Home » Posts tagged 'alterledger.com'

Tag Archives: alterledger.com

A SRIT idea

Will Scottish taxpayers pay less?

From 5th April 2016 a new Scottish Rate of Income Tax (SRIT) will come into force in Scotland. Although is it currently anticipated that taxpayers in Scotland and the rest of the UK will pay the same rate of tax next year, it is likely that the regions will diverge in coming years as more power is devolved to Scotland.

Who is Scottish?

The criteria applied to determine Scottish taxpayers are based on where the individual lives, and not where they work or their feeling of national identity. All of the following would be classed as a Scottish taxpayer:

- WILLIES (Working In London Living In Edinburgh)

- Scottish Parliamentarians (regardless of where they live)

- People living and working in Scotland

- People living in Scotland and working across the border in Carlisle / Newcastle etc

Who decides?

HMRC are responsible for assessing whether or not someone is a Scottish taxpayer. Anyone that HMRC deems to be Scottish based on their principal residence will be issued with a new S tax code. Your payroll software should automatically process the SRIT for anyone with a new S code. As with student loans, it is not for the employer to use their own judgement about applying the SRIT. If an employee disagrees with their tax code, it for the employee to resolve this with HMRC. Employers must act on instructions from HMRC.

Do English employers need to do anything?

Even if your business operates exclusively in England (or any other region of the UK outside Scotland) you will need to comply with regulations as they apply to any of your employees who live in Scotland. Surprisingly, there is no legal obligation to inform HMRC if you move and although employers really ought to know where their employees live, it might not always be obvious, especially if an employee has more than one residence.

Common misconceptions

It is common to think that any of the criteria below qualify for Scottish taxpayer status, but it isn’t the case.

- National identity

- Place of work

- Where income is generated (eg property income in Scotland)

- Regular travel to Scotland

Will Scots benefit?

The costs of the SRIT are to be borne by the Scottish Government. HMRC currently estimates that the total costs of implementing SRIT will be in the range of £30 million to £35 million over the seven-year period from 2012-13 to 2018-19. This is split between IT expenditure of between £10 million and £15 million, and non-IT expenditure of £20 million. The additional annual costs of operating the SRIT will be between £2m and £6m. The lower estimate corresponds to a SRIT where Scots pay the same rate as the rest of the UK. If the SRIT diverges from the neutral rate of 10%, the costs rise in administering the tax regime in the UK including pensions, gift aid and disputes over residence.

Why is the SRIT being introduced?

Scotland as a whole is likely to be worse off as any difference in tax raised is offset by an adjustment to the block grant from Westminster. It is estimated that 2.6m people will be issued with an S tax code. The annual running costs are therefore less that £3 per taxpayer but it is a valid question to ask if it is a good use of taxpayer’s money if tax rates are the same across the UK. It is anticipated that after additional powers are introduced in 2017 the SRIT could be more progressive, meaning that wealthier individuals would pay a higher proportion of tax. For anyone thinking about their residence status and still had a choice, now is a good time to get advice on the best situation for you!

More information

For more information on the SRIT and for guidance on operating your payroll scheme, please contact Alterledger.

Related articles

New Childcare Vouchers from Autumn 2015

Childcare vouchers to be withdrawn for new employees

The existing benefits available in the form of childcare vouchers to employees will be withdrawn to new entrants in the Autumn of 2015. The current scheme saves National Insurance contributions for both employers and employees. Employees also save income tax.

English: British National Insurance stamp. (Photo credit: Wikipedia)

New scheme to start in Autumn 2015

The new scheme for childcare vouchers will not be as good for many employees who currently benefit from the current scheme, but where both parents work and are self employed, they can get the government to pay £2,000 towards registered childcare.

How do I set up childcare vouchers?

Childcare vouchers are set up through your payroll scheme and must be available to all eligible employees to receive the tax benefit.

Alterledger can help

For more information on saving employer’s national insurance and preparing for changes to childcare vouchers, contact Alterledger or visit the website alterledger.com.

Related articles

Who cares what you think?

Are testimonials worth anything?

Many websites include “testimonials” from “customers”, but do they have any worth? If you want to attract new business it is good to be able to publish positive feedback, which helps demonstrate the value that other customers find in your service. The problem is that if reviews are obviously edited and self-selected they are not obviously representative of the views of your customers. Single line reviews taken out of context can be particularly misleading!

Use external review sites

One of the best-known review sites is tripadvisor. The greatest strength of these reviews is that hotels and restaurants etc have no control over the reviews. They have the opportunity to respond to criticism, but can’t cherry-pick the best reviews to give a false impression. The Pensions Regulator website is keen to point out that “private sector organisations we link to are not endorsed by Government and are provided for information only”; however it is worth noting that they include a link to VouchedFor on their advice page for individuals and in their guide to finding an advisor for Pension Auto Enrolment.

VouchedFor

If you are looking for a hotel you would probably prefer to check tripadvisor rather than lot of different websites for reviews. VouchedFor works along similar lines to tripadvisor, but for Accountants, Financial Advisors and Solicitors. Professionals who have a listing on the site must confirm that they recognise the name / email address of any reviewer before the review is posted online. Just like tripadvisor the professionals can’t read the review until is online so they can’t edit out any negative feedback and poor scores.

Tim Alter appeared in the guide in The Sunday Telegraph on March 29th. You can also read all his great client reviews on his VouchedFor profile!

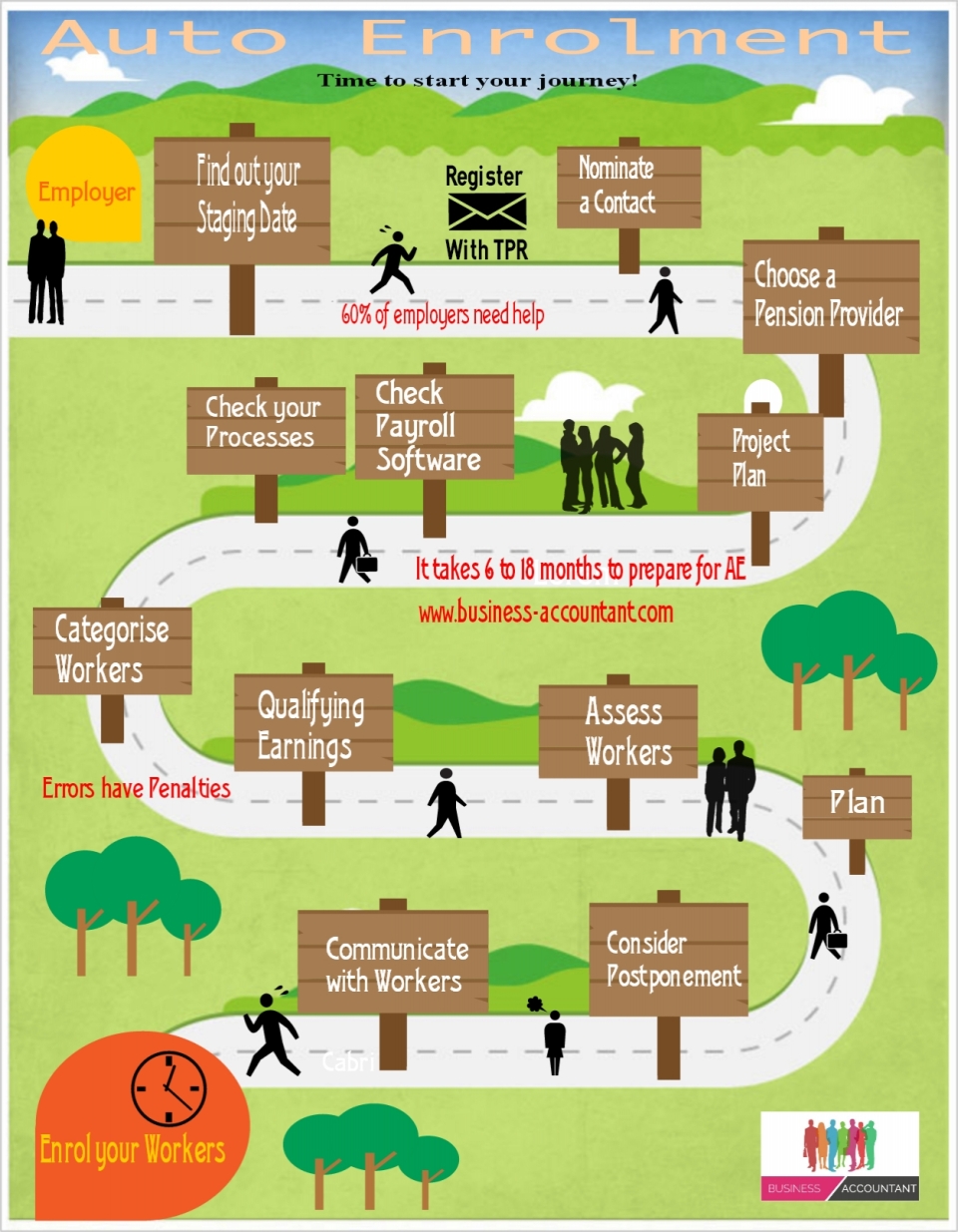

Auto Enrolment

Many small businesses will need professional advice to help them set up a pension scheme to comply with Auto Enrolment regulations. If you are an employer and still need to prepare for your staging date, you can use an Accountant or Financial Adviser to guide you through the process. For help with setting up your payroll and preparing for your staging date, please contact Alterledger.

Related articles

Letters for under 21s

Changes for employees under 21

From 6th April 2015 employer national insurance contributions will be abolished for under 21s. If you employ anyone over 16 and under 21 years old you will need to use one of the new letters for under 21s in the national insurance category setting of your payroll software.

English: British National Insurance stamp. (Photo credit: Wikipedia)

Secondary contribution rates

This table shows how much employers pay towards employees’ National Insurance for tax year 2014 to 2015. The contribution rate calculated by your payroll software is set by the category letter.

| Category letter | £111 to £153

a week |

£153.01 to £770

a week |

£770.01 to £805

a week |

From £805.01

a week |

|---|---|---|---|---|

| A | 0% | 13.8% | 13.8% | 13.8% |

| B | 0% | 13.8% | 13.8% | 13.8% |

| C | 0% | 13.8% | 13.8% | 13.8% |

| D | 3.4% rebate | 10.4% | 13.8% | 13.8% |

| E | 3.4% rebate | 10.4% | 13.8% | 13.8% |

| J | 0% | 13.8% | 13.8% | 13.8% |

| L | 3.4% rebate | 10.4% | 13.8% | 13.8% |

National insurance categories

Most employees will have a category letter of A or D depending on whether or not they are in a contracted-out workplace pension scheme. There are categories for mariners and deep-sea fisherman; the more common categories are shown below:

Employees in a contracted-out workplace pension scheme

| Category letter | Employee group |

|---|---|

| D | All employees apart from those in groups E, C and L in this table |

| E | Married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| L | Employees who can defer National Insurance because they’re already paying it in another job |

Employees not in contracted-out pension schemes

| Category letter | Employee group |

|---|---|

| A | All employees apart from those in groups B, C and J in this table |

| B | Married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| J | Employees who can defer National Insurance because they’re already paying it in another job |

Employees in a money-purchase contracted-out scheme

This kind of scheme ended in April 2012 but some employees might still be part of one.

| Category letter | Employee group |

|---|---|

| F | Tax years before 2012 to 2013 only: all employees apart from the ones in groups G, C and S in this table |

| G | Tax years before 2012 to 2013 only: married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| S | Tax years before 2012 to 2013 only: employees who can defer National Insurance because they’re already paying it in another job |

How to claim zero rate of employer contributions

You should already have proof of age for all your employees. A copy of a passport, driving licence or birth certificate will be required to show that your employee qualifies for the new zero rate of employer’s contribution. The seven new categories are valid from 6th April and must be applied from the first salary payment after 5th April 2015 to benefit from the new zero contribution rate for employers.

What does this have to do with Auto Enrolment?

You need to have proof of age for all your employees aged under 21 to claim the zero contribution rate for employer’s National Insurance. By the time of your staging date you must assess all your workers, based on their earnings and age. To help you prepare for Pension Auto Enrolment you can make sure that all your employee records are up to date and that your payroll software has the full details for all workers including their date of birth. This is a good opportunity to clean up all your employee data.

Alterledger can help

For more information on saving employer’s national insurance and preparing for Pension Auto Enrolment, contact Alterledger or visit the website alterledger.com.

Related articles

Say goodbye to small earnings

Say hello to small profits

HMRC has changed the name of the threshold for paying Class 2 National Insurance from the Small Earnings Limit to the Small Profits Threshold. If you earn less than £5,965 in 2015-16 you won’t need to pay Class 2 NI, but if you do, it will be calculated as part of your 2015-16 tax return and due with the rest of your tax by 31st January 2017.

English: British National Insurance stamp. (Photo credit: Wikipedia)

Alterledger can help

For more information on filling in your tax return, contact Alterledger or visit the website alterledger.com to see if you can organise yourself better and cut your tax bill.

Related articles

What a difference a day makes

How about three extra days?

HMRC has relaxed the rules on “Real Time Information” for payroll reporting. UK employers are required to send electronic reports to HMRC with each payment of wages to employees. HMRC are now saying that you can submit your RTI report up to three days after the payment date without incurring a penalty.

Any employer who has received an in-year late filing penalty for the period 6 October 2014 to 5 January 2015 and filed within three days, should appeal online by completing the “Other” box and add “Return filed within 3 days”.

Outsource your payroll

Despite the relaxation provided by three extra days, the burden on employers is only likely to increase over the coming months. Auto enrolment is being rolled out to all UK employers over the next couple of years. With the new payroll year about to start on 6th April, now is a good time to consider using a payroll bureau – or at least checking that your current systems will deal effectively with auto enrolment pensions. For more information please and see how Alterledger can help please click here.

Related articles

Pension annual allowance

Carrying forward unused pension annual allowance

Money that you pay into a UK registered pension scheme or qualifying pension scheme receives tax relief. Personal pension contributions are paid from your earnings after tax and the pension provider reclaims the 20% tax suffered. All employers will soon be required to offer pension schemes to employees, so now is a good time to think about what you can contribute to your pension scheme.

Embed from Getty Images

Anyone can make (gross) contributions each year of £3,600, but above this threshold the maximum you can put into the fund is 100% of Net Relevant Earnings (NRE). Tax relief on contributions is only available up to the Annual Allowance (including any Annual Allowance carried forward).

| Tax Year | 2011/12 £ |

2012/13 £ |

2013/14 £ |

2014/15 £ |

|---|---|---|---|---|

| Annual Allowance | 50,000 | 50,000 | 50,000 | 40,000 |

Carry-forward relief

Any unused annual allowance can be carried forward provided you were a member of a registered pension scheme, or qualifying overseas pension scheme during the year. The carry-forward relief can be used for any unused allowance from the previous 3 tax years. Assuming you were a member of a pension scheme, but didn’t have any contributions (personal or employer’s) in the tax years from 2011-12 up to 2013-/14, it would be possible to have total contributions of £190,000 in 2014/15.

Net Relevant Earnings

- Earnings from employment

- Benefits in kind

- Self-employed profits as a sole trader

- Share of profits from a partnership

- Any profit from furnished holidaylettings

- Less allowable business expenses

Alterledger can help

Alterledger can explain the tax implication of pension contributions for employers and individuals. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Employers and their staging date

Staging Date

A process started in 2012 which means eventually, all UK employers will be obliged to enrol all their eligible employees into a contributory pension scheme, known as Auto Enrolment. This obligation is already being phased in, starting with the biggest employers. The commencement date for an employer’s obligation to provide a contributory pension scheme is known as the staging date.

The government has said that no small employers (those with fewer than 50 employees) will be affected before the end of the current Parliament. The general election will be on 7th May so we are nearly there. Employers will be able to meet this obligation in any way they choose, but one way will be through a government-sponsored National Employment Savings Trust ( NEST ), a simple, low-cost scheme with very limited fund choice, and initial restrictions on transfers and contribution levels. NESTs will be operated by the NEST Corporation, a not-for-profit trustee body, and will be regulated by the Pensions Regulator.

Alterledger can help

Alterledger can help you prepare for your staging and manage your auto enrolment process along with your payroll once everything is up and running. Contact Alterledger or visit the website alterledger.com for more information.

Related articles

Self Employed National Insurance

Changes to payment of National Insurance

HMRC has announced changes to the way that the self-employed will pay their Class 2 and Class 4 National Insurance Contributions (NIC). This is not the first time the process has changed. Some people still refer to paying their stamp – in days of old you had to buy special stamps for your NIC!

English: British National Insurance stamp. (Photo credit: Wikipedia)

No new direct debits

Until recently I would have encouraged the self-employed to set up a Direct Debit Instruction (DDI) with HMRC to pay their Class 2 NIC. From April 2015 HMRC will calculate the NIC due from your self-assessment tax return.

Deferment of National Insurance Contributions

If you currently defer NIC, you don’t need to re-apply to do so. HMRC will be sending out letters in December to everyone who currently defers NIC to confirm this. Any new applications to defer NIC will not be processed. For more information on National Insurance for the Self Employed please go to my blog post here: Class 2 NIC.

Alterledger can help

For more information on filling in your tax return, contact Alterledger or visit the website alterledger.com to see if you can organise yourself better and cut your tax bill.

Related articles

Orchestra Tax Relief

New Creative Industries Tax Relief

The 2014 Autumn Statement from the UK Chancellor included a proposal for a new Orchestra Tax Relief.

FHM-Orchestra-mk2006-01 (Photo credit: Wikipedia)

Orchestra Tax Relief

Many orchestras are charities and therefore don’t pay Corporation Tax, but any that do pay tax may qualify for a future Orchestra Tax Relief. The tax break proposed yesterday will be going through a consultation process, so if you have an interest get involved!

Other Creative Industries Tax Reliefs

For more information on the tax reliefs for Orchestras, Theatres, Animation, Video Games and High End TV please go to my blog post here: Orchestra Tax Relief.

Alterledger can help

Why wait for the law to favour your industry? Contact Alterledger or visit the website alterledger.com to see if you can organise yourself better and claim more expenses to cut your tax bill.