Home » Small Business (Page 6)

Category Archives: Small Business

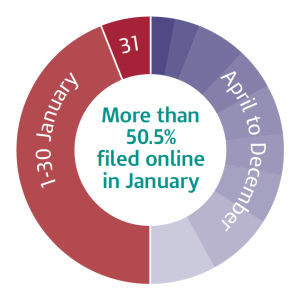

Have you filed your Self Assessment Return?

Last year, while millions of people were exchanging presents, feasting on turkey, and nodding off in front of the television, 1,548 people decided to take time out from the yuletide festivities and do their tax return online – a 40 per cent increase on Christmas Day 2011, when 1,100 people filed online.

The penalties for late Self Assessment returns are:

- an initial £100 fixed penalty, which applies even if there is no tax to pay, or if the tax due is paid on time;

- after three months, additional daily penalties of £10 per day, up to a maximum of £900;

- after six months, a further penalty of 5 per cent of the tax due or £300, whichever is greater; and

- after 12 months, another 5 per cent or £300 charge, whichever is greater.

There are also additional penalties for paying late of 5 per cent of the tax unpaid at: 30 days; six months; and 12 months.

Make sure you get yours done before the end of January!

steve@bicknells.net

Key Points from the Autumn Statement 2013

The Chancellor George Osborne presented the Autumn Statement to the House of Commons on 5th December 2013 and things are getting better, economic growth forecasts for this year have more than doubled from 0.6% to 1.4% but the austerity plan is set to continue.

Here is a summary of the key announcements:

Business Rates

Business rate increases in England will be capped at 2% in 2014/15 (they were set to increase by 3.2%) and businesses will be able to pay over 12 months rather than 10.

The Retail Sector will also get a £1,000 discount in 2014/15 and 2015/16, this applies to pubs, cafes, restaurants and charity shops with a rateable value below £50,000.

A reoccupation relief of 50% is being introduced for up to 18 months on premises that have been empty for a year or more and it will apply from 1st April 2014 to 31st March 2016.

Small Business Rate Relief has been extended to April 2015 under the scheme small businesses with a rateable value of £6,000 or less can get 100% relief, the relief is scaled down to zero on rateable values of £12,000 and there is a lower multiplier on rates between £12,001 and £17,999.

Income Tax

As previously announced the personal allowance will be £10,000 for the tax year 2014/15.

From April 2015, a spouse or civil partner who is not liable to income tax will be able to transfer £1,000 of their allowance to a basic rate tax paying spouse and as a result save £200 in tax.

State Pension Age

By 2020 it will be 66, by 2028 it will be 67 and by mid 2030′s 68, then in 2040′s 69.

Capital Gains Tax

The annual exempt amount will be £11,000 for individuals for 2014/15.

But there was an exemption for principle private residence letting for 36 months and from 6th April 2014 it will be reduced to 18 months.

Consultation will start in April on non-residents paying capital gains on property disposals.

Individual Savings Account (ISA)

The limit will rise to £11,880 for 2014/15 and of this £5,940 can be invested in cash ISA’s

Mortgage Guarantee Scheme

The scheme started in October will run for 3 years and end in January 2017.

Buyers will only need a 5% deposit and the government and the funder will guarantee 15% of the loan in return for a fee.

IR35

Legislation will be tightened from April 2014.

Anti-avoidance

A range of measures were discussed in addition to IR35 and these included:

- Partnership Tax

- Controlled foreign companies

- Charities

- High risk tax avoidance schemes

- Dual contracts

Other headline measures

- Employers NI for under 21′s to be scrapped in 2015

- Rolling back green levies to allow an average saving of £50 on energy bills

- Free school meals for infants

- Scrapping of 1% above inflation rail fare increases

- Electronic tax discs

- Abolition of next years 2p per litre fuel duty rise

steve@bicknells.net

VAT Simplified Invoices

HMRC have released an update this month to their notice on Keeping VAT records. One of these changes relates to VAT simplified invoices which were introduced earlier this year as part of the simplification and harmonisation of VAT rules in the EU. Previously only retailers were exempt from providing full VAT invoices to unregistered businesses.

However the changes mean that any business issuing VAT invoices for £250 or less (including VAT) can issue simplified invoices.

What to include in a simplified invoice:

Your name, address and VAT registration number

The time of supply (date)

A description which identifies the goods or services supplied

The each VAT rate charged, the amount of VAT charged.

How does a simplified invoice differ from a full VAT invoice:

In addition, a full VAT invoice must include:

A sequential number based on one or more series which uniquely identify the document

The date of issue (if different from the time of supply)

The name and address of the person to whom the goods or services are supplied

For each description, the quantity of the goods or the extent of the services, and the rate of VAT and the amount payable, excluding VAT, expressed in any currency

The gross total amount payable, excluding VAT, expressed in any currency

The rate of any cash discount offered

The total amount of VAT chargeable, expressed in sterling

The unit price

The reason for any zero rate of exemption.

VAT invoices over £250

If issuing VAT invoices over £250, a full invoice must still be issued or a modified VAT invoice showing VAT inclusive rather VAT exclusive values.

Rebecca Taylor ACMA

High Income Child Benefit Charge

The High Income Child Benefit Charge (HICBC) is a tax charge which repays part of the child benefit received by high earners earning over £50,000 to a 100% repayment for those earning over £60.000. It applies to child benefit received from 7th January 2013.

Who does it affect?

Who does it affect?

You may need to pay a tax charge if:

- you have an individual income over £50,000

- and either you or your partner receive Child Benefit or someone else gets Child Benefit for a child living with you and they contribute at least an equal amount towards the child’s upkeep.

It doesn’t matter if the child living with you is not your child.

What do you need to do?

If you are affected by the tax charge, you can:

- Stop receiving the Child Benefit (only recommended if you’re adjusted net income is over £60k). Follow this link for how to do this.

- Carry on receiving the benefit and pay any tax charge at the end of the tax year.

How to calculate adjusted net income?

It is important to realise that the income used to calculate the tax charge is your adjusted net income. You can use the calculator on Gov.uk to work out your adjusted income.

How to pay the tax charge

If the tax charge does apply to you, you will need to submit a self-assessment return to HMRC by 31st January following the end of the relevant tax year. Do not rely on HMRC writing to tell you that you need to submit a return as they may not realise you need to. Normal self-assessment penalties apply if returns are late or incorrect.

How much do you need to pay?

The charge is 1% of child benefit received for every £100 of income over £50,000 of adjusted net income. The charge will never be higher than the amount of child benefit received and if the income is over £60,000 the amount paid back to HMRC will be equal to the benefit received.

Rebecca Taylor ACMA

Fake email alerts from HMRC and Companies House

Fake email alerts from Companies House and HMRC have become increasingly sophisticated. There was a time when it was relatively easy to spot a fake email alert but even accountants have been caught out by recent fake email alerts. And it isn’t just Companies House and HMRC. Be careful of emails from banks, other institutions, postal services, voicemail services and even Skype. Previously harmful emails have tried to direct you to a fake website to steal your personal details but these recent emails have attachments which could harm your computer.

Fake email alerts from Companies House and HMRC have become increasingly sophisticated. There was a time when it was relatively easy to spot a fake email alert but even accountants have been caught out by recent fake email alerts. And it isn’t just Companies House and HMRC. Be careful of emails from banks, other institutions, postal services, voicemail services and even Skype. Previously harmful emails have tried to direct you to a fake website to steal your personal details but these recent emails have attachments which could harm your computer.

What to look for

These fake email alertss have an attachment which appears to support details in the email message. For example, it could claim to be a customer complaint from Companies House, a missed delivery or a bank transaction. The email address could give you a clue that it is a fake email alert but many now look like they have come from a genuine email address. Some fake emails have footers which have been obviously copied from another email. If you are not expecting an email from the sender, think twice before opening any attachments, particularly .zip files.

Why

These emails are all trying to get you to do one thing: open the attachment. The attachment invariably contains malware or a virus and will either damage your computer, steal your details or even demand a ransom (see an article from the National Crime Agency on Cryptolocker).

Advice

The National Crime Agency provides this advice:

This is a case where prevention is better than cure.

- The public should be aware not to click on any such attachment.

- Antivirus software should be updated, as should operating systems.

- User created files should be backed up routinely and preserved off the network.

- Where a computer becomes infected it should be disconnected from the network, and professional assistance should be sought to clean the computer.

- Various antivirus companies offer remedial software solutions (though they will not restore encrypted files).

Example of fake emails

Follow the links for some examples of fake emails:

5 ways to reduce the risk of a tax investigation

THE TAX YIELD derived from HM Revenue & Customs investigations into the affairs of small- and medium-sized companies rose by 31% over the last 12 months, according to UHY Hacker Young.

Compliance investigations into SMEs generated £565m for HMRC in 2012/13, up from £434m in 2011/12, with the year ending March 31. Accountancy Age

Some investigations are random and some as a result of HMRC task forces, but many are triggered by risk profiling.

What can you do to reduce your chances of being selected:

1. File your tax returns on time and pay what you owe – If you file late or at the last minute HMRC will think you are disorganised and as such there are more likely to be errors in the return

2. Declare all your income – HMRC get details of bank interest and other sources of income, sometimes they test them and match them to returns

3. Use an accountant – Unrepresented taxpayers are more likely to be looked at, mainly because many of them don’t know what they are doing

4. Trends – if your business doesn’t match the profile of similar business in the same sector or your results suddenly fluctuate it could raise concerns at HMRC, for example, if you suddenly request a VAT refund

5. Tax Avoidance Schemes – if you are using a tax avoidance scheme I am sure HMRC will be looking closely, if they can find a way to challenge the scheme then at some point they will

steve@bicknells.net

Interim or final dividend – does it matter which?

Dividends are used by many business owners as a tax-efficient way to extract profit from a company. So it is important to understand the procedure for paying them. But does it matter whether the dividend is final or interim if the tax treatment is the same?

The Companies Act 2006

It isn’t HMRC that makes the distinction between the two dividend types, but company law. The Companies Act 2006 says “The company may by ordinary resolution declare dividends, and the directors may decide to pay interim dividends”

So one group of people, the directors, may pay interim dividends, but shareholder approval must be obtained before a final dividend is paid.

So why is HMRC interested?

HMRC doesn’t particularly care which type of dividend is paid. It is interested in whether the payment is really a dividend or whether it was salary a bonus or a loan payment. As higher taxes and NI may accrue with these payments HMRC will want to see proof that the payment was a genuine dividend.

And this is where the timing of the payment and the paperwork are important. Under new anti-avoidance rules it is no longer possible for a director to receive a loan from the company, repay it to avoid the 25% tax charge and then take out a fresh loan within 30 days. HMRC will want to be certain that the payment is indeed a dividend. If the correct procedure has been followed and the paperwork is complete then this should not be challenged.

What fees does a barrister need to declare?

Special rules for barristers and advocates

Barristers are not permitted to provide their services through a limited company. All barristers have to register as self-employed and submit business accounts as a sole trader to HMRC. There are special provisions relating to cash accounting and the rules have changed in recent years meaning there are three different regimes that can apply. There are time limits for the cash accounting schemes so if you are in your first few years of practising you will need to make sure that you are reporting the correct figures to HMRC. Guidance is available from the Bar Council here.

A barrister on a mobile phone outside Southwark Crown Court.

(Photo credit: Wikipedia)

Cash Accounting

The Finance Act 2013 introduced the possibility of cash accounting for most unincorporated business including sole traders from 6th April 2013. Barristers already had a cash scheme available when they started their practice with permission to continue the same cash accounting principles for up to 7 years under the Finance Act 1998. This old cash scheme is no longer available to new barristers, but anyone who started preparing accounts under the old cash basis by 5th April 2013 can continue to do so until their seven years is up or they transfer voluntarily to another scheme. Once you have left the old cash scheme there is no turning back.

Barristers can join the new cash scheme where fee receipts do not exceed the VAT registration threshold (currently £79,000 per year). If receipts are more than twice the VAT registration threshold (currently £158,000) the barrister must leave the scheme.

The advantages of the cash schemes are that they are easier to administer so there is less need to engage an accountant to prepare your accounts. You only pay tax on fees received and you do not have make calculations at the year-end for work that is incomplete or invoiced and not yet paid by your clients. This means that your tax payments are delayed compared to the earnings basis below and will improve your cash flow. There are other aspects of the cash schemes which are explained in more detail here.

A barrister on the old cash scheme can elect to leave the scheme early, but the new cash scheme does not allow exit unless there is a “change in commercial circumstances”.

Earnings based accounting

UITF 40 requires that long term contracts are recognised in the year-end accounts to the extent that partly performed work is recognised as taxable income. This requires barristers to calculate the value of any Work In Progress (WIP) at the end of their financial year and include this in their total income.

Materiality is a key concept in accounting, but the materiality of the total WIP must be considered not just the materiality of each individual contract. It is not permitted to disregard a number of immaterial amounts if when considered together they are material to the accounts. In practice this means that almost all WIP is chargeable to tax under the earnings method. One of the few clear cut exceptions is a no fee no win case, where no WIP is to be recognised.

Transitional arrangements

When changing from either cash accounting scheme to the earnings based scheme a calculation of the WIP must be made which will increase the taxable income for the year. The old cash method allows the closing WIP at the time of the change to the earnings method to be recognised over a period of up to 10 years. The provisions under the new cash scheme have a reduced timeframe of 6 years. It is normally the case that anyone transferring from the old cash scheme to the new cash scheme would not need any adjustment to the annual accounts. There are corresponding adjustments for barristers transferring from the earnings scheme to the new cash scheme – explained in more detail here.

For more information on an accountancy firm that can set you up with online accounting and deal with all your business accounts and VAT – contact Alterledger or visit the website alterledger.com.

Useful links

| Bar Council Guidance | practice-updates-and-guidance/remuneration-guidance/ |

| Faculty of Advocates | http://www.advocates.org.uk/ |

| HMRC crackdown on barristers | http://www.bbc.co.uk/news/business-19635051 |

15 ways to improve profitability

Profit is vital to every business, what is the point of being in business if you don’t make a profit?

So here are my tips on how to improve your profitability:

- Weed out loss making products, clients and departments – concentrate on high margin products and services

- Reduce Employment Costs – use Freelancers instead of Permanent Employees where appropriate

- Use Virtual Communication Technology – meetings can be held over the internet with Skype or other systems, it will cut traveling time and costs

- Use Social Media and Networking – marketing can be costly and the results can be hard to measure, use your contacts to generate leads and sales and always ask for referrals

- Increase Productivity – eliminate wasteful and unnecessary processes, I was told it used to take 17 people in the NHS to change a light bulb on a hospital ward (requisitions, approvals, payments, changing the bulb…) the solution to cut wasted processes was to keep a stock of bulbs on the ward

- Negotiate with suppliers – always look at ways to reduce cost including using alternative suppliers

- Understand your clients requirements – the client knows what he wants and what represents value, if you deliver value you will get more business

- Seek add on sales – what other products or services might be useful to your existing clients

- Keep an eye on your competitors – competitor analysis will enable you to understand differences in price, distribution, market and demand

- Find New Markets – use market research to expand into new areas

- Decrease Overheads – analyse all of your overheads including Rent, Rates, Utilities – could you sub-let part or your premises or reduce waste

- Reduce Stock Levels – can you turnover your stock more quickly or buy to order

- Improve your Cash Cycle – reduce slow payment by debtors, invoice promptly and settle disputes quickly

- Invest in Technology – automate processes with ERP systems

- Use Key Performance Indicators – KPI’s help you achieve your goals

steve@bicknells.net

10 reasons why UK Micro Businesses are taking off

New analysis from Direct Line for Business (DL4B), based on data from the Office for National Statistics (ONS), reveals that just over half of all UK small firms are run from the home of the business owner.

The findings show that there are currently 2.5 million home-based business owners in the UK, representing just over half (52%) of the total number of UK SMEs. These home-based business owners now account for 8% of the UK’s total workforce.

The largest concentration of all is in Herefordshire – where 27% of the county’s 92,000 total workforce is a home-based business owner. Pembrokeshire is second with 23% and Eastbourne is third with 20%.

Men are more than twice as likely as women to run their own business from home, with 1.7 million male home business owners across the country, compared to around 818,000 female home business owners.

http://www.itdonut.co.uk/news/it/most-small-firms-are-now-home-based-businesses

Small businesses are a vital part of the UK economy.

Marketing Donut reported this week that a study of UK small businesses has shown a rise in the number of people setting up micro businesses and hiring people for part-time work.

The study by Freelancer.co.uk assessed 300,000 businesses over the past 12 months and it concludes that an entrepreneurial boom is taking place in the UK, with significant numbers of people starting up new ventures across the country.

According to the study, Brighton and Newcastle have seen the highest growth in the number of new micro businesses being launched (up by 24%), followed closely by Manchester and Southampton with 23% growth. London has seen 21% growth, Edinburgh and Liverpool 20%, Birmingham 19% and Sheffield 8%.

The research also shows that there have been positive knock-on effects for freelance workers in business support sectors, such as website design. It found there has been a 19% increase in the number of micro businesses commissioning new ecommerce websites.

In addition, orders for shopping carts to be installed on new small business websites are up 18%, email marketing is up 20%, graphic design is up 12% and logo design is up 6%.

So why are micro businesses taking off:

- You can start off working at home

- Your start up costs are low

- You can do it part time when it suits you

- With wages frozen and costs rising it can provide a useful additional income

- Its easy to be price competitive with low overheads

- The Internet makes it easy to sell your goods and services

- Your social capital can be used to generate sales ie use your contacts and connections

- There could tax advantages – employees generally pay more tax than sole traders

- Some clients prefer the personal touch

- It could be start of something big

steve@bicknells.net