Home » Posts tagged 'Pension Auto Enrolment'

Tag Archives: Pension Auto Enrolment

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

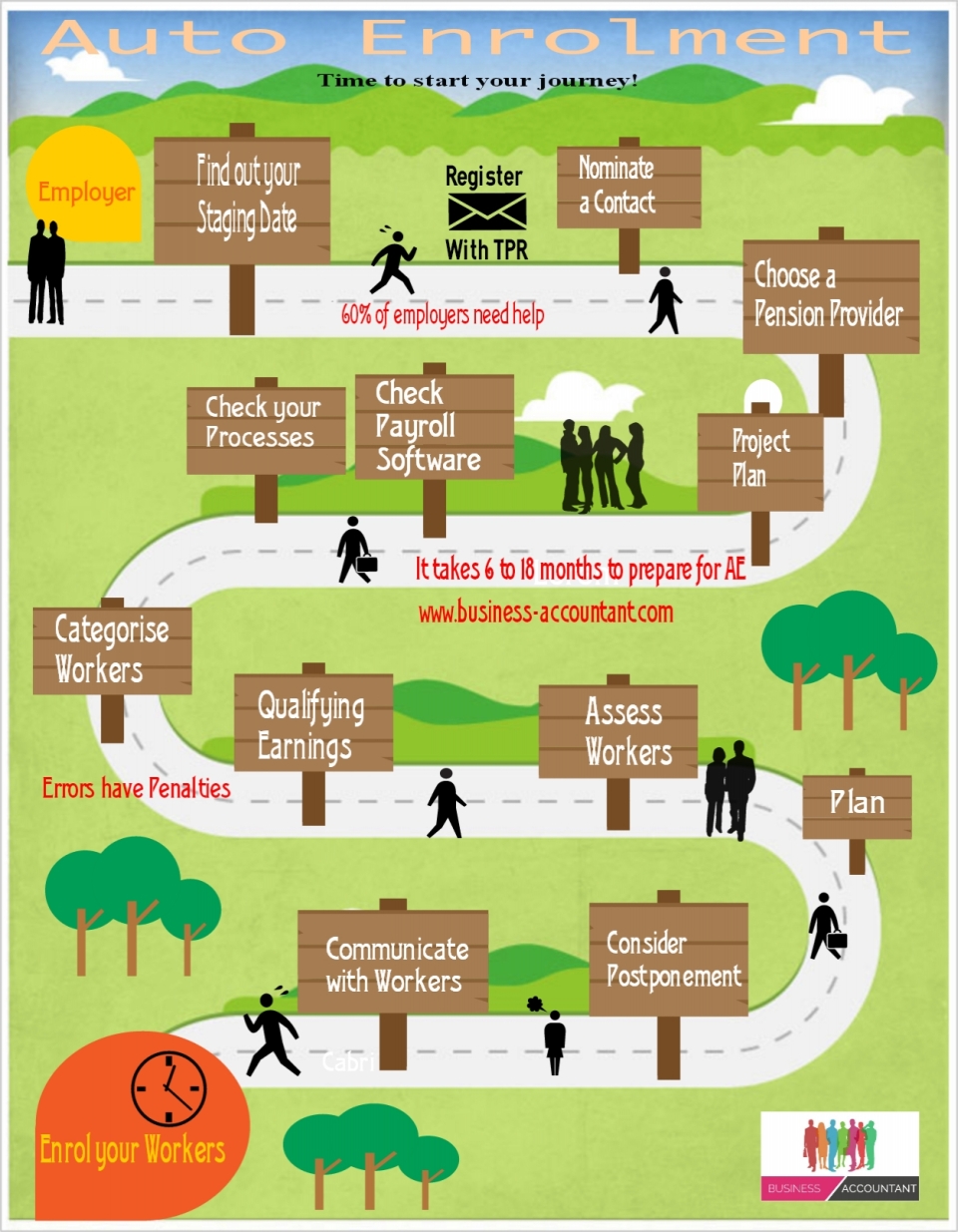

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.