Home » Uncategorized (Page 6)

Category Archives: Uncategorized

How to get paid – Part 2

This post is a follow on from ‘How to get paid – part 1’ so if you haven’t read that you might like to do so before reading this one!

Once you have decided on your payment terms, ensured that both you and your client understand what is to be delivered, and paid for your services, there is still the possibility that a client will let you down and not pay.

The most likely scenario is that the client is strapped for cash and you are not seen as the first payment priority for them. This is a difficult position to be placed in for any service provider. My advice is that you must stand firm and by doing so you may well move yourself up the payment list – especially if the client is looking for further work from you.

Just as an aside, I generally provide an ongoing service to clients and so agree with them a fixed price service, so they can set up monthly standing orders. This has proved to be a win/win strategy. Clients like it because payments are broken down into monthly bite sized payments and I like it because I don’t have to do monthly invoices and then chase for payment.

However, what I did not appreciate until a client pointed it out to me was that, for them, my payments had moved up into the ‘unavoidable’ category – along with rent, rates, electricity etc. Unlike other professional service bills which are paid as and when money is available, my payment is made as one of the first.

Now, many service providers get lulled into doing more work for a client who is not paying, because they believe that they will not be given further work if they insist on being paid. As in my previous blog I would most strongly urge you not to get into this way of thinking. Firstly, the surest way of getting paid for work done is to stop working until payment is made. Secondly, if the client is bad at paying why would you want further work from them – rather than using your limited time to work for a client who will pay!

If a client is unlikely to use your services again, you are in a psychologically stronger position. You may well not be so reticent in sending tough letters demanding payment. Or, in fact, starting legal proceedings. If you want to go down this route it is very important that you understand what your rights are and how best to proceed. My advice would be to use a payment collection service such as that provided by companies like Credebt. They take the hassle away and enable you to concentrate on more positive areas in your business.

Finally, as I said in my earlier blog, don’t be coy about collecting money owed to you. As long as you have done the job required, and to the standard agreed, you are entitled to be paid!

Fiona 🙂

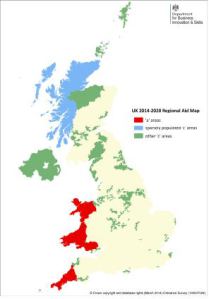

Business Premises Renovation Allowance

The Business Premises Renovation Allowance (BPRA) finishes in 2017 and is a great relief! Changes have been made to the relief to target it more effectively. Additionally the period for balancing adjustments has been reduced from seven to five years.

BPRA is aimed at the renovation of empty business premises, which have been empty for at least 12 months and which are located in an assisted area. See Assisted Areas Map below from the Gov.uk website:

Capital Expensiture must meet conditions A and B, and must be incurred before the expiry date. Also certain exclusions aply.

Condition A

The expenditure must be incurred on:

The conversion of a qualifying building into qualifying business premises.

The renovation of a qualifying building, provided it is or will become qualifying business premises.

Repairs to a qualifying building, or part of a qualifying building, provided those repiars are incidental in nature to that incurred…

View original post 153 more words

Billy No Mates Christmas Bash 2014

I am just in the process of organising the Billy No Mates Christmas Bash for 2014.

As usual it is on the last Friday before Christmas – this year 19th December – at Beah, Union Street, Wells, Somerset. It starts at 12pm, for sit down at 12.30pm, and usually goes on well into the afternoon.

If you have been before you will know it is the office Christmas party for those of us who work on their own – or just with one other. It’s a wonderful opportunity for a pre-Christmas hair let down with like-minded business owners over a glass of wine, a superb meal and a couple of party poppers!

If you haven’t been before – why ever not?

All the details – including the menu – are on the www.billynomates.info website, just click on Wells Christmas Bash.

If you don’t live in Somerset but fancy the idea of having your own Billy No Mates bash the website also gives you some tips on how to do so. If you want us to include it on our site it all you have to do is send the details and menu to fiona@fionabevanfinancialmanagement.co.uk and we will upload it.

How to Get Paid – Part 1!

I often come across service providers who are finding it difficult to get paid. This got me thinking about the psychology of payment.

There are clearly two sides to this particular coin – us and the client. We can be as much, or more, to blame as our customers for not getting paid, because of the way we think and act.

Firstly, as Brits we are sometimes embarrassed to talk to clients about fees and payment. Some business owners hide behind hourly rates, which means there is no upfront agreement about exactly what the client will be expected to pay. This means it is highly likely there will be disagreement and therefore delay in payment. Not only that, but disagreement about fees can leave a bad taste in everyone’s mouth.

Secondly, many service providers are slow to invoice, which means clients receive bills quite a long time after they have had the service. This sends a message to the client that the supplier is probably pretty well off and so doesn’t need the cash quickly (or the invoice would have been sent more promptly). Consequently it is more likely that payment will need to be chased.

Other suppliers do not make it clear what their payment terms are. Now, it is in clients interests to delay payment as long as they can (especially at the moment when many businesses are finding cash flow difficult) so if you are not clear on payment terms you cannot be surprised when payments don’t come through. Make sure your letter of engagement clearly states what your payment terms are and re-iterate these terms on your invoice.

Further to payment terms ask yourself the question ‘Am I a bank?’ If the answer is no (as I expect it is for anyone reading this blog) only give credit if it is absolutely necessary – and then ensure there is some allowance for interest in the price you are quoting! Otherwise, make your payment terms ‘payment on receipt of invoice’. You probably won’t get paid immediately but at least you can chase earlier.

I know business owners who don’t like chasing for payment, even if they have agreed a fixed price, invoiced promptly and have clear payment terms, because they think their good clients will think badly of them. This, in my opinion, is the worst ‘sin’ of all. Firstly, GOOD clients pay as agreed in the contract – a good client is not one who bitches about the agreed price and then fails to pay promptly. Secondly, we are business people who should expect to be paid for a good job done, so there is nothing to be coy about when it comes to asking for what you are legally and morally entitled to!

So, to recap:

1. Agree clearly with your client the exact terms of the engagement both in terms of job to be done and fee to be paid.

2. Bill as soon as the job is complete.

3. Be clear on your payment terms and give as little credit as possible.

4. Be professional! If money is owed to you do not be coy about chasing for it.

Fiona 🙂

October is going to be a busy month for PAYE

It seems now more than ever is the time to make sure you are on top of your payroll each month with some noteworthy changes in October:

Increase in National minimum wage from 1st October

Over 21 – £6.50 p/h

18-20 – £5.13 p/h

16-17 – £3.79 p/h

Apprentice – £2.73 p/h

Then an even bigger change: PAYE late filing penalties

From 6th October, All employers with 10 or more employees and all new businesses set-up for PAYE in the 2014-15 tax year must be up to date with their RTI submissions, as from this date and after the first late submission in a tax year, each subsequent late submission will be charged as follows:

1-9 employees – £100 – This is not being enforced until 5 March 2015 but is worth bearing in mind.

10-49 employees – £200

50-249 employees – £300

250+ employees – £400

The following daily interest rate charges will also be applied to all outstanding employer payments not paid in full and on time:

- 1-3 late submissions will be charged as 1% of the last estimated monetary value

- 4-6 late submissions will be charged as 2% of the last estimated monetary value

- 7-9 late submissions will be charged as 3% of the late estimated monetary value

- 10 or more late submissions will be charged as 4% of the late estimated monetary value

If you have still not paid a monthly or quarterly amount in full, after six months you will have to pay a penalty of 5% of the amounts unpaid. With a further 5% penalty after 12 months. These are in addition to the penalties above and apply even if only one payment in the tax year is late.

lauren@fullstopacccounts.co.uk

What flavour is your Accountant?

Thanks to http://www.freedigitalphotos.net

One of the great joys of working as a ‘CIMA MiP’ (“Chartered Institute of Management Accountants, Member in Pratice”) is that we are generally dealing with ‘small’ and ‘micro’ client firms (micro defined by EU regulations as firms with less than 10 employees/ £2m turnover; small defined as firms with less than 50 employees/ £10m turnover) and that we become involved in an enormous breadth and depth of subjects.

One of the less welcome challenges however is that as far as most small and micro business owners and managers are concerned, one accountant is the same as any other and this includes the myriad unqualified accountants who practice their particular brand of accounting services at rock-bottom rates. Indeed it is rare that I have been asked whether I am a ‘qualified’ accountant, and is rarer still that I am asked what that qualification is (in fact I cannot ever recall being asked that question by a client). The client generally assumes that because one calls oneself an ‘accountant’ then one can ‘do accounts’ and that accountants are all the same.

We’re not.

My particular practice specialises in manufacturing clients and most new clients have come from existing client referrals. Fortunately I do not need to be a great sales person to convert a prospect into a new client when (a). there is a recommendation from an existing client and (b). we appear to ‘speak the same language’. Clients generally put this down to my having owned and run manufacturing firms and to some degree that is true, but is is also because of my CIMA training.

If you’re looking for year end accounts, audit, or tax computation then you will likely be talking to a ‘Certified Accountant’ or ‘Chartered Accountant’, but where they will be reporting back to you on how well (or otherwise) you did overall last year and what your tax liability is, the CIMA ‘Chartered Management Accountant’ will be working with you to establish what activities made money and why, and whether you can do more of it, and of course which did not and how to avoid this in future; indeed the focus is very much ‘future’ as much as ‘past’.

In terms of the client business, it’s not difficult to see that helping the client to understand their business is a valuable element in managing, changing, and improving the business, and this is something which CIMA qualified people have to offer any business, so it’s a great shame that Chartered Management Accountants tend to be employed by big businesses who understand the difference between the different accounting disciplines.

None of this is to say that a Certified Accountant or Chartered Accountant could never do what the Chartered Management Accountant does, but it is not what they have been trained to do and equally as a Chartered Management Accountant in practice for twenty-two years I provide a ‘full service’ including year end accounts and tax returns for my clients, albeit the main focus remains helping them to improve their business.

I would urge Chartered Management Accountants to seriously consider a career in the small and micro business sector which accounts for 99.3% of the 4.7 million businesses in the UK (source: BIS 2013) and 47% of private sector employment (source: FSB 2013) and which is a vital part of the UK economy: whether in practice servicing a number of clients, or a full-time employee of a particular firm, I am sure that you will find the experience very rewarding

I would equally urge owners and managers in that sector to become aware of the differences between the main accounting bodies and the relative strengths of each, and to be sure that whoever they engage with will meet the needs of their particular business.

Paul Driscoll is a Chairman of CIMA MiPs in South West England and South Wales, a director of Central Accounting Limited, Cura Business Consulting Limited, Hudman Limited, and a number of manufacturing companies, and is a board level adviser to a variety of other businesses.

Danger – Bad Tax Advice!

Did you know that the information that HMRC give you is often incorrect?

A Civil Service Capability Review has found that one in four of us contacting HMRC is given incorrect or incomplete information. ONE IN FOUR!

That’s a massive problem.

The official message is that Self Assessment is easy, but it clearly is not true. Tax is complicated and it changes every single year. Even for small mounts of money, tax is taxing!

VAT Mini One Stop Shop (VAT MOSS)

How will the VAT Mini One Stop Shop (VAT MOSS) work?

You may opt to use the VAT Mini One Stop Shop (VAT MOSS) online service to save you having to register for VAT in every EU Member State where you supply digital services. This will be available from 1 January 2015, but you will be able to register to use it from October 2014.

If you are an EU business, you may register and use the VAT Mini One Stop Shop (VAT MOSS) online service in the Member State where you have your business. Using the VAT MOSS online service means you can submit a single calendar quarterly VAT MOSS return and payment covering all your EU digital service supplies. For example, if you register for the VAT MOSS online service in the UK, you will be able to account for the VAT due on your B2C digital service sales in any other Member States where you do not have an establishment by submitting a single VAT MOSS return and any related payment to HM Revenue & Customs (HMRC). HMRC will send an electronic copy of the appropriate part of your VAT MOSS return, and the related VAT payment, to each relevant Member State’s tax authority on your behalf. The VAT rate used will be that of each Member State of Consumption at the time the service was supplied.

Which is your team?

Well it’s all behind us now!

The World Cup with all its highs and lows is over and, as always, we find ourselves dissappointed at the results.

It occurs to me that this sporting event exemplifies many of the trials and tribulations businesses come across in trying to be successful. If you have a team full of players who are only interested in themselves as individuals, it is likely you will get poor results, even if the players seem to be very talented. However, if you have a team of players who are willing to sacrifice their personal status to further the team’s ambitions, the sum becomes greater than the parts and real magic can result.

Further, it is important that the team has a clear and common vision, which is driven through by the directors. If individuals in the team go in their own direction without reference to the vision, or ignore clear management guidance, the team as a whole will suffer.

So my advice is to look at your business and decide which team you would like to be.

Will your company resemble Brazil, Spain, or indeed England? Or will you be like Germany and hold the World Cup aloft?

Fiona 🙂

Employment Status Again!

The importance of “control” in determining the status of self-employed personel

A first Tier Tribunal recently considered the case of Gabriel Oziegbe, who engaged security personel for construction sites. HMRC decided that the personal engaged were AGENCY WORKERS and raised assessments for PAYE & NIC, against which Mr Oziegbe appealed and was successful.

There were two aspects of the appeal that stood out for me:

a) Part of the wording of Mr Oziegbe’s standard contract for services, not only reminded the contractors that they were responisble for thie own tax, he highlighted the fact that although he had some input in the quality and timing of their work he did not control their work (the full wording of this appears in the case report below)

b) His explaination , in tribunal that they had some freedom to operate for as few or as many clients as they wished and thus could affect the amount they earned.

Here is the fuller report of the case as reported by the ICPA:

| Mr. Oziegbe had trained and secured the required licence to act as a security guard and started to work for clients, generally construction companies in 2007. He engaged other similarly qualified security guards when he had work he could not perform personally, entering into Contract for Services agreements with them. The contracts included a number of key aspects normally found in a self-employment relationship including the following in relation to control:“I will not control or have any right to control how you undertake the services to be provided but I am entitled to lay down standards of quality and a time period within which the works must be completed at the commencement of any particular service. You will be obliged to act upon any assignment instruction provided by me.”During the hearing Mr. Oziegbe expanded on the terms of engagement stating that the workers would periodically leave to work entirely on their own account or with some other operator. His letter to HMRC sent in December 2011 was highlighted. In it he confirmed that the security guards he engaged were able to work for as many clients as possible and that he has no direct control while they are were engaged on a job and that they took the risks. The amount of profit they made was in their control. He also confirmed that the security guards had been advised to pay their own tax, and evidence was provided that this had been done for at least four of the people engaged.There was no cross–examination in relation to the contract or letter and the FTT accepted that the statements were broadly realistic. |

|

|

It strikes me that this illustrates the reality of many agents. They do in fact operate remotely from most of thier client’s operation and therefore cannot have a great deal of control over what any operatives do in a remote location.

Perhaps the wording of Mr Oziegbe’s contract and how he explains the position to his contractors is a lesson for anybody who feels that they are at risk from the new Agency Worker Regulations.

Stephen@stephenmilne.co.uk