Home » Self Assessment (Page 2)

Category Archives: Self Assessment

Are you one of the third of workers with a part time business?

Almost a third of British workers run some kind of creative business outside their main job contributing an estimated £15bn to the UK economy, according to new research from Moo.com. Profitability among this group of enterprises has increased by 32% in the past year. One in ten part-time creative entrepreneurs plans to leave their job to focus on their business full-time within the next year. However, 60% said it was their passion for the business, and not making money, that motivated them. The most popular part-time creative ventures are in food and cooking, gardening, photography and knitting. (According to Law Donut)

So why are micro businesses taking off:

- You can start off working at home

- Your start up costs are low

- You can do it part time when it suits you

- With wages frozen and costs rising it can provide a useful additional income

- Its easy to be price competitive with low overheads

- The Internet makes it easy to sell your goods and services

- Your social capital can be used to generate sales ie use your contacts and connections

- There could tax advantages – employees generally pay more tax than sole traders

- Some clients prefer the personal touch

- It could be start of something big

Here are my top 20 home based business ideas:

- Get a lodger – Under rent-a-room a taxpayer can be exempt from Income Tax on profits from furnished accommodation in their only or main home if the gross receipts they get (that is, before expenses) are £4,250 or less

- Ironing and Laundry Services – Always popular and you can start with friends and family

- E Bay Trading – as E Bay say… The first task is to sort through those bulging drawers and messy cupboards, finding stuff to flog. Get a big eBay box to stash your wares in, and systematically clear out wardrobes, DVD and CD piles, the loft and garage. Use the easy 12-month rule of thumb to help you decide what to offload: Haven’t used it for a year? Flog it.

- Blogging – Blogging has taken off and many businesses are looking for people to write blogs for them

- Candle Making – You can sell the candles on line and its easy to buy the wax and things you need to make the candles

- Car Boot Sale – As with E Bay but without going on line

- Cake Making – Make sure everything is labelled correctly and you comply with Health & Safety issues

- Data Entry – The internet makes it easy to enter data from where ever you are

- Social Media – Similar to blogging, businesses need help to manage Twitter, Facebook and Linked In

- Website Design – If you have the expertise, go for it

- Sales Parties – Cosmetics to Ann Summers, there is a long list of opportunities

- Sewing and Clothes Alterations – Perfect before and after Christmas

- Jewellery – Making and selling jewellery is always popular and great for Christmas presents

- Car Repairs – Assuming you have the skills needed and comply with legal requirements

- Pet Care – Walking dogs or grooming is popular

- Virtual Assistant – Also personal organiser or personal shopper

- Wedding Planner – You could start by creating a blog about your expertise

- Direct Sales – For example http://www.netmums.com/back-to-work/working-for-yourself/direct-selling-opportunities

- Computer Repair – Great provided you have the skills

- Marketing – Telesales to leaflet design and freelance writing

steve@bicknells.net

Are Cruise Ship Entertainers Employees?

If they weren’t on cruise ships HMRC would probably argue that they were employees but in the case of cruise ships they argue the opposite.

Pete Matthews (1) Keith Sidwick (2) v Revenue & Customs [2011] UKFTT 24 (TC)

Mr Sidwick was a musician and played piano on a series of cruise ships. Mr Matthews was a juggler, similarly entertaining passengers on cruise ships. Both were subject to a close degree of control by the ships officers but the First-tier Tribunal found that this degree of control was required by the context of a cruise ship.

The First-tier Tribunal concluded that the entertainers were not employees ‘…but earn their living by entering into a series of separate engagements with a number of different cruise lines in a similar way to actors…’

The reason why HMRC argued against employment was to stop a claim for Seafarers Earnings Deductions.

To get the deduction you must:

- work on a ship. Oil rigs and other offshore installations aren’t ships for the purposes of Seafarers’ Earnings Deduction – but cargo vessels, tankers, cruise liners and passenger vessels are

- work all or part of the time outside the UK. This means that for each employment you must carry out duties on at least one voyage per year that begins or ends at a foreign port

- be resident in the UK or resident for tax purposes in a European Economic Area (EEA) State (other than the UK) – find out more by following the link ‘Check your residence status’ in the section below

You get the deduction from your earnings as a seafarer if you have an ‘eligible period’ of at least 365 days that consists mainly of days when you are absent from the UK.

From 6 April 2013 the rules that determine if someone is resident in the UK for tax purposes have been put on a statutory basis. These rules are known as the Statutory Residence Test (SRT).

steve@bicknells.net

What are the differences between employees and contractors?

According to figures released by the Office for National Statistics last week, self-employment is at its highest level since records began almost 40 years ago.

There are currently 4.6 million people self-employed, with the proportion of the total workforce that are making a living for themselves sitting at 15%, compared to 13% in 2008 and less than 10% in 1975.

As highlighted by Everreach and the Daily Mail.

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

steve@bicknells.net

Simple Tax – a great way to file your return

I read about Simple Tax in an article in the Express…

Backed by venture capital investors including EC1 Capital, Seedcamp and Charlotte Street Capital, SimpleTax was set up to help customers find ways to save money on their tax bills and file returns online with HMRC in minutes.

SimpleTax’s users have so far cut a total of £2.5 million from their tax bills

So I tried it out, it’s great and it’s free.

You will need your HMRC Online filing details if you want to file your return alternatively you can just print out the return.

For taxpayers who have very straightforward returns Simple Tax should make it quicker and easier to complete and file online.

As you prepare the return Simple Tax gives you tips on things you can claim and ways to save tax.

Take a look and see what you think https://www.gosimpletax.com/

For those with more complicated tax returns get advice from a CIMA Accountant.

steve@bicknells.net

We love Self Employment in UK…..

The UK has seen the fastest growth in self-employment in Western Europe over the past year, according to the Institute for Public Policy Research (IPPR).

The number of self-employed workers rose by 8%, faster than any other Western European economy, and outpaced by only a handful of countries in Southern and Eastern Europe.

The IPPR’s analysis shows that the UK – which had low levels of self-employment for many years – has caught up with the EU average. If current growth continues, it says, the UK will look more like Southern and Eastern European countries which tend to have much larger shares of self-employed workers.

According to Tax Research UK…

Something like 80% of all the new jobs created since 2010 are, in fact, self-employments, and there are a number of things that very significantly differentiate self-employments from jobs.

The first is security: there is none.

The second is durability: vast numbers of new small businesses fail, which is one reason why I doubt the official statistics. I am sure they record the supposed start-ups correctly but seriously doubt if they have properly counted the failures.

Then there is the issue of pay. The evidence is overwhelming that in recent years earnings from self-employment have, on average, declined significantly.

A worker’s employment status, that is whether they are employed or self-employed, is not a matter of choice. Whether someone is employed or self-employed depends upon the terms and conditions of the relevant engagement.

Many workers want to be self-employed because they will pay less tax, this calculator gives you a quick comparison between being employed, self employed or taking dividends in a limited company.

HMRC have a an employment status tool to help you determine whether a worker can be self-employed or should be an employee http://www.hmrc.gov.uk/calcs/esi.htm

In summary, why is it attractive to use Self Employed Freelancers?

- Skill is more important than location in many business sectors – we live in world where internet can allow you to work with anyone at anytime, you can now track down the best person to work with even if they live thousands of miles away

- Lower fixed costs – Using Freelancers will lower your fixed costs (in similar way to Zero Hours Contracts), you employ them for a specific project and only pay for what you need so there isn’t any surplus capacity

- Tax advantages – Freelancers run their own business and that means they pay less tax than employees. Employers save tax too, such as Employers NI.

- Competitive Advantage – You can put together a team for a contract rather than finding contracts that fit your workforce, this means you can hire the best.

- 110% Commitment – A Freelancers success and future work depends on them performing to the highest level on every contract, failure is not an option for a successful contractor.

So do you think self employment is good for the UK?

Don’t forget your 31 July Payment on Account!

The 31 July 2014 is the date that you should make your second payment on account to HMRC.

For example on 31 July 2014, you’d make your second payment on account for the 2013-14 tax year.

From the 31 July you will have to pay interest on anything you owe and haven’t paid, including any unpaid penalties, until HMRC receives your payment.

As well as the 4.54 million self-employed people in the UK, higher rate taxpayers, company directors and anyone with more than one income are required to make a payment on account – part of their annual tax payment.

Don’t forget to pay!

steve@bicknells.net

Do you have a Second Income? own up now!

On the 9th April 2014 HMRC launched the Second Income Campaign….

A second income could come from:

- consultancy fees, eg for providing training

- organising parties and events

- providing services like taxi driving, hairdressing or fitness training

- making and selling craft items

- buying and selling goods, eg at market stalls or car boot sales

You need to tell HM Revenue and Customs (HMRC) if your additional income hasn’t been taxed through either:

- your main job

- another Pay As You Earn (PAYE) scheme

- Self Assessment

This is called a ‘voluntary disclosure’. To get the best possible terms you need to tell HMRC that you want to take part in the campaign.

You’ll have 4 months to calculate and pay what you owe.

You can find out about the campaign and how to make a disclosure here

The criteria used to assess if an activity is a hobby or a business are:

- The size and commerciality of the activity.

- The frequency of the activity and transactions

- The application of business principles.

- Whether there is a genuine profit motive.

- The amount of time devoted to the activities.

- The existence of arm’s-length customers (as opposed to just selling your wares to family and friends).

If you have a Second Income its better to disclose it now rather than wait till HMRC find you.

Limited Liability Partnerships

Limited Liability Partnerships came under closer scrutiny in the Budget 2013. The aim is to target LLPs which use the structure to hide the employment relationship of the partners and those with Corporate partners who divert business profits to the corporate partners in order to avoid tax.

Although the following measures come in to play from 6th April this year, the anti-avoidance measures make it effective from 5th December 2013. This is to prevent partnerships changing their arrangements in order to avoid the new rules.

The two main areas of focus are salaried or fixed profit share partners which is referred to as disguised employment, and profit and loss sharing arrangements within mixed partnerships.

LLP partners with fixed profit share

HMRC believe that many members of an LLP should be taxed as employees, because they don’t see them is true partners.

A new test has been brought in which has three conditions. Where the member tested meets all three conditions then he or she must be treated as an employed salaried member and be brought within the PAYE system with tax and class I NIC applied to any earnings, which had previously been Taxed as profit share.

This also means that if a vehicle is provided for the members use by the partnership this will be taxed as a benefit in kind. As such the member will have to pay tax and NIC and the LLP will have to pay Class 1a NIC on the benefit.

HMRC does actually accept that employment tax rules are imposed on the individual but that in fact the individual has no employment rights. This is because he is not actually an employee for employment law purposes.

The test is as follows. The provision is triggered when all conditions A to C are met:

Condition A: The Member is performing services for the LLP in his capacity as a member of the partnership and it’s reasonable to expect as a result of these arrangements that any amounts paid to him in respect of his services will be wholly or substantially wholly a disguised salary. In other words if his reward package is comparable to that received by an employee, either a fixed salary or a variable bonus based on performance rather than profit share.

Condition B: The Member doesn’t have significant influence over the affairs of the partnership.

Condition C: The Member’s capital contribution to the LLP is less than 25% of the total amount of his disguised salary which would be expected to be paid in the relevant tax year by the LLP in respect of the members performance of services as a member. Normally the relevant time would be the beginning of the new tax year.

These tests must be reviewed each tax year.

Corporate LLP Members

This applies to partnerships who have members which are not subject to UK income tax for example this might be a limited company. The problem here is that HMRC believes these structures are used to avoid tax on a very large scale. Where for example an individual member introduces his Ltd company as a corporate member, and which then receives a profit share that would otherwise have been paid to the individual member. If the Member then has the power to enjoy the fund which had been paid to his company then:

- The individual member will be treated as a salaried member.

- The amount paid to the company will be treated as employment income paid to the individual member.

There are anti-avoidance rules are in place to catch anyone trying to put measures in place to counteract these new rules.

fiona@grant-jonesaccountancy.com

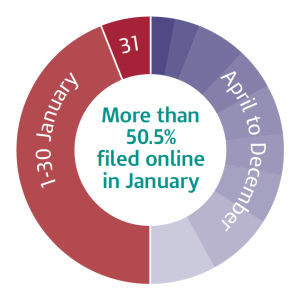

How did you get on with Self Assessment?

According to the Government…

This year, a record-breaking 8.48 million returns were filed online, representing 84.5% of all returns received. This meant that, of the 10.74 million tax returns due for the tax year 2012 to 2013, 93.4% met the SA deadlines for paper and online filing.

On 31 January we saw a final rush to file, with 569,847 online returns coming in on time – the highest percentage ever recorded. It shows that many of you and SA taxpayers now prefer to use our digital service, over paper.

How did you find self assessment, was it easy or nightmare?

steve@bicknells.net

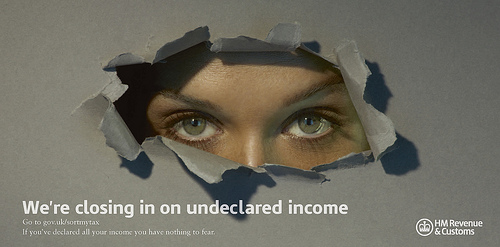

How HMRC use IT systems to seek out tax evaders

There is no doubting the resolve of HMRC to track down and prosecute tax evaders.

The Government has committed to spend £917m to tackle tax evasion and raise an additional £7bn each year by 2014/15.

HMRC are using 2,500 staff to tackle avoidance, evasion and fraud, there is also a website to help those who want to declare income https://www.gov.uk/sortmytax

In the search for tax evaders, HMRC have a £45m computer system called Connect which in 2011 delivered £1.4bn in tax revenue and the system is getting bigger and better all the time. According to Accounting Web:

It uses a mathematical technique to search previously unrelated information and detect otherwise invisible ‘relationship’ networks. Using Connect, HMRC sifts through information on property transactions at the Land Registry, company ownerships, loans, bank accounts, employment history, voting and local authority rates registers and compares with self-assessment records to spot taxpayers who might be under-declaring or not declaring income.

Last year Connect made links between tax records and third party data from hospitals, pharmaceutical companies, insurers and even gas SAFE registrations. DVLA records and the shipping and Civil Aviation Authority registers help identify owners of cars and planes who declare income that the computer suggests cannot support such purchases.

In addition HMRC have also identified 200 accountants, lawyers and professionals who advise on tax avoidance structures and its currently unclear how HMRC will be dealing with them and their clients.

It is important to remember that most people pay the correct tax, in fact HMRC calculate that 93% of tax due is paid correctly, its only a small minority who try to evade tax.

steve@bicknells.net