R&D Relief is a Corporation Tax relief that may reduce your company or organisation’s tax bill.

Alternatively, if your company or organisation is small or medium-sized, you may be able to choose to receive a tax credit instead, by way of a cash sum paid by HM Revenue and Customs (HMRC)

But your company or organisation can only claim R&D Relief if it’s liable for Corporation Tax.

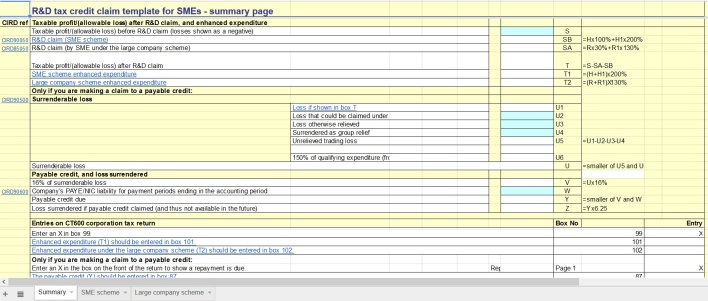

The Small and Medium-sized Enterprise Scheme

This scheme has higher rates of relief. Since 1 April 2015, the tax relief on allowable R&D costs is 230% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £130 on top of the £100 spent. It also includes a payable credit in some circumstances.

The Large Company Scheme

If your company isn’t small or medium-sized, then you can only claim under the Large Company Scheme.

Since 1 April 2008, the tax relief on allowable R&D costs is 130% – that is, for each £100 of qualifying costs, your company or organisation could have the income on which Corporation Tax is paid reduced by an additional £30 on top of the £100 spent. If instead there’s an allowable trading loss for the period, this can be increased by 30% of the qualifying R&D costs – £30 for each £100 spent. This loss can be carried forwards or back in the normal way.

Government Statistics show a steady growth in claims

Construction Examples of R&D

- The investigation into the removal of contamination from sites, including land remediation

- Advancements in structural techniques that aid construction relating to unusual ground conditions

- The innovative use of green or sustainable methods and technology

- Development or adaptation of tools to improve efficiency

- The use of new or unique materials, e.g. recycled products

- Improvement on existing construction methods or development of new ideas to solve ongoing issues related to the site environment or project specifications

- Innovative architectural design

IT Systems Examples of R&D

- The design, construction and testing of systems, devices or processes e.g. new hardware or software components, digital interface and control systems

- Integration of legacy and new systems e.g. following a corporate merger or acquisition, the adoption of an Enterprise Architecture or externally with partners in joint ventures

- Advances in network management and operational tools, development of wired or wireless technologies, designing mobile and interactive services, evolution of new generation network switching and control systems

- Data intensive activities e.g. the collection, storage and analysis, distribution and retrieval. Defining or working with new or emerging data models and metadata standards, integration with third party content

These examples and more are shown on the Cost Care Website

There are also examples by Industry on the Alma CG website

http://www.taxdonut.co.uk/blog/2014/12/beginners-guide-claiming-rd-tax-credits-infographic

These are the key questions that you will be asked when requesting an R&D Tax Credit from HMRC:

- How was it decided that R&D had taken place

- A description of the scientific & technological advance sought

- The uncertainties involved

- How and when the uncertainties were resolved

- Why the knowledge being sought was not readily deducible by a competent professional

- Were any grants, subsidies or contributions received for the project within the claim

- Who owns the Intellectual Property of the products resulting from the R&D

- Was the R&D carried out for others ie clients, this could mean your claim is rejected

This HMRC Spreadsheet will help you calculate your Claim

steve@bicknells.net