Home » Posts tagged 'pension scheme'

Tag Archives: pension scheme

BrightPay: Now Supporting 14 Pension Providers

The introduction of automatic enrolment means that employers across the UK must enrol eligible jobholders into a workplace pension scheme.

Employers must choose a pension scheme that meets the qualifying criteria for auto enrolment. The Pensions Regulator recommends that you choose your pension provider 6 months before your staging date to allow enough time to make the right choice for you and your staff.

There are a number of things to consider when choosing a pension provider, one of the most important being compatibility with your payroll software. Each pension provider requires information in various formats and so it is essential that your payroll software supports your chosen pension provider.

Speak to your payroll provider and ask them if your chosen pension scheme will work with your software. If it doesn’t, you should consider updating your software.

BrightPay currently supports 14 different pension providers, with more constantly being added. If your chosen pension provider is not on the list below, feel free to let us know and we can look into making it available.

The pension provider support in BrightPay allows you to create customised enrolment and contribution files for each of the pension providers, where applicable. APIs with a number of the above pension providers are also in working progress. This means that there will be a direct link between BrightPay and the pension scheme provider.

Although BrightPay supports these pension providers, the software does not choose the pension scheme provider for you. It is the employer’s responsibility to choose a relevant pension provider for their workforce.

To assist with choosing a pension scheme, The Pensions Regulator has recently released a guide to selecting a pension scheme for automatic enrolment for employers. If you need extra guidance, you can also contact an Independent Financial Adviser, but ultimately, the choice of scheme is the responsibility of the employer.

![]()

Written by Rachel Hynes for BrightPay Payroll and Auto Enrolment Software

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

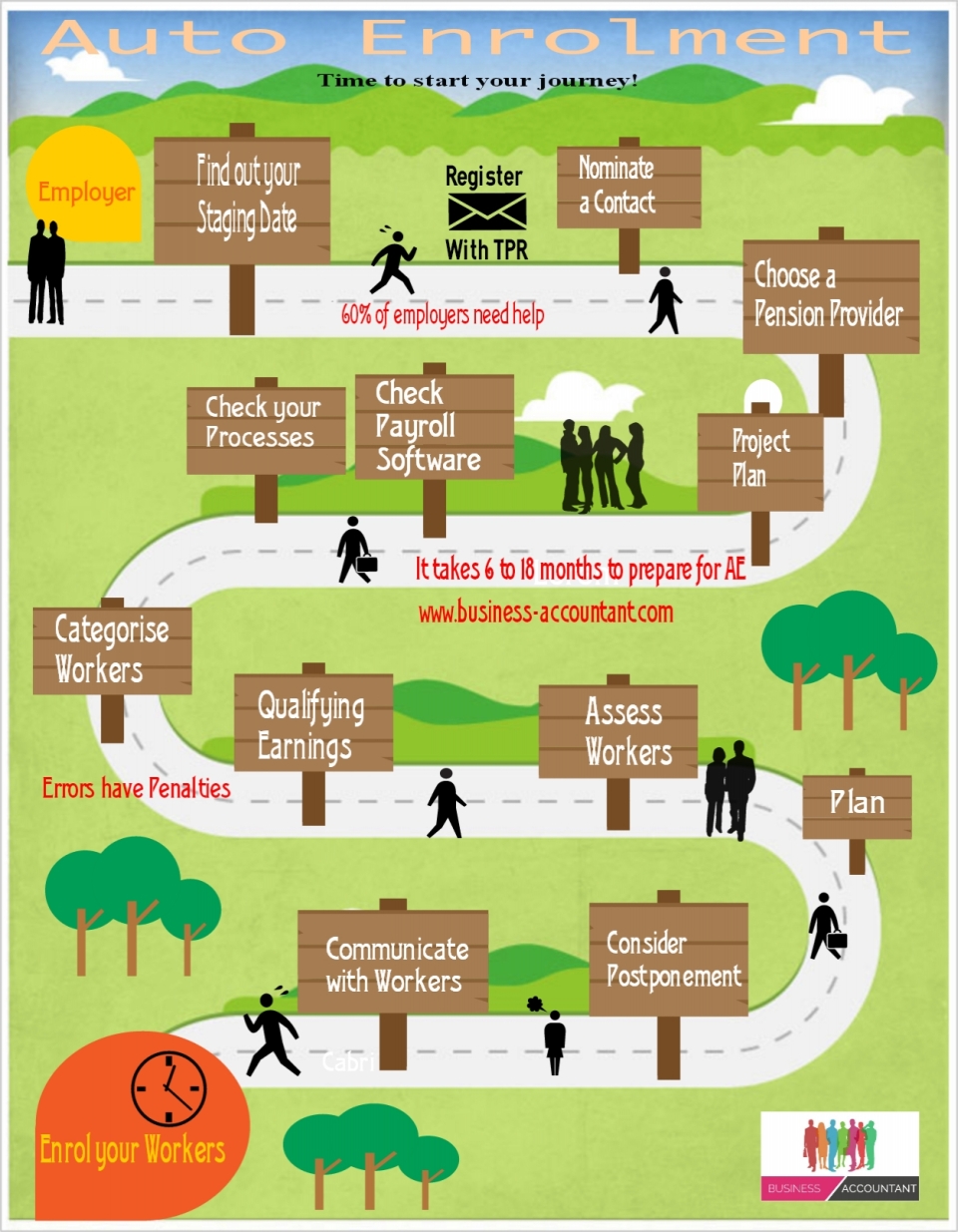

Auto Enrolment do you need help?

New research*, from workplace pensions provider NOW: Pensions reveals that four in ten (44%) small and medium sized companies haven’t given any thought to how they’ll go about finding a pension scheme to comply with the new auto enrolment legislation. But, a significant proportion, (14%) intend to get help from their accountant.

Of the 450 small and medium sized firms surveyed 5% are going to consult an IFA, 4% are going to search the market and do the research themselves. Only 2% have already made a decision and secured a scheme.

Over a fifth (22%) intend to use their existing pension provider for auto enrolment. This comes despite growing concern that some providers will not support smaller employers’ auto enrolment needs.

Despite a large proportion of SMEs admitting they are yet to think about their pension scheme, over half (57%) of firms surveyed think that their choice of pension provider is either important (33%) or very important (24%). Only 8% think it is unimportant.

Four in ten (40%) believe offering a good quality pension scheme will help with employee retention and nearly a third (32%) think it will help to improve the attractiveness of their company to potential employees.

Morten Nilsson, CEO of NOW: Pensions continues: “As auto enrolment gathers pace, accountants will play a key role in guiding small and medium sized companies through the complexities of the legislation. For those accountants that manage payroll, auto enrolment is unavoidable so getting to grips with it sooner rather than later is a must.”

Stephen Milne Chair of the CIMA Members in Practice Panel said: “With over 10,000 employers auto enrolling each month, support for SMEs is inevitably in short supply. Accountants are ideally placed to provide much needed help with the process from scheme selection to assessment and implementation.”

Through Business Accountant, a service provided by CIMA Members in Practice, companies facing auto enrolment can book a local CIMA Member in Practice by calling: 023 8064 3763.

*Research undertaken by BDRC Continental, an award-winning insight agency. Questions were put to 450 UK SMEs (up to and including 250 employees) via BDRC Continental’s monthly Business Opinion Omnibus. Telephone-based interviews with a nationally representative sample of senior financial decision makers across the UK, weighted by size, region and sector. Fieldwork dates 3rd to 13th March 2014

**Research conducted online with 264 advisers by Defaqto between 25th November and 5th December 2013.