Home » Posts tagged 'FRS102'

Tag Archives: FRS102

Now we have Deferred Tax on Investment Properties!

FRS102 has led to many changes in the way we account for things and investment property is a prime example.

The fair value of investment properties changes over time, generally, it goes up in value.

The reporting of gains and losses under old and new UK GAAP differs fundamentally.

Under FRS 102, annual changes in the fair value of Investment Properties are taken to profit or loss, whereas under SSAP 19, equivalent gains and losses were taken in most cases to the Statement of Recognised Gains and Losses. This may have a significant impact on reported performance. The resultant earnings volatility may need to be explained to lenders and other users of the accounts.

FRS 102 removes some of FRS 19’s exemptions from recognising deferred tax. As a result, in contrast to current UK GAAP (that is, FRS 19), companies will often need to recognise significant deferred tax liabilities on revaluation gains.

The tax won’t be payable until the gain is realised.

Many property investors are likely to switch to Micro-entity accounting because its much simpler and doesn’t require property revaluations and deferred tax.

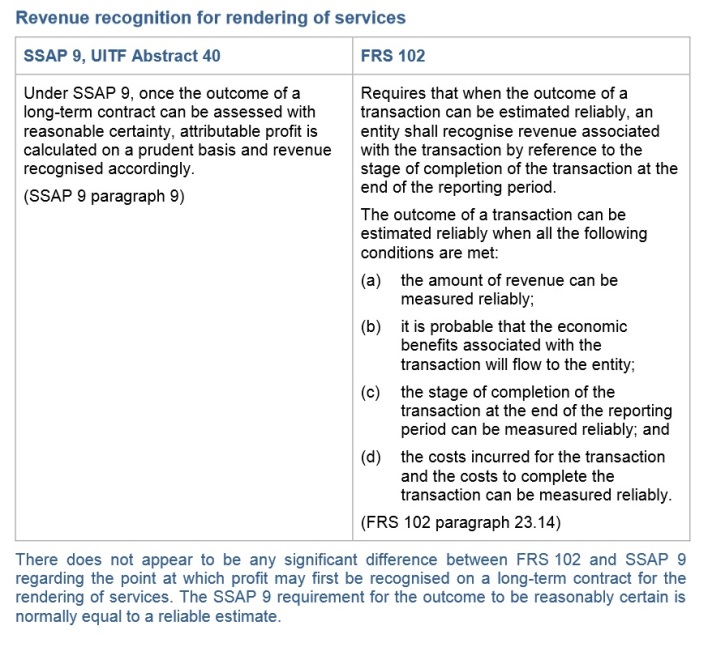

When should you recognise revenue on services provided?

The International Accounting Standard IAS 18 states

‘where the outcome of a transaction involving the rendering of services can be estimated reliably, associated revenue should be recognised by reference to the stage of completion of the transaction at the end of the reporting period’ . In other words, the revenue is recognised gradually, rather than all at one ‘critical point’, as is the case for revenue from the sale of goods. IAS 18 further states that the outcome of a transaction can be estimated reliably when all the following conditions are satisfied:

(a) The amount of revenue can be measured reliably.

(b) It is probable that the economic benefits associated with the transaction will flow to the seller.

(c) The stage of completion of the transaction at the end of the reporting period can be measured reliably.

(d) The costs incurred to date for the transaction and the costs to complete the transaction can be measured reliably.IAS 18 does not prescribe one single method that should be used for determining the stage of completion of a service transaction. However the standard does provide some examples of suitable methods:

(a) Surveys of work performed.

(b) Services performed to date as a percentage of total services to be performed.

(c) The proportion that costs incurred to date bear to the estimated total costs of the transaction.If it is not possible to reliably measure the outcome of a transaction involving the provision of services (perhaps because the transaction is in its very early stages) then revenue should be recognised only to the extent of costs incurred by the seller, assuming these costs are recoverable from the buyer.

In the UK UITF40 and SSAP9 defined the way we report revenue and profit in relation to Services, although accountants and lawyers were among the most high profile casualties of the new regime back in 2005, which forced them to re-catagorise WIP and Revenue, many other service providers also had to consider how they accounted for income. Professionals such as surveyors, architects, doctors and dentists all had to consider the impact of the new rules on their tax liabilities.

FRS102 has not changed the rules.

steve@bicknells.net

Do you know how FRS102 is changing Currency Conversion?

FRS102 affects many things and Section 30 sets out the rules on Currency Conversion.

FRS 102 states that

An entity can conduct foreign activities in two ways. It may have transactions in foreign currencies or it may have foreign operations. In addition, an entity may present its financial statements in a foreign currency

Entities will have a Functional Currency (a concept also used in IFRS) and it allows translation into a Presentation Currency

Reporting at the end of the subsequent reporting periods

30.9 At the end of each reporting period, an entity shall:

(a) translate foreign currency monetary items using the closing rate;

(b) translate non-monetary items that are measured in terms of historical cost in a foreign currency using the exchange rate at the date of the transaction; and

(c) translate non-monetary items that are measured at fair value in a foreign currency using the exchange rates at the date when the fair value was determined.

30.10 An entity shall recognise, in profit or loss in the period in which they arise, exchange differences arising on the settlement of monetary items or on translating monetary items at rates different from those at which they were translated on initial recognition during the period or in previous periods

That all sounds pretty familiar, however, as pointed out by Grant Thornton

Under SSAP 20 Foreign currency translation in current UK GAAP, where matching forward contracts are in place for a transaction, the contracted rate can be used for translation of the matched transaction. This option is not permitted under FRS 102. Instead, a foreign exchange forward contract will be recognised on the balance sheet as a financial instrument at fair value and the associated debtor or creditor will be retranslated at the year-end rate.

A key difference (FRS102) to note in comparison to SSAP 20 Foreign Currency Translation is that SSAP 20 regards consolidated goodwill as an asset of the parent company and not the subsidiary. [Steve Collings Blog]

Have you accrued for Holiday Pay correctly? Section 28 FRS102

Most larger businesses, especially if they are audited probably already accrue for Holiday Pay but not every business has been accruing the cost. FRS102 Section 28.1 will require that holiday pay is accrued. Here is an example from the FRC.

Holiday pay isn’t always easy to calculate for example if you have part time employees or casual workers, Gov.uk have a calculator to help work out the entitlement – GOV.UK Holiday Calculator

The next issue is the rate of pay, for some employees with regular hours its easy but for those with fluctuating rates, bonuses etc a 12 week average is used as explained by ACAS

On 4 November, the Employment Appeal Tribunal (EAT) ruled that holiday pay should reflect non-guaranteed overtime. Non-guaranteed overtime is where there is no obligation by the employer to offer overtime but if they do then the worker is obliged by their contract to work that overtime.

The Government set up a taskforce to consider the possible impact of the EAT’s ruling on holiday pay. Regulations were laid out on 18th December 2014 to limit claims for unlawful deductions from wages to two years. The rules apply to Employment Tribunal claims made on or after 1 July 2015.

Further details at ACAS Calculating Holiday Pay

steve@bicknells.net

When can you make a Prior Year Adjustment?

Until FRS102 basically an error had to be Fundamental for a Prior Year adjustment to be justified

This position is about to change with arrival of FRS 102. Paragraph 10.21 states that ‘an entity shall correct a material prior period error retrospectively in the first financial statements authorised for issue after its discovery’. This means that, on adoption of FRS 102, the threshold for correcting an error by use of a prior period adjustment has reduced from fundamental to material (ICAEW)

How will FRS102 affect your tax position?

FRS102 will affect us all, even small companies will be subject to a version of FRS102.

Its not just a reporting standard it will affect your tax position too, for example

Intangible Assets and Goodwill

Under FRS102 these assets will have a maximum life of 5 years where as UK GAAP allowed them to have an infinite useful life.

Distributable Reserves

There are various FRS102 changes that can effect these but one specific one is deferred tax which will be calculated on investment properties.

Operating Leases

Leases incentives will be spread over the entire life of the lease rather than to first break clause.

Asset Reclassification

Some assets such as Websites and software development could be reclassified as Intangible

Have you assessed the changes for your business?

FRS 102 is effective for periods beginning on or after 1 January 2015.

steve@bicknells.net