Home » Posts tagged 'cash-flow'

Tag Archives: cash-flow

Why alternative finance could be the key to growth

MarketInvoice is the leading online invoice trading platform. They offer fast, flexible cashflow solutions to help businesses grow. Piers Garthwaite from MarketInvoice talks us through the opportunities alternative finance provides growing businesses.

The problem of funding for growing businesses is an all too common one. For any company to grow it needs medium-term financial support to hire new staff, increase supply, buy more equipment, move to a larger office etc. In this blog, we look at the options your client has to fund their business and why alternative finance could be the key to growth.

There are several ways clients can fund growth for their business:

- invest previous profits back into the business

- take out a loan

- raise equity

- look for other sources of finance

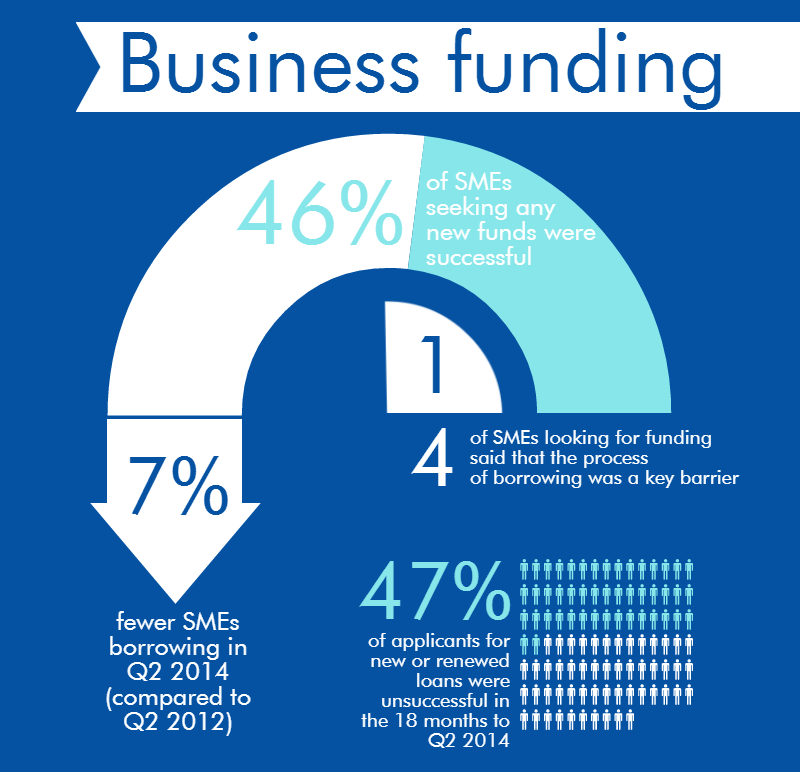

The majority of businesses’ first port of call will be to ask their bank for a loan. As we can see from the infographic, banks are not particularly keen on loans at the moment, given the economic environment.

52% of small businesses say that the availability of credit is “poor” or “very poor” and around half say that credit is unaffordable. In the same period, net lending to SMEs is down at -£400m.

This has been a long-term trend: businesses don’t want the products and banks aren’t keen on offering them. The banks’ policy of belt-tightening has affected growing businesses across the UK.

“So how,” we hear you ask, “am I to help my clients?”

Selling equity instead of a obtaining a loan is one option, but there are a number of disadvantages to this, chiefly your client giving up some control of their company.

Other sources of finance could be a grant, an overdraft (although this is unlikely to be big enough to cover any significant expense), leasing and asset finance, invoice factoring or discounting and, what we will be looking at in this blog, alternative finance.

Firstly, some statistics

The size of the alternative finance market is £1.74 billion. When compared with the banks this is, of course, a drop in the ocean. However, the market has been growing at over 150% year-on-year. The peer-to-peer (P2P) business lending market alone is £750 million and has grown at an average rate of 250% in the past three years. Online invoice trading sits at roughly £300 million, with a growth rate of 174%.

Alternative finance has now matured and is mounting an ever-growing assault on outdated, slow and fee-heavy traditional finance.

The industry-leading Nesta report backs up these findings. 33% of P2P business borrowers believed they would have been unlikely to get funds elsewhere. 63% also said that they saw a growth in profit and 53% saw an increase in employment.

What are the main draws?

For many, the main draws are what define alternative finance against the painful and outdated traditional banking experience:

- Speed: it can still take up to 6 weeks to get a loan. Alternative providers use technology to build automated credit scoring systems. With the amount of data available online, there is no reason for a business to have to wait more than 24 hours to be accepted (or declined) for finance.

- Simplicity and transparency: Standard contracts for bank finance are long and often have charges hidden in the Ts & Cs. Alternative finance tends to be more flexible and more transparent on everything, especially pricing. Most leading alternative finance providers have simple online tools to show how much your client will be charged dependent on the terms you choose.

- Service: Most alternative finance providers are run by entrepreneurs and so they have a natural propensity to understand the concerns and aspirations of small business owners looking to grow their business.

For a growing business to be able to access funding within 24 hours, instead of six weeks, could be crucial to its future success in the modern digital age. Additionally, being able to understand exactly what your clients are getting and at what price will help immensely with financial planning at such a critical stage of a business’ life.

Having explored some of the options available to your client, we hope it’s clear there is a plethora of funding opportunities on offer for small businesses.

You don’t need to be at a loss when considering funding options, even if the banks have said no. Financial support can be fast, simple and accessible and, therefore, the lifeline that a growing business needs at a crucial developmental stage.

If you’d like to find out more, visit MarketInvoice’s website or give them a call on 0845 548 0508.

Twitter: @MarketInvoice and @piersgarthwaite.

Get HMRC to pay you

HMRC will pay you interest

It is not that well-known that HMRC will pay you interest on tax paid early. The interest rate is only 0.5% though, so it isn’t going to change your life.

In the case of Corporation Tax, any payment is due 9 months and a day after your year-end. If you have a business bank account that pays no interest and the cash to pay your tax early you can pay your tax as soon as you have filed your return. After the 9 months is up HMRC will send you the interest calculated.

What spare cash?

See my earlier post on paying your debts first. In the situation where you have cash in the bank that you aren’t putting to good use and no outstanding debts paying your tax liability early will yield a small benefit.

Get your tax return done early

It is difficult to plan your cash flow if you don’t know how much tax you are due to pay. Even if you don’t want to pay your tax early, it is helpful to know how much cash you will need to set aside. The later you leave it to file your tax return the more pressure you can end up putting on your cash flow. More importantly the later you leave it, the more pressure you put on your accountant. Most accountants increase their fees as tax deadlines approach – or to put it another way you are likely to get a discount for starting early!

Don’t be late!

It won’t surprise anyone that HMRC will charge interest on late payments. The interest rate isn’t the measly 0.5% mentioned above but is currently 3%. As Bank of England rate increases – expect this to increase too!

For support and advice on preparing your annual accounts and filing your tax returns contact Alterledger or visit the website alterledger.com.

Should you start your own business?

Economy in recovery

It now looks like the UK economy is in recovery. Even if this isn’t the case, when people think that times will get better they start to spend money again. With interest rates at historic low rates there is little incentive to stockpile cash in the bank for consumers and for entrepreneurs debt is relatively cheap to finance a new venture.

No Change for Currency (Photo credit: Wikipedia)

What’s your plan?

If you are starting a new business, it is important to work out what you will be selling, but to survive the early days of a start-up you will need good projections of your cash flow. As you grow you may need investment from banks or other third parties. Without good quality management accounts is it more difficult to persuade a potential investor to part with their cash.

Ask for help!

You can’t do everything on your own. Work out what your core activities are and how much time you need to do them. If you have time left over for ancillary activities then you are better completing these yourself too. The cost of hiring specialist help, whether it be an accountant, web designer or lawyer can seem to be too much for a nascent company to bear. However if you are spending so much time working out your accounts that you don’t have time for your customers you will cost yourself more in the long-term.

Business booming in Scotland

According to this article from the BBC more Scots are starting up their own business. Records from Companies House show that more than 340,000 companies were formed in Scotland last year. Glasgow and Edinburgh are at the forefront of the economic recovery in Scotland. If you have a good business idea, now could be the time to let that idea take form, especially if you have a service that supports other new businesses.

Give yourself a break

To give your business the best start, make sure you understand your finances. Don’t forget that if you registered a company you are obliged to file accounts with Companies House as well as HMRC. For more information on company formation see my blog here.

For support and advice on the finances of your business contact Alterledger or visit the website alterledger.com.

20 ways to improve cash flow

Cash is vital to you and your business, lack of cash kills businesses.

So how can you improve cash flow:

- Prepare a detailed cash flow forecast, schedule your direct debits and standing orders, knowing how much cash you need and when will help you focus on where the cash will come from

- Invoice your clients as soon as you can, often small businesses invoice late and this just lengthens the time it will take to collect payment

- Get stage payments on large contracts

- Negotiate payment terms with your suppliers, try to at least match the client payment terms with the supplier terms

- If you are able to spread payments do it, for example, most insurance companies will offer you that chance to spread the payments over 10 months

- Adopt ‘just in time’ for stock items, don’t carry more stock than you need to

- Pay sales commissions only after the client has paid

- Change weekly payrolls to monthly where possible

- Sell assets you don’t need

- Sell obsolete and slow moving stock

- Consider paying mileage allowances rather than owning company cars

- Chase your debts

- Get a good credit rating as it will help you negotiate better supplier terms

- File your accounts and tax returns on time to avoid penalties

- Credit check your clients and agree terms based on their credit history and rating

- Diversify to smooth out seasonal trends

- Control your costs and reduce them where possible

- Make cash collection a KPI for your business

- Finance your fixed asset purchases

- Use Invoice Finance if your clients demand long terms

steve@bicknells.net

The Cash Cycle – What is it? what is your Cycle? How can you improve it?

As the saying goes, Sales are Vanity, Profit is Sanity and Cash is King. The Cash Cycle also known as the Working Capital Cycle helps you to quickly understand how much cash you need to run your business.

Here is a great example from Steve Grice for an average business

| Average time to collect payment from customers | 60 days | Add |

| Average days sales held in stock | 25 days | Add |

| Average days taken to pay suppliers | 35 days | Subtract |

| Cash cycle | 50 days |

http://stevegrice.wordpress.com/2012/02/06/working-capital-cycle/

Here is a brilliant Cash Flow Improvement Tool from NAB http://oms.nab.com.au/media/10/power_of_one/CF.html

This model quickly and easily calculates your cash cycle but also shows the effect of making improvements.

Having discovered what the cashflow cycle is, what can you do to improve it? well that depends, assuming you have agreed the best possible terms with your suppliers, you need to find ways to speed up cash received from Customers, if your business Sells to other businesses the first thing to look at is Credit Management.

CIMA have produce a comprehensive guide http://www.cimaglobal.com/Documents/ImportedDocuments/cid_improving_cashflow_using_credit_mgm_Apr09.pdf.pdf

But Credit Management may not be enough on its own, perhaps Invoice Finance might help?

Invoice discounting is an excellent, cost-effective way for certain businesses to improve their cashflow position.

- Invoice discounting is most suitable for businesses with good financial controls in place and a strong financial background.

- Invoice Discounting is ideal if you have an annual turnover above £500,000

- Invoice discounting is suitable for business with an established credit control department.

- Invoice Discounting is suitable for a wide range of businesses including manufacturers, wholesalers, transport firms, employment agencies and providers of some business services.

- Suitable businesses for invoice discounting are growing businesses because the level of funding grows in line with increasing sales.

If your business sells to end customers you might consider Card Processing Advances.

You must be masterful. Managing cash flow is a skill and only a firm grip on the cash conversion process will yield

results.

steve@bicknells.net

12 ways to get your invoices paid faster

- Discuss credit terms with your new client – set the expectation

- Change your credit terms to be less than they are right now – research has shown that invoices are paid 2 weeks late. So better to be paid late on short credit terms than late on long credit terms

- Get invoices out on time – be clear about what makes a service or product billable and bill it. Don’t be shy about billing promptly, the client has had the service\product, they need to pay for it

- Make it standout – clients processing lots of invoices may put it on the pile with the rest, but if it stands out then chances are that it will get paid faster

- Be able to report your aged debtors and then chase the late ones rigorously. Send a statement and call them – some people get so much email that it gets ignored

- Add late payment charges – you can always reverse them but it will generate a conversation where you can re-iterate your priority to be paid on time

- Get the entity right that you are invoicing – if it is called Jupiter Construction Limited, don’t put JC limited on the invoice

- Make it get to the right person – does it need to go to the budget holder or accounts payable or both

- Do you offer multiple payment methods – cheque, bank transfer, paypal, debit card, credit card – the more methods the more likely you will get paid faster.

- Review the average days to pay for your clients and target the late ones – don’t treat all clients the same

- Delegate your credit control – if you are running the business and delivering to clients you won’t focus on this and a part time resource can

- Send electronic invoices with Pay Now feature – Xero cloud accounting does this

david@graceaccountants.co.uk