Home » Posts tagged 'HMRC' (Page 9)

Tag Archives: HMRC

Will HMRC help you get over the Floods?

Will it ever stop raining!

But help is at hand, HMRC launched their helpline (12/2/14)

The helpline will enable anyone affected to get fast, practical help and advice on a wide range of tax problems they may be facing.

HM Revenue and Customs (HMRC) will also:

- agree instalment arrangements where taxpayers are unable to pay as a result of the floods;

- agree a practical approach when individuals and businesses have lost vital records to the floods;

- suspend debt collection proceedings for those affected by the floods;

- cancel penalties when the taxpayer has missed statutory deadlines.

The helpline is in addition to other HMRC telephone contact numbers.

The helpline is 0800 904 7900. Opening hours are Monday to Friday, 8.00 am to 8.00 pm; Saturday and Sunday, 8.00 am to 4.00 pm, excluding bank holidays.

I hope the weather improves soon and your business can keep going and survive the storms.

steve@bicknells.net

The Risk-Based Approach – Risky business for SMEs? – Part I

HMRC (Photo credit: Images_of_Money)

The issue:

Risk-based approaches to manage Compliance Service delivery are undergoing a maturity model evolution.

This per se is not a negative issue, however, do risk-based approaches leave us exposed to more or less compliance risk?

We pose this question because a number of process advances, including technological drivers have over the past few years increased the incidence of the risk-based approach (r)evolution.

As an example, HMRC launched their risk based approach pilot scheme related to business record keeping called ‘Business Records Check‘ a few years ago (2011), only for the initiative to ‘go quiet’ and then suddenly to rear its head again late in 2013.

The facts:

From the HMRC web site, the following information was published:

By extrapolation, HMRC also publish within their background report the following table:

Next steps:

Related articles

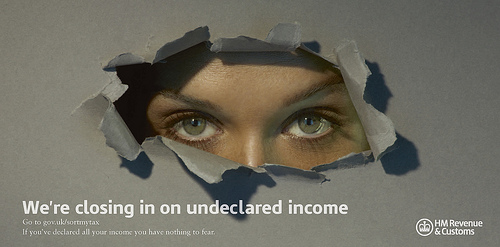

How HMRC use IT systems to seek out tax evaders

There is no doubting the resolve of HMRC to track down and prosecute tax evaders.

The Government has committed to spend £917m to tackle tax evasion and raise an additional £7bn each year by 2014/15.

HMRC are using 2,500 staff to tackle avoidance, evasion and fraud, there is also a website to help those who want to declare income https://www.gov.uk/sortmytax

In the search for tax evaders, HMRC have a £45m computer system called Connect which in 2011 delivered £1.4bn in tax revenue and the system is getting bigger and better all the time. According to Accounting Web:

It uses a mathematical technique to search previously unrelated information and detect otherwise invisible ‘relationship’ networks. Using Connect, HMRC sifts through information on property transactions at the Land Registry, company ownerships, loans, bank accounts, employment history, voting and local authority rates registers and compares with self-assessment records to spot taxpayers who might be under-declaring or not declaring income.

Last year Connect made links between tax records and third party data from hospitals, pharmaceutical companies, insurers and even gas SAFE registrations. DVLA records and the shipping and Civil Aviation Authority registers help identify owners of cars and planes who declare income that the computer suggests cannot support such purchases.

In addition HMRC have also identified 200 accountants, lawyers and professionals who advise on tax avoidance structures and its currently unclear how HMRC will be dealing with them and their clients.

It is important to remember that most people pay the correct tax, in fact HMRC calculate that 93% of tax due is paid correctly, its only a small minority who try to evade tax.

steve@bicknells.net

5 ways to reduce the risk of a tax investigation

THE TAX YIELD derived from HM Revenue & Customs investigations into the affairs of small- and medium-sized companies rose by 31% over the last 12 months, according to UHY Hacker Young.

Compliance investigations into SMEs generated £565m for HMRC in 2012/13, up from £434m in 2011/12, with the year ending March 31. Accountancy Age

Some investigations are random and some as a result of HMRC task forces, but many are triggered by risk profiling.

What can you do to reduce your chances of being selected:

1. File your tax returns on time and pay what you owe – If you file late or at the last minute HMRC will think you are disorganised and as such there are more likely to be errors in the return

2. Declare all your income – HMRC get details of bank interest and other sources of income, sometimes they test them and match them to returns

3. Use an accountant – Unrepresented taxpayers are more likely to be looked at, mainly because many of them don’t know what they are doing

4. Trends – if your business doesn’t match the profile of similar business in the same sector or your results suddenly fluctuate it could raise concerns at HMRC, for example, if you suddenly request a VAT refund

5. Tax Avoidance Schemes – if you are using a tax avoidance scheme I am sure HMRC will be looking closely, if they can find a way to challenge the scheme then at some point they will

steve@bicknells.net

HMRC demand payment from Landlords

HMRC launched the ‘Let Property Campaign‘ on the 10th December 2013.

If you’re a landlord who has undisclosed income you must tell HMRC about any unpaid tax now. You will then have 3 months to calculate and pay what you owe.

The Let Property Campaign is an opportunity open to all residential property landlords with undisclosed taxes. This includes:

- those that have multiple properties

- landlords with single rentals

- specialist landlords with student or workforce rentals

- holiday lettings

- anyone renting out a room in their main home for more than £4,250 per year, or £2,125 if the property was let jointly, but has not told HMRC about this income

- those who live abroad or intend to live abroad for more than 6 months and rent out a property in the UK as you may still be liable to UK taxes

According to the Telegraph….

Fewer than 500,000 taxpayers are registered with HMRC as owning properties other than their home. And yet other sources put the number of Britain’s growing army of landlords at between 1.2million and 1.4million.

Why the discrepancy? No one can say for sure, but the taxman has his answer: not enough people are declaring – and paying tax on – their property incomes and gains.

HMRC will identify those who they believe should have made a disclosure by:

- comparing the information already in their possession with customers’ UK tax histories

- continuing to use their powers to obtain further detailed information about payments made to and from landlords

Where additional taxes are due HMRC will usually charge higher penalties than those available under the Let Property Campaign. The penalties could be up to 100% of the unpaid liabilities, or up to 200% for offshore related income.

If you owe tax, you must tell HMRC of your intention to make a disclosure. You need to do this as soon as you become aware that you owe tax on your letting income.

At this stage, you only need to tell HMRC that you will be making a disclosure.

You do not need to provide any details of the undisclosed income or the tax you believe you owe.

steve@bicknells.net

Are you coding your VAT entries correctly?

When you enter transactions its important to use the right tax code otherwise your VAT returns are likely to either need adjustment or contain errors, but often when entering transactions your software won’t tell you what the codes mean, here is a list of Sage codes:

| T0 | Zero rated transactions |

| T1 | Standard rate |

| T2 | Exempt transactions |

| T4 | Sales of goods to VAT registered customers in EC |

| T5 | Lower rate |

| T7 | Zero-rated purchases of goods from suppliers in EC |

| T8 | Standard-rated purchases of goods from suppliers in EC |

| T9 | Transactions not involving VAT |

| T20 | Sales and purchases of reverse charges |

| T22 | Sales of services to VAT registered customers in EC |

| T23 | Zero-rated purchases of services from suppliers in EC |

| T24 | Standard-rated purchases of services from suppliers in EC |

| T25 | Flat rate accounting scheme, purchase and sale of individual capital items > £2,000 |

There are different rates of VAT, depending on the type of goods or services your business provides. At the moment there are three different rates. They are:

- standard rate – 20 per cent

- reduced rate – 5 per cent

- zero rate – 0 per cent

You can check which rate to use on the HMRC Website http://www.hmrc.gov.uk/vat/forms-rates/rates/rates.htm

UK supplier who aren’t VAT registered would use T9 in Sage.

steve@bicknells.net

Garden bagging – profit from property development in your back yard

The rate of new housing required to meet demand in England is now estimated at between 240,000 and 245,000 units a year, an increase of 10,000 new homes annually on previously accepted figures.

Gazumping and other nasties that flourished in the last property boom are making a return, as competition for homes increases with the bringing forward of the second phase of Help to Buy.

So now could be the time to sell off your garden:

- Its a way of building homes without building on the Green Belt

- It can be a zero risk way to make money if you sell the plot

Garden Bagging works as follows:

- Home Owners with suitable land approach a local builder

- The builder buys the right to seek planning permission for a nominal fee

- If the application is successful the builder will pay up to 85% of the open market value of the consented plot less his costs

Alternatively you could develop the plot yourself for a typical self build its estimated that 35% would be the land cost, 40% build cost and 25% profit margin.

steve@bicknells.net

Tax Free Childcare will the new rules be better or worse?

The Government wants to help working families and currently if you are an employee your employer can help with childcare and could for example buy childcare vouchers of up to £55 per week, the vouchers would be a tax free benefit to the employee. However, if you’re self employed you aren’t an employee so the rules don’t apply.

So recently there has been a consultation on what should be be done in the future.

The key proposals are:

- New Scheme to go live in Autumn 2015

- Working Families will open Voucher Accounts (self employed or employed)

- As parents pay in the government tops up the account with 20p for every 80p paid in

- Top up capped at £1,200

- To be eligible all parent must work and not receive tax credits or be an additional rate tax payer

The chart below shows how it should work:

steve@bicknells.net

No more Class 1NI for Self Employed Entertainers

Following 18 months of extensive engagement with representatives from all fields of the entertainment industry, HMRC published on 15 May 2013 a public consultation document: ‘National Insurance and Self-Employed Entertainers’, which discussed the precise difficulties being caused by the current application of the Regulations. The consultation presented four possible options for simplifying the NICs treatment of entertainers going forwards.

The consultation ran for 12 weeks receiving 11,814 individual responses of which 99.1% supported the option of repealing the Social Security (Categorisation of Earners) Regulations in relation to the entertainers. On 23 October 2013 HMRC published a summary of the consultation responses which included the announcement of the Government’s decision to repeal these Regulations insofar as they relate to entertainers from 6 April 2014 and a first draft of the legislation implementing this.

From 6 April 2014, producers engaging entertainment performance services will not be required to deduct Class 1 NICs contributions from any payments they make to you. This includes additional use payments such as royalties. The engager will make payments to the entertainer gross of tax and NICs and the entertainer must declare these earnings as part of their normal self-employed Self-Assessment return.

Please note that this guidance does not apply if you are an entertainer on an employment contract, and receive a regular salary from your engager with tax and NICs deducted at source under the Pay As You Earn (PAYE) system.

If you engage the services of entertainers

From 6 April 2014, you will not be required to operate Class 1 NICs for the entertainers you engage. If you are currently deducting employees’ Class 1 NICs from the payments you make to your entertainers (including additional use payments such as royalties), and paying the respective employers’ Class 1 NICs on these payments, you should continue to do so up until 5 April 2014. From 6 April 2014 however you should cease to do this.

The changes will be of interest to all national broadcasters, film companies, theatre managers, independent production companies, their representative bodies and agents in the Film & TV Production Industries, Equity, individual entertainers, companies engaging entertainers, and any other interested parties.

See HMRC Brief 35/13 for more details

steve@bicknells.net

How long does it take to register for VAT?

It currently takes around a month for HM Revenue & Customs (HMRC) to process applications for VAT registration, although it can take longer if they need to carry out additional checks.

GOV.UK say it could take as little as 14 working days.

HMRC aims to process 70 per cent of applications within 10 working days and most are processed within a month.

But there are cases where it can take a lot longer, possibly even 6 months.

Between applying for VAT registration and receiving your VAT registration number, you must still account for and pay any VAT due. You become liable for VAT from the date you must be registered or asked for your voluntary registration to start, not the date that you actually apply for registration or the date you receive your VAT registration number.

You may also reclaim any VAT you pay on your purchases from the date you must be registered, so you must also keep records of any invoices where your suppliers have charged you VAT.

Until you receive your VAT registration number you must not charge VAT, or show VAT on your invoices. To make sure that you do not lose income in the period after you applied for VAT registration but before you receive your VAT registration number, you should increase your prices by an amount equivalent to the VAT rate relevant for your goods or services, and explain to your customers why you are doing so.

Once you receive your VAT registration number you can then reissue those invoices, amended to show your VAT registration number and the VAT charged. This will make sure that your VAT-registered customers may reclaim the VAT that they have paid.

From a business perspective this is messy, you have to ask you customers to pay 20% extra on the promise that you will later give them a credit and a vat invoice so that they can reclaim the VAT!

I think HMRC should give this some thought, perhaps VAT registration could be fast tracked or done instantly by phone or online?

steve@bicknells.net