, if granted, these powers will be applied retrospectively.

Given that at the current time there are unresolved cases going back ten years or more and that once HMRC has the tax payers’ money there will be even less incentive for them to come to a resolution then this is essentially HMRC to act as judge, jury, and executioner. Isn’t this simply a ‘guilty until proven innocent’ treatment of tax payers?

2. Direct Debit – where HMRC believe that the tax payer owes them money then they will be able to simply take money directly from the tax payer’s bank account. As I understand it there will be further powers to obtain previous bank statements and this will no doubt lead to further tax investigations.

The legislation which will encapsulate these powers is currently going through Parliament, and despite opposition from lobby groups and committee members alike, HMRC seem intent upon pushing this legislation through with a view to achieving Royal ascent in mid July 2014.

Of course, should HMRC gain these powers they will hit the easy targets first i.e. those who have ‘played by the rules’ and properly disclosed everything through DOTAS, and those who operate proper business bank accounts, so it will do nothing to address those who have hidden their activities from HMRC and those who operate in the black ‘cash-in-hand’ economy.

Whilst the general public may have little sympathy for people who ‘don’t pay their fair share of tax’ (if there is such as thing – see Did Jimmy Carr just use the wrong vehicle?) we have to remember that tax avoidance is entirely legal as it simply takes the rules and regulations enacted in law and uses these to reduce a tax payer’s liability.

The new powers will do nothing to tackle tax evasion, which is illegal, and so it is no surprise that spokesmen for HMRC, and representatives for HM Government, have sought to blur the lines between legal avoidance and illegal evasion in recent times. We can be equally sure that HMRC will not be tackling the multi-nationals like Google and Starbucks who have made recent headlines with their tax affairs, and so it will (as ever) be small firms that will bear the brunt of any HMRC action.

What we shall no doubt see is an increase in non-DOTAS schemes being made available to tax payers by providers of such schemes, and I fear beyond that we shall see a rise in business insolvencies and loss of jobs, all of which will run contrary to HMRC’s aim to raise further tax revenues.

Paul Driscoll is a Chartered Management Accountant, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and AJ Tensile Fabrications Limited, and is a board level adviser to a variety of other businesses.

A Trillion Euro’s lost to tax evasion in the EU

A Trillion is a huge amount, its almost too large to imagine.

Here is the latest campaign video

http://ec.europa.eu/avservices/video/player.cfm?ref=I080915

As part of the intensified battle against tax fraud, the Commission launched on 6th February 2014 the process to start negotiations with Russia and Norway on administrative cooperation agreements in the area of Value Added Tax (VAT). The broad goal of these agreements would be to establish a framework of mutual assistance in combatting cross-border VAT fraud and in helping each country recover the VAT it is due. VAT fraud involving third-country operators is particularly a risk in the telecoms and e-services sectors. Given the growth of these sectors, more effective tools to fight such fraud are essential to protect public budgets. Cooperation agreements with the EU’s neighbours and trading partners would improve Member States’ chances of identifying and clamping down on VAT fraud, and would stem the financial losses this causes. The Commission is therefore asking Member States for a mandate to start such negotiations with Russia and Norway, while continuing exploratory talks with a number of other important international partners.

http://ec.europa.eu/taxation_customs/taxation/tax_fraud_evasion/missing-part_en.htm

steve@bicknells.net

Limited Liability Partnerships

Limited Liability Partnerships came under closer scrutiny in the Budget 2013. The aim is to target LLPs which use the structure to hide the employment relationship of the partners and those with Corporate partners who divert business profits to the corporate partners in order to avoid tax.

Although the following measures come in to play from 6th April this year, the anti-avoidance measures make it effective from 5th December 2013. This is to prevent partnerships changing their arrangements in order to avoid the new rules.

The two main areas of focus are salaried or fixed profit share partners which is referred to as disguised employment, and profit and loss sharing arrangements within mixed partnerships.

LLP partners with fixed profit share

HMRC believe that many members of an LLP should be taxed as employees, because they don’t see them is true partners.

A new test has been brought in which has three conditions. Where the member tested meets all three conditions then he or she must be treated as an employed salaried member and be brought within the PAYE system with tax and class I NIC applied to any earnings, which had previously been Taxed as profit share.

This also means that if a vehicle is provided for the members use by the partnership this will be taxed as a benefit in kind. As such the member will have to pay tax and NIC and the LLP will have to pay Class 1a NIC on the benefit.

HMRC does actually accept that employment tax rules are imposed on the individual but that in fact the individual has no employment rights. This is because he is not actually an employee for employment law purposes.

The test is as follows. The provision is triggered when all conditions A to C are met:

Condition A: The Member is performing services for the LLP in his capacity as a member of the partnership and it’s reasonable to expect as a result of these arrangements that any amounts paid to him in respect of his services will be wholly or substantially wholly a disguised salary. In other words if his reward package is comparable to that received by an employee, either a fixed salary or a variable bonus based on performance rather than profit share.

Condition B: The Member doesn’t have significant influence over the affairs of the partnership.

Condition C: The Member’s capital contribution to the LLP is less than 25% of the total amount of his disguised salary which would be expected to be paid in the relevant tax year by the LLP in respect of the members performance of services as a member. Normally the relevant time would be the beginning of the new tax year.

These tests must be reviewed each tax year.

Corporate LLP Members

This applies to partnerships who have members which are not subject to UK income tax for example this might be a limited company. The problem here is that HMRC believes these structures are used to avoid tax on a very large scale. Where for example an individual member introduces his Ltd company as a corporate member, and which then receives a profit share that would otherwise have been paid to the individual member. If the Member then has the power to enjoy the fund which had been paid to his company then:

- The individual member will be treated as a salaried member.

- The amount paid to the company will be treated as employment income paid to the individual member.

There are anti-avoidance rules are in place to catch anyone trying to put measures in place to counteract these new rules.

fiona@grant-jonesaccountancy.com

How HMRC use IT systems to seek out tax evaders

There is no doubting the resolve of HMRC to track down and prosecute tax evaders.

The Government has committed to spend £917m to tackle tax evasion and raise an additional £7bn each year by 2014/15.

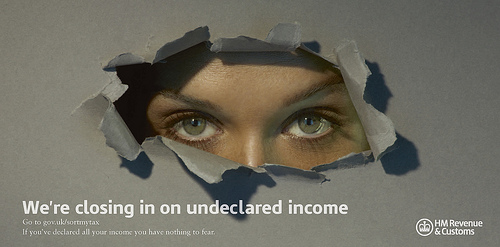

HMRC are using 2,500 staff to tackle avoidance, evasion and fraud, there is also a website to help those who want to declare income https://www.gov.uk/sortmytax

In the search for tax evaders, HMRC have a £45m computer system called Connect which in 2011 delivered £1.4bn in tax revenue and the system is getting bigger and better all the time. According to Accounting Web:

It uses a mathematical technique to search previously unrelated information and detect otherwise invisible ‘relationship’ networks. Using Connect, HMRC sifts through information on property transactions at the Land Registry, company ownerships, loans, bank accounts, employment history, voting and local authority rates registers and compares with self-assessment records to spot taxpayers who might be under-declaring or not declaring income.

Last year Connect made links between tax records and third party data from hospitals, pharmaceutical companies, insurers and even gas SAFE registrations. DVLA records and the shipping and Civil Aviation Authority registers help identify owners of cars and planes who declare income that the computer suggests cannot support such purchases.

In addition HMRC have also identified 200 accountants, lawyers and professionals who advise on tax avoidance structures and its currently unclear how HMRC will be dealing with them and their clients.

It is important to remember that most people pay the correct tax, in fact HMRC calculate that 93% of tax due is paid correctly, its only a small minority who try to evade tax.

steve@bicknells.net

5 ways to reduce the risk of a tax investigation

THE TAX YIELD derived from HM Revenue & Customs investigations into the affairs of small- and medium-sized companies rose by 31% over the last 12 months, according to UHY Hacker Young.

Compliance investigations into SMEs generated £565m for HMRC in 2012/13, up from £434m in 2011/12, with the year ending March 31. Accountancy Age

Some investigations are random and some as a result of HMRC task forces, but many are triggered by risk profiling.

What can you do to reduce your chances of being selected:

1. File your tax returns on time and pay what you owe – If you file late or at the last minute HMRC will think you are disorganised and as such there are more likely to be errors in the return

2. Declare all your income – HMRC get details of bank interest and other sources of income, sometimes they test them and match them to returns

3. Use an accountant – Unrepresented taxpayers are more likely to be looked at, mainly because many of them don’t know what they are doing

4. Trends – if your business doesn’t match the profile of similar business in the same sector or your results suddenly fluctuate it could raise concerns at HMRC, for example, if you suddenly request a VAT refund

5. Tax Avoidance Schemes – if you are using a tax avoidance scheme I am sure HMRC will be looking closely, if they can find a way to challenge the scheme then at some point they will

steve@bicknells.net

How long to keep your records

As a general rule, you should keep your records for a minimum of six years. However,

if you are:

• an employer, you need to keep Pay As You Earn (PAYE) records for 3 years

(in addition to your current year)

• a contractor in the Construction Industry Scheme (CIS), you need to keep your CIS

records for 3 years (in addition to your current year)

• keeping records to complete a personal (non business) tax return, you only need to

keep them for 22 months from the end of the tax year to which they relate.

If you need to keep records for other reasons, for example the Companies’ Act

requires limited companies to keep specific records and you also use those records

for tax purposes, you need to be aware that there may be different time limits for

retaining them. Be careful not to destroy any records you also use for tax purposes

too soon.

niall@odfinancialservice.co.uk

Life after submitting a tax return

You’ve completed your tax returns, you think you can now breathe a sigh of relief, but can you?

HMRC can inspect any taxpayer’s records under Schedule 36 by FA08, FA09 and FA10. They can check the tax records for:-

Pay as You Earn (PAYE)

Value Added Tax (VAT)

Income Tax (IT)

Capital Gains Tax (CGT)

Corporation Tax (CT)

Insurance Premium Tax (IPT)

Inheritance Tax (IHT)

Stamp Duty Land Tax (SDLT)

Stamp Duty Reserve Tax (SDRT)

Petroleum Revenue Tax (PRT)

Aggregates Levy (AGL)

Climate Change Levy (CCL)

Landfill Tax (LFT) and

Bank Payroll Tax (BPT)

The technical term for the inspection is a Compliance Check. They will check that the tax payer has:-

- Complied with their obligations

- Paid the correct amount of tax and at the right time

- Claimed the correct reliefs and allowances

The inspection

This can be completed by anything from a short telephone call to confirm a single fact, to a detailed investigation of a person’s entire financial affairs over a period of years.

HMRC may undertake checks by either asking for information or documents or by arranging a meeting or visit.

They may:

- Require taxpayers by notice in writing to provide information and produce documents (a “taxpayer notice”)

- Require third parties by notice in writing (for example a supplier or bank) to provide information and produce documents (a “third party notice”)

The caveat being that these requirements are reasonable for the purpose of checking a tax position. The generic term for these types of notice is information notice.

The recipient has the protection of a right of appeal to, or prior approval by, an independent tribunal. There is no right of appeal however where the notice only refers to information or documents that form part of a taxpayer’s statutory records, or any person’s records that relate to:

- The supply of goods and services

- The acquisition of goods from another member state, or

- The importation of goods from outside the European Union (EU) by a business

If the taxpayer is not forthcoming with the information, HMRC may invoke their statutory powers to obtain them.

They may also request assistance with aspects of a tax check from other government departments.

This could include a situation where there is reason to believe that a taxpayer:

- did not notify chargeability to tax

- did not register for VAT if required, or

- is operating in the informal economy

Restrictions on Information Powers

The taxman is not all-powerful; some safeguards have been installed, set out in the law and with guidance so that in carrying out compliance checks

- HMRC’s powers are used reasonably and proportionately

- Taxpayers are clear about when a compliance check begins and ends

- Officers have no right to enter any parts of premises that are used solely as a dwelling, whether to carry out an inspection or to examine documents produced under an information notice. They can, however, enter if invited

- FA09 adds to Sch 36 FA08 a power to inspect all property for the purpose of valuation (for direct taxes purposes). This requires either the taxpayer’s agreement or Tribunal approval

- Unannounced visits will only be made where agreement has been given by an authorised officer

Other safeguards include the fact that officers can’t require certain things to be provided:

- Information relating to the conduct of appeals against HMRC decisions

- Legally privileged information

- Auditors or tax advisers advice to a client about their tax affairs

- Information about a person’s medical or spiritual welfare

- Journalistic material

Time constraints

- Information over six years old can only be included in a notice issued by or with the approval of an authorised officer

- HMRC cannot give a notice in respect of the tax position of a dead person more than four years after the person’s death

The Power to Visit Business Premises and Check Assets and Records

Inspection powers allow an officer of HMRC to enter business premises and inspect the premises, business assets and statutory records.

If an information notice has been issued earlier, the documents required in that notice could be inspected at the same time.

FA09 incorporates into Schedule 36 inspection powers in respect of the:

- business premises of Involved third parties

- valuation of premises for Income Tax or Corporation Tax

These inspections:

- must only be undertaken where it is reasonably required to establish the tax position and

- will normally be by prior arrangement, the date and time being convenient to the taxpayer

The Power to Visit Business Premises and Check Assets and Records

Inspection powers also allow any officer to enter any premises when they believe the premises are to be used in connection with taxable supplies of goods or taxable acquisition of goods from Member States, and such goods or documents relating to such goods are on the premises.

There is no right of appeal against an inspection but the occupier can refuse entry and prevent the inspection from being completed.

The occupier can be penalised for such obstruction, where the inspection has been approved by a Tribunal.

There may be occasions when a pre-arranged visit will be inappropriate, for example where there is a strong risk that the taxpayer would move the business or remove stock or other assets. In such cases, an unannounced visit may be undertaken subject to prior agreement by an authorised officer.

If a formal statutory approach is needed, and it has not been possible to agree the time of inspection and give written confirmation, the inspection must be approved by a Tribunal and 7 days written notice of the time of the inspection given. The application for approval must be made by, or with the approval of, an authorised officer.

When a Penalty can be charged where a person:

- Fails to comply with an information notice

- Conceals, destroys or otherwise disposes of documents required by an information notice

- Conceals, destroys or otherwise disposes of documents that they have been notified are, or are likely to be, required by an information notice

- Deliberately obstructs an inspection that has been approved by the Tribunal.

- In complying with an information notice provides inaccurate information or produces a document that contains an inaccuracy,

- Fails to comply with a notice requiring contact details of a tax/duty debtor to HMRC.

These rights are covered in sections 38 FA 08 and 09

Types of Penalties

There are four types and amounts of penalty:

- An initial penalty of £300

- A daily penalty of up to £60 for every day that the failure or obstruction continues after the date the initial penalty is assessed

- A tax-related penalty

- A penalty not exceeding £3000 for providing inaccurate information or documents in response to an information notice

A tax-related penalty is in addition to the initial penalty and any daily penalties. The amount of the penalty is decided by the Upper Tribunal having regard to the amount of tax which either has not, or is unlikely to be, paid by that person.

A person is not liable to a penalty if they have a reasonable excuse for:

- Failing to comply with an information notice, or

- Providing inaccurate details or documents, or

- Deliberately obstructing a tribunal approved inspection

If they correct their failure as soon as the excuse ends, the excuse will then be treated as continuing until the correction is made.

Normally, daily penalties will not be assessed after the failure has been remedied.

Record Keeping

Schedule 37 of FA08 amended existing record keeping legislation in respect of PAYE, VAT, IT, CGT and CT, whilst Schedule 50 to FA2009 extends this approach to IPT, SDLT, AGL, CCL, and LFT with BPT being included from 8 April 2010. Following consultation it was accepted that SDRT and PRT did not require separate statutory provisions, whilst IHT will be addressed through guidance.

These provisions are aimed at alignment and clarification.

This approach is designed to be flexible across a range of business and non-business taxpayers.

There are penalties for failure to keep adequate records.

The basic requirements in relation to record keeping have not changed but rules have been aligned on how long records are kept.

niall@odfinancialservice.co.uk

Tax Planning v’s GAAR and the “Double Reasonableness Test” – Will GAAR stop tax avoidance abuse?

The general anti abuse rule (GAAR) has now been adopted by many advisers in the UK.

The GAAR will apply to Corporation Tax (and amounts treated as Corporation Tax), Income Tax, Capital Gains Tax, Petroleum Revenue Tax, Inheritance Tax, Stamp Duty Land Tax, and the annual tax on enveloped dwellings.

Heather Self, Pinsent Mason commented. “Many of the examples are complex and contrived – we need more examples of ‘normal’ tax planning, to help show where the boundary will lie.”

The key changes to the legislation relate to the “double reasonableness test”. Nearly all the respondents to the consultation expressed concern about this test. The stated purpose of the GAAR is to counteract “tax advantages” arising from “tax arrangements” that are “abusive”. The tests of “tax advantage” and “abusive” both use concepts of reasonableness and this has been referred to as the “double reasonableness test”.

Accountancy Age reported on the 3rd April 2013:

A LACK OF CLEAR DEFINITION within the incoming General Anti-Abuse Rule is likely to cause “considerable uncertainty”, advisers have warned.

The GAAR, designed to catch and prevent contrived tax avoidance schemes, was included in the 2013 Finance Bill and will take effect once it has received Royal assent in July, although many practitioners have been treating it as if it came in on 1 April.

Chair of the House of Lords committee on the Finance Bill Lord MacGregor said : “There is a misconception that GAAR will mean the likes of Starbucks and Amazon will be slapped with massive tax bills.

“This is wrong and the government needs to explain that to the public. GAAR is narrowly defined and will only impact on the most abusive of tax avoidance.”

The Institute of Chartered Accountants in England and Wales (ICAEW) has reiterated its criticisms of draft legislation for a General Anti-Avoidance Rule, claiming that the proposed GAAR is confusing and that it could be in breach of international obligations by overriding double taxation treaties.

The ICAEW draws attention to Article 27 of the Vienna Convention, which the UK signed in 1971 and which states that “a party may not invoke the provisions of its internal law as justification for its failure to perform a treaty.” ICAEW argues that the GAAR may therefore be unlawful, particularly in the case of around 100 agreements with non-OECD countries.

HMRC will be monitoring for GAAR by:

- Reviewing DOTAS (Disclosure of Tax Avoidance Schemes) for abusive schemes, in general DOTAS are reported by the scheme promoter or scheme user – HMRC have a number schemes under the spot light

- Intelligence via other sources or disclosure

- Records of successfully litigated or settled by agreement GAAR cases

- Regular communication with taxpayers and their advisers

DOTAS penalties fall into three categories:

- Disclosure penalties: apply to failure to disclose a scheme. There are variations in cases where a Tribunal has issued a disclosure order.

- Information penalties: apply to other failures to comply with DOTAS.

- User penalties: apply to failure by a scheme user to report a Scheme Reference Number (SRN) to HMRC.

In all cases apart from user penalties (which are up to £1,000) the initial and daily penalty is determined by a Tribunal and could be up to £5,000 per day.

Its important to note:

Tax avoidance is not the same as tax planning. Tax planning involves using tax reliefs for the purpose for which they were intended. For example, claiming tax relief on capital investment, saving in a tax-exempt ISA or saving for retirement by making contributions to a pension scheme are all legitimate forms of tax planning.

So will GAAR work? does it need to be clarified so that we can understand it? I am sure we all agree that everyone should pay their fair share of tax but is GAAR the best way to achieve this?

steve@bicknells.net

How HMRC use IT systems to seek out tax evaders

There is no doubting the resolve of HMRC to track down and prosecute tax evaders.

The Government has committed to spend £917m to tackle tax evasion and raise an additional £7bn each year by 2014/15.

HMRC are using 2,500 staff to tackle avoidance, evasion and fraud, there is also a website to help those who want to declare income https://www.gov.uk/sortmytax

In the search for tax evaders, HMRC have a £45m computer system called Connect which in 2011 delivered £1.4bn in tax revenue and the system is getting bigger and better all the time. According to Accounting Web:

It uses a mathematical technique to search previously unrelated information and detect otherwise invisible ‘relationship’ networks. Using Connect, HMRC sifts through information on property transactions at the Land Registry, company ownerships, loans, bank accounts, employment history, voting and local authority rates registers and compares with self-assessment records to spot taxpayers who might be under-declaring or not declaring income.

Last year Connect made links between tax records and third party data from hospitals, pharmaceutical companies, insurers and even gas SAFE registrations. DVLA records and the shipping and Civil Aviation Authority registers help identify owners of cars and planes who declare income that the computer suggests cannot support such purchases.

In addition HMRC have also identified 200 accountants, lawyers and professionals who advise on tax avoidance structures and its currently unclear how HMRC will be dealing with them and their clients.

It is important to remember that most people pay the correct tax, in fact HMRC calculate that 93% of tax due is paid correctly, its only a small minority who try to evade tax.

steve@bicknells.net

Contractor Loan Schemes

HMRC is challenging certain types of tax avoidance arrangements used by contractors and other professionals. These schemes aim to avoid tax by entering into a contract of employment with an offshore employer, meanwhile the contractor continues to provide their services in the UK. The contractor then receives a large proportion of the fees for their services in payments which are reported as loans. However HMRC argues that these arrangements do not succeed in avoiding tax.

Individuals using these schemes may shortly or already have received letters opening enquiries into their recent returns. HMRC will be sending tax assessments to those who have used these schemes between 2008 and 2011. If your client receives an assessment he can according to HMRC either accept the assessment and pay the tax due, try to reach an agreement with HMRC or appeal against the assessments and begin the tribunal process.

HMRC is urging individuals affected or their advisers to contact HMRC by phone or by email at the following link at http://www.hmrc.gov.uk/news/contractor-loan-schemes.htm.

Fiona@grant-jonesaccountancy.com