Home » Posts tagged 'Childcare'

Tag Archives: Childcare

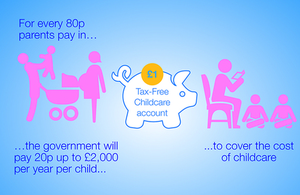

Tax Free Childcare from 2017

Tax-Free Childcare will be available to around 2 million households to help with the cost of childcare, enabling more parents to go out to work, if they want to, to provide greater security for their families.

In summary:

- The new scheme will start in early 2017

- You will open an online GOV.UK. Tax-Free Childcare account

- For every 80p paid in there will be a top up of 20p. The government will top up the account with 20% of childcare costs up to a total of £10,000 – the equivalent of up to £2,000 support per child per year (or £4,000 for disabled children). You or anyone can pay in whenever and whatever amounts you choose.

- Its available for children under the age of 12 or 17 if disabled

- Parents must be working and earning between £100/week and £100,000/year, there will be a 3 month checking process.

- Any working family can use Tax-Free Childcare, provided they meet the eligibility requirements. Its not dependent on your employer offering a scheme. Its also available to self employed parents and those of paid sick leave, SMP, SPP and Adoption leave.

- You will also have the option to continue with an employer supported scheme

- If you need to you can withdraw the 80p part paid in

You find more details at Gov.UK

steve@bicknells.net

Salary Sacrifice was “clarified” in April, does your scheme comply?

Salary Sacrifice is a very tax efficient way to give your employees benefits and the most popular benefits are Pensions and Childcare. I wrote a blog back in 2011 which explained how it can save 45.8% in tax and NI

HMRC decided on 9th April 2013 that it was time to “clarify” in their Manuals what are successful and unsuccessful salary sacrifice schemes and have added some further guidance. Their Staff are instructed not to approve schemes (Employment Income Manual EIM42772)….

You (HMRC) may get requests for advice:

- on how to set up a salary sacrifice arrangement, or

- on whether draft documentation will achieve a successful salary sacrifice.

You (HMRC) should not comment on either of these areas. Salary sacrifice is a matter of employment law, not tax law. The nature of an employee’s contract of employment is a matter for the employer and employee.

The specific updates are:

EIM42750 – Salary Sacrifice – updated – this contains the examples of schemes

EIM42777 – Contractual arrangements – this has interesting comments on childcare and pensions

- If the scheme involves childcare or childcare vouchers then the conditions for exemption must be met. (See EIM21905 and EIM16057). Is the agreement to provide childcare between the employee and the childminder or nursery. If so the employer by paying the cost directly is meeting the employee’s personal liability. (See EIM00580).

- For a registered pension scheme the amount which can be contributed to the scheme is normally linked to the employee’s chargeable earnings. In consequence if the salary sacrifice results in some of the employee’s income no longer being taxable, then the amount of contribution, which can be made to the scheme, will also drop.

EIM42778 – Exemption from Tax/NIC – basically stating that exemption may require that the sacrifice may be available to all employees but that the sacrifice must not reduce the employees wages below National Minimum Wages

The following is an example of an unsuccessful Childcare Salary Sacrifice:

The pay slip for the month ended 31 July 2006 gives monthly pay as £2000 plus overtime of £100, deductions for tax of £355 and NIC. The pay slip for the following month shows monthly pay of £2000 plus overtime of £100, deductions for NIC, childcare vouchers of £200 and tax of £310. The code number operated on the salary has not changed.

The situation is not clear from the payslip. When asked, the employer explains that for August, because childcare vouchers of £55 a week are exempt, £220 of vouchers has been deducted from the gross pay of £2100 and tax charged on the net figure of £1880. Further information is needed, for example a copy of the employment contract and any variations agreed by the employer and employee to that contract.

It is established that in July the employee bought childcare vouchers. The employer was not involved. The employer accepts that as the childcare in July was not provided by him, no tax exemption is available. In August the employee asked the employer to buy the childcare vouchers to take advantage of the exemption. The employer did this and deducted the cost from the monthly salary. The contract of employment shows that the employee is entitled to a base salary of £24000 to be paid monthly. This contract has not been varied. As the employee’s entitlement has remained the same, this is not a successful sacrifice. (See EIM42766).

If you operate salary sacrifice schemes its worth checking that your schemes comply, the tax consequences of failure to comply could be substantial.

steve@bicknells.net